Blue Harbinger Research, Big Dividends PLUS Kumer/iStock via Getty Images

Healthcare is a diverse sector. And recent performance has been wide ranging (see data below). This is creating select, highly-attractive big-dividend opportunities ranging from individual pharmaceutical stocks, to healthcare-focused CEFs and even “healthcare” REITs, to name just a few. In this report, we review three particularly attractive big-yield healthcare opportunities. We begin with a special, the Tekla Healthcare Investors Fund (NYSE:HQH).

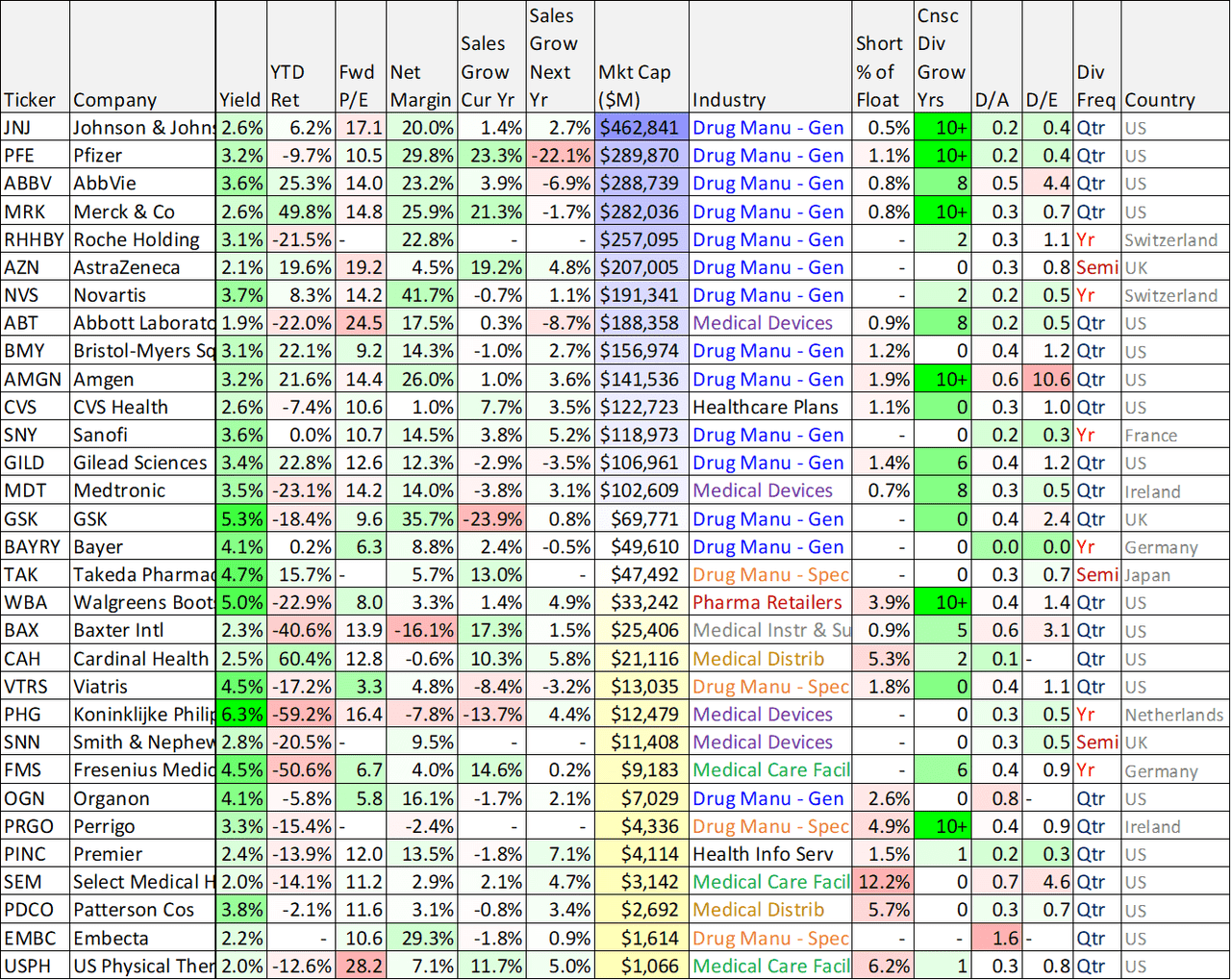

data as of 22-Dec-22 (StockRover)

(JNJ) (PFE) (ABBV) (MRK) (OTCQX:RHHBY) (AZN) (NVS) (ABT)

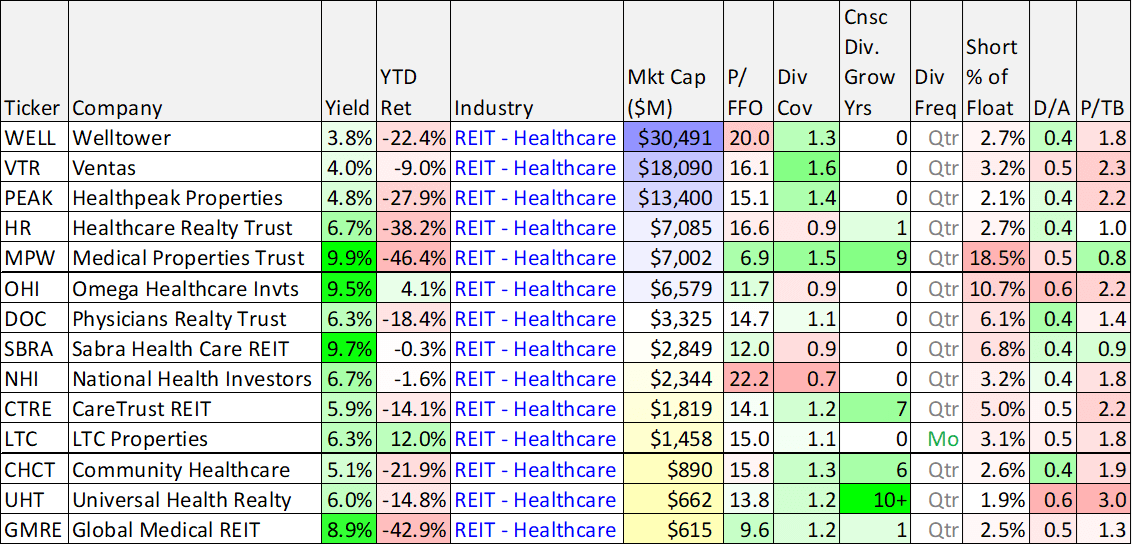

data as of 22-Dec-22 (StockRover)

(WELL) (VTR) (PEAK) (HR) (MPW) (OHI)

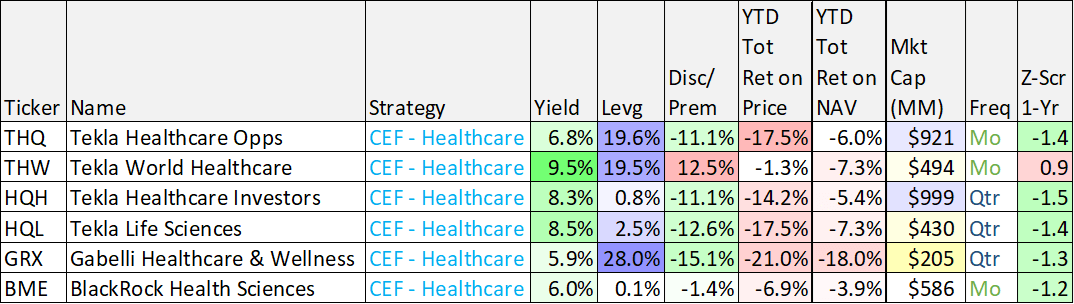

data as of 22-Dec-22 (CEF Connect)

(THW) (THQ) (HQL) (HQH) (GRX) (BME)

You likely recognize at least a few of your favorites in the tables above. You’ll also notice a variety helpful (hopefully) data points, depending on the type of investment, as well as year-to-date performance and current dividend yields.

With that backdrop in place, let’s get into some specific opportunities.

