2027, When TD Bank Buys TELUS NurPhoto/NurPhoto via Getty Images![]()

On our last update on TELUS Corporation (NYSE:TU) (TSX:T:CA), we made a case to continue staying out of the wireless giant. At the center of our thesis was a bloated valuation and it was further supported by relatively weak earnings. We went with a “hold” but had short-sell price in mind as well.

We will see tooth and nail competition in the quarters ahead from the telecom sector. Valuation does not look remotely appealing at 17-18X free cash flow and 23X earnings for TELUS. We would stay out and consider a Sell/Short Sell rating above $27.00.

Source: About That Herculean One-Foot Putt

TELUS did not test that ceiling and has drifted a bit lower since the last update.

Seeking Alpha

We go over the recently released results and update our valuation model with numbers for 2024 and 2025.

The Last Two Years

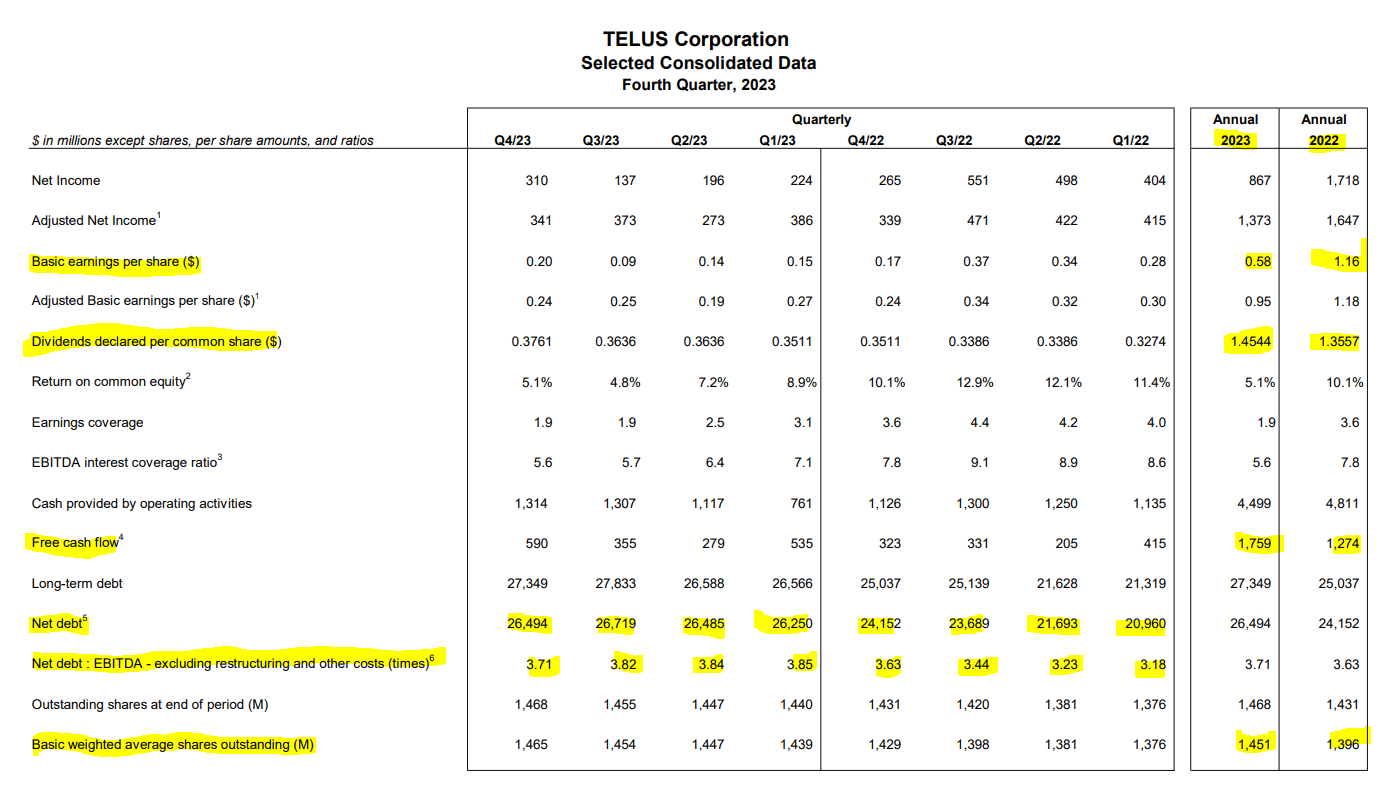

There is a lot to unpack in the quarterly numbers but let’s look at the two year trend of some fundamentals first. You can see below that basic earnings per share have been quite weak in both 2022 and 2023. Neither came anywhere in the postal code of the dividend.

TELUS Q4-2023 Supplemental

In fact earnings coverage for the dividend was under 40%. Put another way, payout ratio via earnings was near 250%. Before we move on to the free cash flow aspect, we must note that this coverage is in real stark contrast to the A&T (T) and Verizon (VZ) numbers. Both comfortably cover their dividends via earnings. So one does not need dismiss those poor ratios as an industry standard. The free cash flow does come closer to the dividend. For 2023, free cash flow per share was at $1.21. Still lower than the $1.4544 dividend, but definitely within striking distance. Of course over the last two years you heard of nothing but phrases complimenting the numbers and the subscriber adds. But did anyone else ever tell you that net debt is up $5.5 billion since Q1-2022? Did you hear about net debt to EBITDA going from 3.18X to 3.71X? Those are big moves and when you complain the stock price has not responded to these “great results”, it actually has responded exactly at it should. The market is taking away from the market capitalization what TELUS is adding to its debt load.

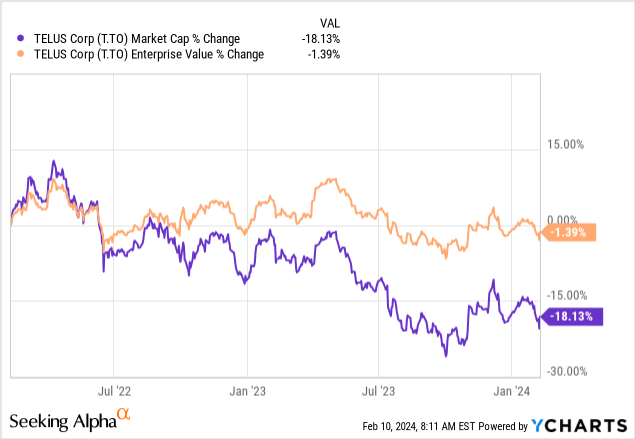

TELUS’ has almost the same Enterprise value over the last two years. The higher debt load has weighed on the market capitalization.

Q4-2023

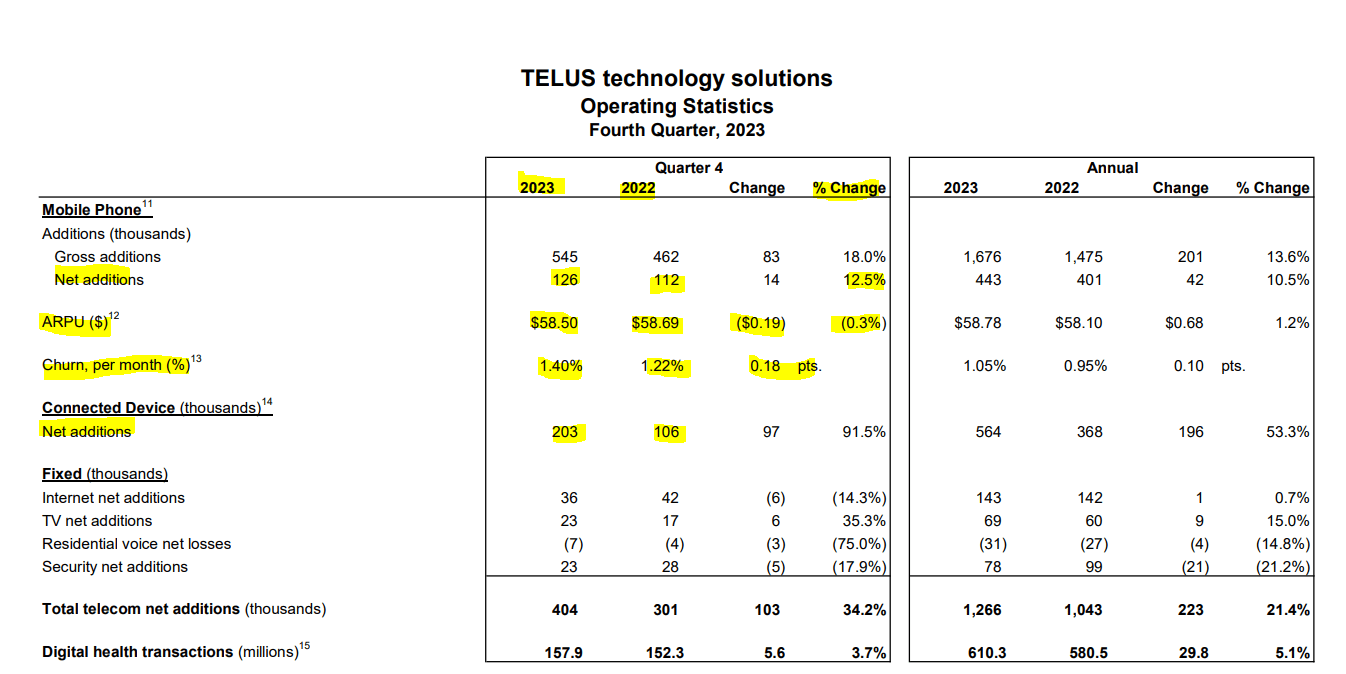

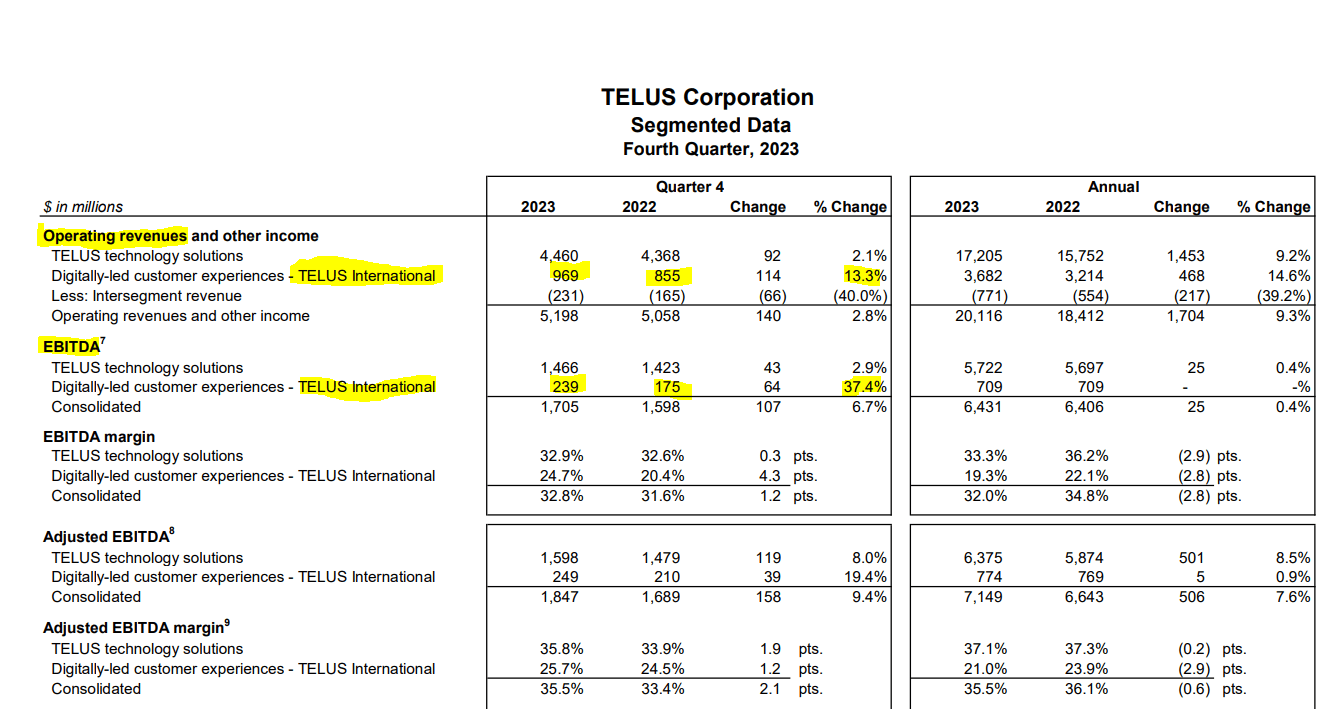

Ok, with that said, let us look at the Q4-2023 numbers. Net additions were impressive once more and came in at 126,000.

TELUS Q4-2023 Supplemental

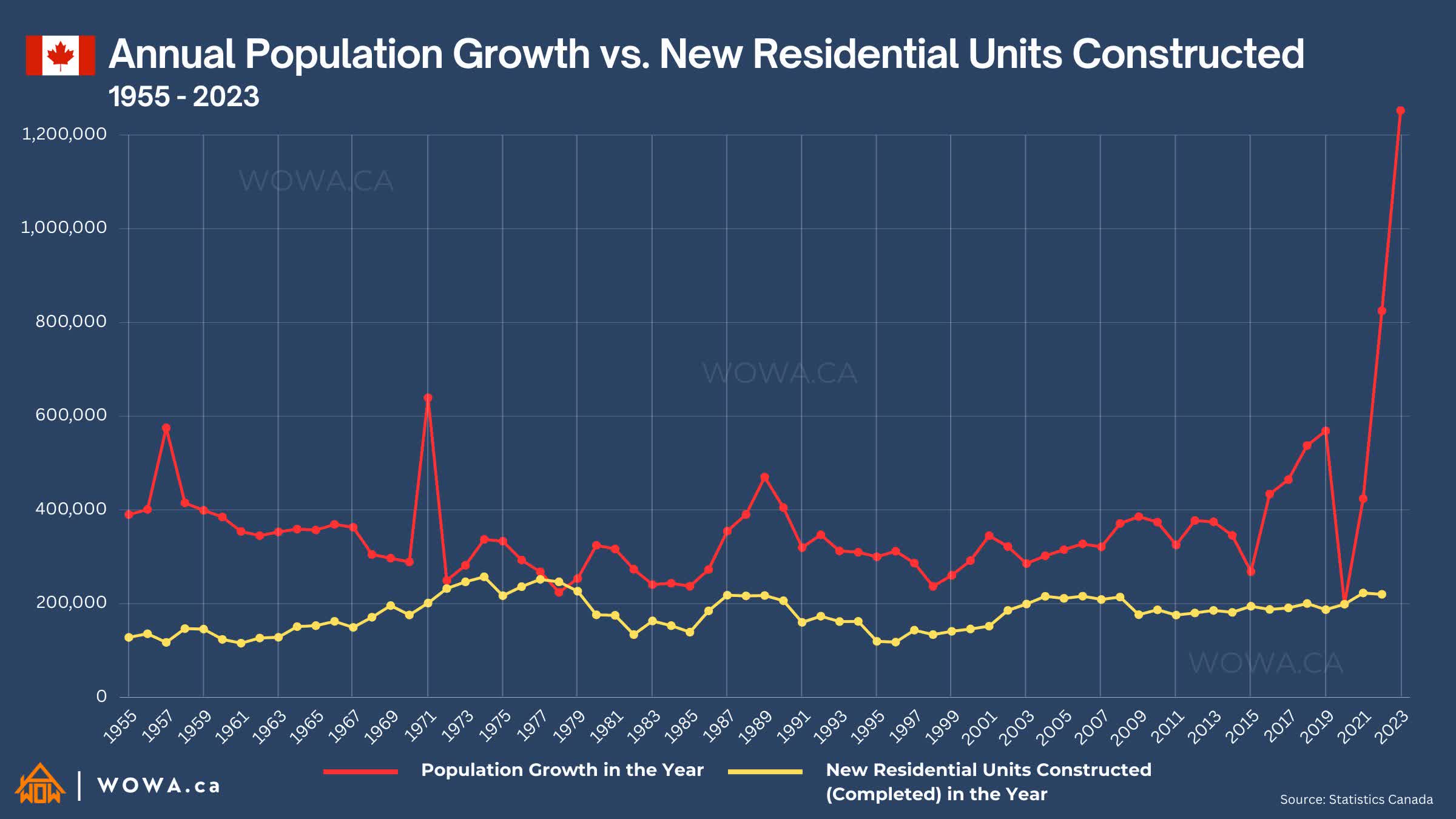

This has been a consistent theme for all telecoms in Canada, ever since we completely messed up our immigration policy. For those that want to retort that we did not completely mess up our immigration policy, we will just leave you with the next chart.

WOWA via Hanif Bayat on X

Of course that chart is the reason TELUS stock is not completely in the gutter. Had they been expanding their debt load so much and overpaying dividends far above their free cash flow, without that benefit above, you can bet that TELUS would have been another 30% lower. But even with all of this benefit from newcomers, the average revenue per subscriber slipped in Q4-2023 to $58.50. This is likely to slip further in Q1-2024 and in Q2-2024 as those massive year-end promotions finally have their full impact. Even in Q4-2023, it was clear that things were not moving too briskly if we stripped out the impact of TELUS International (TIXT)(TIXT:CA).

TELUS Q4-2023 Supplemental

Outlook

The good news is that TELUS will be covering its dividends via free cash flow in 2024.

Lastly, consolidated free cash flow for 2024 is forecasted to be $2.3 billion driven by higher EBITDA and stable CapEx. The strong growth includes higher cash restructuring payments related to our efforts undertaken in 2023 as discussed earlier, as well as incremental restructuring targeted in 2024.

Putting it all together, our combined and combined with TI’s outlook announced earlier today, on a consolidated basis, we expect operating revenues and adjusted EBITDA to grow similar to that of TTech.

Source: TELUS Q4-2023 Conference Call Transcript

That should leave nothing to pay down debt and that 3.7X debt to EBITDA looks unwieldy. This is higher than BCE Inc. (BCE)(BCE:CA) but lower than Rogers Communications Inc. (RCI.B:CA). Currently the market does not care, but when it does, you can expect big pressure on the firm. AT&T for example has felt it for a few years now and is finally close to getting debt to EBITDA under 3.0X in 2025. So we see more valuation compression in the year ahead and the downside risks would be higher in a recession. Yes, the labor reports look strong but there is a lot of noise under the surface and the last report was extremely strange (see detailed breakdown here).

Verdict

If you go back to March 2022 (see, One Growth Bubble Waiting To Implode), TELUS traded at a huge premium to fair value. You had to look all the way into 2025 to remotely make sense of the valuation and even then you were left confused. Fast forward to today and we are now beginning to get into some level of sanity. EV to EBITDA is now at 8.0X and free cash flow yield is close to 6.2%. If you want to bet on low interest rates returning, then this is not the worst play you can get. But we come back to our AT&T comparison. That one has a free cash yield of 14%. You can argue all you want about the bungles and errors that AT&T has made but it is just as likely that TELUS ramping debt to EBITDA to 3.7X is an error as well. We would need to see some buffer coming into the free cash flow to pay down debt, before we can slap a buy rating. We rate this a Hold and would consider a Buy under $20.00.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment