ra2studio

Introduction

I like investing in public markets because it allows me to analyze companies from a broader range of perspectives; fundamentals, money flows, and market sentiments. It is highly liquid, allowing me to change my mind if I wish to do so and it offers extremely high options for portfolio diversification, which is core to my investing approach of making many, small and fast bets.

However, one thing I have always envied about private market investors is their ability to capture a large chunk of the value and using late public market investors as exit liquidity. If only I could get in alongside them…

Thankfully, in today’s global markets, this is possible by investing in listed private equity firms such as TPG Inc. (NASDAQ:TPG), which I analyze in this article:

Industry Background Information

In the asset management industry, there are mainly four main ways to make money on the assets under management (AUM):

- Increase AUM via more fundraising

- Increase AUM via higher returns

- Increase management fees

- Increase performance fees

A key industry lingo to understand is ‘fee paying AUM’. This refers to the pool of AUM that has a management fee charged tied to it. Generally, fee-related AUM is a high quality revenue stream as it is less volatile due to immunity from market gyrations.

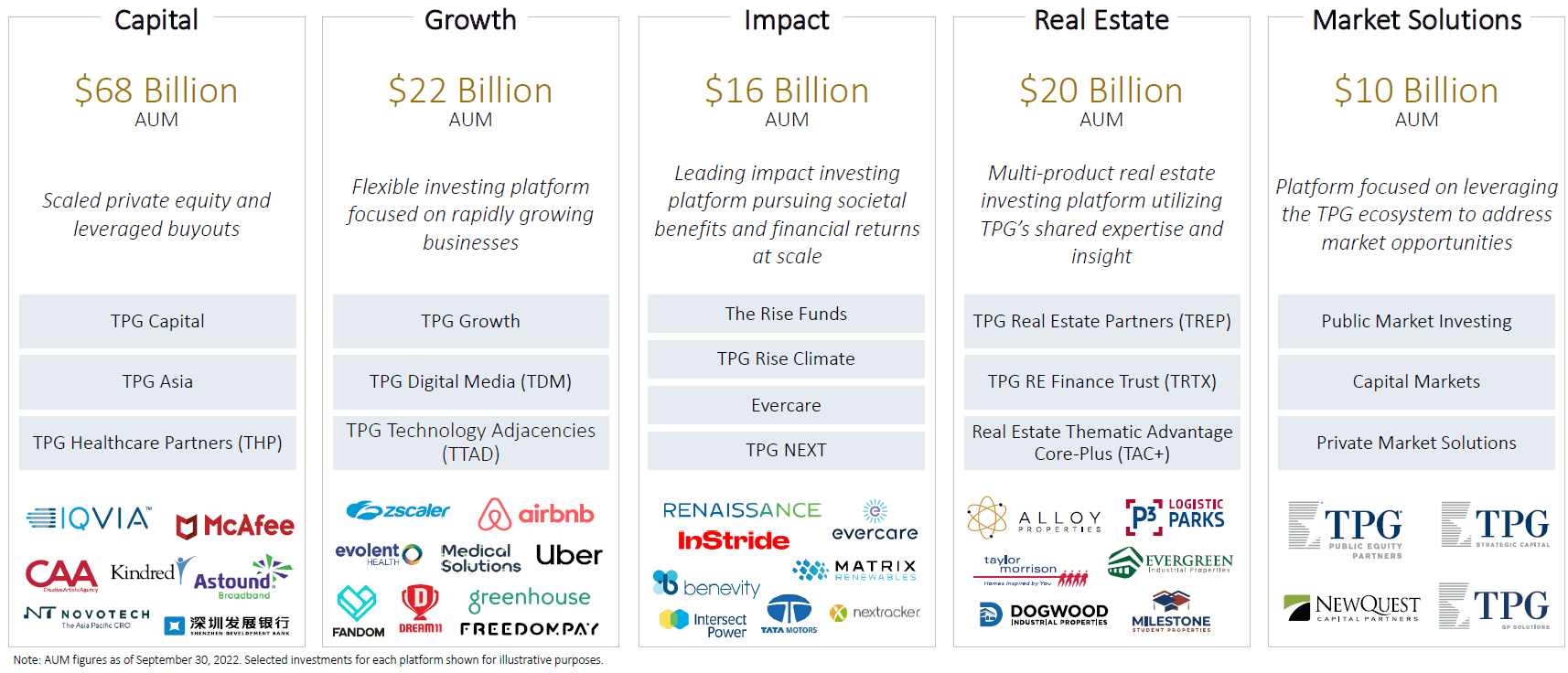

TPG Brief

TPG Portfolio Brief (TPG November 2022 Investor Presentation)

TPG is a large private equity firm managing $135 billion across various businesses as shown above in the extract of the company’s November 2022 presentation. With origins in private equity 30 years ago, the firm has expanded into various other asset classes. More recently, impact investing and real estate have been major vectors of growth as the world seeks a greater blend of investable options in the constant search for uncorrelated alpha.

My View on TPG

I am bullish on TPG due to 3 key reasons:

- TPG is growing and improving its AUM profile

- Sustainable fee growth will boost margins

- TPG is an attractive destination for investors seeking yield

TPG is growing and improving its AUM profile

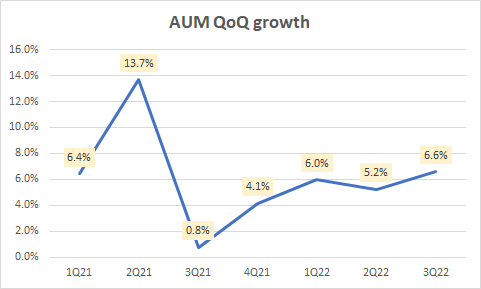

Faster growth track relative to industry

Since the end of 2020, TPG’s AUM has grown at a 26% CAGR compared to the industry’s 13.7% CAGR. This has been due to strong fundraising execution over the past 2 years as well as value creation. Importantly, the growth in AUM has been quite consistent, clocking in a healthy rate of around 6% QoQ despite a weak market:

AUM QoQ growth (Company Filings, Author’s Analysis)

In the November 2022 Investor Presentation, the company noted a high degree of cross-selling among its products as more than 75% of limited partners invested in three or more products. Incremental growth traction is also very healthy as more than 30% of commitments in active funds are from new customers over the last 5 years.

Overall, this displays TPG’s strong fundraising capabilities.

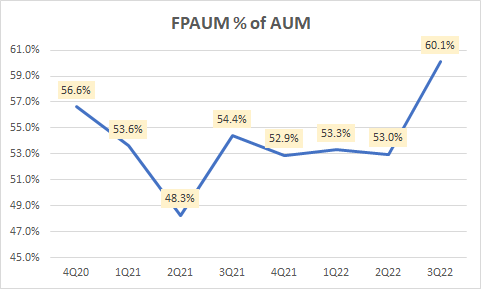

Improving fee paying AUM profile

TPG has been improving its fee paying AUM (FPAUM) mix consistently over the past few quarters:

Fee paying AUM as % of total AUM (Company Filings, Author’s Analysis)

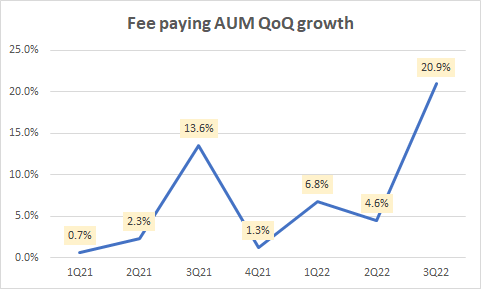

In the last quarter, fee paying AUM grew almost 21% QoQ:

Fee paying AUM QoQ growth (Company Filings, Author’s Analysis)

Importantly, the increase in this less volatile form of revenue has a long tenure; 90% of fee-earning AUM is in long-dated funds with a duration of more than 10 years, and 84% of fee-earning AUM has a duration of more than 5 years.

This leads to a structural improvement in TPG’s overall revenue profile, prompting some reasons for valuation re-ratings.

Dry powder to capitalize on bear market valuations

Throughout 2020 and 2021, it has capitalized on the high valuations and exited its investments, returning value to its investors.

Management cites that this has been instrumental to them being able to have strong fund raising amid the current weak market. This has led to $46 billion, that is 57% of fee paying AUM is TPG’s dry powder (deployable cash) position currently.

I believe this places TPG in a prime position to nab attractive deals and boost returns in a discounted market.

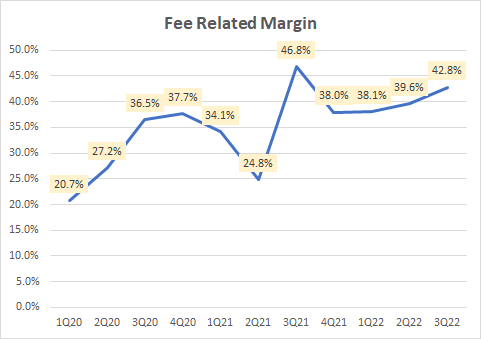

Sustainable fee growth will boost margins

TPG’s strong fee growth combined with operating leverage has led to a steady rise in its fee related margins:

Fee related margin (Company Filings, Author’s Analysis)

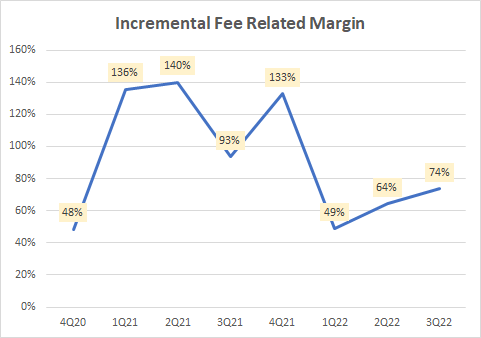

Importantly, incremental fee related margins are consistently at very healthy levels, well above current fee related margins, reflecting the company’s strong pricing power and scale effects:

Incremental fee related margin (Company Filings, Author’s Analysis)

In the Q3 FY22 earnings call, management noted a fee related income margin target of 45% by the end of 2023. Based on the current traction, they are comfortably out-delivering here. Thus, I expect a margin guidance upgrade soon in Q4 FY22.

TPG is an attractive destination for investors seeking yield

Markets don’t simply move on fundamentals. Flows of capital based on the kinds of profiles investors value more in various environments are key drivers of share prices too.

Through this lens too, I believe TPG is well-positioned to gain from flows of dividend seeking investors. This is because management intends to pay out at least 85% of after-tax distributable earnings as dividend every quarter. At the current rate, this corresponds to a dividend yield of 3.6%. This is higher than the US 10 year yield of 3.56%. I believe this is attractive, considering that this is accompanied by appreciation of the equity value.

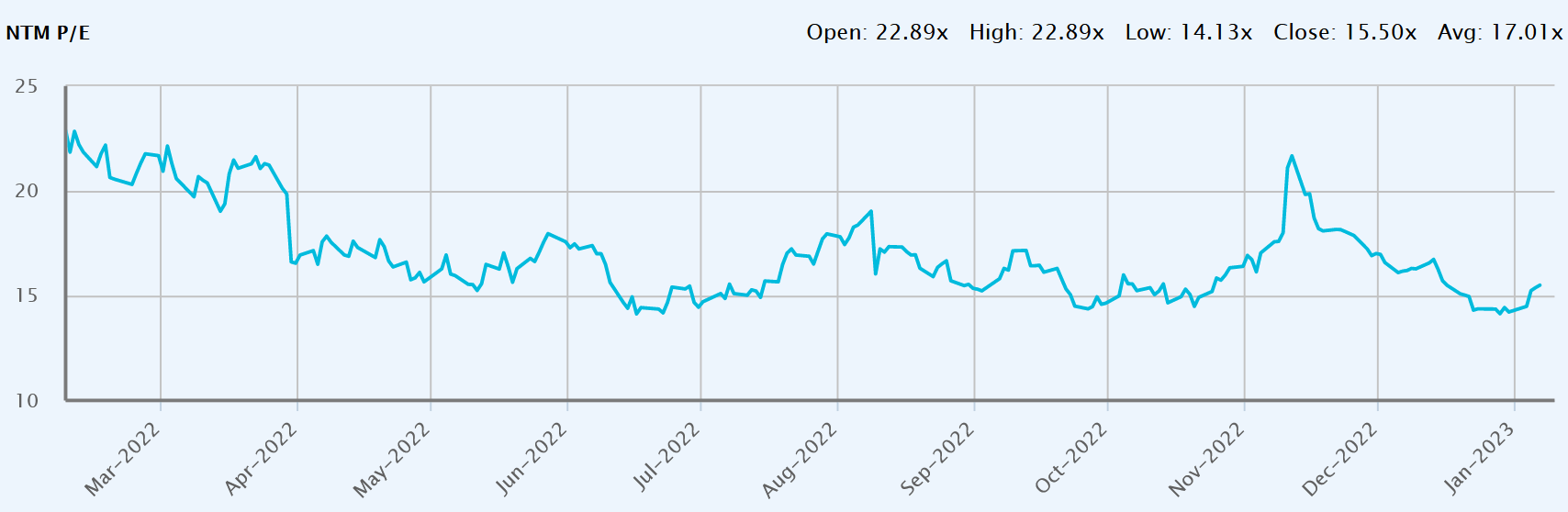

Valuation

Currently, TPG is trading at a 1-yr forward PE ratio of 15.5x, which is below its longer-term average of 17.0x:

TPG 1-year fwd PE (Capital IQ)

This corresponds to a 13% discount to its historical trading average multiple. I believe the recent strong uptick in fee paying AUM and the margin accretion that follows from that, combined with ample reserves of dry powder to capitalize on bear market opportunities positions TPG in a much superior position today.

Therefore, I believe it deserves a valuation multiple at least equal to the historical average range, if not higher. This would conservatively imply an upside of at least 13%.

