Roman Tiraspolsky/iStock Editorial via Getty Images

V.F. Corporation (NYSE:VFC) is crawling into the new year following a disastrous 2022 where shares fell by more than 60%. Recognized as one of the world’s largest apparel manufacturers and specialty retailers, the setup here was significant inflationary cost pressures hitting earnings. The challenging economic environment also left sales underperforming while the company’s large balance sheet debt position didn’t help, which added to the equity weakness amid rising interest rates.

With the stock currently trading near a decade low, let’s recognize there are some real challenges and any turnaround won’t be easy. That being said, one silver lining has been encouraging recent reports out of China, which is getting an economic boost as the authorities end its “Covid-zero” policies. This is important because the country represents a strategically important market for VFC, with the region a major culprit of the poor performance last year.

Over the next few quarters, we see room for VFC to benefit as China evolves into a growth driver, providing some upside to the latest guidance and consensus estimates. We are cautiously bullish on VFC, which is supported by a global brand footprint and underlying profitability.

VFC Key Metrics

The company last reported its fiscal 2023 Q2 earnings in late October with EPS of $0.73, down -34% year-over-year, but in line with previous management targets that had been revised lower since Q2. Revenue of $3.1 billion was down -4% y/y and was slightly below estimates, although the topline presented a 2% increase in constant currency terms. By this measure, FX volatility from a strong Dollar has also been part of the dynamic pressuring VFC results.

Rising input costs and logistical expense has been the culprit in the declining profitability reflected in an adjusted operating margin of 12.3%, down by 440 basis points compared to 16.7% in the period last year. Year-to-date adjusted EPS of $0.81 is down -40% from fiscal 2022.

Company IR

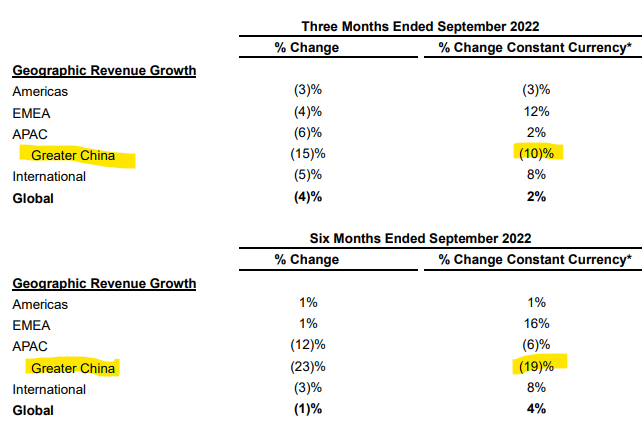

As mentioned, the trends in China were concerning through 2022. Compared to the Americas region, which delivered 1% sales growth over the last six months, and even a 16% increase in the EMEA region on a constant currency basis, the -19% decline in China stood out and dragged lower the firm-wide results. One strong point has been the momentum of “The North Face” brand with a 14% increase in constant currency globally, balancing a decline from “Vans” and “Dickies” which were particularly impacted by production issues from China.

Company IR

The situation in 2022 included an 8-week lockdown disrupting key suppliers along with retail shutdowns limiting store and wholesale channel availability to consumers. At the time of the Q2 earnings release, 7% of stores in China were closed compared to zero at the start of the quarter.

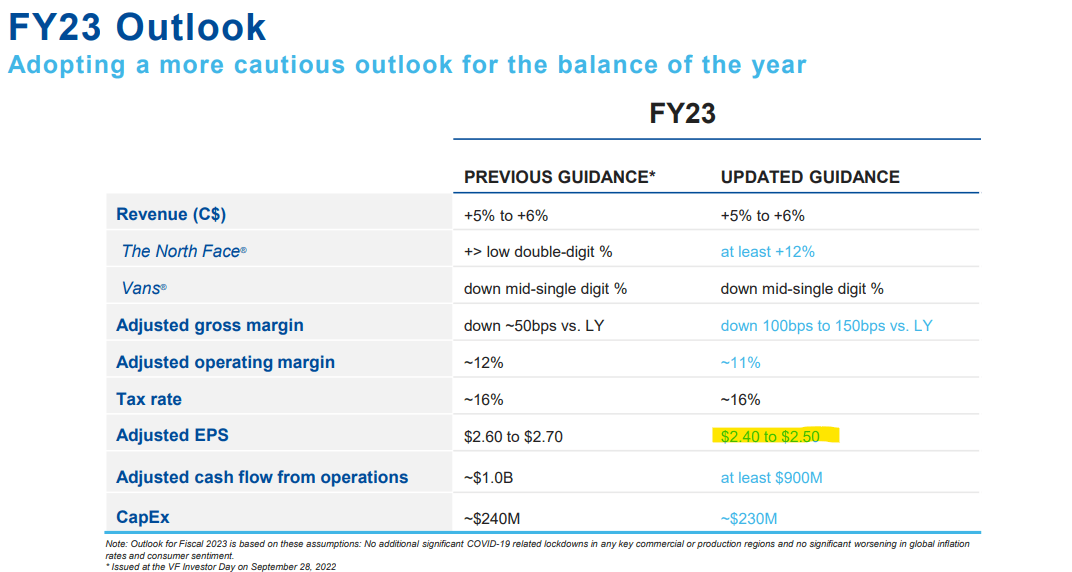

Management used the backdrop to push a more cautious tone with a revision lower to full-year earnings guidance. The company now expects fiscal 2023 EPS in a range between $2.40 and $2.50, compared to a prior $2.65 midpoint target. The trend is based on an expectation for a lower gross margin compared to fiscal 2022 with a view that inflationary cost pressures will continue along with ongoing FX weakness.

Company IR

Keep in mind that the timing of these events is critical, as the situation has improved since December. The shift goes back to the headlines that the Chinese government was easing Covid restrictions, quarantine requirements, and testing policies with an approach more consistent with the rest of the world. The sense is that authorities are cognizant of the economic weakness with risks to the broader financial system and looking to restart growth in the country, including through new stimulus measures.

As it relates to V.F. Corporation, the development is encouraging because it helps to remove one of the major headwinds for the company, opening the door for sales and earnings from the region to outperform a low bar of expectations.

Is VFC Dividend Sustainable?

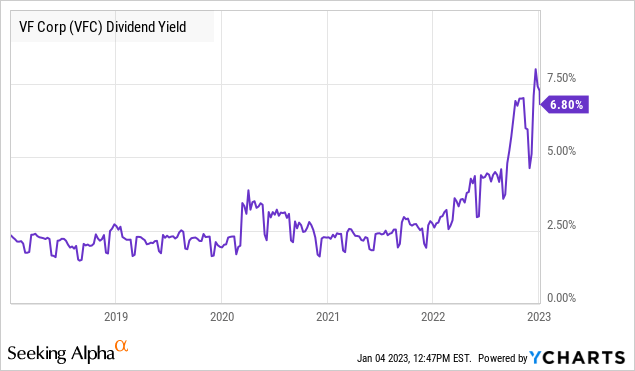

The other important subject with VFC comes down to its quarterly dividend, which was hiked in December by 2% to the new quarterly rate of $0.51 per share. In our view, any stock with a yield above 5% warrants some skepticism that the payout can be sustained. The forward yield on VFC approaching 7% reflects that concern.

The new annualized rate represents a distribution of nearly $800 million, which is well above the company’s current cash position last reported at $553 million. The figure also compares to a full-year 2023 adjusted cash flow from operations guidance by management of “at least $900 million” while actual free cash flow is expected to be materially lower. This is also in the context of more than $3.5 billion in total debt. The adjusted earnings payout rate on the 2023 EPS guidance is above 80%.

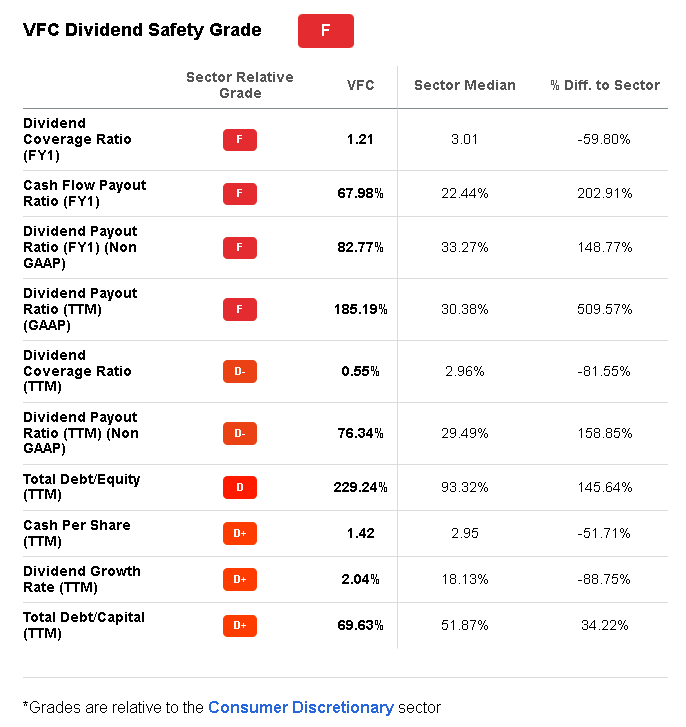

The trends are reflected in Seeking Alpha’s quant-based “Dividend Safety Grade” for VFC, where it receives an “F” based on several metrics. We agree here that the dividend is at risk, as it’s clear the room for financial flexibility is extremely narrow. A dividend cut would be an easy solution for the company to immediately improve liquidity.

Seeking Alpha

That said, considering the stock price performance over the last several months, there is a thought that a potential dividend cut has already been priced into the equity value. An official announcement, whether it happens over the next few months or into next year, would not necessarily be seen as negative for the stock if it supports an improvement in financial efficiency. Again, nothing is confirmed, and some reports that VFC is looking to divest its “JanSport” backpacks brand for up to $500 million could essentially buy the company some more time to restructure.

Our takeaway here is that financial conditions are poor, but it’s not over yet. Investors should not look at VFC as necessarily a strong dividend stock or income idea but focus more on its growth opportunity as macro conditions improve. The narrative for the company can turn more positive, especially if we’re right that stronger consumer spending trends in China translate into an uptick in sales and earnings over the next few quarters.

VFC Stock Price Forecast

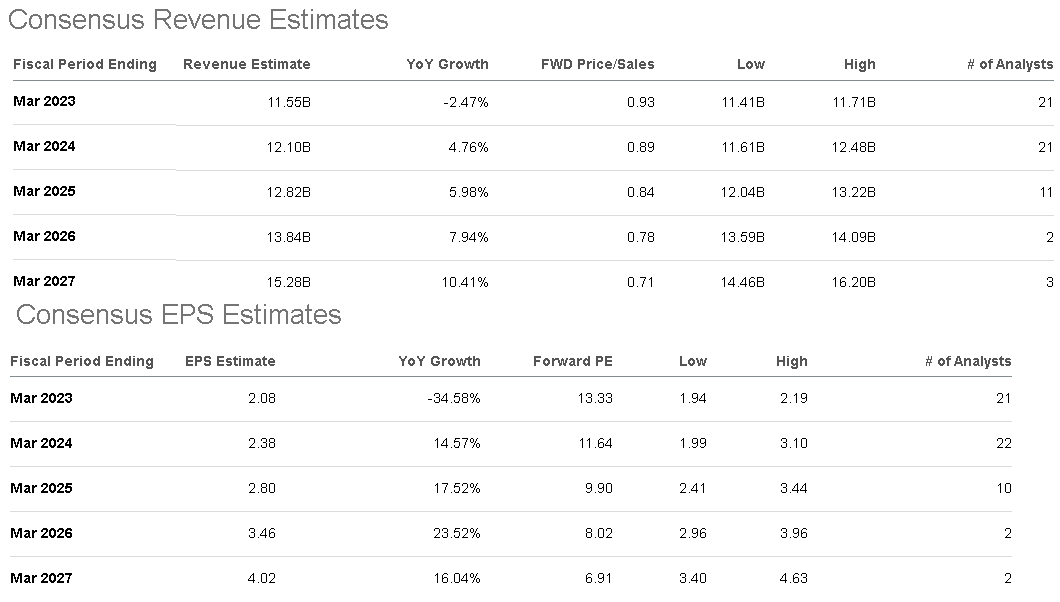

The bullish case for VFC is that the company can outperform expectations, which are backed by our view that the consensus is too pessimistic. The forecast for fiscal 2024 revenue growth rebounding to 4.8% may prove to be conservative, as the recent trends in China leave a low base of comparison. VFC would also benefit as the Dollar strength has pullback reversing some of the FX pressures while easing inflation can be positive for margins.

Seeking Alpha

Of course, we can cover the risks, which would center around a scenario where macro conditions deteriorate even further. A resurgence of inflationary pressures or sharply higher energy prices would undermine any bullish case as a negative towards earnings. Consumer spending trends in core regions like the Americas and EMEA would also be hit by rising unemployment and further increases in interest rates. A potential escalation of the Russia-Ukraine conflict lingers as a cloud to any forecast.

Nevertheless, we believe risks are tilted to the upside and take a cautiously bullish view, taking a more optimistic approach. We rate VFC as a buy with a price target for the year ahead at $40.00 per share, representing a 1-year forward P/E ratio of 15x on the current fiscal 2024 consensus EPS. This is a level shares last traded at in September and could be back in play with another leg higher.

The way we see it playing out is that strong trends over the next few quarters can lead to revisions of higher earnings estimates, which would make the stock look increasingly compelling. We can look forward to the Q3 earnings report set to be released on January 25th as an opportunity for management to provide an update on current conditions. Monitoring points include the trends in margins and cash flow to the balance sheet, with implications for the dividend.

Seeking Alpha

Be the first to comment