Spencer Platt

Introduction

As a dividend growth investor, I always search for new ways to invest in income-producing assets. When I find these assets to be attractively valued, I often add to my existing positions. Additionally, I use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income while using less capital.

Within the financial sector, I often analyze money managers. I analyzed BlackRock (NYSE:BLK) in June of this year, and after carefully considering the company’s financials, position, and future opportunities, I found it to be a good buy. Since then, the company’s stock has performed remarkably well, with a 22% increase in price compared to the S&P 500’s 2% increase over the same period. This strong performance has caused me to revisit my analysis of BlackRock and consider whether it is still a good investment opportunity.

I will analyze the company using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company’s fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it’s a good investment.

Seeking Alpha’s company overview shows that:

BlackRock is an investment manager. The firm provides its services to the institutional, intermediary, and individual investors, including corporate, public, union, and industry pension plans, insurance companies, third-party mutual funds, endowments, public institutions, governments, foundations, charities, sovereign wealth funds, corporations, official institutions, and banks. It also provides global risk management and advisory services. The firm manages separate client-focused equity, fixed income, and balanced portfolios. It also launches and manages open-end and closed-end mutual funds, offshore funds, unit trusts, alternative investment vehicles, and structured funds.

Fundamentals

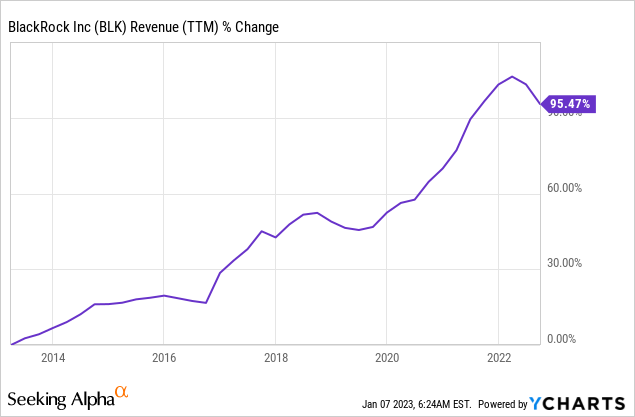

The revenues of BlackRock have almost doubled over the last decade. A 95% increase equals an annual sales growth of nearly 7%. BlackRock grows sales by increasing its AUM (assets under management) either by raising new capital or due to positive returns, which increase the value of investments. In the future, as seen on Seeking Alpha, the analyst consensus expects BlackRock to keep growing sales at an annual rate of ~5% in the medium term.

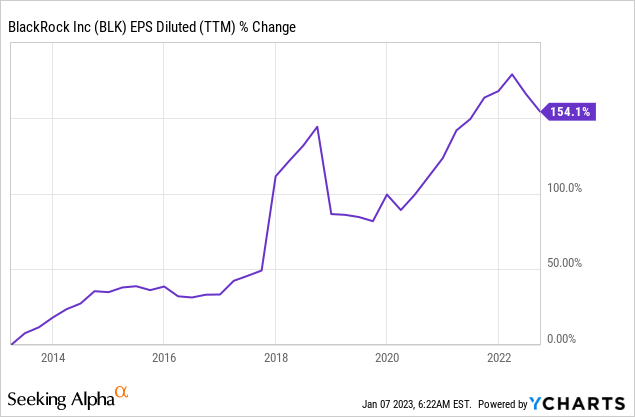

The EPS (earnings per share) increased faster over the last decade. A 150% increase equates to ~10% annual growth. The rapid growth can be attributed to higher revenues, buybacks and higher margins as the company increase its AUM and limit expenses increase. In the future, as seen on Seeking Alpha, the analyst consensus expects BlackRock to keep growing EPS at an annual rate of ~8% in the medium term.

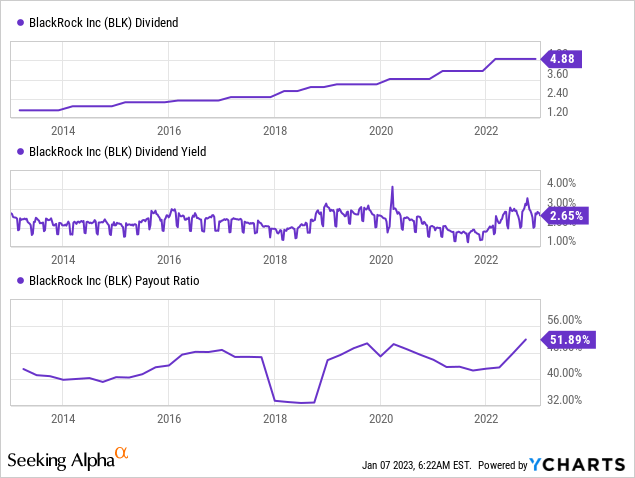

The dividend has been growing steadily on an annual basis over the last twelve years. During the challenges of the financial crisis, the company froze the dividend, yet it didn’t lower it since initiating it. The last increase was 18% in January 2022, meaning that BlackRock will likely increase the dividend again this month. Investors should expect a lower increase as the EPS declined in 2022, and the company’s payout ratio is 52%, which means the payment is safe, but there is not much room for payout ratio expansion.

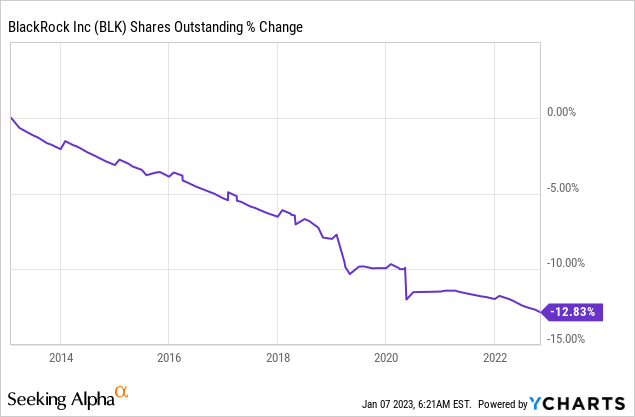

In addition to dividends, companies also return capital to shareholders via a share repurchase program. Share buybacks support EPS growth as they lower the number of outstanding shares. Over the last decade, BlackRock has repurchased almost 13% of its shares. Buybacks are highly effective when shares are cheap and should be used more aggressively when the price is attractive. BlackRock is committed to returning capital to shareholders.

Valuation

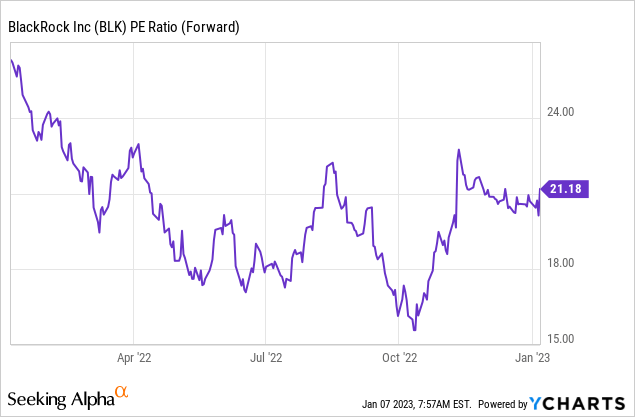

The P/E (price to earnings) ratio of BlackRock, when using the 2022 forecasted EPS, stands at 21. Over the past twelve months, the stock’s average valuation has been. Paying 21 times the EPS for a company that grows at 8% annually during the current business environment is a little bit high. However, it makes sense as the company is a leader in its field and has shown strong fundamentals during challenging periods in the past.

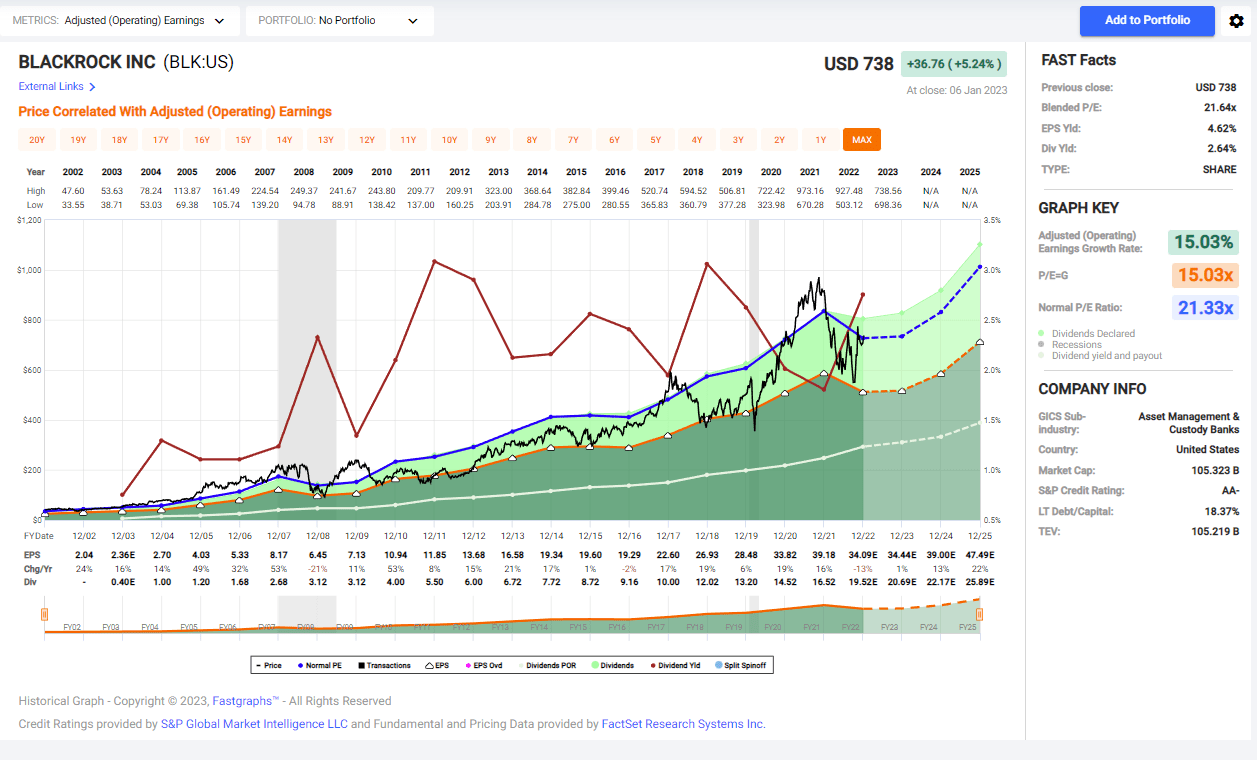

The graph below from Fastgraphs emphasizes that BlackRock is fairly valued or slightly overvalued. The current P/E ratio is in line with the average P/E ratio over the last two decades, which stands at 21.3. The growth rate has slowed due to the current environment and higher rates. Still, the company has grown following challenges such as the 2008 financial crisis. Therefore, I believe that the shares of BlackRock are fairly valued at the current price.

Fastgraphs

To conclude, BlackRock is a financially strong company with solid fundamentals. Its long history of stability and performance in the industry makes it a reliable investment option. The company’s stock is also fairly valued, which is priced in line with its intrinsic value. To be an attractive investment, a stock should have solid fundamentals, be reasonably valued, and show excellent growth potential and limited risks.

Opportunities

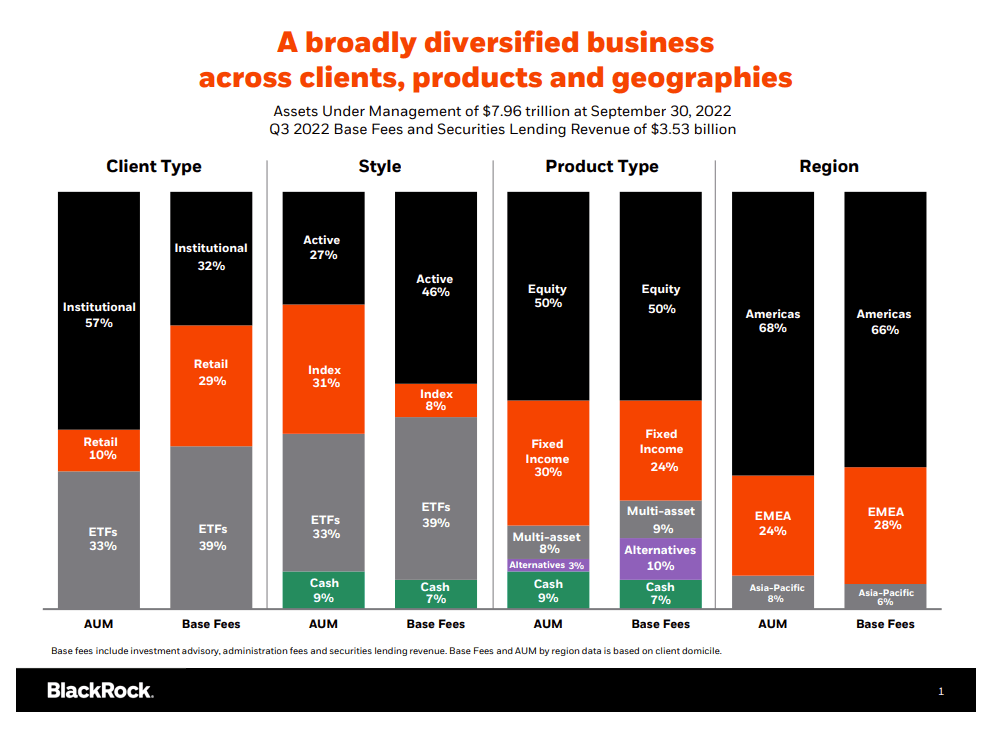

BlackRock’s global and product diversification provides numerous growth opportunities. BlackRock has a presence in multiple countries, allowing it to tap into diverse markets and a wide range of investment opportunities. It also helps the company to mitigate risk by spreading its operations across different regions and countries. In addition, BlackRock’s diverse product offerings, which include 8 trillion USD of actively managed and passively managed investment products, allow it to cater to a wide range of investor needs and preferences.

BlackRock

Another reason to invest in BlackRock is that the company is well-positioned to benefit from long-term trends in the financial services industry. The increasing demand for low-cost, passively managed investment products is a trend that is likely to continue in the coming years. BlackRock is a leading product provider and well-positioned to capitalize on this trend. Additionally, the company’s investment in technology and innovation has been helping it to stay ahead of the curve and remain competitive in an increasingly digital world.

Data scientists at BlackRock leverage AI and ML to scale data tasks for operational processes. Use cases include surveillance, data cleansing, and support functions. For example, we create and review over 1 million daily risk and exposure reports on portfolios through our system called Aladdin.

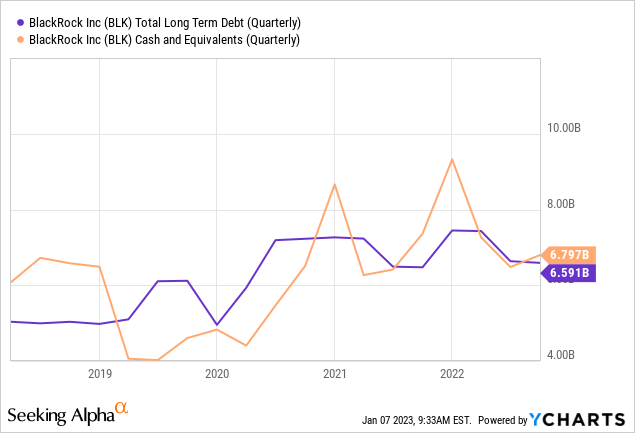

(Artificial intelligence and machine learning in asset management, OCT 2019) BlackRock’s strong balance sheet presents an opportunity for the company to pursue strategic acquisitions and partnerships that can drive growth and increase shareholder value. The company has a solid financial position, with a strong cash balance and low debt levels. This financial strength gives BlackRock the flexibility to pursue various growth opportunities, including acquisitions of other companies or assets, partnerships with complementary firms, and investments in new technologies or product offerings.

Risks

One risk that BlackRock faces is competition from other asset managers. The asset management industry is highly competitive, with many firms vying for market share. BlackRock competes with many other asset managers, including large, established firms and smaller, niche players. To maintain its market position and attract new assets under management, BlackRock must constantly innovate and offer competitive products and services. Another risk is that BlackRock’s actively managed funds may not perform as well as passively managed funds in certain market conditions. In recent years, there has been a trend towards passive investing, as many investors prefer to track the performance of a broad market index rather than trying to beat the market through individual stock selection. If this trend continues, it could potentially lead to outflows from BlackRock’s actively managed funds, which account for 27% of the AUM, and negatively impact the company’s financial performance. One risk that BlackRock may face is the impact of higher interest rates on its business. As a large asset manager, BlackRock is exposed to market movements, and an economic downturn or market correction could negatively impact the company’s AUM. BlackRock has a high beta, which means that its stock price tends to be more volatile and moves more in line with the market. It implies that BlackRock’s stock price could be more affected if the market were to decline.

Conclusions

Overall, BlackRock is a well-established company with solid fundamentals and a track record of strong performance. The company’s financials are healthy, with a diversified revenue stream and a solid balance sheet. Additionally, BlackRock’s stock is trading at a fair valuation, with a price-to-earnings ratio in line with its historical average. While there are some risks to consider, such as competition and market volatility, these are primarily mitigated by BlackRock’s scale and position as a market leader. There are also decent opportunities for growth, as the asset management industry is expected to continue expanding in the coming years. Given these factors, it may be reasonable to rate BlackRock as a HOLD. While the company is a solid investment with limited risks, the current market environment is volatile. It may be wise for investors to wait for better opportunities to buy the stock. Alternatively, investors who are comfortable with BlackRock’s business and are looking to build a position in the stock may want to consider buying gradually over time. This approach can help reduce the impact of market fluctuations on the investment’s overall performance.

Be the first to comment