Tekla Healthcare Investors (HQH), Yield: 8.3%

Based in Boston, Tekla offers four closed-end funds focused primarily on the healthcare sector. The Tekla Healthcare Investors Fund is currently attractive for a variety of reasons. For starters, it offers exposure to a wide variety of healthcare sector companies (it recently had around 150 holdings, including stocks like Amgen (AMGN), Gilead (GILD) and UnitedHealth Group (UNH)), thereby giving investors some instant healthcare sector diversification.

Tekla Capital

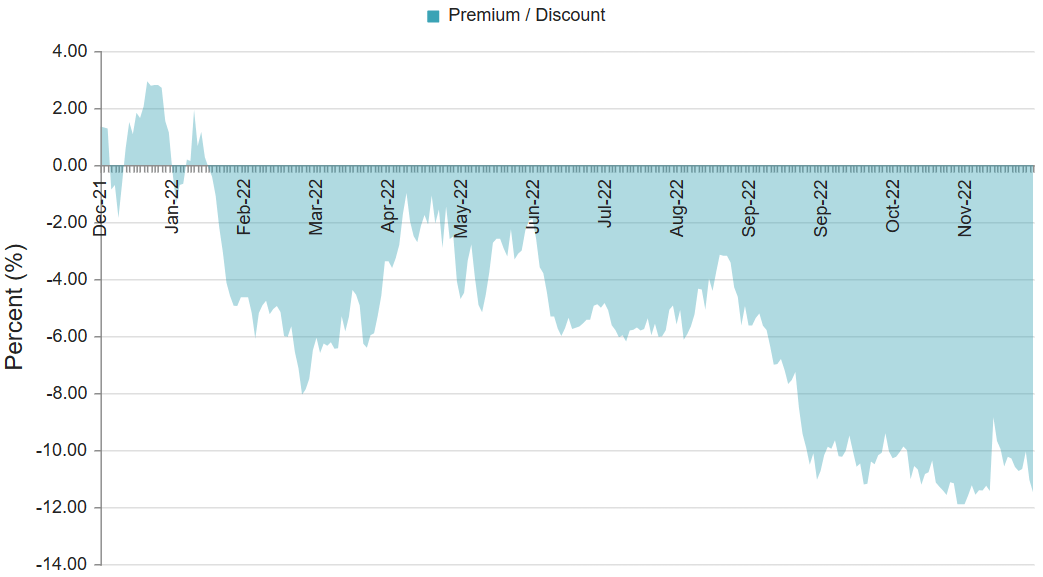

HQH currently trades at a ~10% discount to the value of its underlying holdings, or Net Asset Value (“NAV”), a wide discount by historical standards (the 1-year z-score was recently -1.5, arguably a good sign). Large discounts and premiums to NAV are a unique characteristic of CEFs (as compared to other mutual funds and exchange traded funds) and they can create unique risks and opportunities (we generally greatly prefer to buy attractive CEFs at large discounts).

HQH Current Price Discount to NAV (CEF Connect)

Perhaps one reason why this fund currently trades at a wide discount is because investors may have been hitting the sell button as the quarterly dividend (technically a distribution) was recently reduced.

Seeking Alpha

As a matter of policy, the fund has a managed distribution policy:

The Fund has a managed distribution policy (the Policy) which permits the Fund to make quarterly distributions at a rate of 2% of the Fund’s net assets to shareholders of record. The Fund intends, to the extent possible, to use net realized capital gains when making quarterly distributions. However, implementation of the policy could result in a return of capital to shareholders if the amount of the distribution exceeds the Fund’s net investment income and realized capital gains.

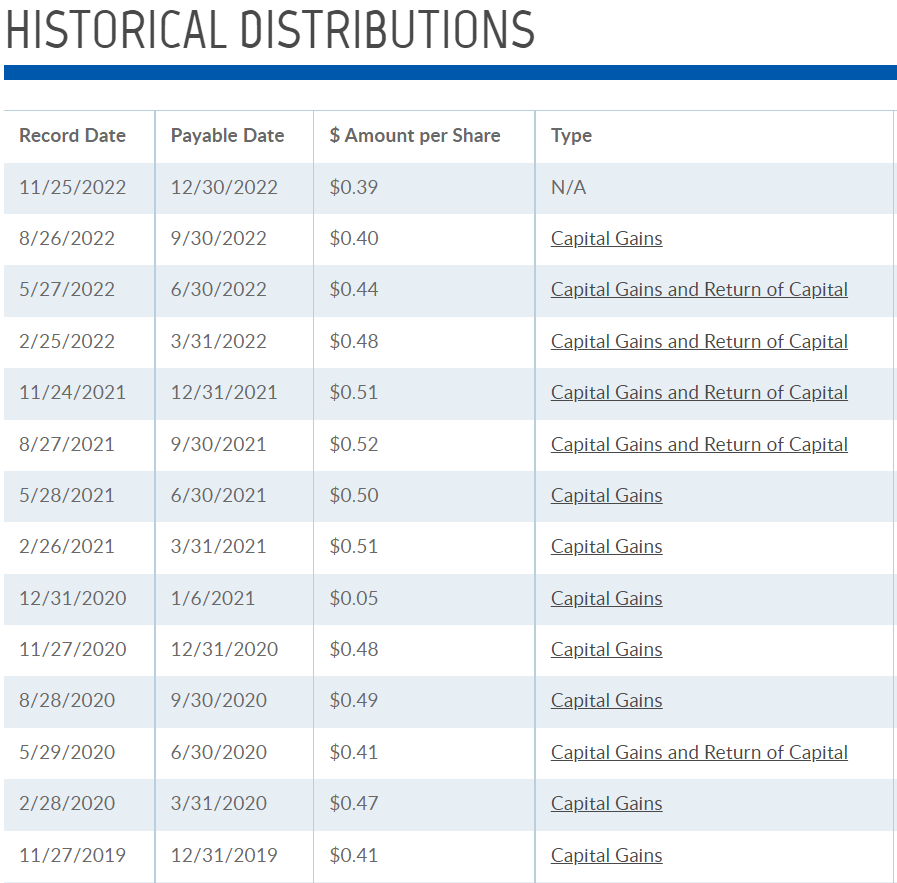

Another important consideration is the source of HQH distributions. As you may have guessed, not all of the distributions are sourced from income on the underlying holdings, but rather a portion can come from capital gains and/or return of capital. A portion from capital gains is expected over time, and a portion from return of capital (“ROC”) is also acceptable but should be monitored. Specifically, ROC can reduce your cost basis, thereby generating an unexpected capital gains tax if/when you do sell your shares. As you can see in the table below, the recent source of distributions has been mixed, but is acceptable in our view given current market conditions.

Tekla

Management fees are another metric that should be monitored for reasonableness. The management fee on HQH was recently 0.99% (reasonable) plus 0.20% in other expenses. This fund has recently been using close to 0% leverage (or borrowed money) which we view as a good thing (leverage can magnify income, but also magnify risks when the market gets volatile–like it has this year). Leverage is also expensive (especially with rates rising) and can add to a fund’s total expense ratio. The total expense ratio on HQH was recently 1.19%, which we view as acceptable for an actively managed CEF (view the fund’s management team here).

Overall, if you are an income-focused investor, we view HQH as attractive for its large price discount (versus NAV), its very low use of leverage (recently 0.85%), reasonable expense ratio (recently 1.19%), attractive exposure to the healthcare sector, and big distribution yield (paid quarterly). And if you like CEFs in general, we recently shared more CEF ideas here.

Gilead Sciences (GILD), 2023 Bonds, Yield: 5.0%

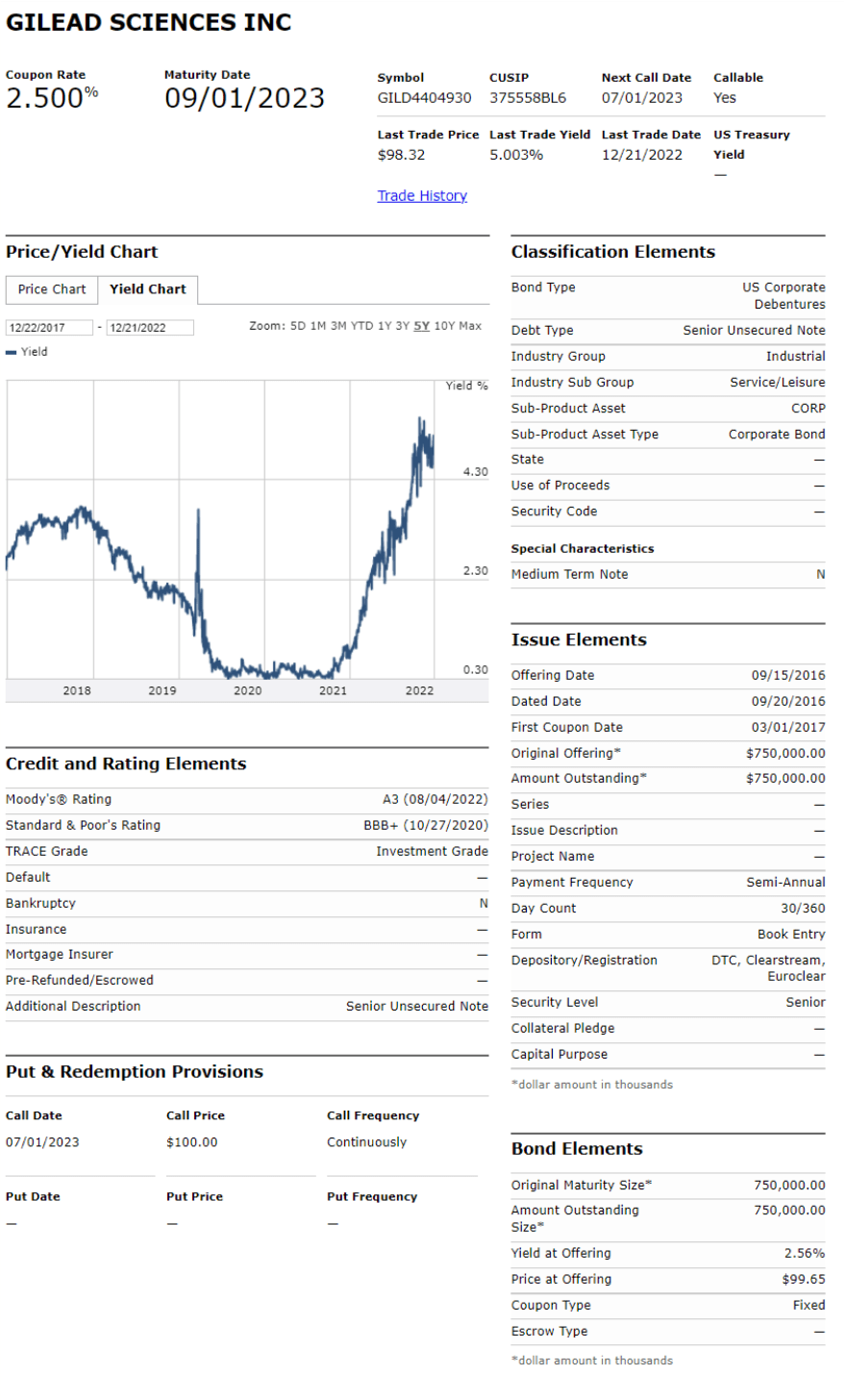

Gilead in a biotech company that offers a compelling yield on its common stock (currently around 3.4%), but considering the recent strong performance of those shares and the healthy valuation, we like the bonds more than the stock. Specifically, the September 2023 bonds are rated investment grade and offer an annualized yield of 5.0% (that is an amazing yield considering it was close to 0.0% just one year ago, as you can see in the chart below) as interest rates have been rising sharply.

FINRA-Morningstar

In particular, the bonds trade below par-so you’ll get some price appreciation in addition to coupon payment. Gilead is an extremely profitable business (thanks to its HIV drugs), but the pipeline is lackluster, and this is why we prefer these bonds that offer an attractive yield and mature in less than a year. Moreover, if you are uncomfortable with all the near-term volatility in the stock market, these income-producing bonds are highly attractive. We recently shared a variety of additional bond opportunities here.

Baxter International (BAX), Yield: 2.3%

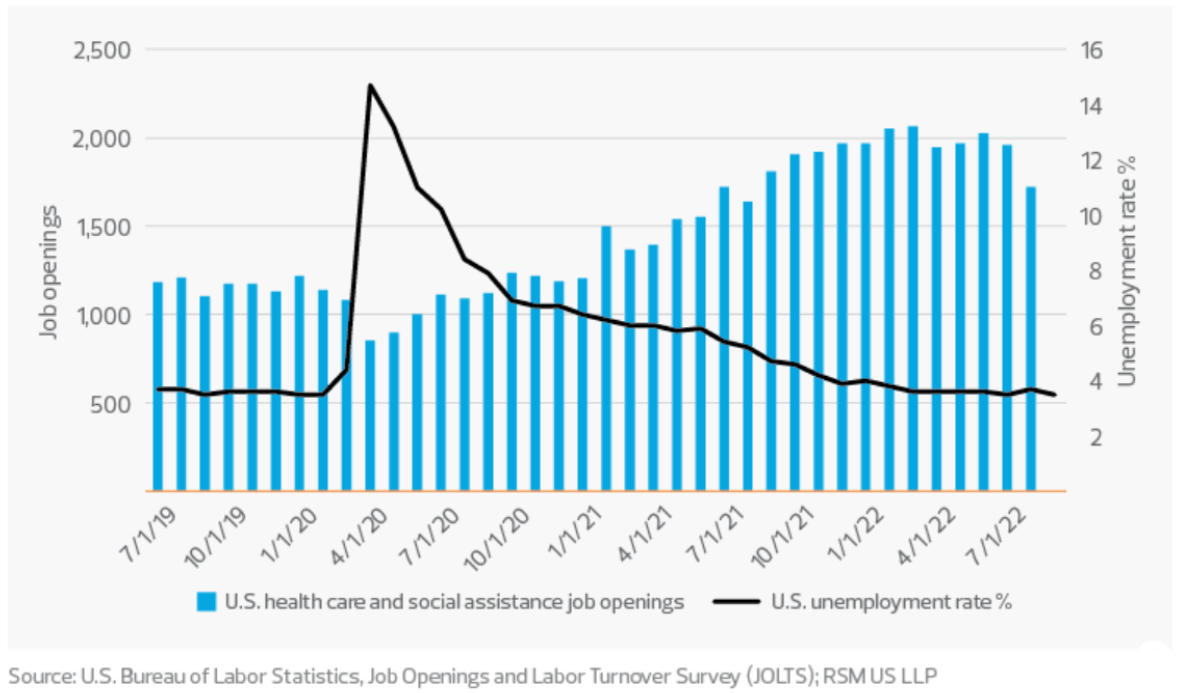

Don’t be fooled by Baxter’s relatively lower yield, it has significant share price appreciation potential and a long history of dividend strength. Baxter is an attractive healthcare equipment company, but the shares have fallen sharply this year as its pandemic recovery has been slower than expected. Specifically, many patients are simply scheduling previously-postponed surgeries at a slower pace due to healthcare staffing issues, inflation and lingering pandemic concerns. For perspective, here is a look at how healthcare job openings have remained elevated as the overall US employment situation has recovered.

RSM (Financial trends in the health care industry: Winter 2023)

Baxter will recover and continue to thrive, but in the near term, conditions remain slower. For example, Baxter announced third quarter results in-line with expectations, but lowered its full-year guidance as SG&A expenses rose (post-pandemic inflation). And this near-term slowdown has created an attractive long-term contrarian opportunity considering Baxter remains the industry leader in many of the products it offers, and it trades at an attractive earnings multiple (13.9x forward p/e). If you are a disciplined long-term investor, Baxter is worth considering.

Conclusion:

The healthcare sector is diverse, but currently offers a variety of select attractive opportunities, such as those highlighted in this report. And if you like the data and ideas in this report, we share more specific attractive opportunities in this new report: Top 10 Big-Yield Healthcare Opportunities.

And while big-yields can be very tempting (especially given the current market environment), it’s important to only select opportunities that are consistent with your own personal situation and goals. Despite short-term market volatility, we believe disciplined goal-focused long-term investing will continue to be a winning strategy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment