lcva2

Introduction

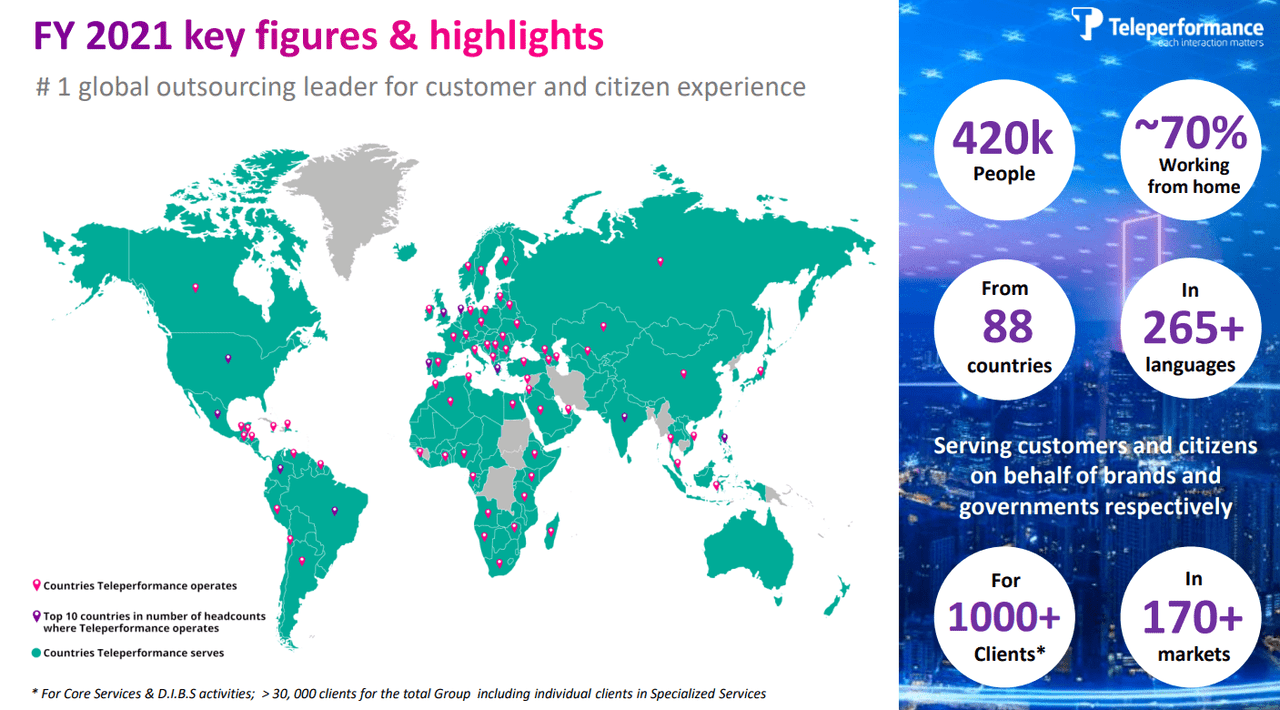

Based in France, but with operations across the six populated continents, Teleperformance (OTCPK:TLPFY) is a leader in providing tech-based customer experience services (CX). As the world’s business and governmental organizations attempt to become more efficient through the use of technology, Teleperformance is one of the best turnkey providers to rely on. In fact, the company has been in business for over 30 years and has become the leader in their industry according to both research firms Everest and Forrester. Teleperformance is not stopping with just providing services for CX, multiple large acquisitions over the past few years have expanded operations into a wide range of business solutions.

This new diversification of revenue sources and operational experience has improved the company’s financial outlook, and is the basis for the long thesis. I hope this article reflects the opportunity that is suitable for a wide range of investment goals, all made available through a simple analysis. Sometimes investing is all about looking around for these opportunities rather than pseudo-technical financial calculations that usually do not pan out as expected.

Teleperformance Investor Presentation

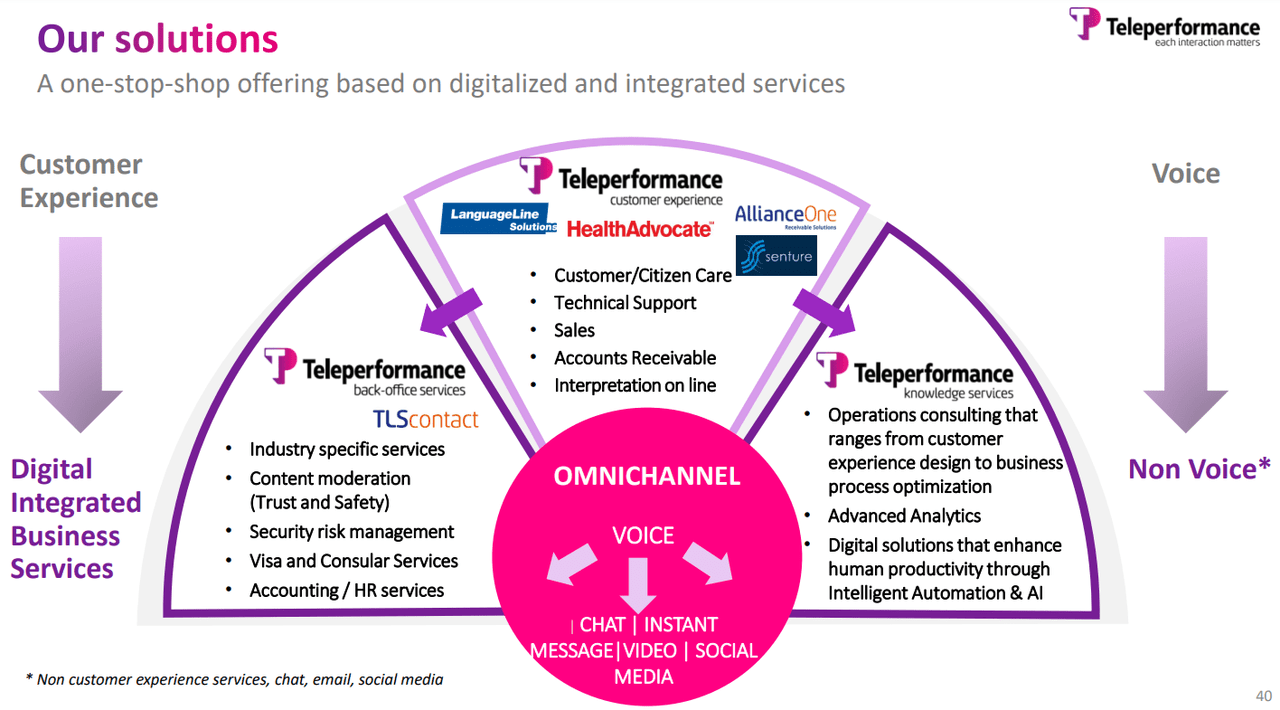

To understand how Teleperformance will succeed in the future, we must understand the services they provide. Most importantly, I believe that Teleperformance offers critical business solutions that allow for reduced volatility through weak market conditions as businesses continue paying long-term subscriptions. This is because Teleperformance’s solutions allow their clients to interact with their own customers, and these processes are required 24/7 and will not be under-funded. The primary solutions rely on communication between a business and their customers across all mediums.

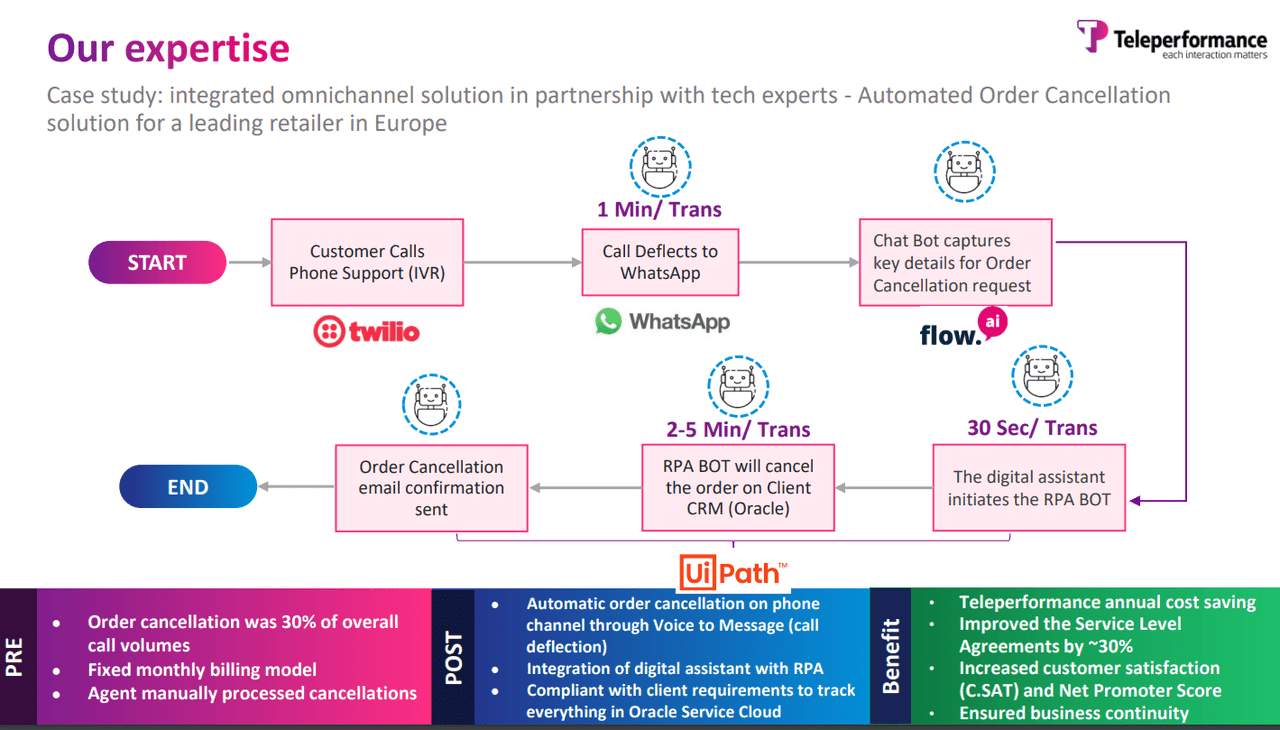

One case study provided below includes the total integration of services provided by Twilio (TWLO), WhatsApp (META), and even UiPath (PATH), just for a customer to cancel their order. The key is that the full process is not automated without the need for human intervention, can collect data for analysis, decreases overall cost, and improves customer satisfaction. Due to the widening TPF platform, clients no longer need to hire large IT departments to deliver technological improvements, and these benefits support higher margins for TPF.

Teleperformance Investor Presentation Teleperformance Investor Presentation

The expanded expertise beyond the traditional “contact center outsourcing” business model that was lower margin and highly competitive is incredibly transformative for TPF. As they move towards a broader fully integrated platform across all business solutions, the TAM increases, margins improve, revenues stabilize away from cyclicality, and the valuation will inherently rise.

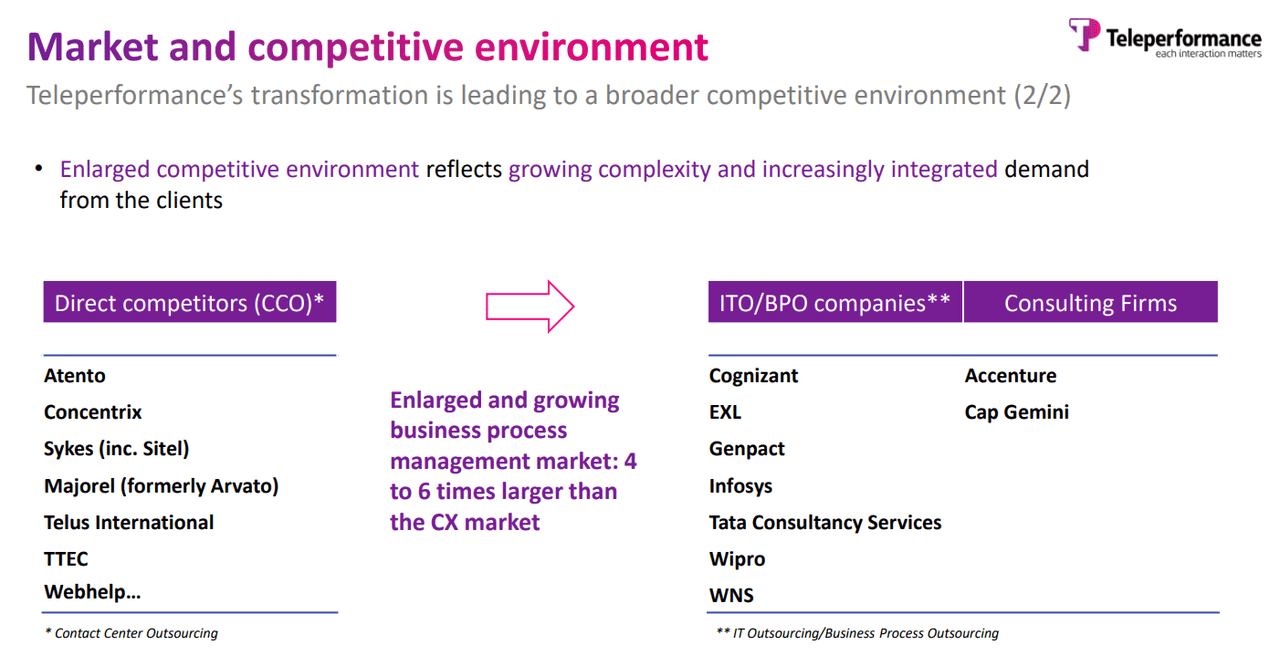

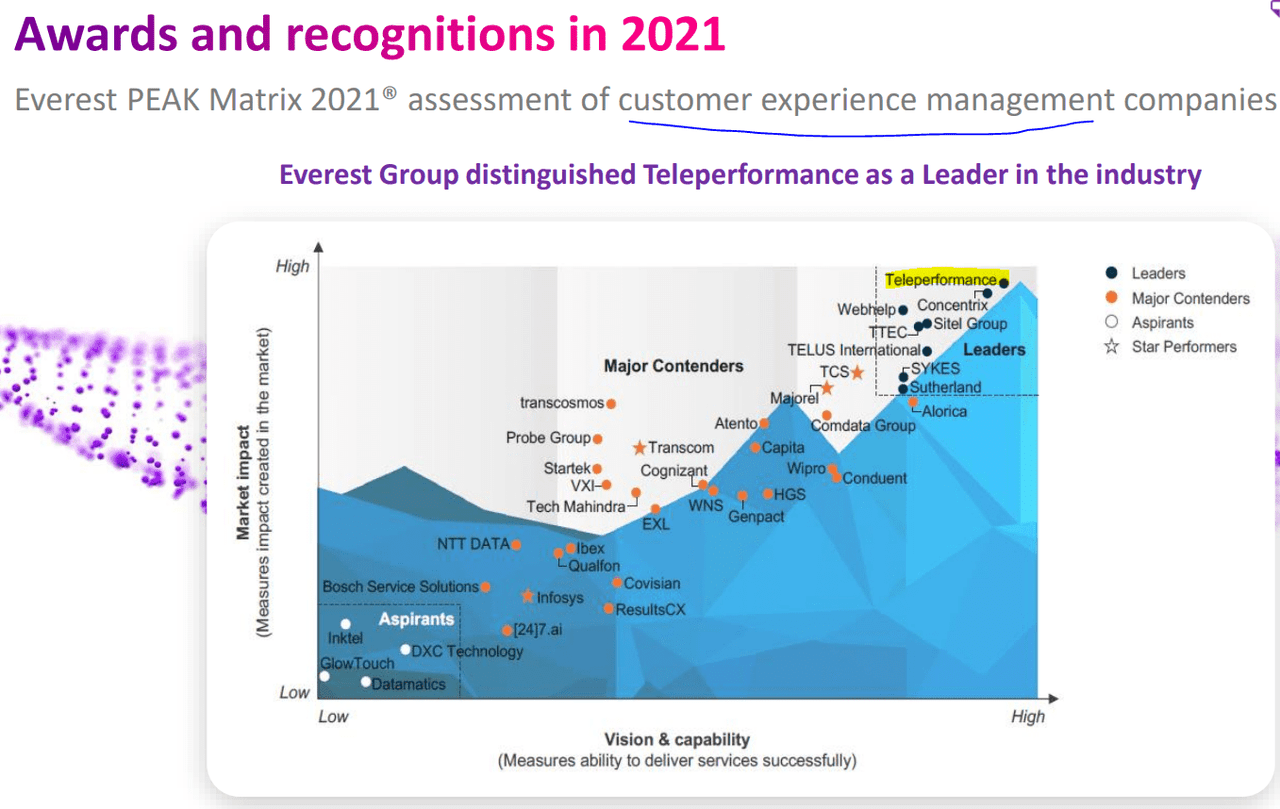

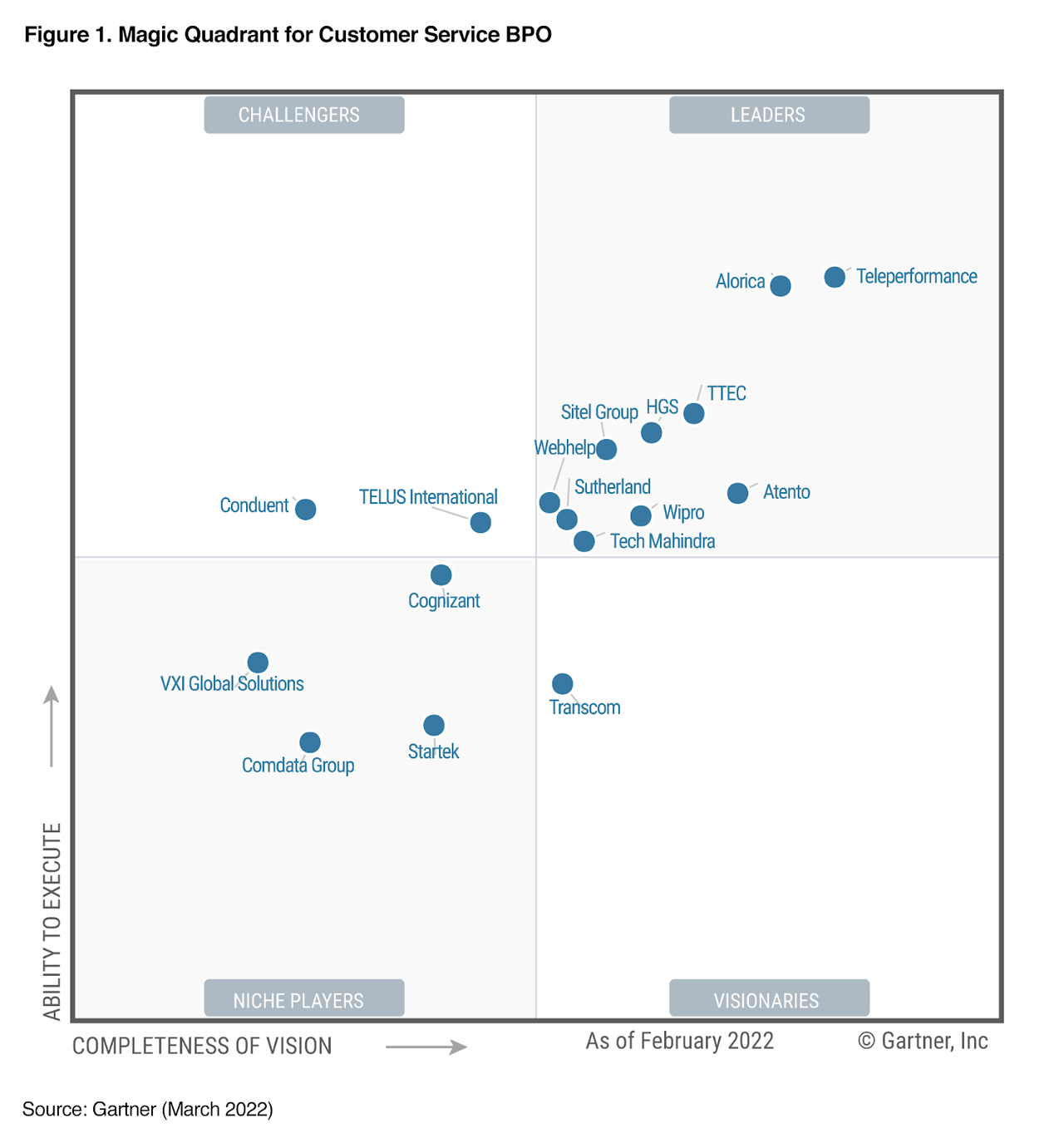

As shown in the image below, TPF is moving toward more esteemed companies/peers such as Cognizant (CTSH), Infosys (INFY), Capgemini (OTCPK:CGEMY), and even Accenture (ACN). Then, considering TPF is already the leader in their field (according to Everest and Gartner) with thousands of clients worldwide, the transition to additional platform services will be far easier than other small-scale peers who must acquire new customers.

Teleperformance Investor Presentation

Teleperformance Website Gartner

Quantitative Data

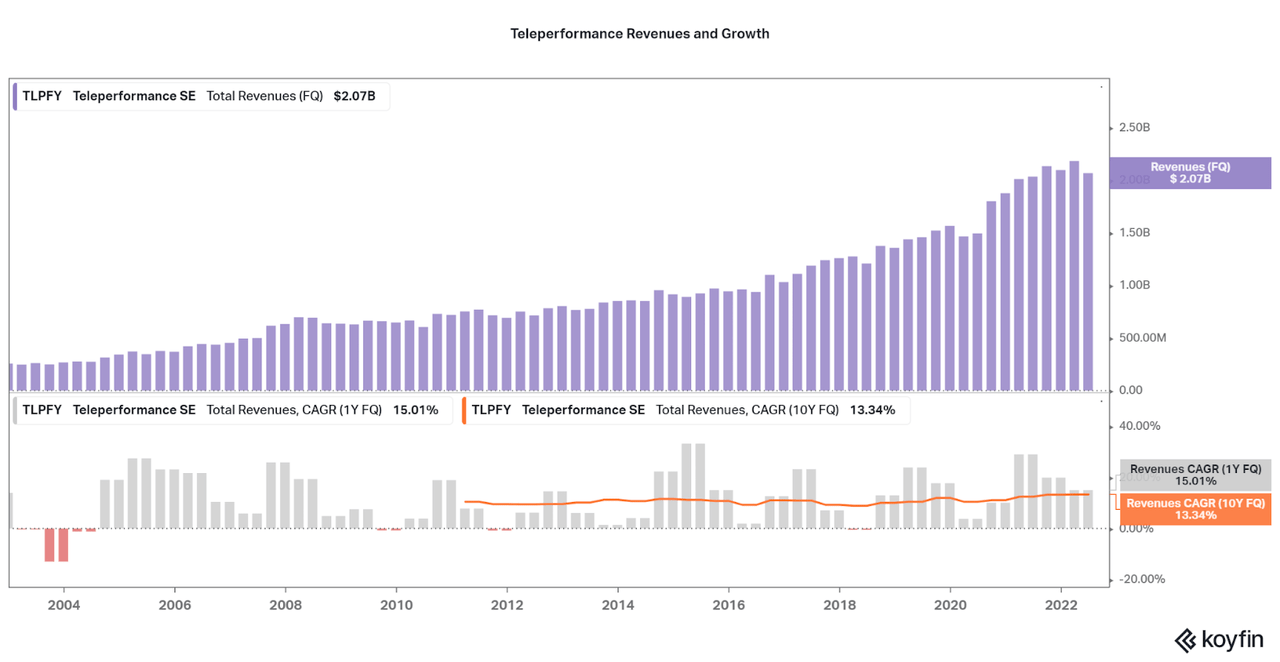

Teleperformance is in a transition phase and so I believe that financial performance will improve over time, however, revenue growth is one area that remains unaffected by the transition. Historically, organic or like-for-like growth (LFL), has remained below the 10% level until the pandemic, but a wide range of acquisitions over the years have boosted the average growth rate above 13.3%. This is evident by the seemingly cyclical revenue growth per quarter, but the variation can be more attributed to bolt on acquisitions rather than cyclicality. I will expect growth to remain strong as this Euro-based company earns favorable forex benefits here in 2022.

Koyfin Teleperformance Investor Presentation

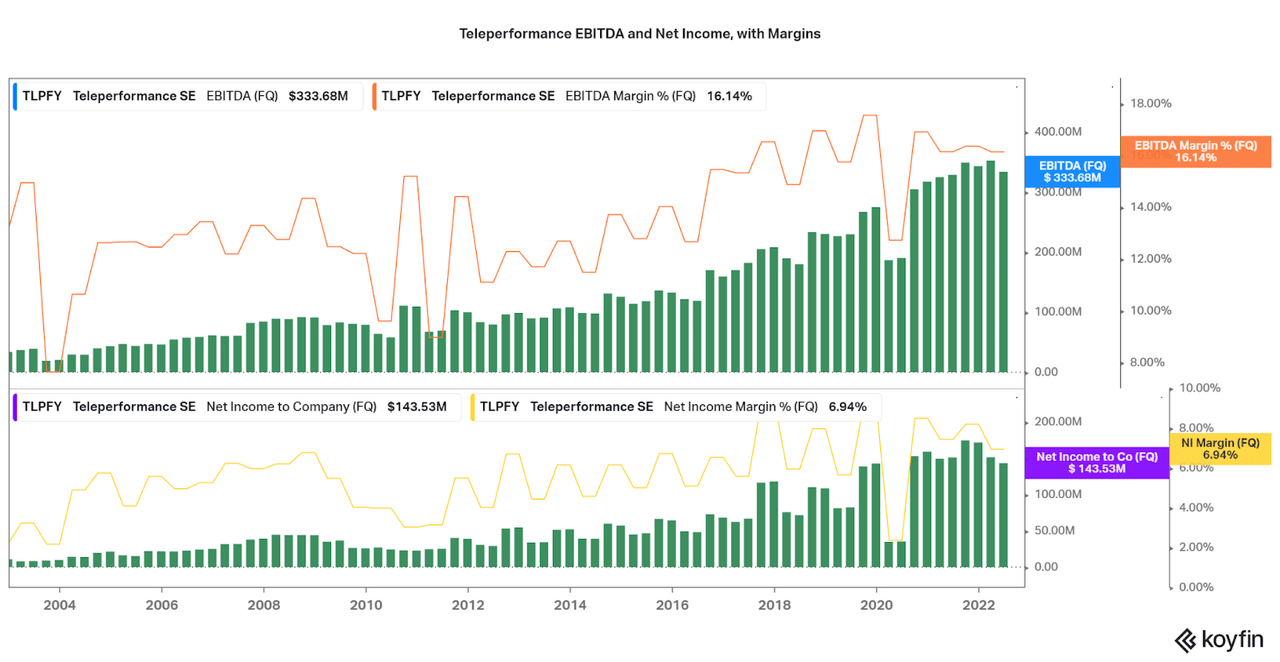

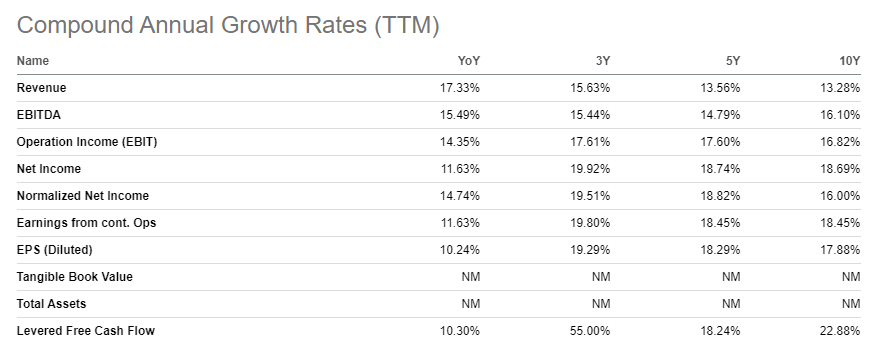

Where the money can be found is in the earnings data. As shown in the chart below, both EBITDA and Net Income margins have improved significantly over the past five years as more services that earn high margins are added to the platform. Now, TPF offers competitive margins that will be the basis of the long-term thesis when I compare to peers later in the article. For now, investors should look for continued profit margin improvements over time, leading to earnings to grow faster than revenues. This will be a continuation of the recent trend as depicted by the CAGR data shown in the second image below.

Koyfin Seeking Alpha

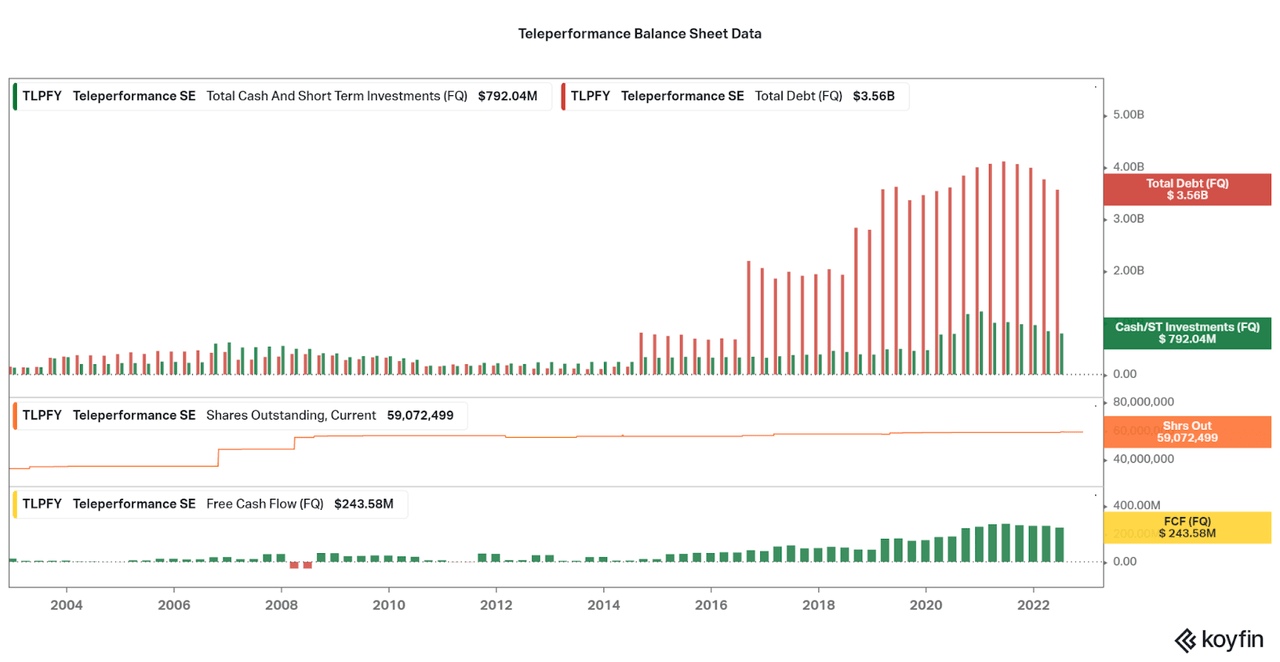

One risk point to consider, however, is the fact that debt was increased significantly through 2020. This has weakened the balance sheet, but debt is on the decline already over the past five quarters. Dilution has not been an issue though, and the earnings improvement can be directly impactful to EPS growth for investors. As margins improve with time, look for buybacks to occur that will allow EPS to grow even faster. I find the opportunity is quite significant as the company is maturing, but the thesis relies on continued improvements over time.

Koyfin

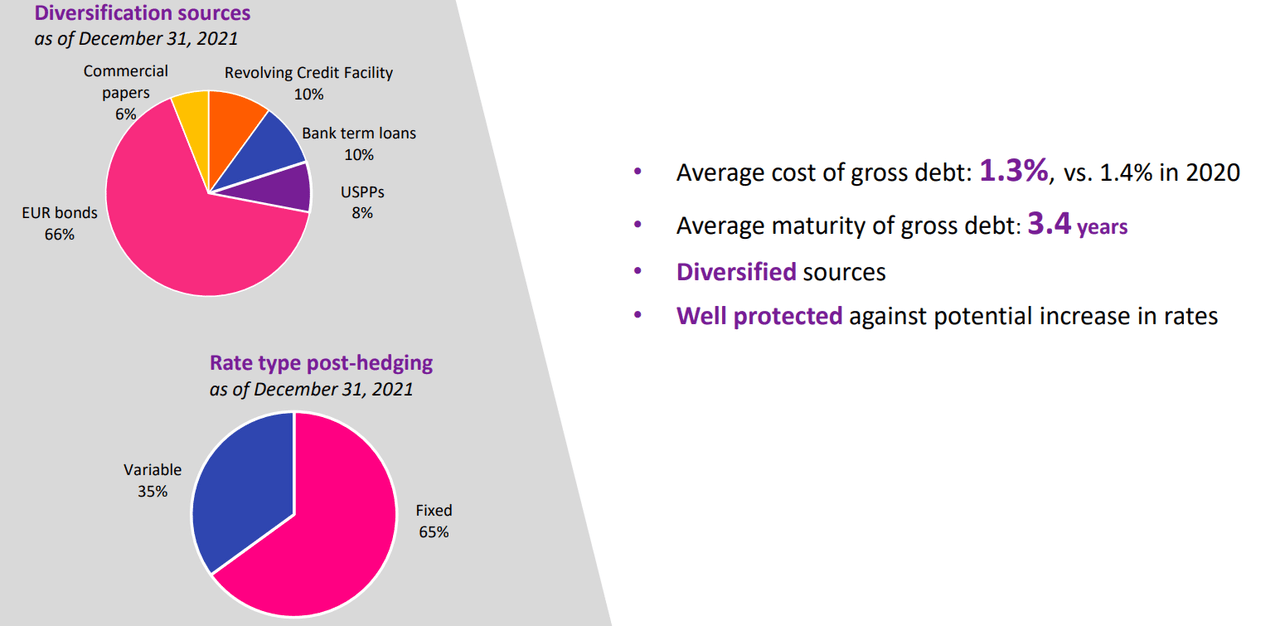

So far into 2022 performance has been strong, including a transformative 2021. First, TPF performed a key acquisition to enter into the healthcare industry, an area of high growth and available market. Then, leverage has decreased below a 2.0x level (allowing S&P Credit to increase the company’s rating). For a sub-$15 billion company, the credit rating is quite high and the investment should be considered relatively safe for most investors’ needs. It is also important to note that the average yield on the debt is only 1.3% and US-based peers may see higher interest rates at the same leverage ratio.

Teleperformance Investor Presentation

Valuation

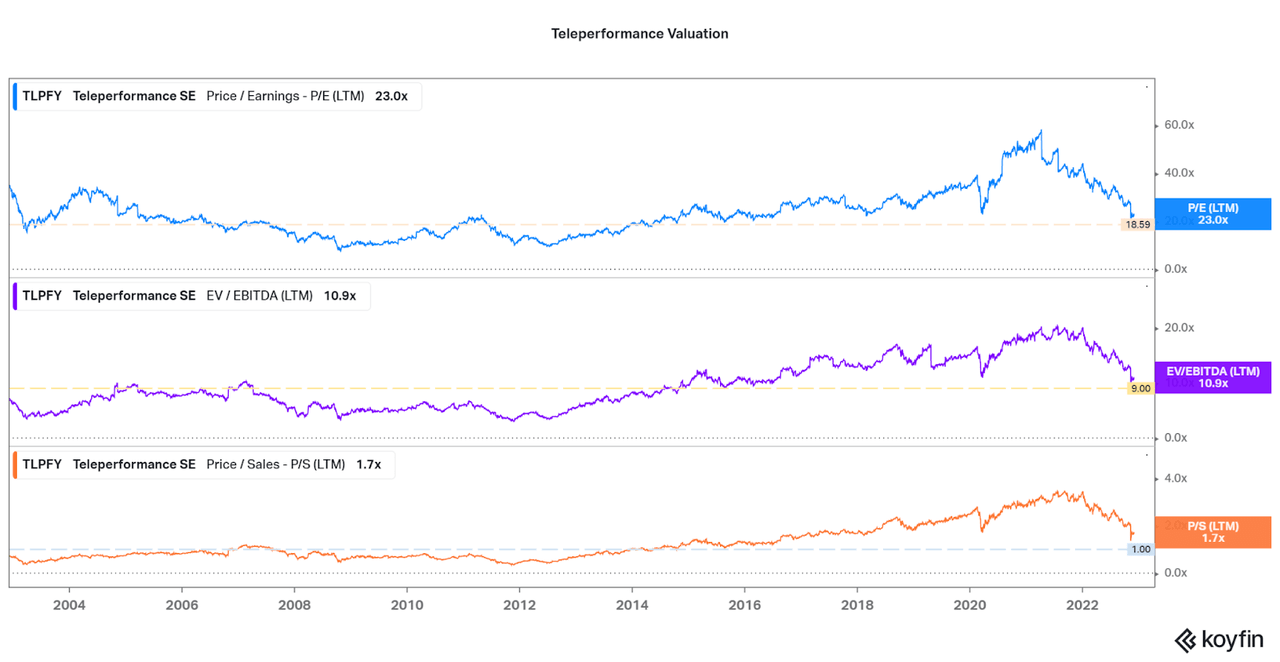

Despite the transformation into a more profitable and resilient company that is set to grow EPS at a rapid clip, investors must also consider the valuation. At the moment, I would state that the valuation is quite enticing at current levels considering the relative performance and state of the company. The current P/E of 23.0x is close to five-year lows as margins improve and the valuation falls. Even the increased debt has not led to EV/EBITDA to be considered overvalued at the current 10.9x level. On the chart below, I list general valuations levels that I would consider the best time to buy, but I do not necessarily believe shares will fall to that level. However, how does the current valuation compare to peers?

Koyfin

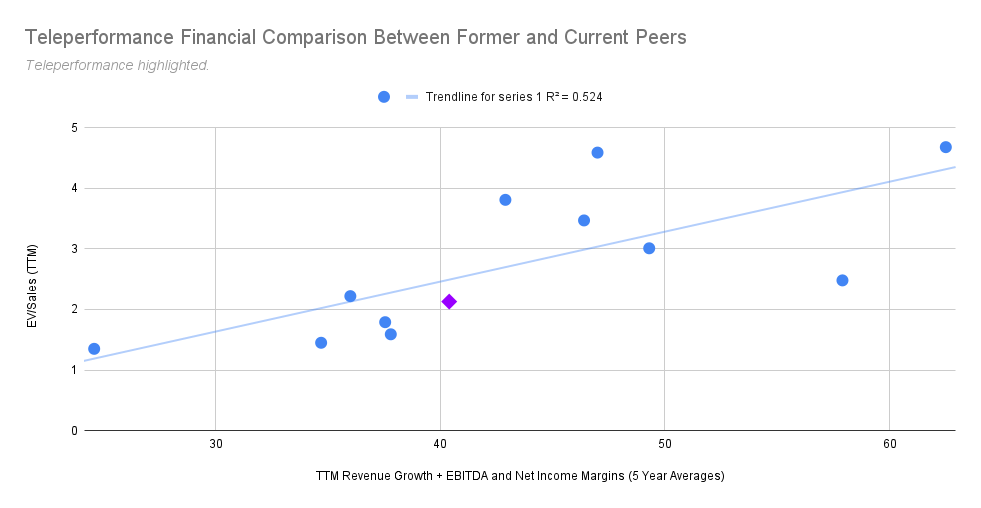

Using the company’s “Market and Competitive Environment” slide shown above, I compared the performance and valuation of Teleperformance to their current and historical peers. As such, the data is clear that Teleperformance’s current valuation is below trend, and that upon financial improvement and maturation, the valuation will rise significantly. This means that the company will begin to move diagonally up and to the right in the chart below. Therefore, I believe that Teleperformance offers one of the best opportunities in the industry at the moment and investors will see above-average returns moving forward despite economic headwinds.

Seeking Alpha data compiled by Author.

Conclusion

It is quite lofty of me to state that Teleperformance will outperform an industry that typically has offered low-volatility returns over the years. However, TPF is the only transition company that is actively expanding their services and proving this by an increase in profitability over time. This will lead earnings per share to rise faster than revenues that are already set to grow at approximately 10-15% per year organic and inorganic combined. Then, margins will increase in line with other business solutions providers, an increase of 50-100% over time. Lastly, with high profits come buybacks, and I think investors can consider a 5-10% reduction in shares outstanding overtime with a conservative buyback plan.

The thesis remains reliant on future performance and can be considered speculative, but even if current performance remains the valuation will allow for upside in my view. For now, I believe that those who would like exposure to the global tech-based customer experience and general business solutions industry can begin to add shares on a recurring basis and look to hold for years to come. I would say that it would be hard to predict short-term trading patterns for the stock, so the investment is more suited for longs. I hope my research is insightful and complimentary to your own due diligence.

Thanks for reading.

Be the first to comment