Scott Olson

The grocery store industry has undergone immense change over the past two decades. The growth of automated technologies has dramatically benefited larger retailers that can capitalize on self-checkout and supply-chain automation. Companies like Kroger (NYSE:KR) and Albertsons (ACI) have slowly acquired most surviving grocery store brands, with most local retailers failing under competitive pressure. More recently, Amazon’s (AMZN) incursion via its online platform and through Whole Foods brought competition to a new level as in-store retailers struggle to maintain margins against the internet giant.

After Kroger and Albertsons acquired numerous grocery brands, the two firms are looking to join forces via a substantial, nearly $25B merger. The combined company accounts for around 13.5% of the grocery market share. However, it would be, by far, the largest pure-play grocer as its largest competitors, Walmart (WMT), Costco (COST), etc., sell both food and non-food items. This bold effort is a higher-risk strategy as it does not necessarily solve the core issues within the grocery industry, but focuses them on one massive firm.

Kroger trades at a fairly reasonable valuation with a 10.7X forward “P/E.” and potential gains from a merger deal that could promote EPS growth. Of course, the agreement is subject to considerable FTC scrutiny due to potential anti-trust violations. Beyond that, Kroger has generally maintained profit margins despite immense food and wage inflation. The company is subject to lower economic risks than most but is exposed to supply-chain challenges and competitive pressures. While Kroger has potential, I believe the stock is subject to high risk in the current market environment.

Will The Albertsons Deal Add Value to Kroger?

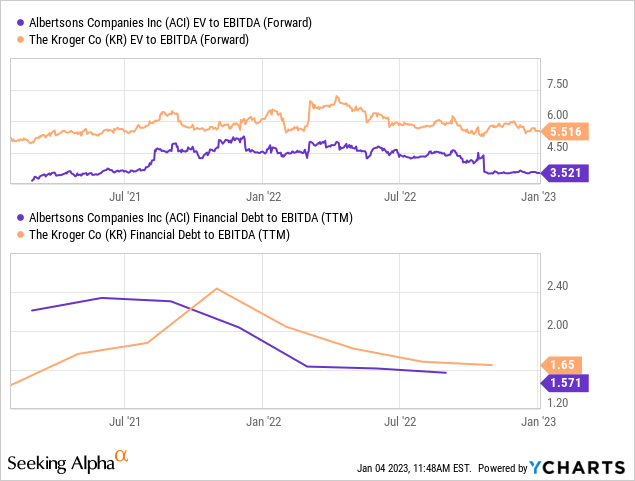

Albertsons struggles to compete with Kroger and trades at a lower valuation. Thus, Kroger should score an accretive benefit if the merger is finalized. Of course, interest rates are much higher, and Kroger nearly has a below-investment-grade credit rating, so it will pay a high cost for Albertsons. Neither company has an excessively high debt level today, but after Kroger acquires ACI and its debt, it will operate with very high leverage. See debt levels and valuations below:

On the positive side, Albertsons trades at a much lower “EV/EBITDA” than Kroger, mainly due to its competitive struggle against its larger peer. Thus, if Kroger acquires Albertsons, it should see its EBITDA-per-share rise materially without any significant business changes. Of course, Kroger aims to complete the merger with around $17.4B+ in debt financing, creating an immense new burden for Kroger, given today’s 6-9%+ interest rates on high-yield corporate debt. Kroger aims to reduce its financial debt-to-EBITDA level to 2.5X over the first two years after the deal is completed. The combined firm will likely have around $32B in total debt (adding the bridge loan and each firm’s existing net debt). The combined current EBITDA of both is $12B (~2.66X debt-to-EBITDA), so its hypothetical net debt to EBITDA will likely be slightly above that 2.5X level for some time after the merger is completed.

With Kroger willing to increase its leverage substantially amid a tumultuous grocery market environment, I believe the company is subject to relatively high credit downgrade risk. While the combined firm would see a rise in EBITDA, that would likely go to pay substantially higher interest costs. Further, it is not necessarily guaranteed that the combined will result in a substantial strategic benefit.

Kroger and Albertsons are both struggling to compete in the online market and against Walmart and Target (TGT) – which may offset losses on food items with profits on other things. Kroger has pioneered automation efforts to maintain its low margins, adding belted-self checkout, “no-checkout” or “smart cart” technology, AI theft reduction tools, and robotic fulfillment centers. While Kroger has argued that its Albertsons merger will create new jobs, I believe the opposite is far more likely as the firm has made immense strides to reduce employee needs. Of course, that is understandable as Kroger faces growing pressure from rapidly rising retail-worker wages and shortages. Combining the firms may allow Kroger to deploy its automating technologies into Albertsons stores and supply chain at a much more rapid pace.

In my view, there are a few key points to consider regarding the upside and risks of the deal. First, it will result in a highly levered firm with immense risk exposure to competitive and economic pressures facing pure-play grocers. This includes the difficulty of maintaining margins amid food price inflation and labor shortages. The merger may mitigate this threat by improving in-store and supply-chain automation, but that may not occur for years. While food price inflation is slowing, it is well-above overall inflation and may hamper Kroger as customers switch to lower-cost food items if it continues long enough. Overall, it may add value to KR investors today, but it could also dramatically increase its bankruptcy risk if the strategy does not work as expected.

Will The Merger Deal Go Through?

The FTC has the authority to block mergers that would create market dominance for one firm that could harm customers through price-hiking. Kroger and Albertsons are extremely close competitors, and rising grocery prices are a significant political issue, so the deal has been met with considerable controversy. Last month, the FTC extended the “waiting period” for analyzing the agreement, so the verdict should be announced shortly. In my view, there are numerous reasons why the deal may go through or be blocked by the FTC.

It is virtually guaranteed that the merged companies would create a grocery monopoly in many local markets, so even if the deal is completed, the combined company will likely need to sell many of its stores. Due to massive consolidation, this has been an ongoing issue in the grocery market over the past decade. Still, the combined firm would not have as large a total grocery market share as Walmart, so I do not believe the FTC is likely to block the deal altogether.

Is Kroger Worth The Risk?

In my view, Kroger is a considerable gamble today. On the positive side, the stock trades at a decent “P/E” of 10.7X. KR’s value has not risen substantially over recent years, so it is unlikely to be overvalued. Further, Kroger is relatively resistant to recessionary pressures and has managed to maintain its profit margin despite immense increases in food prices and retail worker wages. Its immediate economic risk is low, but if events change that create even more food price inflation pressures (and associated supply chain strains), Kroger may see profits fall as customers switch toward lower-margin, lower-cost products.

If the merger deal is completed, then Kroger may see strong growth over the coming years as it deploys its automating technology on a broad scale, improving its margins and competitive edge against Amazon or other retailers. With food prices rising, I expect retailers with lower margins to have the greatest resiliency as customers opt for those with lower prices. Of course, if transportation costs rise enough, then local groceries with greater access to local food production may gain a competitive edge, so Kroger is certainly not guaranteed to maintain an edge amid economic pressures.

On the negative side, the merger will create immense debt for Kroger that could offset much of its accretive potential. Further, it will concentrate on “pure play” grocery market risks tremendously – risks that multi-product retailers like Walmart and Costco are less exposed to. Thus, while Kroger has some growth potential, it may eventually have a high bankruptcy risk if its gamble does not pan out. With this in mind, I am not particularly bullish on the stock, but I may be more interested if its price declines or corporate borrowing rates fall.

Be the first to comment