da-kuk

Author’s note: This article was released to CEF/ETF Income Laboratory members on October 6th.

In keeping with my covered call fund coverage, thought to do an article on the Nuveen S&P 500 Dynamic Overwrite Fund (NYSE:SPXX). SPXX invests in S&P 500 components, and sells covered calls on around 50% of its holdings. Doing so boosts the fund’s distribution yield to 7.3%, but reduces potential capital gains as well.

Structurally, SPXX is incredibly similar to the Nasdaq 100 Covered Call & Growth ETF (QYLG). SPXX is somewhat better structured, more tax-friendly, than QYLG, or at least tries to be. SPXX is a CEF, and currently trades with an atypical 8.5% premium to NAV. QYLG is an ETF, and so rarely trades with significant premiums or discounts.

In my opinion, SPXX is a reasonable investment opportunity, but not a buy at current prices and discounts. SPXX would become a buy at NAV, or at a discount to NAV.

SPXX – Overview

SPXX invests in all S&P 500 components and sells covered calls on 35% – 75% of its holdings, with a long-term target of 55%.

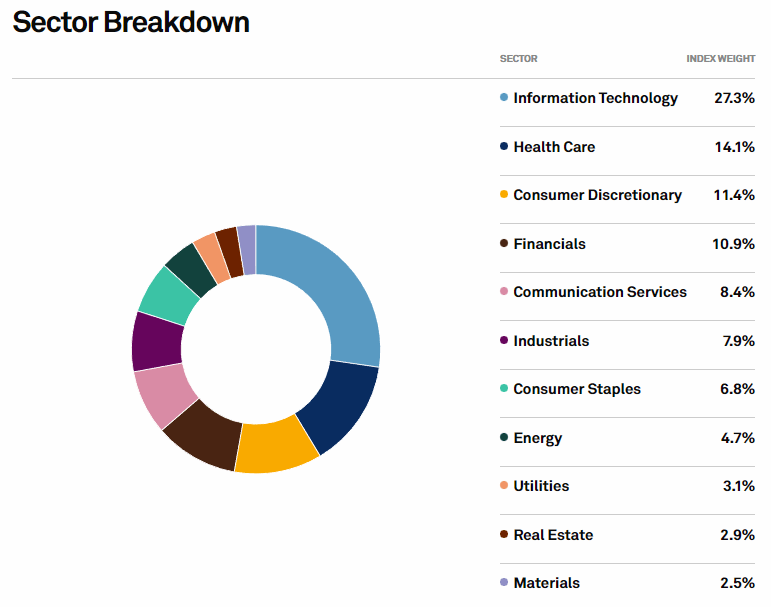

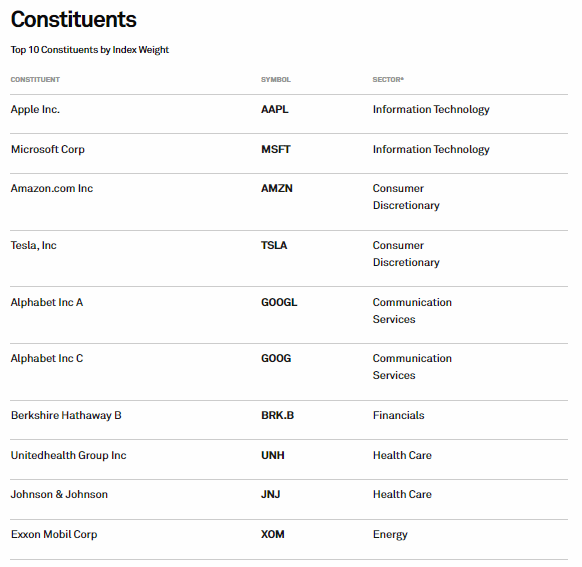

The S&P 500 is the largest, most well-known U.S. equity index in the market. It includes the 500 largest U.S. corporations, subject to a basic set of inclusion criteria. S&P 500 components are overwhelmingly large, blue-chip stocks with strong fundamentals. Components are reasonably well-diversified, although somewhat overweight tech. Index industries and largest holdings are as follows.

S&P

S&P

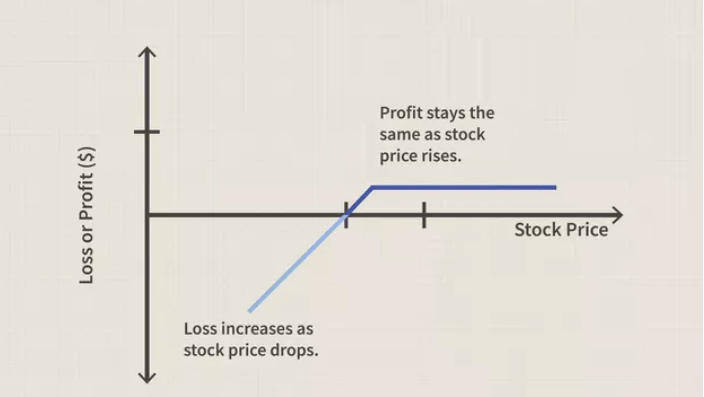

SPXX sells covered calls on around 50% of its holdings. Selling a covered call gives SPXX’s counterparty the right, but not the obligation, to buy the S&P 500 at a predetermined date, for a predetermined price. Selling a covered call generates quite a bit of premium for the fund, which then gets distributed to shareholders. In practice, selling a covered call means selling potential capital gains in exchange for higher distributions. Profits depend on market conditions, especially realized capital gains. In graph form, profits are as follows.

Investopedia

Selling covered calls has many important implications for the fund and its shareholders, some positive, some negative. Let’s have a look at these, starting with the positives.

SPXX – Positives and Benefits

Strong Distribution Yield

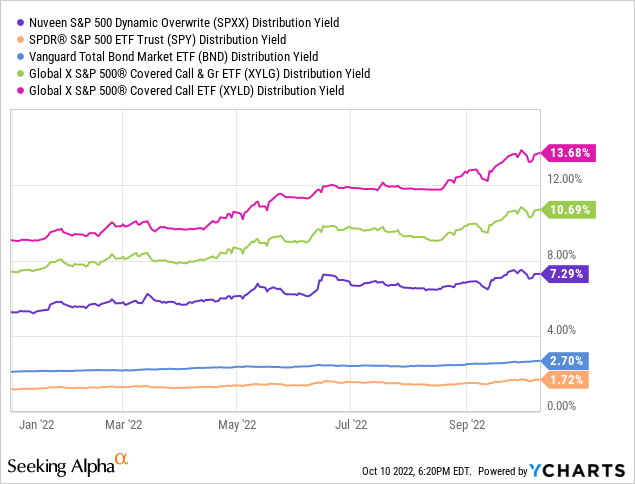

Selling covered calls generates quite a bit of income for SPXX, which then gets distributed to shareholders. The result is a strong 7.3% distribution yield for the fund, fully-covered by option premiums. It is a strong yield on an absolute basis, but somewhat lower than average for a covered call fund.

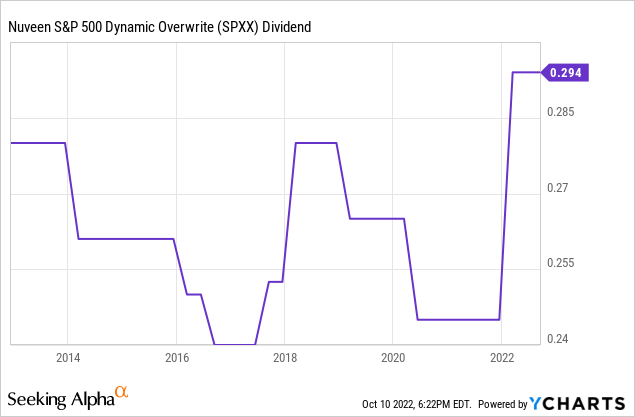

Selling covered calls is, in moderation, a reasonably sustainable strategy, so SPXX’s distributions are reasonably sustainable as well. SPXX’s distributions fluctuate quarter to quarter, but distributions have remained roughly stable since 2009, even grown a bit. There was a hefty 30% distribution cut during the financial crisis, but I don’t think that fund performance that far off to be all that material.

SPXX’s strong, fully-covered 7.3% distribution yield is a significant benefit for the fund, and its core investment thesis.

Outperformance During Flat Markets

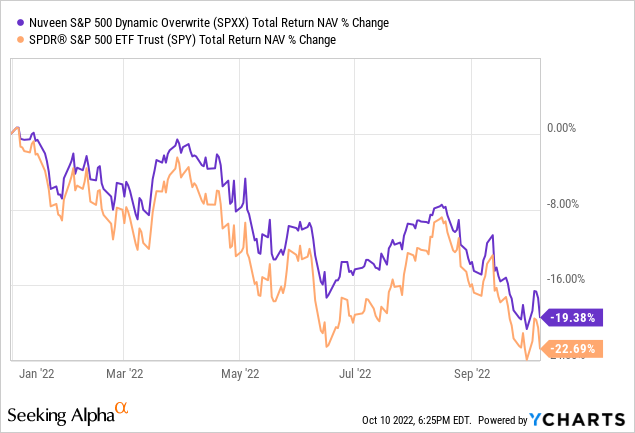

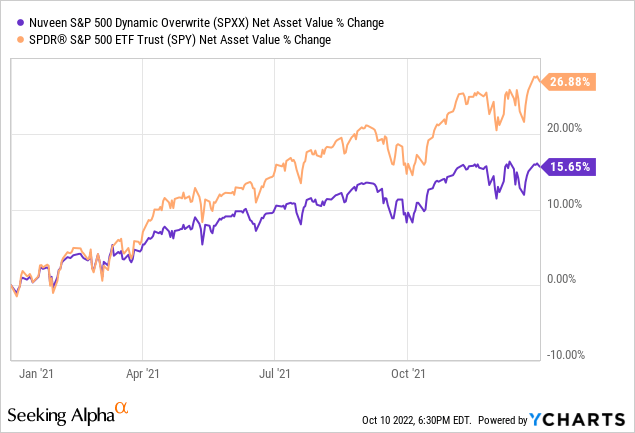

Strong distribution yields are always beneficial, but tend to be particularly impactful when capital gains are low, or when markets drift downwards. This has mostly been the case in the past for SPXX, but performance does vary somewhat from one would expect from a simple covered call strategy, almost certainly due to the fact that the fund is actively-managed. In any case, SPXX’s strong distribution yield has led the fund to outperform YTD, more or less as one would expect.

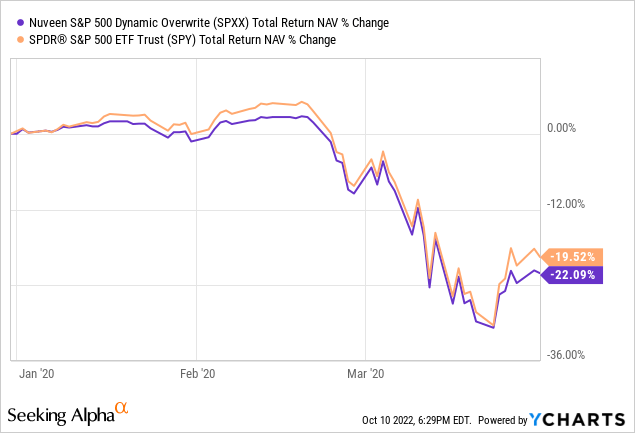

Importantly, SPXX’s strong distribution yield tends to be less relevant during more severe, sharper, downturns, as capital losses tend to swap distributions during these. SPXX, for instance, underperformed during 1Q2020, the onset of the coronavirus pandemic, and a very sharp downturn.

SPXX’s strong distribution yield should lead to further gains and outperformance if markets remain drifting downwards or flat, a benefit for the fund and its shareholders.

Actively-Managed Covered Call Strategy

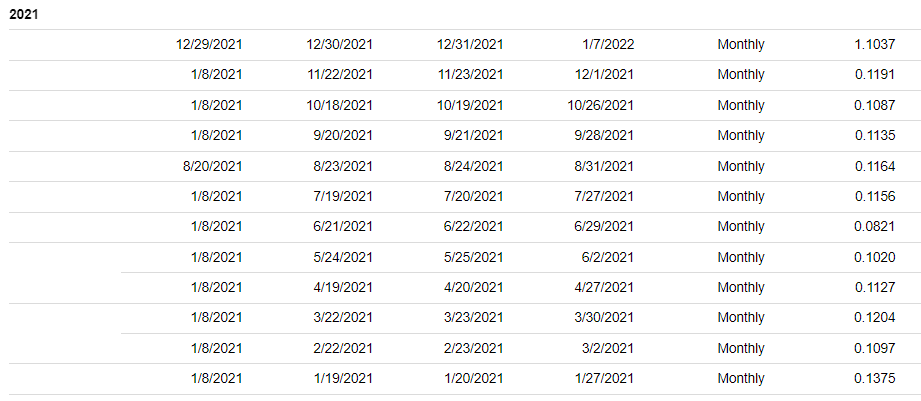

Selling covered calls is a relatively simple investment strategy, but one with important, complicated, tax implications. In certain / most cases, derivative and option profits must be distributed to shareholders, which is generally a taxable event. Option profits are quite volatile, so distributing option profits can lead to excessively volatile distributions. Some covered call funds, for instance, were forced into distributing quite a bit of excess cash to shareholders in late 2021. XYLG, the covered call ETF which is most similar to SPXX, paid a $1.10 special distribution in late 2021, almost ten times as high as the fund’s standard monthly distribution.

Seeking Alpha

These special distributions might have unforeseen, negative tax implications for shareholders, and complicate retirement planning regardless. Although I don’t see these distributions as significant negatives, investors can simply re-invest them where they wish, they do seem to be less than ideal.

SPXX attempts to avoid the issues described above, by only selling covered calls when the tax and distribution consequences of doing so are favorable to investors. Although I’m uncertain about the effectiveness of their attempts, I don’t see any forced special distributions in the fund’s history, so these seem to be adequate.

SPXX’s active-management strategy has been somewhat successful in reducing taxes for shareholders in the past, a benefit for the same.

SPXX – Risks and Drawbacks

Reduced Potential Capital Gains

SPXX sells covered calls on around half of its holdings. Doing so reduces potential capital gains by around 50%. Downside potential remains unchanged.

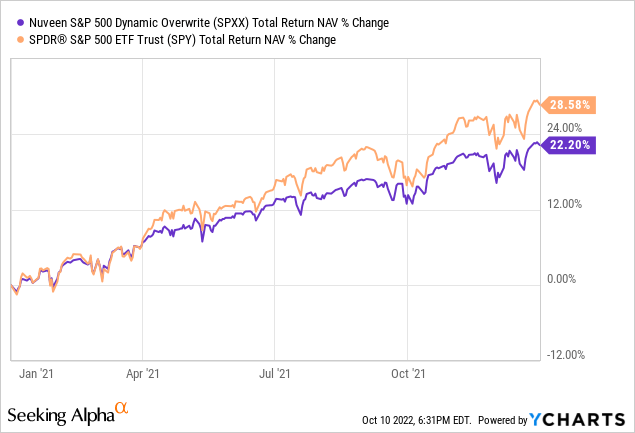

SPXX’s lower potential capital gains are a significant negative for the fund and its investors. Lower potential capital gains are particularly harmful during bull markets, as capital gains tend to be high during these. As an example, SPXX’s NAV per share appreciation was around 11% lower than that of the S&P 500 during 2021, a period of strong equity market gains. SPXX’s capital gains were lower than those of the S&P 500, although a bit less than expected.

Underperformance During Bull Markets

SPXX has a comparatively strong distribution yield, but comparatively weak potential capital gains. The net effect is dependent on market conditions. During bull markets, capital gains tend to be quite high, so the net effect tends to be negative.

As an example, SPXX underperformed relative to the S&P 500 in 2021, during which said index saw capital gains of almost 27%, and total returns of almost 30%. SPXX’s 7.3% distribution yield is quite strong, but no match for these returns, even after accounting for the fund’s partial / moderate capital gains.

SPXX’s underperformance during bull markets is a negative for the fund and its shareholders, and particularly important considering how common bull markets are. Stocks mostly go up, so reducing stock upside potential is rarely a good idea. Which brings me to my next point.

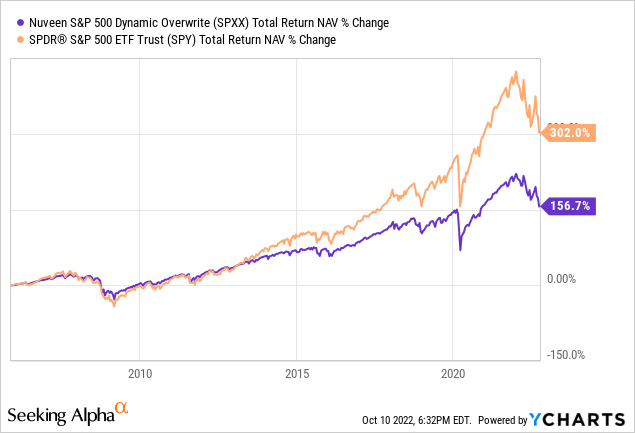

Underperformance Long-Term

SPXX underperforms during bull markets, but tends to outperform when markets move sideways or drift downwards. Bull markets are the most common market scenario, so SPXX should underperform long-term. This has been the case since the fund’s inception, as expected.

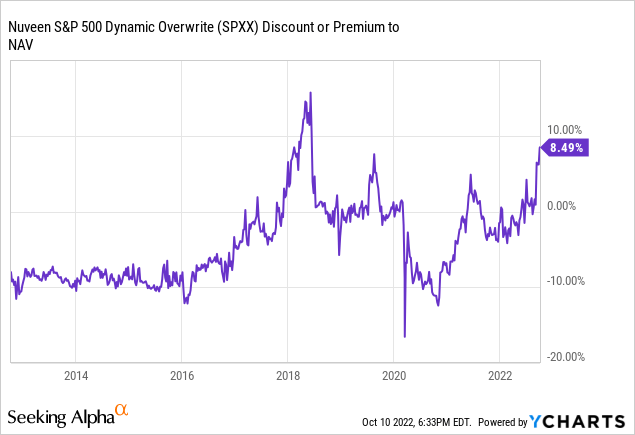

Above-Average Premium to NAV

SPXX currently trades with an 8.5% premium to NAV. It is a high premium on an absolute basis, and much higher than the fund’s historical average. SPXX tends to trade at NAV, or with a small discounts. Premiums are somewhat rare, and +5.0% premiums are incredibly rare.

In my opinion, waiting until SPXX’s premium comes down seems like the wisest course of action. No need to buy a fund with an uncharacteristically high price, especially in the middle of a bear market, were buying opportunities are plenty.

Conclusion

SPXX is an actively-managed S&P 500 covered call fund. SPXX offers investors a strong, fully-covered 7.3% distribution yield, but moderately reduced upside potential. Although the fund is a reasonable investment opportunity, it is not a buy at current prices and premiums to NAV.

Be the first to comment