wonry

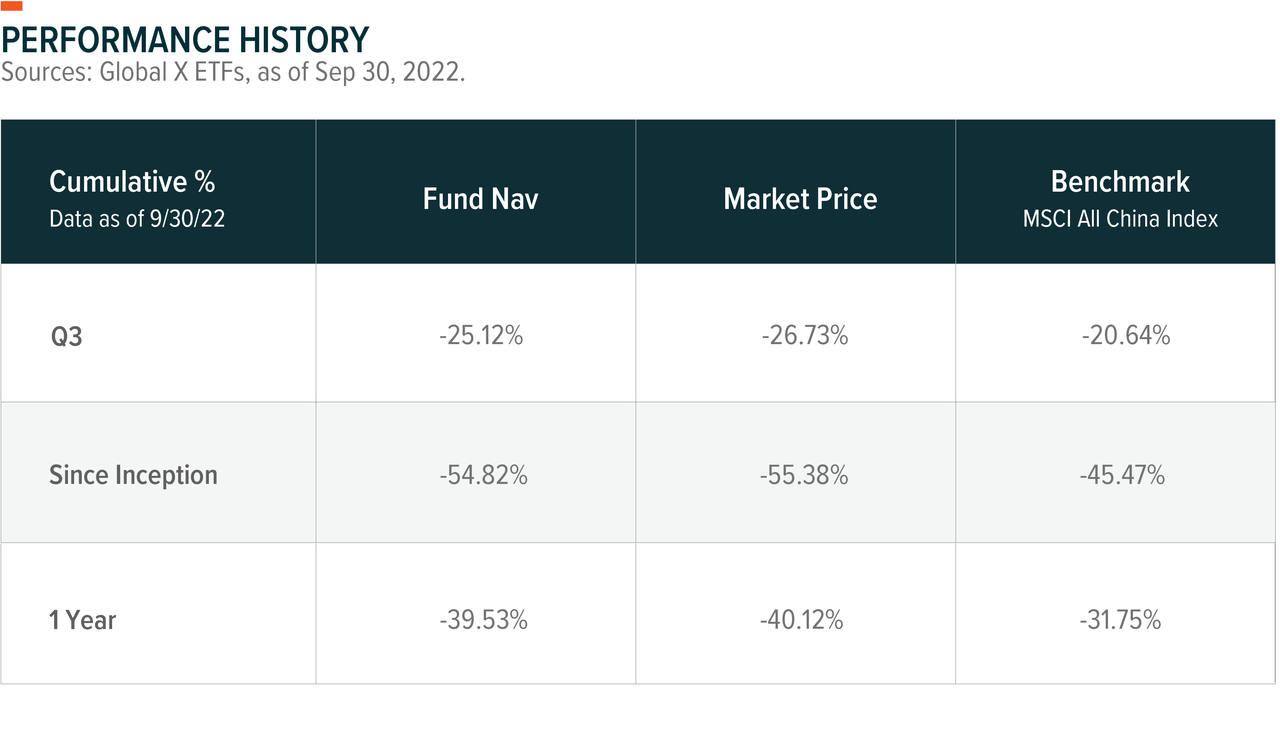

The Global X China Innovation ETF posted returns of -25.12% in Q3 2022. By comparison, the MSCI All China Index, which serves as the benchmark for KEJI, returned -20.64% over the same period. In this piece, KEJI’s portfolio managers discuss how China’s changing market conditions affected the fund and our strategy going forward.

The performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Returns shown for periods one year and greater are annualized. For performance data current to the most recent quarter or month end, please click here. Total expense ratio: 0.75%.

General Market Review

In Q3 2022, global and Chinese equity markets were in a bearish mood. Optimism towards Chinese equities after stellar performance in June 2022 was tested by volatility in July. Later in August, a deal between US and Chinese regulators to allow inspection of audit books came as positive news for Chinese ADRs, though implementation of the deal should be watched closely.

For the quarter, the China Securities Index 300, which is a cap-weighted index that tracks the top 300 stocks on the Shenzhen and Shanghai exchanges, returned -14.29%. The Hang Seng, a free-float cap-weighted index that tracks the largest companies on the Hong Kong Stock Exchange, posted -20.13% in Q3 2022.1

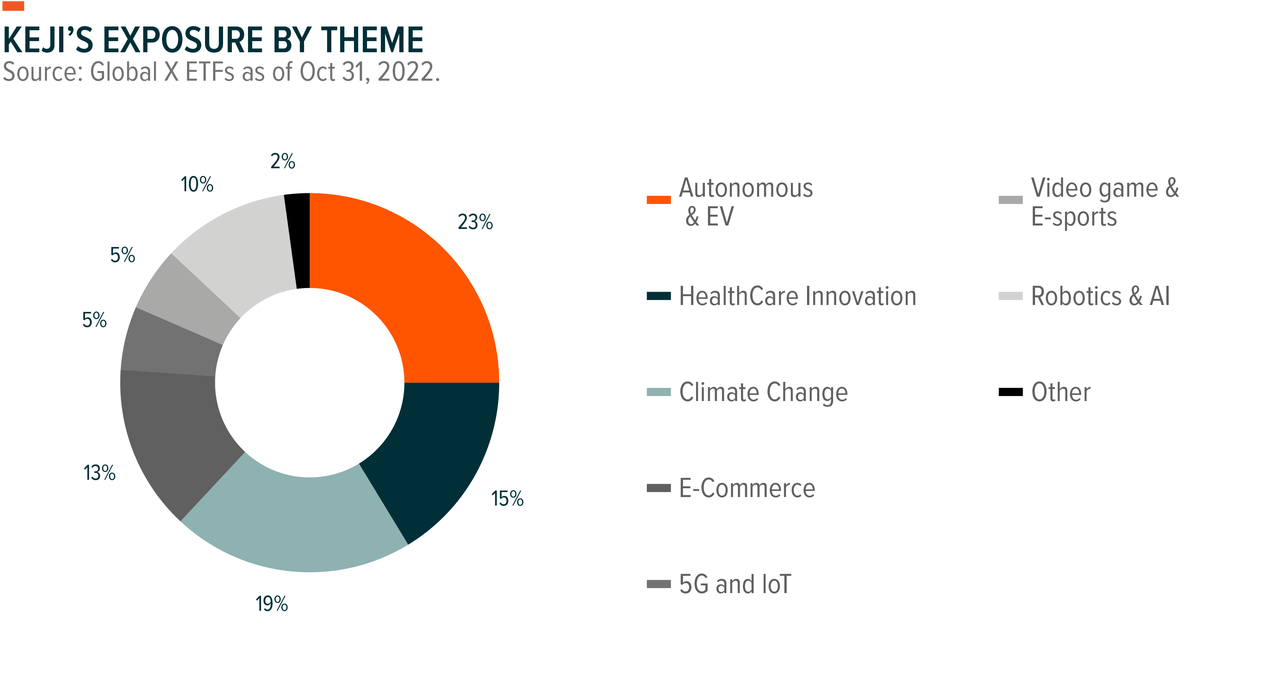

Within the portfolio, we maintain most of our exposure towards Autonomous and Electric Vehicles, Climate Change, and Healthcare Innovation.

Outlook and Strategy

The portfolio managers believe there was an overreaction in Chinese markets based on two points: 1) Chinese stocks were directly affected by US-China tensions, 2) China’s property downturn and zero-COVID policy put a lot of pressure on the economy.

KEJI has meaningful exposure to the EV, battery, and solar industries. Though recent market overreactions have resulted in negative performance for KEJI in Q3 2022, the managers still think there are mispricing opportunities on these stocks.

US-China Tensions Continue to Be Source of Concern for Investors

Over the last two months, the Biden administration has introduced a number of measures such as the Inflation Reduction Act (IRA), the CHIPS and Science Act, and the Executive Order (EO) for Advancing Biotechnology and Biomanufacturing Innovation. These measures include components that indirectly or even directly target segments of China’s economy. Market participants have been concerned by the risks presented by geopolitical tensions, and in some sense, this has been a major reason for our underperformance YTD. However, the portfolio managers believe this only provides greater opportunities in the near future.

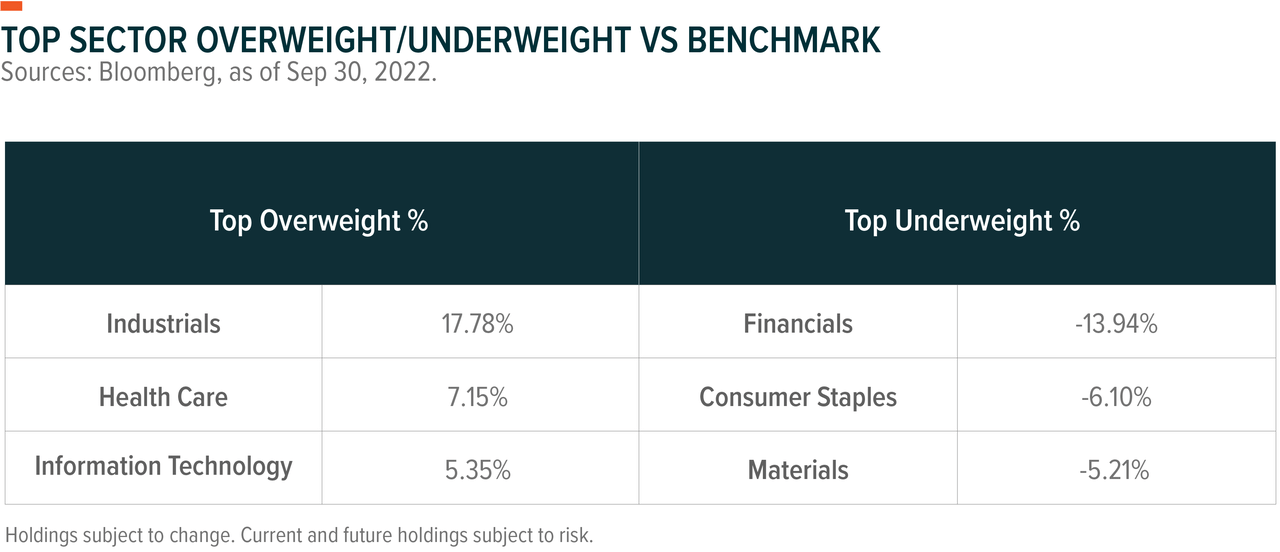

Given the US’ more dominant position in the semiconductor industry, the US can meaningfully hinder China’s development of semiconductors. For this reason, the managers do not have significant exposure to China’s semiconductor industry. However, it is a completely different story when it comes to the EV battery and solar industries, where the US does not have as much of a dominant position.

The IRA includes some actions to bolster the importance of these newly emerging industries. Success in EV batteries and solar energy requires manufacturing, which America has lost some ground in over the past few decades. For batteries, American-made batteries are likely to be much more expensive than Chinese-made batteries. On top of that, demand from the US is less influential in the global market than demand from China and Europe. For instance, in the electric vehicle market, 16% of vehicles sold in China were EVs, whereas only 5% of vehicles sold in the US were EVs in 2021.2

Chinese Battery Makers Maintain Advantageous Position

The battery industry is worth a closer look. Leading Chinese battery manufacturers could face added competition in the US over the coming years due to the expected growth in US battery manufacturing as a result of the IRA. That said, the managers expect the impacts to Chinese companies like CATL to not be as consequential as they can still export to the US and Europe and are likely to remain cost-competitive. Europe has welcomed Chinese investments and China can still export to the US market regardless of subsidies. In contrast, US-centric battery makers are less likely to export to other markets because their production costs are likely to be higher.

While there has been elevated policy uncertainty surrounding the role of Chinese battery companies in the US and subsequent bearish sentiment, growing demand for batteries and EVs continues to point to strong potential growth prospects globally. For instance, the world-leading battery maker CATL, one of the fund’s top 3 holdings, announced its Q3 2022 results ahead of schedule in early October with a profit range of 169-200% year-on-year.3

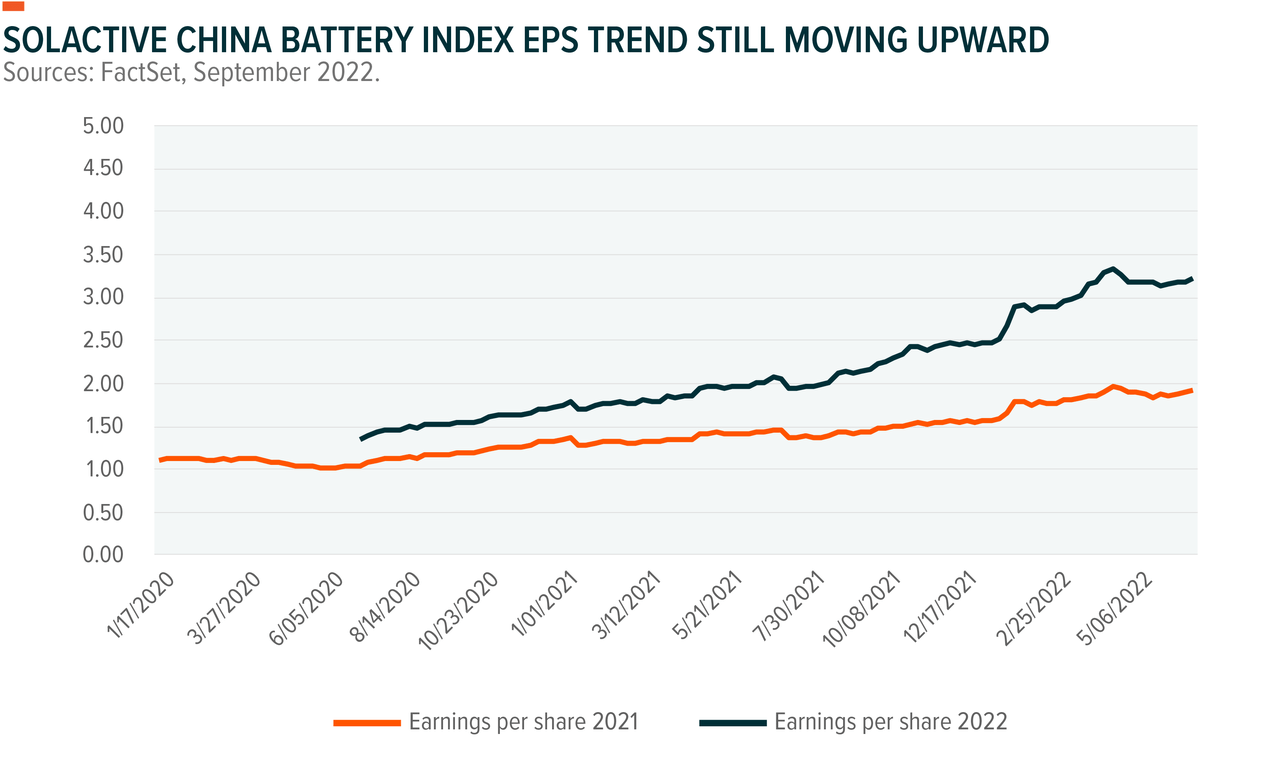

The Solactive China Battery index, which captures broader trends in China’s battery supply chain, is a useful reference. As of the end of September, it traded at 17x 2023 earnings per share (EPS), while the index is likely to deliver 32% growth in 2022 and 39% in 2023, implying 0.5 times price-earnings to growth (PEG).4 The index is cheap, in part due to policy uncertainty creating bearish market sentiment. The managers believe this bearish sentiment is misguided.

Relaxation of Zero-COVID Policy Could Alleviate Skepticism Towards China

Finally, when it comes to skepticism towards China, the managers broadly understand and agree with the near term outlook but hold a different view for the mid- to long- term. They believe China’s main headwinds right now are linked to the zero-COVID policy. Chinese households saved a lot during the pandemic. Their excess deposits since the start of the pandemic have accumulated more than 12tn Chinese yuan, amounting to 10% of GDP, according to Citi. Furthermore, local governments faced setbacks as they spent portions of their budget on quarantine-related expenses, which otherwise could have been used for investments in areas such as software, cloud, and other medical services. Currently, there is no clear answer as to when the zero-COVID policy will end. However, the managers believe it will eventually end, likely around March 2023 at the earliest.

Conclusion

The managers believe that misperceptions and skittishness are part of the reason why Chinese equities are so cheaply valued. In Q3, US-China tensions and the zero-COVID policy continued to push Chinese equities down towards lower valuations. If markets are indeed overreacting, this trend could create opportunities in the mid to long term.

Related ETFs

KEJI: The Global X China Innovation ETF is an actively-managed fund sub-advised by Mirae Asset Global Investments (Hong Kong) Limited that seeks to invest in companies that are economically tied to disruptive innovation in China. Disruptive themes targeted by KEJI may include advancements in technology, changing demographics and consumer preferences, and adaptations to the physical environment.

Please click the fund name above for current fund holdings and important performance information. Holdings are subject to change.

Footnotes

1. Bloomberg, L.P. (n.d.) [COMP function, total returns, as of 11/8/22]. Data retrieved on November 9, 2022 from Global X Bloomberg terminal.2. Olano, M, V. (2022, September 2). Chart: Which countries buy the most EVs? Canary Media.3. J.P. Morgan. (2022, October). CATL: Contemporary Amperex Technology Co Ltd.4. FactSet financial data and analytics. (n.d.). Solactive China Battery index data as of November 22, 2022. Data retrieved on November 22, 2022.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular.

Investing involves risk, including the possible loss of principal. The investable universe of companies in which KEJI may invest may be limited. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from social, economic or political instability in other nations. Emerging economic themed companies typically face intense competition and potentially rapid product obsolescence. Thematic companies may have limited product lines, markets, financial resources or personnel. They typically engage in significant amounts of spending on research and development, capital expenditures and mergers and acquisitions, and there is no guarantee that the products or services produced will be successful. KEJI is non-diversified.

As an actively managed Fund, KEJI does not seek to replicate a specific index. KEJI may invest in securities denominated in foreign currencies. Because the Fund’s NAV is determined in U.S. dollars, the KEJI’s NAV could decline if currencies of the underlying securities depreciate against the U.S. dollar or if there are delays or limits on repatriation of such currencies. Currency exchange rates can be very volatile and can change quickly and unpredictably.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. The market price returns are based on the official closing price of an ETF share or, if the official closing price isn’t available, the midpoint between the national best bid and national best offer (“NBBO”) as of the time the ETF calculates current NAV per share, and do not represent the returns you would receive if you traded shares at other times. NAVs are calculated using prices as of 4:00 PM Eastern Time. Indices are unmanaged and do not include the effect of fees, expenses or sales charges. One cannot invest directly in an index.

Since the Fund’s shares did not trade in the secondary market until several days after the Fund’s inception, for the period from inception to the first day of secondary market trading in Shares, the NAV of the Fund is used to calculate market returns.

Carefully consider the funds’ investment objectives, risks, and charges and expenses before investing. This and other information can be found in the funds’ full or summary prospectuses, which may be obtained at globalxetfs.com. Please read the prospectus carefully before investing.

Global X Management Company LLC serves as an advisor to Global X Funds. The Funds are distributed by SEI Investments Distribution Co. (SIDCO), which is not affiliated with Global X Management Company LLC or Mirae Asset Global Investments. Global X Funds are not sponsored, endorsed, issued, sold or promoted by MSCI, nor does MSCI make any representations regarding the advisability of investing in the Global X Funds. Neither SIDCO, Global X nor Mirae Asset Global Investments are affiliated with MSCI.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment