Ruediger Fessel/iStock via Getty Images

Introduction

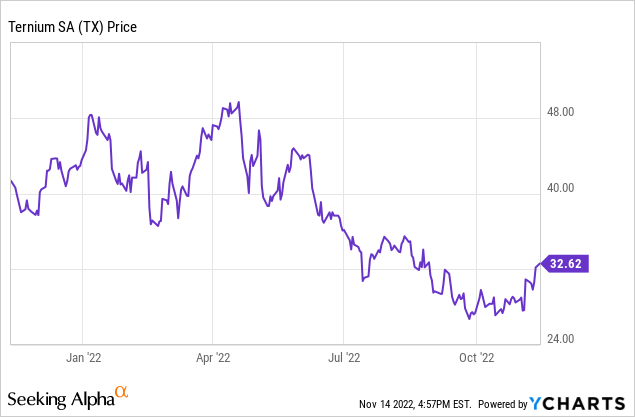

The steel market is a very cyclical market and producers and investors have to deal with potentially massive price swings. The entire sector enjoyed a massive tailwind in the post-COVID era but steel prices have come down by quite a bit in the past few quarters. While Ternium (NYSE:TX), my favorite Mexico and Argentina focused steel producer, is definitely seeing and feeling the impact of a deteriorating market, its very strong balance sheet offers additional protection. Earlier this year the question wasn’t “if” but “when” the steel market and steel producers would see a correction.

While margins are being compressed, Ternium’s financial performance remains strong

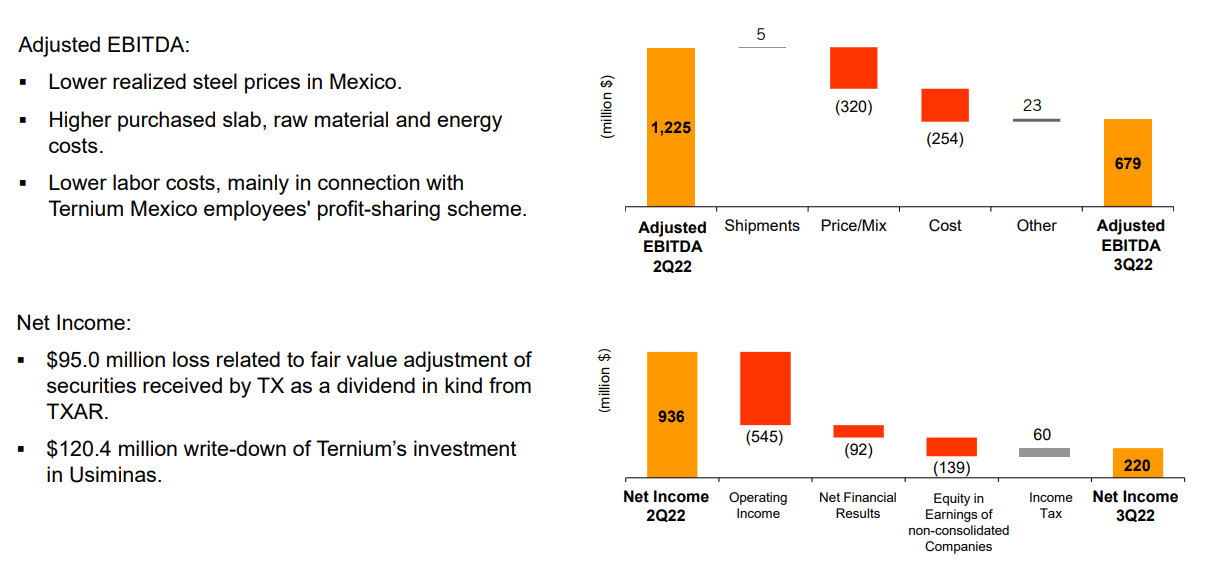

During the third quarter, the company produced 2.97 million tonnes of steel, which is a 3% decrease compared to the third quarter of last year while the output remained virtually unchanged on a QoQ basis. The steel price has been decreasing for a while now, and this means the EBITDA margins are being compressed. While the company generated an EBITDA margin of $414/t in the second quarter and even $612/t in the third quarter of last year, these margins collapsed to 16% of the revenue for a total EBITDA of $679M.

Ternium Investor Relations

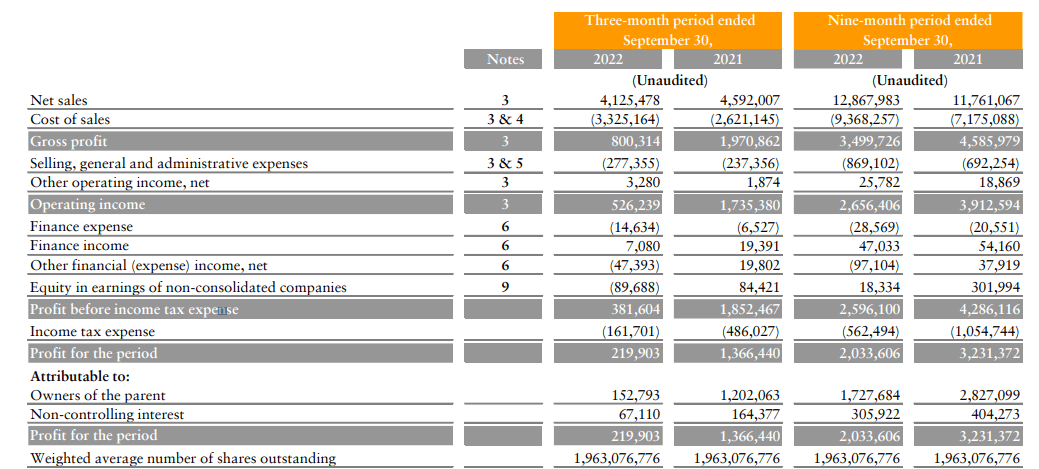

Of course, that still is a decent result, and as you can see below, Ternium definitely remained profitable. Total revenue in the third quarter came in at $4.1B and despite the higher COGS, the gross profit was still pretty decent at $800M. The operating income fell to $526M and the pre-tax income fell by almost 80% although there obviously is a $175M swing in the contribution from equity accounted investees while there also was a $66M swing in the “other financial expense” which is mainly related to FX changes.

Ternium Investor Relations

That also explains why the average tax rate was so high as some of the expenses are not (immediately) deductible. About $153M of the $220M in reported net income was attributable to the shareholders of Ternium and this represents an EPS of $0.078 per share. Every share of TX represents 10 underlying shares which means the EPS for the US-traded stock was $0.78.

Ternium Investor Relations

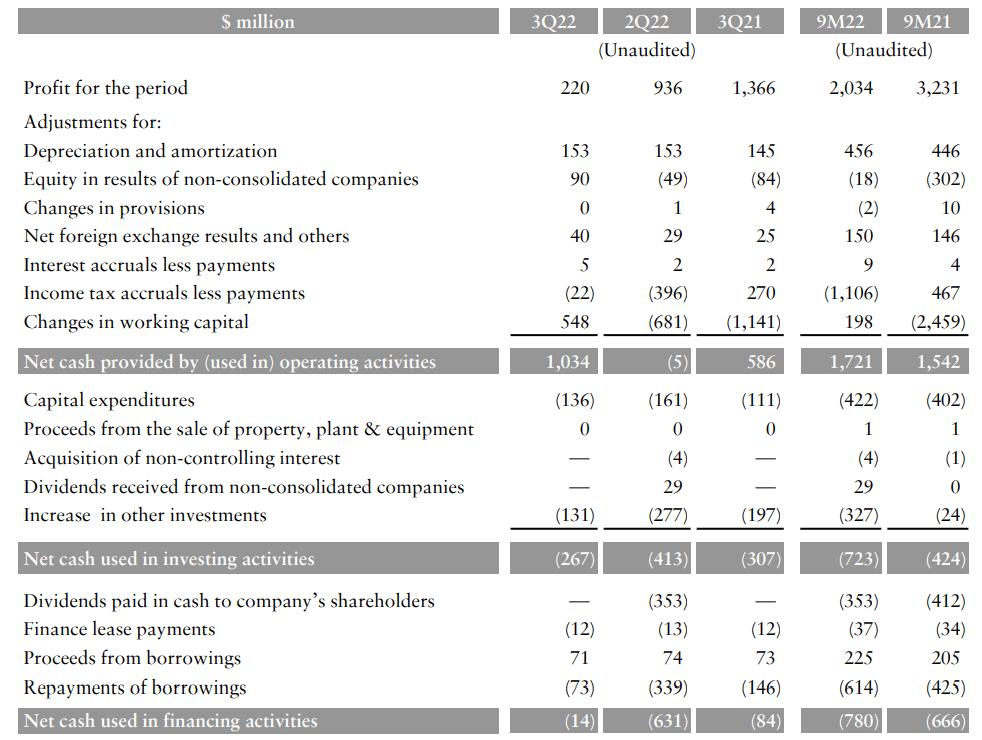

My previous investment theses were based on the free cash flow profile of Ternium, so it only makes sense to judge the company based on its free cash flows. As you can see below, the total reported operating cash flow was $1.03B. However, this included a $548M contribution from changes in the working capital position and excluded $12M in lease payments. This means that on an adjusted basis, the operating cash flow was approximately $474M.

Ternium Investor Relations

The total capex was just $136M which means the adjusted free cash flow in the third quarter was approximately $338M. A portion is attributable to minority interests and applying the same ratio as the attributable net income, the attributable free cash flow result was approximately $235M. This likely underestimates the attributable free cash flow as even the attributable net income in Q3 2022 was relatively low vs. previous quarters and years. While Ternium does not provide a breakdown of how much of the free cash flow was attributable to the minority interests, I think the $235M I mentioned is on the conservative side of the spectrum, and based on previous years I’d argue the number likely is closer to $275M.

But just to err on the cautious side, I will use the $235M. Divided by 196 million ADS currently outstanding, the underlying free cash flow per share was approximately $1.20. And that’s still a respectable result.

The balance sheet

One of the main reasons why I was never too worried about Ternium is its excellent balance sheet. As of the end of September, the company had about $1.5B in cash and an additional $1.27B in other investments. Meanwhile, the total gross debt came in just under $1.1B resulting in a total net cash position of approximately $1.7B. That’s approximately $8.5 per ADS (although some of that net cash likely is attributable to the minority interests) and it goes without saying this exceptionally robust balance sheet will help Ternium to get through difficult times. It’s definitely not the only company in the sector with a net cash position, but the size of the cash pile is pretty attractive.

This also means the upcoming dividend payment of $0.90 per ADS (payable on Nov. 17) will barely make a dent in the net cash position.

Investment thesis

While the net income and underlying free cash flow nosedived compared to a year ago or even last quarter, we can’t say Ternium is terribly expensive (although the share price has already put in a strong performance, stronger than I expected in my August article).

The high net cash position acts as a cushion against market volatility and that likely helps to explain why Ternium’s share price is holding its ground. I’m considering writing out of the money put options but I’m in no rush as I already have exposure to the steel market with Algoma Steel (ASTL). The option writing strategy on Ternium has served me well in the past and that will likely be my approach this time as well.

Be the first to comment