Avalon_Studio/E+ via Getty Images

Steel Partners Holdings (NYSE:SPLP) reported its second quarter results on August 5, 2022. Quarterly revenue per share increased by $1.03 after total earnings hit a record $441.41 million, representing an 8.8% rise (QoQ). In the Trailing Twelve months (‘TTM’) since December 2021, the conglomerate generated $6.10 as diluted earnings per share (‘EPS’) indicating an increase of 22.74% in the period. This report comes against the backdrop of SPLP’s agreement to purchase all common shares of Steel Connect (STCN) with the deal expected to close in H2 2022.

Thesis

Over the past year, SPLP has added 43.49% in gains even as investors remain uncertain over the company’s completion of the proposed merger with STCN. The company expects higher pricing of building materials to continue into the second half of the year. Higher demand for energy products is also expected to augment the shareholder value through the increase in earnings. Still, the company is faced with the challenge of significant volatility in product prices as well as demand that may hinder the increase in earnings.

Earnings Performance analysis

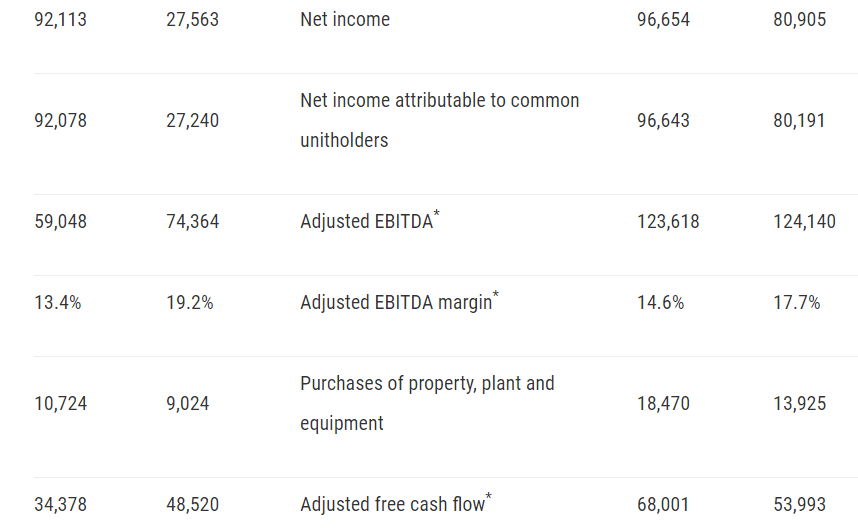

SPLP’s revenue increased 14.22% (QoQ) to $441.4 million leading to a rise of $146.227 million YTD or +20.86%. The 234.19% increase in net income (QoQ) to $92.1 million in Q2 2022 was dragged down by a 20% decline in the adjusted EBITDA and a 29.15% decrease in the adjusted free cash flow (QoQ). As we know the EBITDA includes the capital structure and the tax situation of the company, unlike the net income which excludes these aspects. A decline in the EBITDA, therefore, was accompanied by a decrease in the free cash flow as a result of higher capital expenditures.

Steel Partners

The lower cash flow was attributed to a dismal performance in the EBITDA although the management stated that it was offset by a better application of the working capital. Still, capital expenditures in the three months ended on June 30, 2022, increased by 0.1 percentage points of the revenue to $10.724 million or 2.4%. Apart from generating record revenue in the quarter, the company also managed to lower its debt and reinvest capital back into its business. Of importance, is that SPLP managed to reduce its total debt by 34.91% and its net debt by 49.19%.

Steel Partners sold off its subsidiary SLPE for $144.5 million to AEI, a subsidiary of Advanced Energy Industries, Inc. (AEIS). The all-cash transaction was completed on April 25, 2022, and the proceeds from the sale were used to lower SPLP’s debt levels in Q2 2022. SLPE formed the core basic element of Steel Partners’ industrial element, particularly in charge of designing, manufacturing, and marketing power conversion solutions. These products were used in the medical, lighting, and even audio-visual controls.

Stronger Pricing

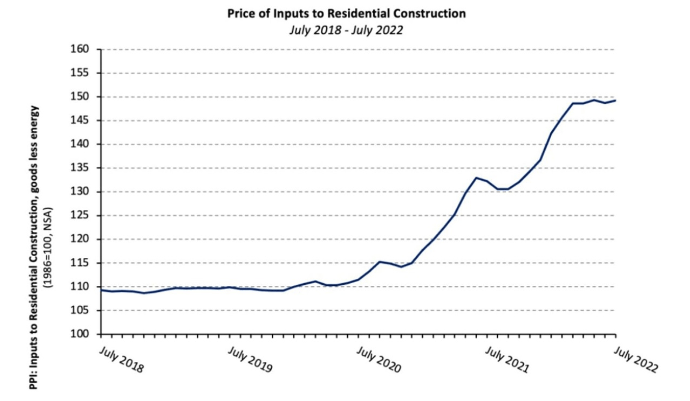

Despite the divestiture of SLPE, SPLP recorded an increase in sales by $27.1 million. The rise was attributed to the favorable pricing of building materials sold by the company in Q2 2022. In home building, the prices of building materials ticked up 0.4% in July 2022 with commodities such as lumber rising 2.3%. While prices of building materials have surged 35.7% since January 2020, approximately 80% of this increase was registered in January 2021.

National Association of Home builders

Prices of gypsum products have gained 7.6% through the first half of 2022 after soaring 23% in 2021. However, the price of steel mill products declined 3.7% in June 2022 with the index showing an overall decrease of 10.1% since December 2021.

Market Watch

HRC Steel Futures for November 2022 in the US have remained on an extended downward trend after it hit a high of $1600 in Q1 2022. It has since dropped towards the $850 mark as of August 2022 indicating a decrease of more than 40% (YTD). Companies such as the United States Steel Corporation (X) have declined 19.63% over the past year despite a 20% increase in its quarterly revenue to $6.29 billion.

The global market has generally weakened since Q1 2022 as a result of China’s Covid19 lockdowns and the conflict in Ukraine. These have augmented demand outlook uncertainty in 2022 and the beginning of 2023. However, the ending of the lockdown and resumption of business activities post-Covid is expected to raise the demand situation.

Investment Matrix

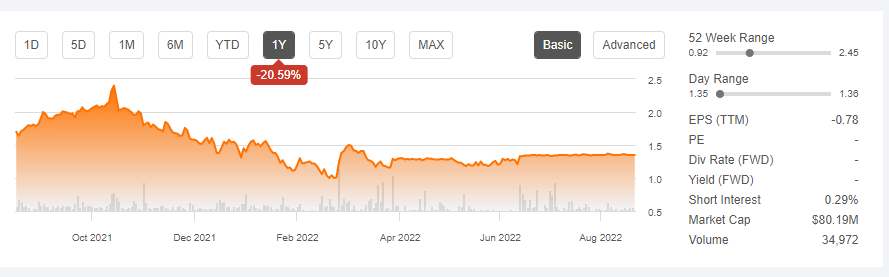

SPLP’s investment strategy includes among other things making opportunistic acquisitions, partnerships, collaborations, and restructurings that aim at improving its financial position in the long run. Since entering into a plan of the merger agreement with Steel Connect on June 12, 2022, SPLP has gained ⁓10% on year-to-date (YTD) analysis indicating shareholder optimism in the deal. However, the opposite is true with STCN which has since lost 9.50% (YTD) with its market capitalization stuck at $80.19 million.

SPLP’s agreement with STCN (as of May 27, 2022) considered $1.35 per share to STCN’s shareholders which at the time represented a premium of 12.5% over the stock’s closing price as of May 31, 2021.

Seeking Alpha

The stock has stagnated at $1.35 with all indications showing that the board of STCN will sign the agreement by the end of 2022. Another contingent benefit to be received by investors will be the right to receive pro-rata shares of the proceeds from the sale of the ModusLink business if this business exceeds $80 million. SPLP anticipates that it will sell the ModusLink business within two years after the completion of this combination. SPLP hopes to buy the remaining 52% of STCN within the second half of 2022 and it plans to first divest this business.

ModusLink serves the supply chain management market while also providing digital solutions to leading brands across the world. STCN’s quarterly results released in June 2022 indicated that various ModusLink facilities had been closed down in the third and fourth quarters of 2020 and Q4 2021. True to form, STCN has managed to reduce its net liabilities despite slow sales from this business but it has affected its gross profit level. Still, STCN’s main revenue has been attributed to the supply chain business which raked in about $51.548 million in the three months leading to April 30, 2022.

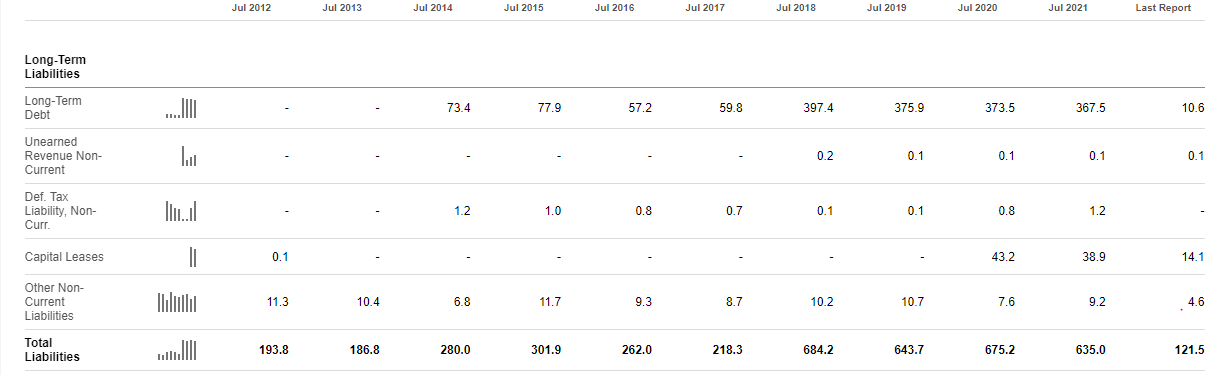

STCN’s total liabilities have declined 82% since July 2020 from $675.2 million to $121.5 million in June 2022.

Seeking Alpha

In the three months ended on April 30, 2022, STCN’s net revenue surged 4.28% to $51.55 million while gross profit declined 6.64%. The decline in gross profit is a result of an increase in the cost of revenue that increased by 7% in the quarter.

STCN needs to increase the number of clients accounting for its revenue and this forms another basis for its divestiture. In the nine months ending on April 30, 2022, the company increased its client base (among the 10 largest clientele accounting for at least 78% of its net revenue) by 1 percentage point (YoY).

For SPLP, the deal sweetener here is the benefit accruing from the net operating losses (NOLs) carry-forwards. STCN reported that it had accumulated NOL carry-forwards for federal tax uses (as of July 31, 2021) amounting to $2.1 billion. For state purposes, the NOLs stood at $110.0 million at the time. These NOLs arose in tax years ending on January 1, 2018. From a company’s viewpoint, the NOL acts as a valuable asset that the company can use to reduce its future taxable income.

Long-term STCN investors wrote a letter to the company’s board terming SPLP’s deal as an offer that substantially undervalues its tax assets. One point noted is that at the share purchase price of $1.35, STCN will be offering a 61% discount to the 48% stake purchased at $3.50 and a 45% discount to the 52-week trading high of $2.45.

About the NOL tax asset, STCN’s ability to use it to offset future taxable income will be affected by this ownership change. Under the company’s rule (that is section 382), any stakeholder with ownership of at least 5% who increases aggregate ownership by more than 50% points will limit the company’s use of the NOL. SPLP is eyeing this tax benefit as it presents a key asset for the company.

In my view, STCN will consider this offer since its usage of the NOL will be tied to the availability of sufficient federal and state taxable income in future years. STCN’s net income (attributable to common shareholders) in the three months ending on April 30, 2022, stood at $29.663 million up more than 100% after a net loss of $28.148 million incurred in the quarter ending on April 30, 2021. We should note that STCN’s ability to use its current NOL in future years solely depends on the amount of taxable income generated. Lower-income generation means that the company will be limited to using the NOLs and may run the risk of losing the tax assets permanently.

Additionally, STCN investors should note that other than the trading price, SPLP has also considered the volatility of its common stock, risk-free return rate, dividend and the maturity of the company’s note. All these support purchase of the stock under $2.00. Still the share purchase price is subject to consideration and approval by STCN shareholders.

Financial Risks to consider

SPLP recorded an 8.8% increase in the cost of revenues (QoQ) to $294.4 million up from $270.6 million recorded in Q1 2022. The company’s cash balance since December 2021 has also declined by 38.05% to $201.6 million. Cash used in operating activities in the six months ending on June 30, 2022, stood at $100.86 million. Capital expenditures in the same period were $27.356 million. Overall the company’s current cash reserve will be available for the next nine months until it requires new funding possibly in March 2023.

Failure to purchase the remaining stake from STCN may adversely affect the trading price of the stock while the vice versa holds true.

Bottom Line

Steel Partner’s offer to STCN appears a substantive deal considering the latter’s low-income levels. Still, minority shareholders may oppose the deal with the argument that it undervalues STCN’s overall worth. SPLP’s cash levels also registered a substantial decline since December 2021 despite selling its subsidiary SLPE for $144.5 million in an all-cash transaction. The company is using more cash in operating activities as well as capital expenditures that may require the company to raise more money in Q1 2023. For these reasons, we propose a hold rating for the stock.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment