DNY59

(This article was co-produced with Hoya Capital Real Estate.)

This past May 15, I wrote an article based on a then-recent note from Credit Suisse Investment Strategist Zoltan Pozsar.

Here’s just a tiny snippet of what I wrote in that article.

As Pozsar says, the message [of recent quotes from Bill Dudley, former President of the Federal Reserve Bank of New York], could not be clearer. What might this entail? Pozsar suggests that the Fed could go as far as engineering “a (covert) recession . . . in order to maintain price stability.” (Italics mine)

Not long after that, in roughly mid-June, the S&P index bottomed around the 3,636 range, and the Nasdaq at 10,565. Based on Pozsar’s observations, I felt at the time that the market might experience a small relief rally but then fall back again, possibly even to the 3,400 range on the S&P.

Sure enough, the market rallied. So far, so good. But then it continued to rally, doing so to a much greater extent than I would have thought possible. During the trading session of August 16, the S&P briefly touched 4,325 and the Nasdaq 13,181, roughly 20% and 25% above those June lows.

Some of this powerful rally came after the July, 2022 inflation number came in at 8.5%, surprising to the downside for the first time in a while. This likely led to the thought that we may have been on our way “out of the woods,” so to speak, in the battle against inflation. As for me, I left money on the table during this rally. While I was fortunate enough to increase my weighting in stocks fairly close to those June lows, I sold that additional weighting far too soon into the upturn.

Certainly, this was a humbling experience, and it caused me to spend a fair amount of time reading analysis from qualified sources I respect. In short, that review only strengthened my belief that the strength of the recent rally was a mirage, and that we are in for some fairly challenging times ahead.

Revisiting The World Of 4,818

The S&P 500 reached its all-time high of 4,818 during the trading session of January 4, 2022.

To properly understand some of the challenges ahead, it helps to take a brief look at how we got to 4,818 in the first place. Now, please do not take my reference to 4,818 to mean that there were no issues before January 4, far from it. At the same time, that high was achieved based on a set of economic circumstances that I will go on to argue may not repeat themselves in the foreseeable future.

Commentators on the recent rally have expressed the view that investors appear to believe that a “Goldilocks” financial environment can continue. Here’s one example, from Morgan Stanley.

These developments indicate markets may be counting on a “Goldilocks” scenario, where policymakers tame inflation with limited damage to economic growth and keep long-term rates low by historical standards.

Very briefly, let’s touch on the “Goldilocks” environment that got us to 4,818. We’ll start at the point of the Global Financial Crisis (GFC) in 2009.

Following the Global Financial Crisis, or GFC, in addition to lowering short-term interest rates to zero the Fed engaged in what is known as quantitative easing (QE). Normally, monetary policy this stimulative in nature would have led to inflation. And yet, the U.S. inflation rate remained low.

Between 2010 and 2017, the Consumer Price Index CPI ranged between 0.12% to 3.1%, averaging roughly 2%. In Goldilocks’ terms, this can be considered “just right”.

In 2018, inflation experienced a small upwards blip, to 2.44%. However, in 2019, inflation slid back below the Fed’s 2% target, dropping to 1.8%.

In 2020, COVID hit. This sudden shock to the economy caused yet more stimulus to be introduced. In combination, the effect of this was to both increase the money supply, as well as hold down longer-term interest rates.

In time, however, inflation started to raise its ugly head. The pandemic led to a drop in spending on services but a sharp increase in spending on goods, as people found themselves confined to their homes. Then came supply chain issues, followed by the war in Ukraine.

In spite of this, the Fed left monetary stimulus in place through the entirety of 2021, contending that such inflation would be “transitory” in nature. It was not until February 18, 2022 that the Fed approved a 1/4 percent interest rate hike.

However, the picture goes much deeper than the Fed. There were many other factors that could be described in “Goldilocks” terms that led to 4,818. In large part, these were geopolitical in nature.

Here is how Zoltan Pozsar expressed this, in a very recent note. He started by referencing cheap immigrant labor keeping service sector wages stagnant in the U.S., cheap goods from China, and cheap Russian gas. He capped it with this marvelously-worded explanation.

U.S. consumers were soaking up all the cheap stuff the world had to offer: the asset rich, benefiting from decades of QE, bought high-end stuff from Europe produced using cheap Russian gas, and lower-income households bought all the cheap stuff coming from China. All this has worked for decades, until nativism, protectionism, and geopolitics destabilized the low inflation world. (Italics mine, for emphasis)

In short, in the biggest of all pictures, for the past few decades the world trended towards globalization. Taking advantage of cheap labor and resources, strong supply chains were built. Goods were produced as cheaply as possible, then transported efficiently to the ultimate consumer. In the quote above, Pozsar refers to this as the “low inflation world.”

With respect to geopolitics, certainly there were several wars and other conflicts in specific areas of the globe. Nevertheless, there was at least what might be described as mutually-beneficial tolerance between the world’s major powers, notably the United States, China, and Russia.

The World of 4,818 Confronts Change

As investors, however, we must look forward as opposed to backwards, to the future instead of the past. Here, to me, is the million-dollar question (perhaps literally for some of us).

Do you believe the world of at least the near-term future will be the same world as the one that got us to 4,818?

Let’s briefly talk about two related reasons why it may be very difficult for this to be the case.

Challenge #1: Inflation – Including Monetary Inflation

Briefly, inflation becomes an enemy when the total funds available from money, income, and credit fuel an excess level of spending in relation to the quantity of goods and services that are available.

Think about that last sentence for just a minute. You have likely read about the sharp increase in the M2 money supply as a result of COVID-related stimulus. However, the contribution of excess credit at low interest rates must also be considered.

In short, an individual earns income from productive labor, whatever that may be. In addition to this, however, they may have access to credit. In the short term, this allows an individual to spend beyond his or her income. In total, all of that money chases goods and services. When there is an excess of this, inflation becomes an issue.

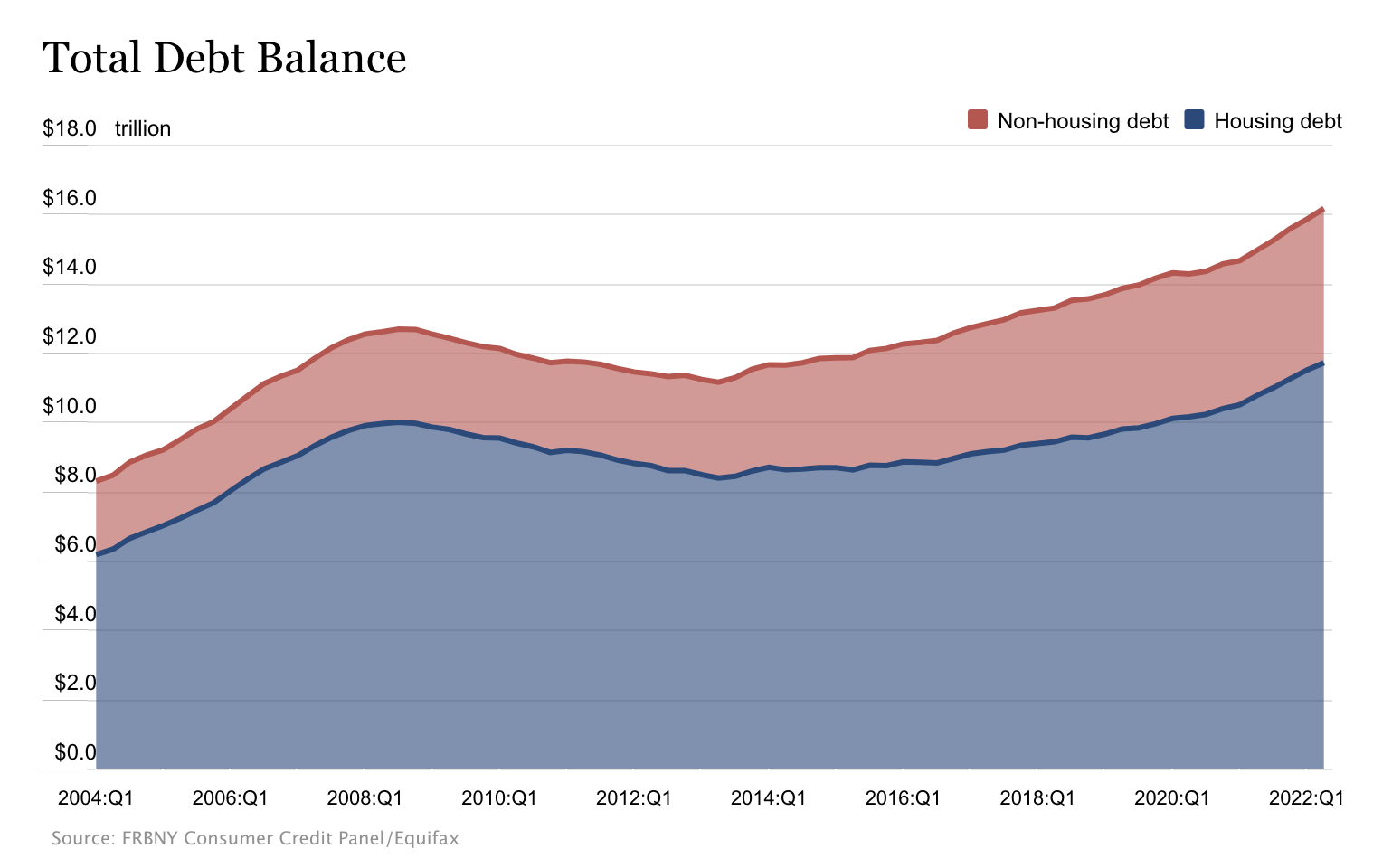

With that thought in mind, here is a look at the Q2 2022 report on total U.S. household debt, from the New York Fed.

Total U.S. Household Debt (Federal Reserve Bank of New York)

Looking at the graphic, it becomes clear that the overall amount of U.S. household debt continues to rise. In fact, during Q2 it increased by $312 billion (2%) to $16.15 trillion. This is $2 trillion higher than at the end of 2019, before the COVID-19 pandemic.

In addition to income, then, this growing amount of credit has contributed to inflation. Sharply rising housing prices, perhaps even more so than the rising stock market, have contributed to the inflation of household balance sheets. In other words, people feel rich, so they spend. And spend. And spend.

Here’s the specific issue, however, that seems troubling to me. It would appear that, whether spending on genuine needs or to maintain a desired lifestyle, the American consumer is turning to debt to an even greater degree.

Here’s an excerpt from the written summary provided with the above graphic.

Credit card balances saw a $46 billion increase since the first quarter – although seasonal patterns typically include an increase in the second quarter, the 13% year-over-year increase marked the largest in more than 20 years. . . . Auto loan balances increased by $33 billion in the second quarter, continuing the upward trajectory that has been in place since 2011. Other balances, which include retail cards and other consumer loans, increased by a robust $25 billion. In total, non-housing balances grew by $103 billion, a 2.4% increase from the previous quarter, the largest increase seen since 2016. (Italics mine)

Summarized, of the $312 billion increase in overall debt during the quarter, roughly one-third of that had nothing to do with housing, but related either to auto loans, credit cards, and other consumer loans.

How may this affect the stock market, and even the housing market, going forward? Simply put, it does not appear that the Pandora’s box of inflation will be easily closed.

In the opening section of this article, I introduced the thought that some may believe that, after a quick round of tightening, the Fed will “chicken out” and cut interest rates, perhaps even in early-2023.

As it happens, Minneapolis Fed President Neel Kashkari recently participated in a panel discussion, “Is the U.S. Headed for Stagflation?” at the Aspen Economic Strategy Group’s 2022 annual meeting in Aspen, Colorado.

I will simply say that, over the course of many comments, Kashkari painted that view as unrealistic. Here is just one brief snippet from his words:

The idea that we are going to start cutting rates early next year, when inflation is very likely going to be well, well, well in excess of our target, I just think it’s not realistic. I think a much more likely scenario is that we will raise rates to some point and then we will sit there until we get convinced that inflation is well on its way back down to 2% before I would think about easing back on interest rates.” (Italics mine)

In summary, unless one believes that we will quickly get back to an environment of easy money, further stimulus, and cheap credit, it will be difficult to quickly return to the world of 4,818.

Challenge #2: Geopolitical Shocks

As featured earlier, for decades now, we have lived in a world of increasing globalization, improving supply chains, and cheap resources (labor, goods, and commodities).

I won’t spend as much time dissecting this challenge as I did the previous challenge, that of inflation. All it takes is a couple of hours spent reading commentary from quality news sources to understand that this era is tremendously at risk, if not over for the foreseeable future.

In February, long-simmering tensions between Russia and the West (including NATO) became a “hot war” as Russia invaded Ukraine. Commentators suggest that this was inspired by Vladimir Putin’s world view of a Russia that assumes its rightful place in the world, as leader of a Eurasian empire that stands in opposition to the “decadent” west.

These events have had significant economic ramifications, and not in a good way. Europe, in particular, may be headed for an extremely difficult winter.

Meanwhile, China, under Xi Jinping, appears to be bent on reversing what Chinese refer to as the “Century of Humiliation“. Following reforms initiated by Deng Xiaoping that led to an impressive economic and military ascent, China has been flexing its muscles in Hong Kong. Additionally, recent events in Taiwan have led to the highest level of tension between the U.S. and China in modern history.

In short, all of these developments wreak havoc with the deflationary environment that prevailed for many years, contributing instead to inflationary pressures, such as broken supply chains, COVID lockdowns in China, and the like.

These issues, then, form a second challenge in quickly returning to the world of 4,818.

Putting It All Together

I don’t claim to know how all of this will play out any more than anyone else does. However, while I won’t go as far as calling what got us to 4,818 as a bubble, at the very least it would appear to be a confluence of circumstances that are likely a thing of the past, at least in the foreseeable future.

However, here are a few things to consider.

We may well be in for a multi-year period of volatility, similar to what we have experienced in 2022. Growth may slow, and inflation may prove more persistent than any of us would like.

Ironically, after the worst start to a year for the traditional 60/40 portfolio since the 1970s, bonds and TIPS may be getting more attractive. The income level across the board is higher. If the actions of the Fed have the desired effect, and inflation gradually subsides, returns from bonds and TIPS may help to stabilize one’s portfolio.

Finally, keep an eye on international stocks, and in particular those of emerging markets. While the road ahead will almost certainly be difficult, valuations are relatively low, offering the potential for gains for investors with a long-term perspective.

Thanks for taking the time to consider this somewhat lengthy article. I hope it has given you something to think about, and possibly even some things to argue about in the comments section below. I’d love to hear from you.

Be the first to comment