Pascal Le Segretain/Getty Images News

Thomson Reuters (NYSE:TRI) is a brand that most of us will recognise because of its news segment. But they actually are mainly an enterprise focused business on legal, tax and admin solutions for enterprise clients. They’ve been a beneficiary of the pandemic’s digitalisation acceleration, and their growth rates have been organic and ample for years. The company has attractive economics and is a brand whose services are admin based, so a cost centre, and aren’t really the focus of cost programmes for clients, who will always need someone or another for these services. They are undergoing a change programme, so margins are slumping, but we believe they’ll improve according to their guidance on top of other cost savings initiatives. The change programme is a necessary speedbump in order for their services to be migrated to the cloud and better configured as remote working and digital backend increasingly becomes the norm.

A Look At the Financials

The change programme is a major source of confounding in the company’s finances. There are two opposing vectors. One off costs from the change programme, and long term cost saving being instituted as part of the change programme and other cost control initiatives. At the moment the change programme is winning out and hurting margins.

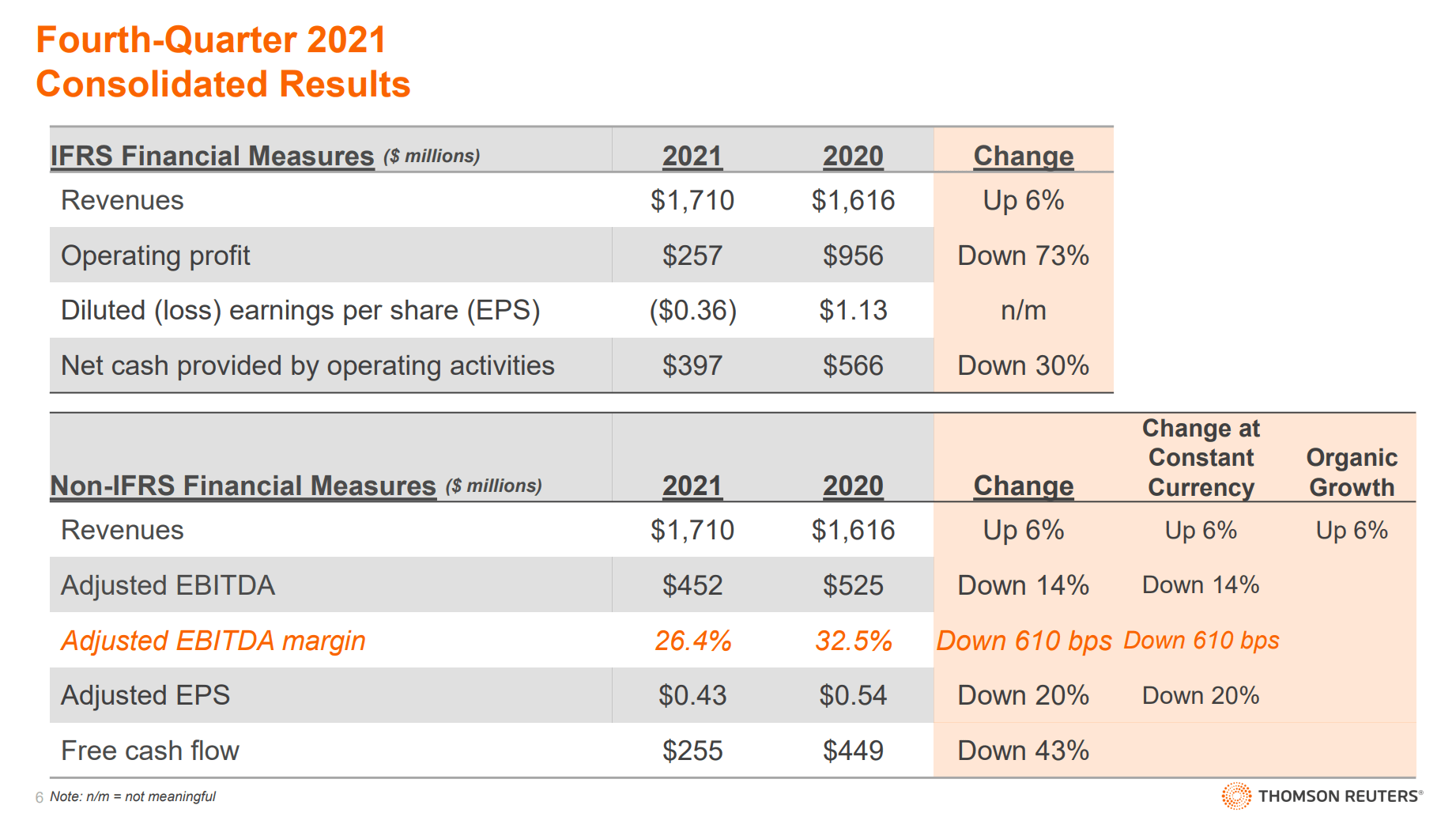

Adjusted EBITDA declined 14% to $452 million due to costs related to the Change Program, higher performance bonus expense, and a discretionary investment of $25 million to better position the business for 2022 which Mike will discuss. This resulted in a margin of 26.4%. Excluding Change Program costs adjusted EBITDA margin was 31.1%.

If you were to apply these change programme adjusted margins to the current Q4 revenue, which has grown 6% organically from 2020, the EBITDA evolution would essentially be flat YoY, with the adjusted EBITDA (further adjusted for the change programme) for 2021 at around $530 million excluding those change programme costs.

Q4 Financials (TRI Q4 2021 Pres)

The efforts to keep their digitalising services updated to the current world order as far as cost centre operations go have been proceeding smoothly. 37% of their revenue is now from cloud based solutions, and there is a plan to get it to 90% by 2023, as customers who were apprehensive about switching from a more traditional configuration become more open to the idea.

Thinking About Valuation

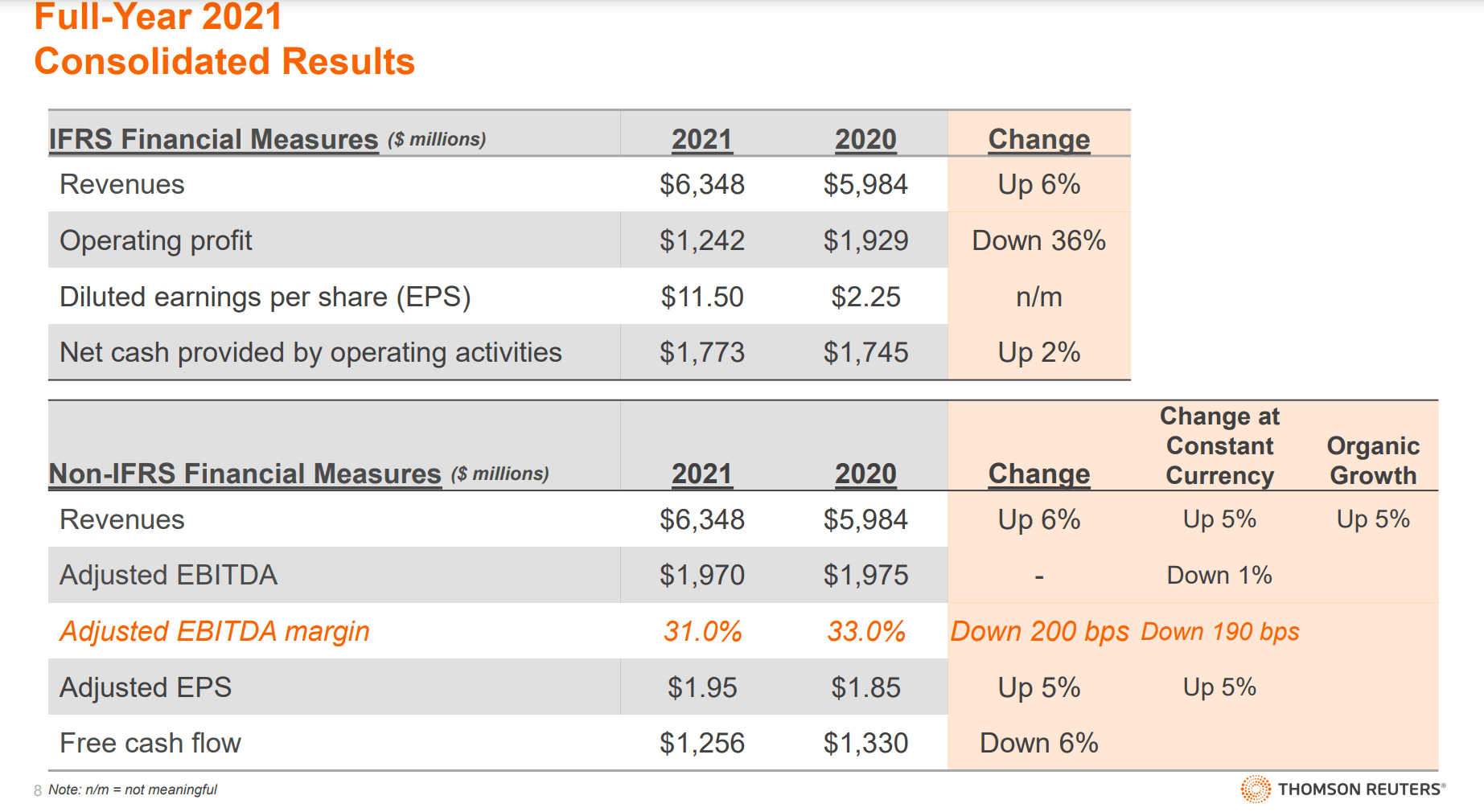

Supposing that we ignore for the time being the change programme related costs and do a pro forma calculation for EBITDA assuming the saving programme is fully realised, where would that leave us? Right now, the margins are slightly lower YoY, but TRI is guiding towards margins of 40% in 2023, once the cloud migration is almost fully realised and the cost saving plan comes into full effect.

We forecast an adjusted EBITDA margin of 35% for 2022 and between 39% and 40% for 2023.

Steve Hasker, CEO

FY Highlights (TRI Q4 2021 Pres)

Applying that margin to the current revenue would put us ahead to $2.539 billion in EBITDA, which is $600 million ahead of current EBITDA reflecting the expected cost savings, of which only about 33% is currently realised, also the proportion of cloud based sales relative to the plan target.

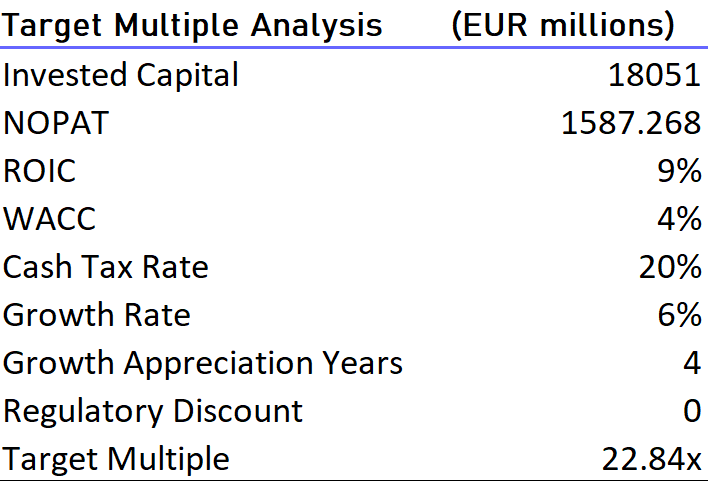

The best comp we could think of for TRI is a company called Intertrust (OTC:ITRUF), one of our successful investments from 2021, which was acquired at a multiple of around 12.5x on EBITDA. The company does fund administrations services, but it is not as comprehensive as TRI which also offers legal services, and also serves a much narrower vertical. Nonetheless, it is a cost centre service and also increasingly digital.

TRI currently would trade at about a 20x multiple on this pro forma figure. But the key difference between TRI and Intertrust is the growth profile. Moreover, the TRI ROICs are slightly higher. Intertrust was clearly undervalued, but on a target multiple analysis basis, TRI is not a bad deal either despite the substantial premium to Intertrust.

TMA Analysis (VTS)

Even with pretty conservative assumptions in terms of growth appreciation periods, i.e just 4 years of the 6% organic growth, you get a fair multiple that is actually a little higher than TRI’s current multiple. TRI doesn’t have much leverage, so the difference in multiple doesn’t really create a big upside margin, and we always have to take cash flow based approaches like target multiple analysis with a grain of salt, but the valuation definitely does appear fair.

Conclusions

Of course it is essential for the cost saving initiatives and the cloud based transition related to the change programme to be fully realised. We are currently at 33% of the plan target, but to justify the current multiple, the effects are fully priced in already by markets. We don’t think this is an unreasonable expectation. As said, there is clear evidence of uptake of these cloud based solutions thanks in part to the pandemic, and the company shouldn’t have major problems convincing clients that what they’re offering is better. However, with the multiple already being rather fair, even if maybe we could give some more upside if we assume a longer GAP due to the quality of the company and its likely ability to keep growing earnings, we just aren’t interested enough in this sort of risk-reward to take a bite.

Be the first to comment