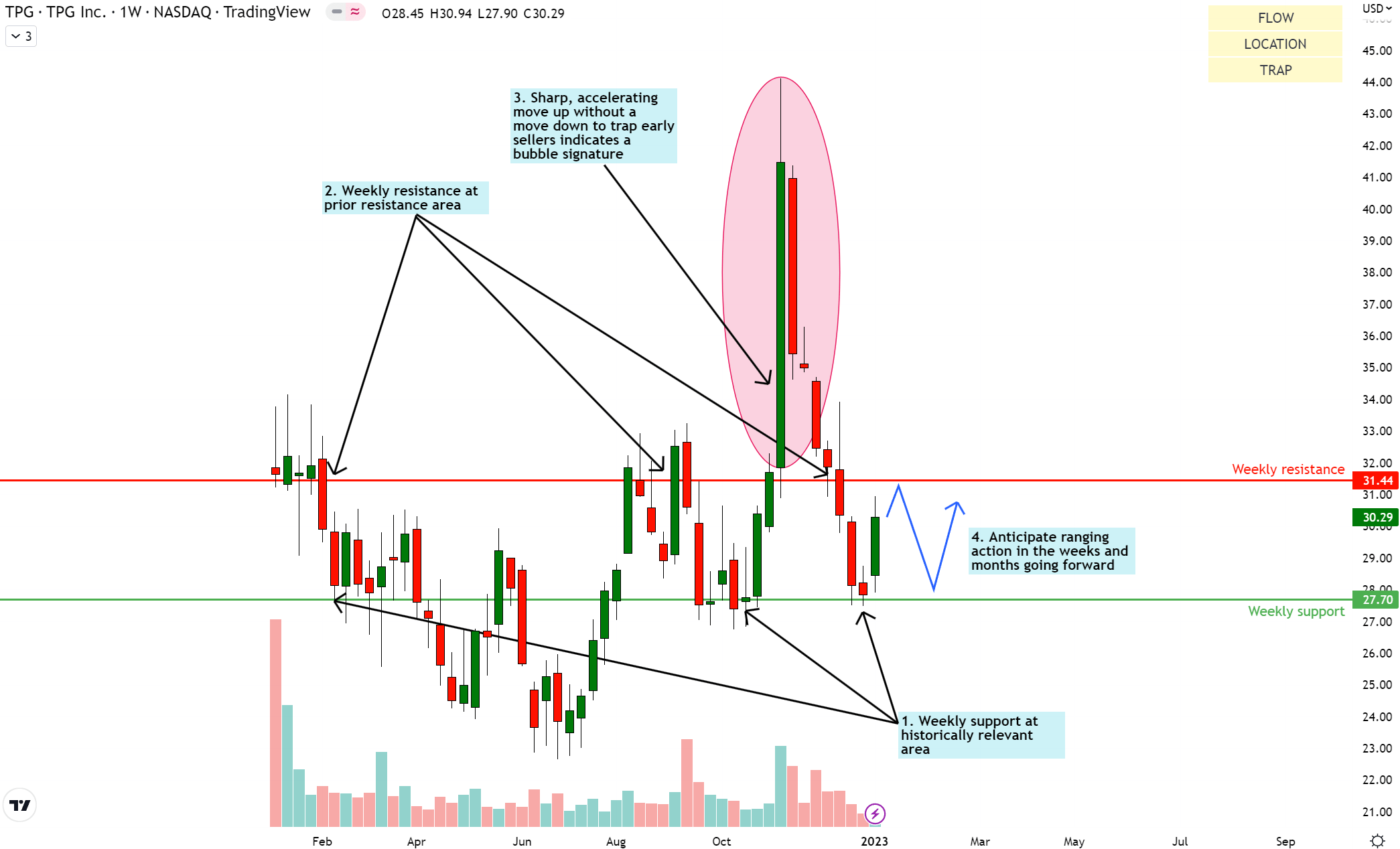

Technical Analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do, utilizing principles of Flow, Location and Trap.

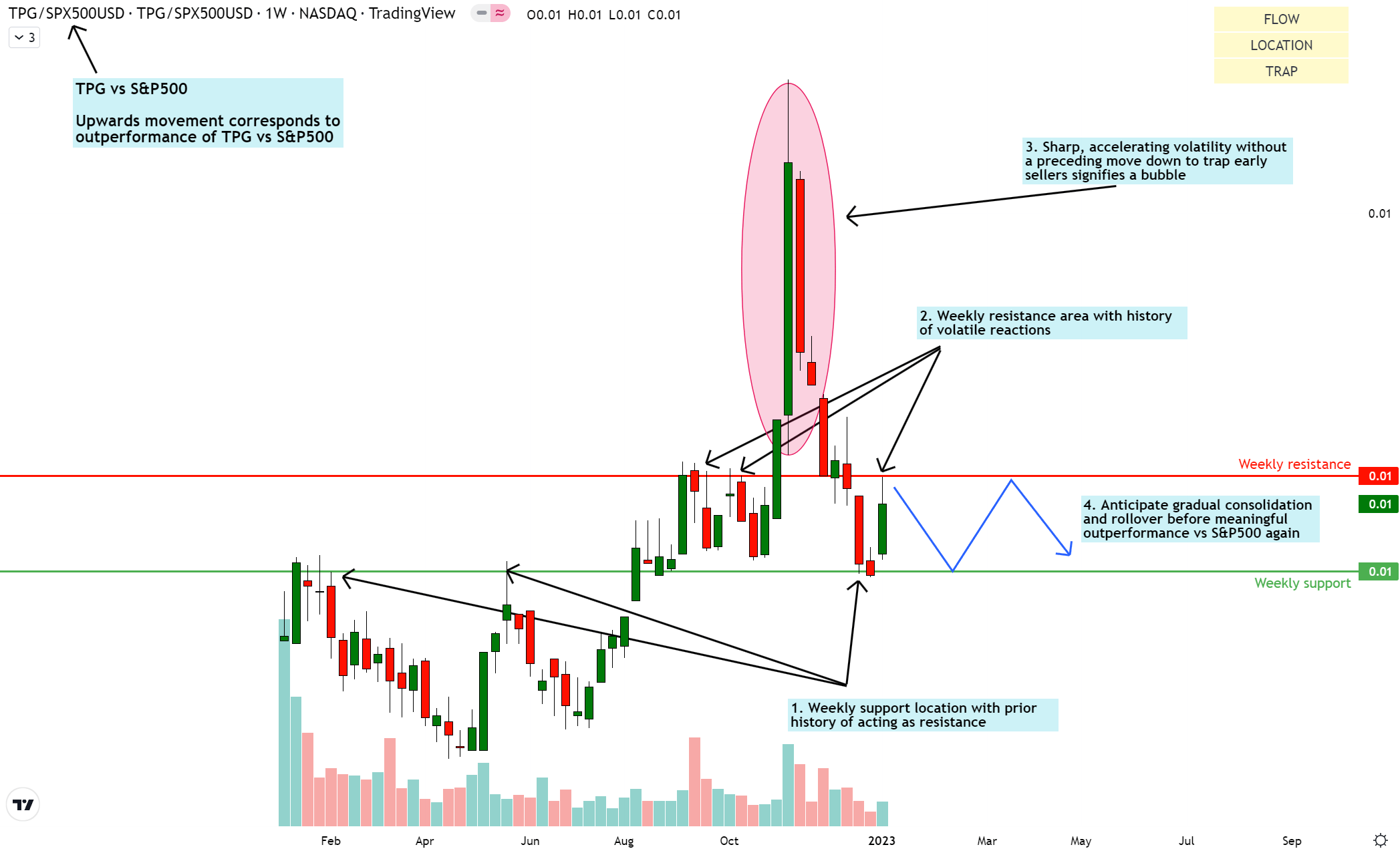

Relative Read of TPG vs SPX500

TPG vs SPX500 Technical Analysis (TradingView, Author’s Analysis)

On the relative chart of TPG vs S&P 500 (SPY) (SPX), the sudden, sharp, accelerating move up in November 2022 followed by a rapid reversal signifies a bubble signature. Bubble pops, unlike normal market corrections, tend to have slow and gradual recoveries rather than sharp reversals. Hence, I anticipate a ranging consolidation to develop.

Standalone Read of TPG

TPG Technical Analysis (TradingView, Author’s Analysis)

Key Monitorables

In a December 2022 company conference presentation, TPG CEO Jon Winkelried noted that despite relatively good fundraising execution by the company, in absolute terms, the fundraising environment is slower. I believe a turnaround in the market sentiment will be a key monitorable for this to turn.

Private market valuations are also generally correlated with public market valuations and common macroeconomic forces such as interest rates. Thus, as with the rest of the market, these are also key variables that would impact the attractiveness of TPG as an investment. Interest rate sensitivity would particularly impact roughly 28% of TPG’s growth oriented AUM, as represented by its ‘Growth’ and ‘Impact’ lines.

A reversal of market sentiment back to ‘risk-on’ may be the much required trigger to align together the bullish fundamental sentiments along with the neutral views suggested by the technicals.

Takeaway & Positioning

Overall, I believe TPG is growing stronger by the day even in a weak market environment. Its AUM continues to grow and its revenue and earnings profile continues to expand and shift towards a lower volatility stream. TPG’s investing teams have proven their judicious nature in exiting much of their investments amid bull market euphoria in 2020 and 2021. I believe they are positioned to do well and outperform the S&P 500 when the market sentiment turns constructive again.

For now, I have this on ‘hold’ in my watchlist of compelling buys.

Be the first to comment