The release of Asana’s (NYSE:NYSE:ASAN) Q2 report, in conjunction with the news of a $350M investment by Dustin Moskovitz [CEO], was met with investor cheers as the stock rallied ~25% in a single session. While Asana’s Q2 report represented a beat on the top and bottom lines, Asana’s growth is decelerating, and Q3 guidance was, let’s say, lukewarm. And this is why I believe that Dustin’s decision to double down on Asana is what’s driving the significant jump in Asana shares. Now, I understand that Dustin is a multi-billionaire, and he could easily afford to make such an investment. However, $350M is a massive capital allocation in a liquidity-constrained market (even for Dustin), and hence, I see it as a big vote of confidence in Asana.

In this note, we will analyze Asana’s Q2 report, assess its liquidity situation, determine its fair value, and test it under TQI’s Quantamental analysis process. We have a lot to cover, so let’s just get started!

Breaking Down Asana’s Q2 Report

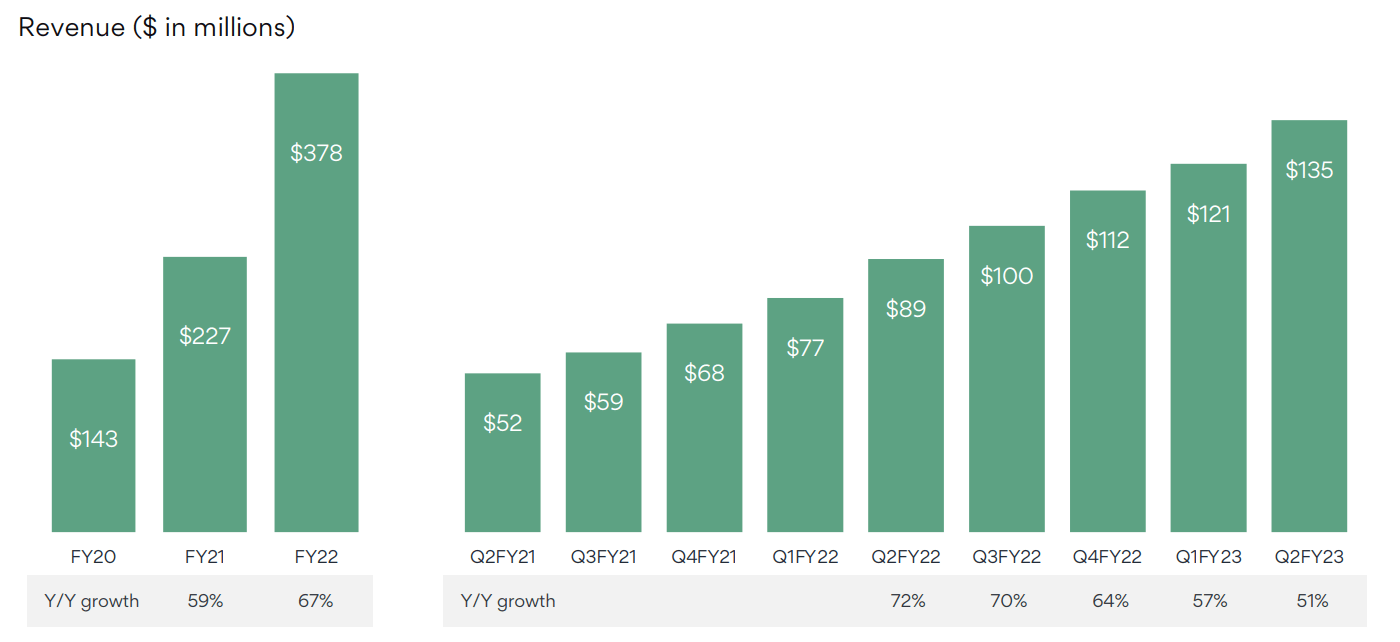

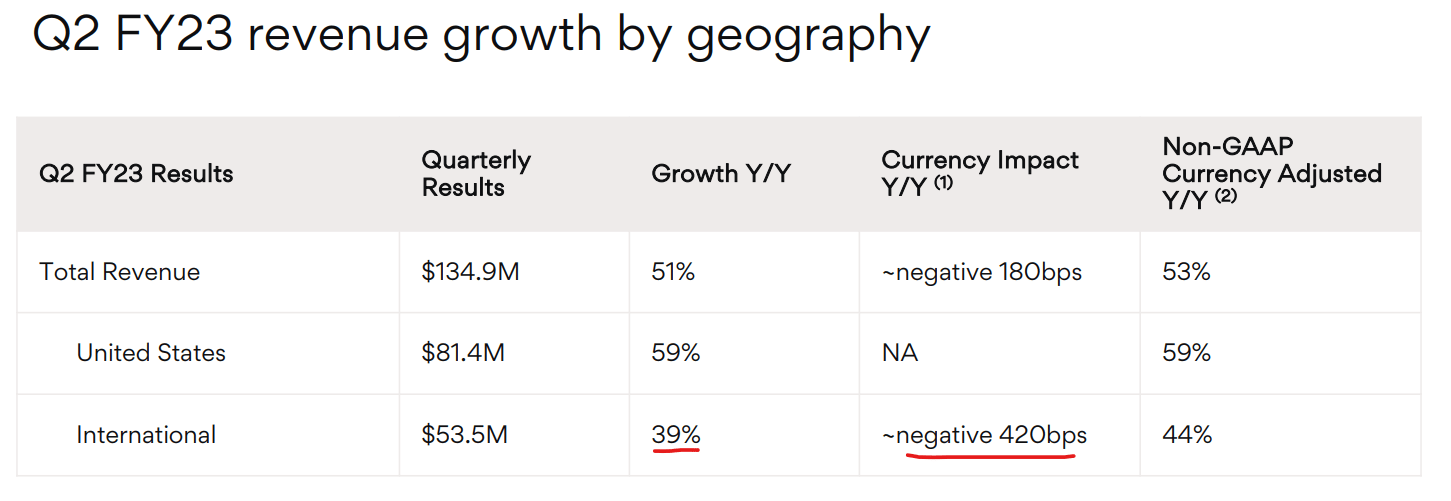

In Q2 FY-2023, Asana reported revenue of $135M (up 51% y/y), with a strong performance in the United States being somewhat offset by currency impact in the International markets (negative 420 bps impact on growth). These results represented a top-line beat of ~6%.

Asana Q2 FY2023 Investor Presentation

Asana Q2 FY2023 Investor Presentation

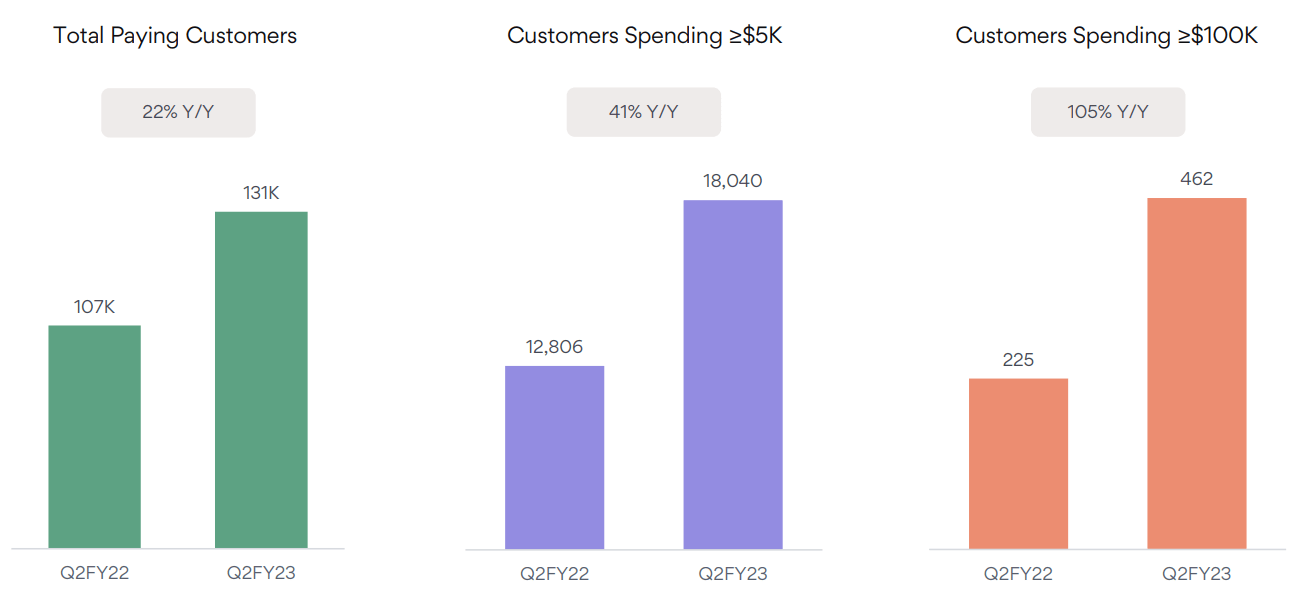

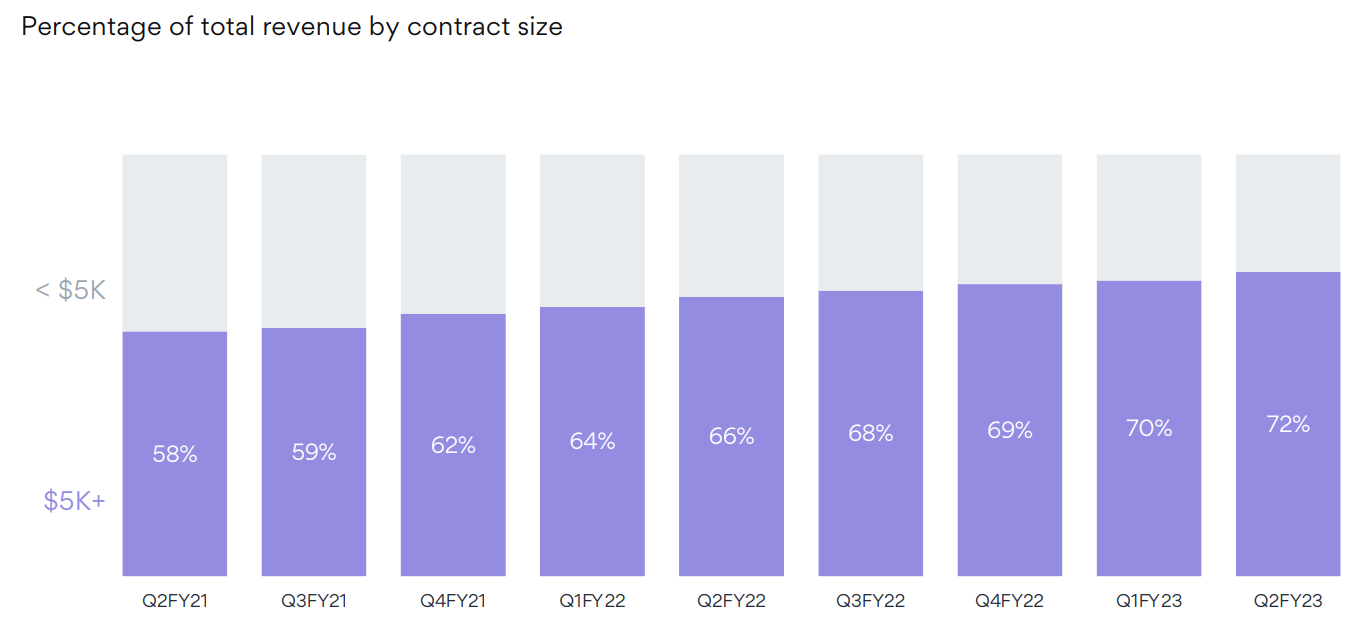

As you may have noticed, Asana’s revenue growth has been decelerating in recent quarters. While a larger revenue base is a significant driver of this deceleration, Asana is up against a challenging macro environment. In Q2, Asana’s Total Paying Customer count went up just 22% y/y; however, Asana’s move upmarket is a saving grace for the company. With more prominent customers, Asana’s deal size is getting larger.

Asana Q2 FY2023 Investor Presentation

Asana Q2 FY2023 Investor Presentation

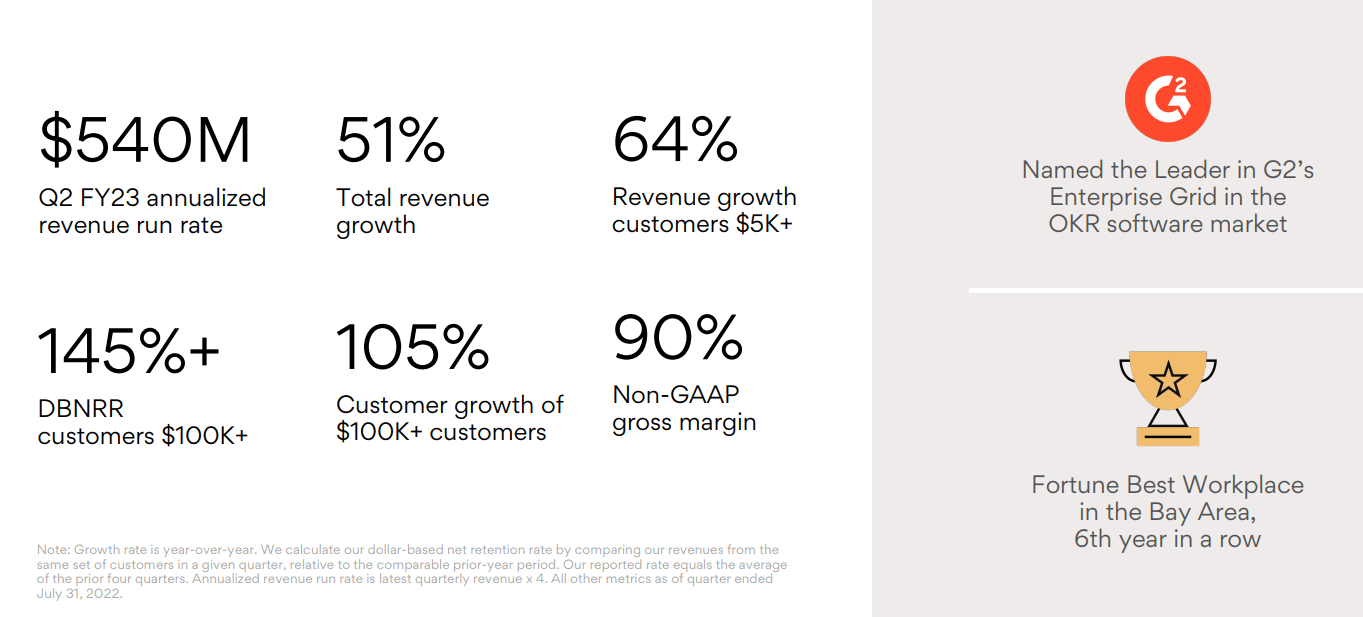

And so far, Asana’s platform has proven itself to be even stickier among enterprise customers than SMBs, as evidenced by Asana’s dollar-based net retention rate of more than 145% for customers spending >$50K.

Asana Q2 FY2023 Investor Presentation

Asana Q2 FY2023 Investor Presentation

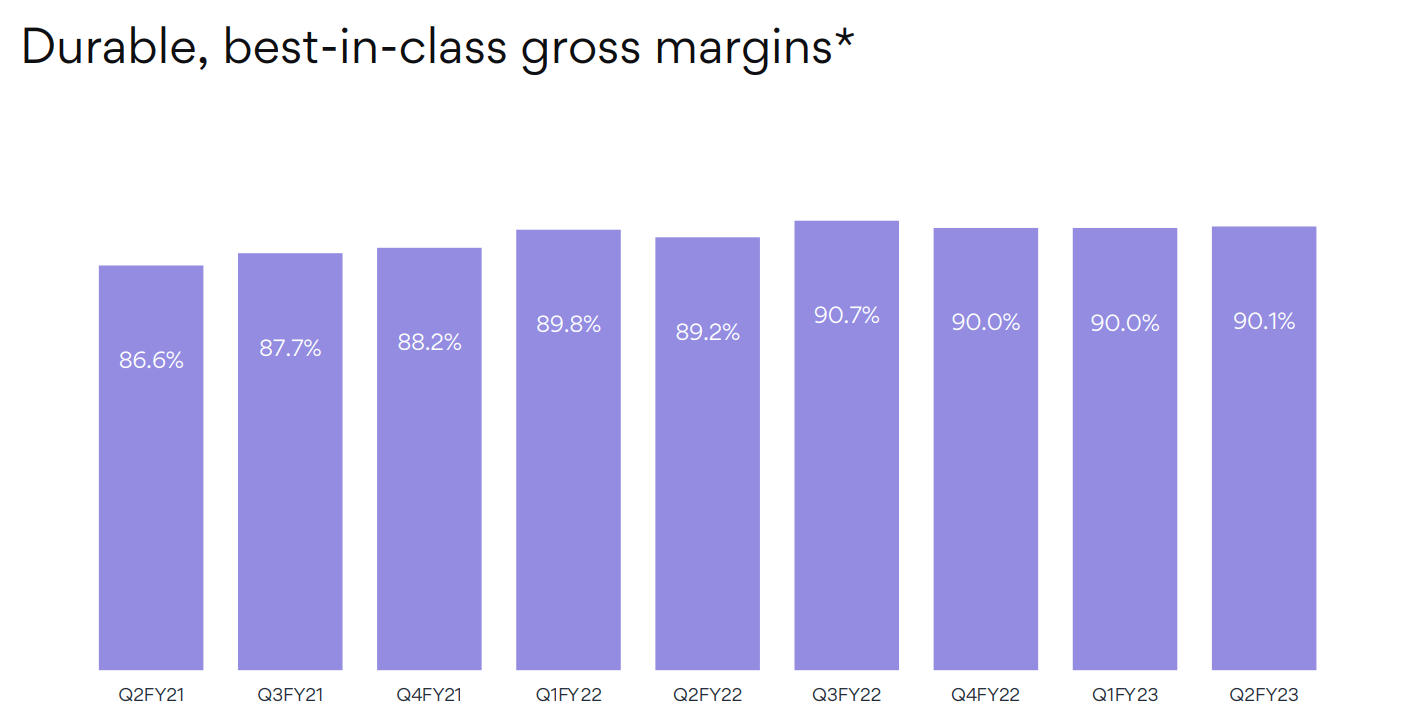

Despite Asana’s highly-differentiated products commanding best-in-class gross margins of ~90%, Asana’s operating losses are getting wider as the company reinvests aggressively into Research & Development and Sales & Marketing (frontloaded to the first half of this year according to management).

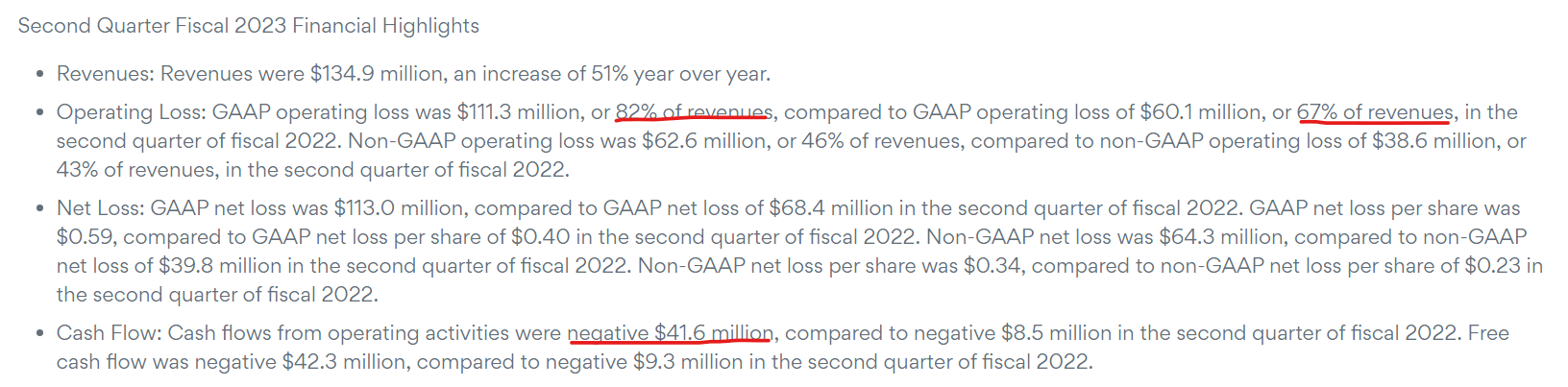

Asana Q2 ER Press Release

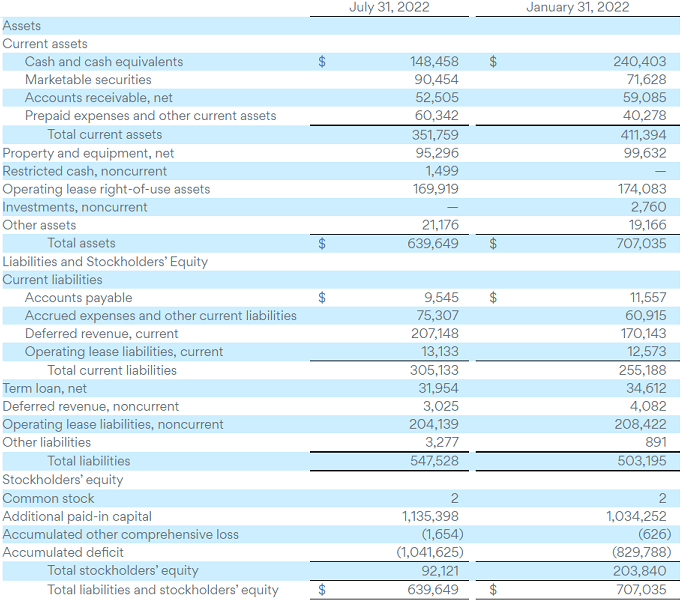

In Q2 alone, Asana recorded a negative free cash flow of ~$41.6M. With revenue growth set to decelerate further in the second half of this year, Asana’s losses could get bigger, and suddenly, Asana’s financial position was looking tricky (with only ~$250M of cash & investment left on the balance sheet after Q2).

Asana Q2 ER Press Release

Asana Q2 ER Press Release

Having a multi-billionaire as a Co-Founder and CEO is a dream for every young, high-growth business, and for Asana, this dream is a reality!

Dustin To The Rescue

With its cash burn rate, Asana seemed to be facing a liquidity crunch (less than 4-5 quarters of cash left), and Dustin Moskovitz dipped into his deep pockets and bankrolled the company with an additional $350M by buying ~19M shares from the company at $18.16 per share via a private placement.

Boom! Problem solved, crisis avoided!

Here’s what Dustin had to say on the investment:

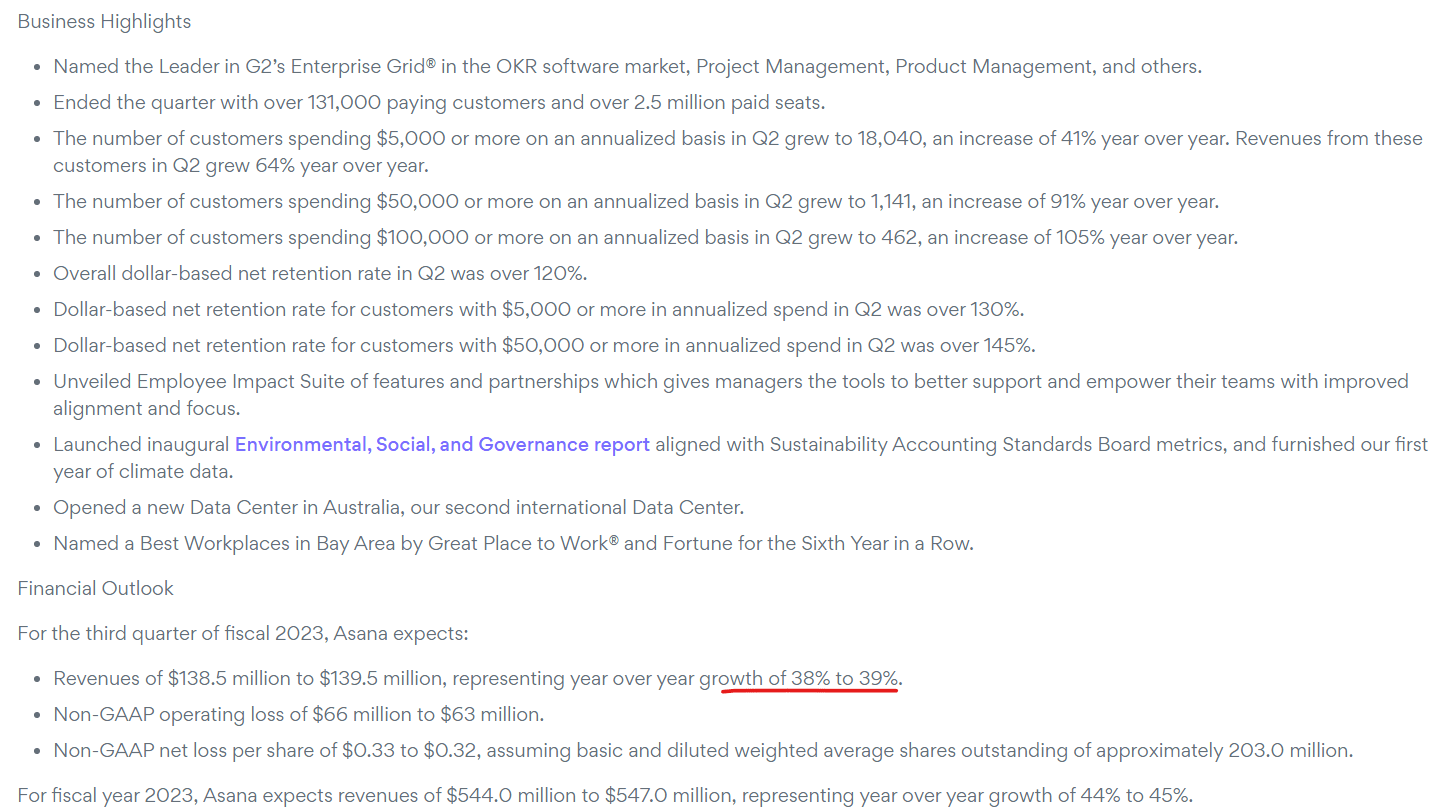

This quarter we beat our revenue guidance by 6 percent and non-GAAP operating loss guidance by 14 percent. Growth was driven by large enterprise deals and momentum in the US, with the number of customers spending $100,000 or more on an annualized basis up 105 percent. We believe that Asana is the most scalable work management platform out there, as evidenced by our broad deployment and millions of users worldwide, including our largest customer deployment of over 100,000 paid seats.

I am investing further in Asana because I strongly believe the market opportunity is enormous and that the Work Graph is the best possible solution for helping enterprises achieve their most important goals.The market is ready and our customers are validating our strategy every day. With the additional $350 million in capital announced today, we believe we are fully-funded to execute on our current strategies and well-positioned to reach free cash flow positive before the end of calendar 2024.

Dustin’s vote of confidence has mitigated the liquidity risk brewing at Asana due to decelerating growth and widening operational losses. Hence, Asana’s stock is getting re-rated.

Now, let’s analyze Asana using TQI’s Quantamental analysis process.

Running Asana Through TQI’s QA Process

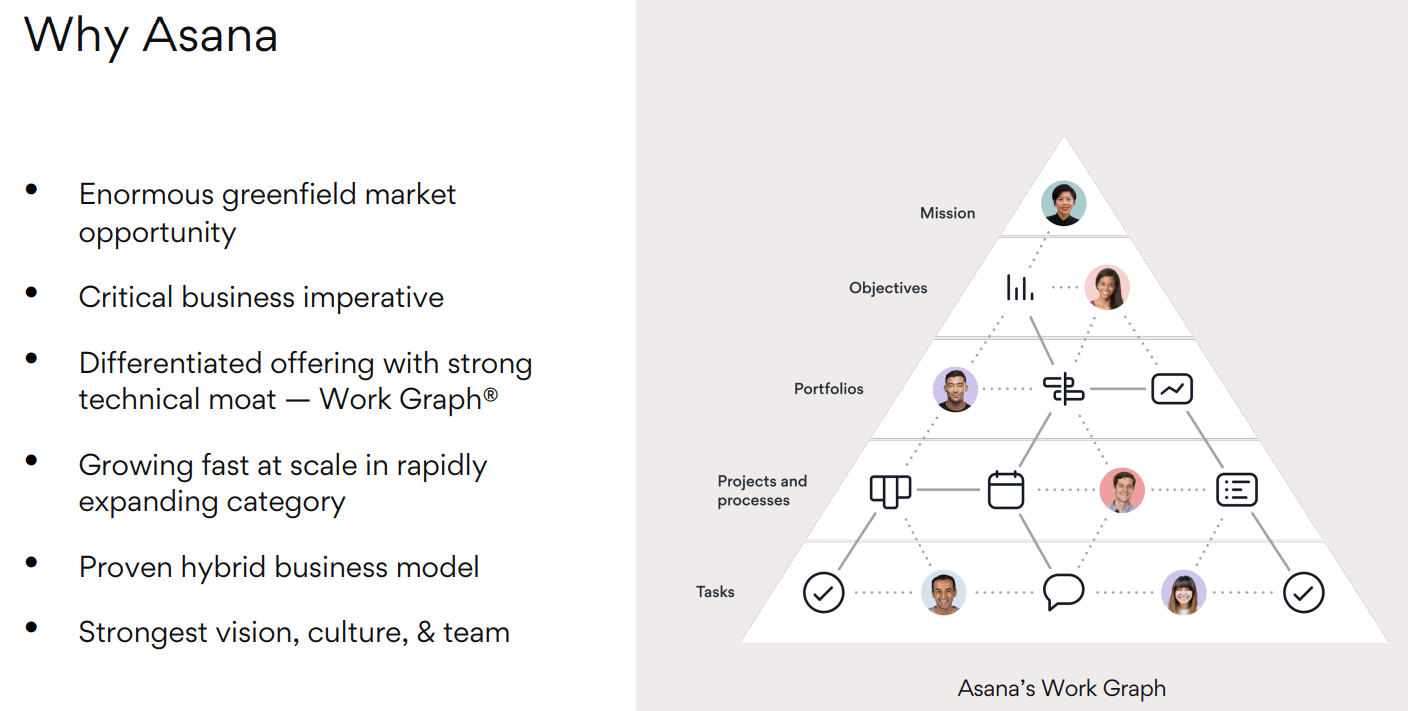

Asana’s modern work management platform is powered by its proprietary Work Graph technology developed by co-founders Dustin Moskovitz and Justin Rosenstein, who met during their time at Facebook (META). Today, more than 131K organizations use Asana to boost collaboration and productivity among their workforce.

Asana Q2 FY2023 Investor Presentation

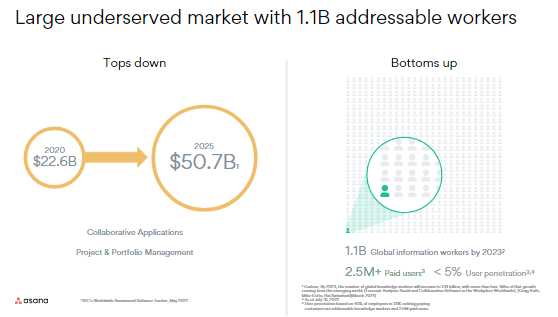

While work management and collaboration software tools are aplenty, Asana is carving out a special place for itself in the market. Currently, Asana’s market share (measured by ARR [$540M] divided by TAM [$22.4B]) is just about 2.4%. In addition to growing its market share, Asana’s TAM itself is set to expand from $22.6B to $50.7B by 2025. Hence, Asana has a tremendous greenfield opportunity to drive future growth.

Asana Q2 FY2023 Investor Presentation

As of Q2 FY2023, Asana is running at an ARR of $540M and delivering rapid growth (~51% y/y) at scale with robust customer retention (DBNRR > 145% for customers with ARR > $100K, and overall NRR > 120%). Asana is moving upmarket, and this shift towards larger enterprise customers could propel the company towards profitability.

Asana Q2 FY2023 Investor Presentation

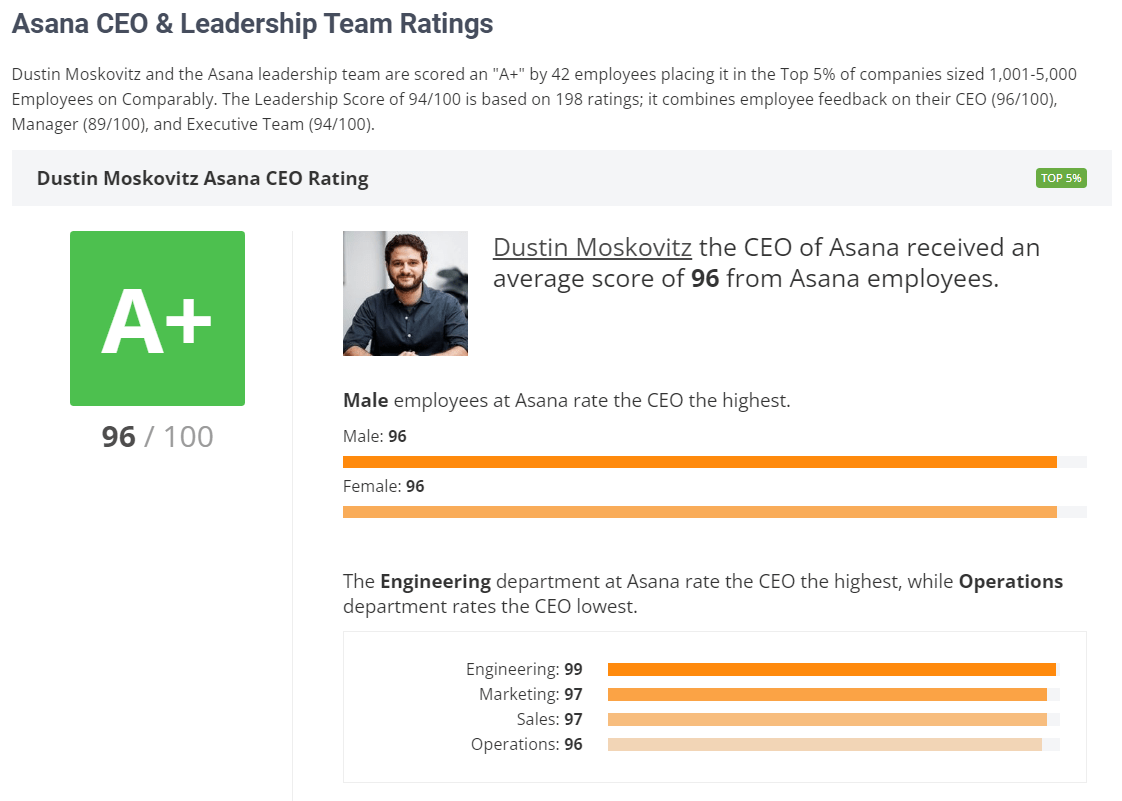

According to data from Comparably, Dustin is a highly-rated CEO. Furthermore, Asana has received multiple awards for its workplace culture, such as the ‘Fortune Best Workplace in the Bay Area’ [6 years in a row].

Comparably

As you may know, Dustin was one of the co-founders [first CTO] of Facebook, and he is a multi-billionaire. Asana is his baby, and Dustin’s confidence in Asana’s future was once again on full display as he bankrolled the company with additional capital of $350M last week [through a purchase of ~19M shares via a private placement]. And this is after him buying up shares worth ~$700M from the open market across the last twelve months. Clearly, Dustin is doubling down on Asana, and that’s a very encouraging sign.

From a fundamental perspective, Asana is still an early-stage growth company with a massive TAM opportunity. The business is growing rapidly at scale, with robust margins indicating a differentiated and highly-valued product. So far, Asana has proven its land-and-expand GTM strategy. As the company moves upmarket into the enterprise market, its economics are set to improve over the coming quarters and years. With a visionary & dedicated leader at the helm and a strong workplace culture, Asana’s long-term business fundamentals are robust.

Asana Q2 FY2023 Investor Presentation

Now, let’s take a look at some quantitative data and technical charts.

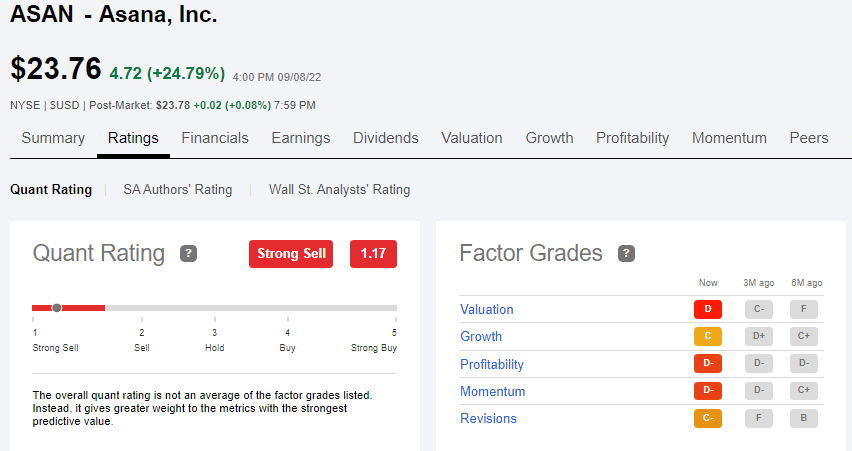

According to Seeking Alpha’s Quant Rating system, Asana is rated a “Strong Sell” with a score of 1.17/5. While a lack of profitability and negative share performance warrant the “D-” rating for Profitability and Momentum, I don’t think Asana’s y/y growth of 50%+ deserves a factor grade of “C” on Growth. After all, Asana is one of the fastest-growing software companies out there. With that said, Asana’s growth rates are decelerating, and operational losses are widening, which means a “C-” grade for Revisions is palatable. On Valuation, Asana is rated a “D”, but its EV/S multiple of 10.28x is not excessive in my view.

SA Quant Rating

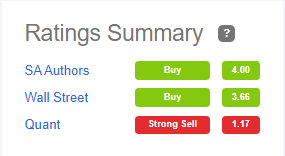

Clearly, quant factor grades are not in favor of Asana right now, which means a short-term position is unfathomable. Despite a poor quantitative rating, Asana is rated as a “Buy” by SA Authors and Wall Street analysts.

SA Quant Rating

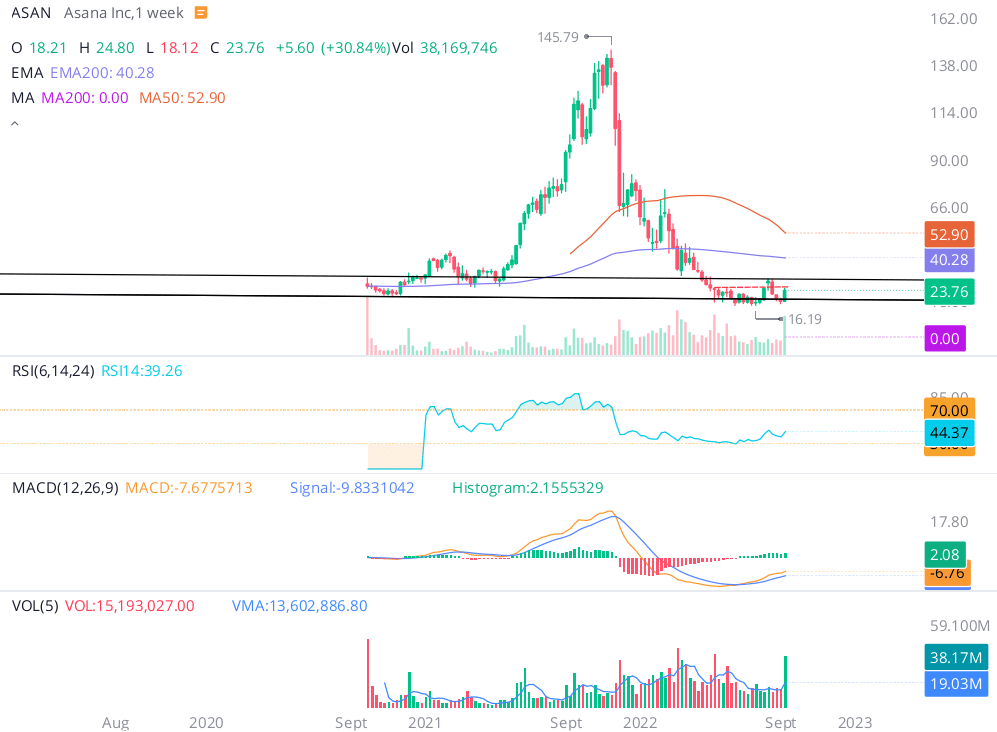

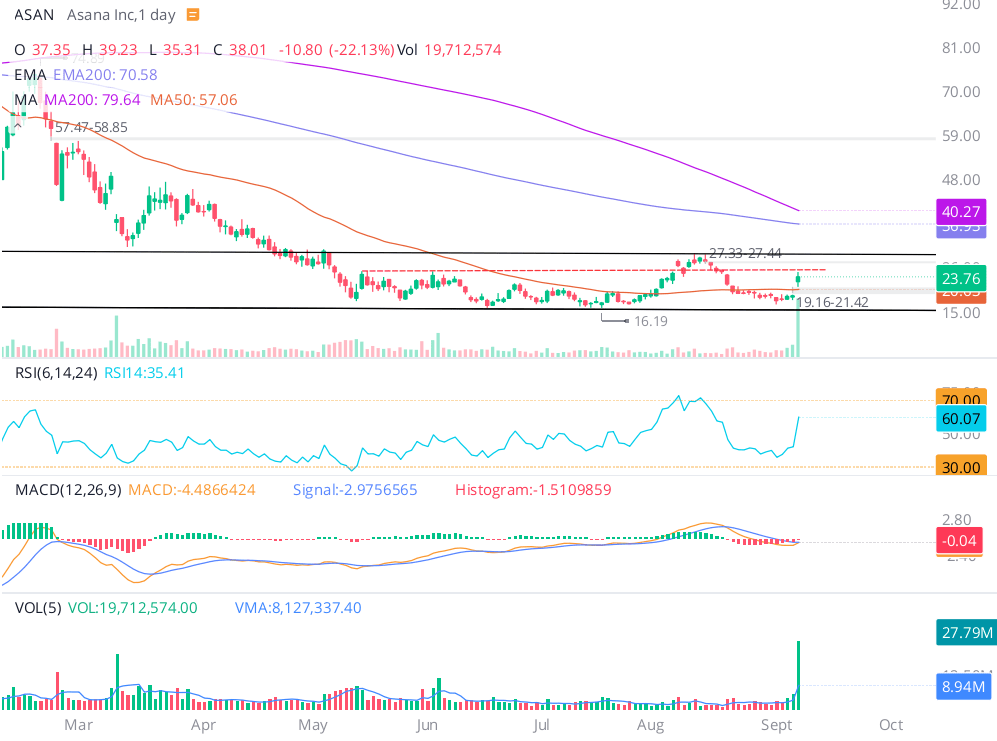

Asana has a relatively short trading history as a public company; however, it has been a complete roller coaster. After its IPO at $21, Asana’s shares headed to the mid-teens. Hype followed Asana’s robust growth in 2021, with the stock peaking at $145.79 (~90x EV/S) in early November. However, FED’s pivot pricked the bubble in Asana (along with many other high-growth tech stocks). After months of sell-off, Asana is back to where it started its journey as a public company, and it is showing signs of stabilization in a tight range around its IPO price.

WeBull Desktop

As you can see below, Asana’s stock has been forming a base in the $16-25 range over the last few months. Interestingly, Asana’s IPO price was $21, which happens to be right in the middle of this base. After the withdrawal of liquidity risk, Asana’s stock has bounced up from the lower end of this range, and this rally could extend up to $27.5 in quick order.

With the stock getting closer to its fair value, we might just stay in the base for the next few weeks. I don’t know what the stock is going to do, but decelerating growth and widening losses do not support an upside breakout move in the near term. However, if we do get a breakout, Asana’s rally could extend up to the mid-40s.

WeBull Desktop

I recently analyzed Opendoor (OPEN) post its Q2 results with the stock making a sharp move up from the lower end of its own base (trading range) [similar to what we see with Asana]:

Opendoor’s technical setup is getting interesting – a breakout from the base here could take the stock up to $8-10 in a jiffy. While Opendoor’s Q2 results were good, the bounce is likely a result of the announcement of the Zillow partnership, and a news-based rally can fade off fast.

Twitter

Since Opendoor failed to get past resistance at $5.7-5.8 during Friday’s session, the breakout is not confirmed, and we may well break back into the base over the coming days. Hence, I am not convinced about a short-term trade here. However, I think the long-term risk/reward is simply fantastic, and investors should use the ongoing volatility in Opendoor to take/build long positions at these depressed levels.

Since this take was published, Opendoor’s stock has declined by ~14% (and it was down by ~30% at one point), breaking back into its base and testing the lower end of the base. A news-based rally can fade off quickly, especially if the impact of the news is uncertain and way out in the future. For Opendoor, the deal with Zillow is killer, but the rollout will take time, and the economics are, as of yet, unclear.

However, in the case of Asana, the news of the $350M private placement has created an immediate impact on the business by removing liquidity risk (at least for the foreseeable future). And this is why Asana’s stock has been re-rated higher, and hence, I don’t see this ~25% jump in the stock fading away anytime soon (primarily because Asana is still undervalued). That said, we are operating in a volatile market, and anything could happen. Asana is still trading within its base of $16-25, and unless we get a confirmed breakout above $27.50, we are likely to remain range bound for the foreseeable future. After this vertical move up, Asana’s stock might face resistance soon, and hence, I would just accumulate slowly.

In my view, weak quantitative and technical data render any short-term bets a bad idea. However, for long-term investors, this brutal sell-off in Asana’s stock is an opportune moment to build up a long position slowly.

Concluding Thoughts

Asana is a rapidly-growing, modern work management platform with a massive greenfield opportunity. While a challenging macroeconomic environment is causing a steeper-than-expected growth deceleration at the company, Asana’s CEO, Dustin Moskovitz, just purchased ~19M shares to add $350M of capital to the company’s balance sheet. With this infusion of cash, Asana has ample liquidity to ride through this tough period and get to free cash flow positivity.

Asana’s robust gross margins will enable the company to deliver operating leverage as the business scales up. While management’s FCF breakeven target timeline of CY2024 seems far-fetched at this point, with operating losses standing at ~82% of revenue in Q2 FY2023, it is not out of reach for a business with superb unit economics (Asana’s GM: 90%) and high stickiness (Asana’s NRR: 120%+).

After assessing Asana’s valuation and testing it through TQI’s Quantamental analysis process, I view it as a strong buy for long-term investors. As a short-term play (<12 months), investors are better off skipping Asana due to weak quantitative factor grades and a broken technical chart. I don’t have a crystal ball, and I am not sure where Asana’s stock will bottom out eventually (or if it has bottomed out already).

TQI’s valuation, 5-year price target, portfolio allocation, capital deployment, and risk management strategy for Asana are reserved exclusively for my marketplace subscribers. However, according to TQI Valuation Model, Asana is currently undervalued and deemed a strong buy based on expected returns. Despite a completely broken technical chart and poor quant factor grades, Asana’s business fundamentals render it a buy for the long-term. At TQI’s Moonshot Growth Portfolio, I built a 1% position in Asana on 2nd September at ~$18.2 per share, and I plan to continue to accumulate more shares slowly for the long haul over the next few months [despite this massive post-ER bounce of ~25% on Thursday].

Key Takeaway: I rate Asana a strong buy at $24 for long-term growth-oriented investors with an appetite for volatility.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment