Scott Olson

It is tough to do a market prediction because it will invariably be wrong; I am sure mine will be no different. However, the exercise is well worth going through as the direction of the broad market as well as what may succeed during the economic times is one of the primary drivers for overall stock performance. Knowing where the broad market is going has been utilized by traders for decades, best immortalized in the memoirs of Jesse Livermore in a Reminiscences of a Stock Operator. In this article, I look at the macro factors affecting the economy & stock market, the impact to corporate profits, the potential multiple for these profits as well as risks to this thesis.

Overall Market Environment

When we talk about market environment, there are really two to consider: the one for the economy and the one for stocks. The market economy does not always necessarily impact stocks, especially in a bull market. However, I do not believe that we are in a bull market anymore. Indexes, major contributors to it and the past bull market leaders such as Apple (AAPL), Tesla (TSLA), and other FAANG members are all rolling over, hitting lower lows and lower highs.

With the S&P down sharply already at over 20% from its all-time highs early in 2022, it could be argued that the markets have priced an economic slowdown. I don’t believe this has happened, largely due to the high market multiple still in place at almost 20x P/E ratio. This remains well above the mean and median levels the index has experienced over time and nowhere near the lows the index has traded at historically.

This is due to the Fed’s recent interest rate hike policy taking a lot of liquidity out of the market. The Fed has been raising rates very aggressively as the stated inflation rate rapidly increase to the 8% level and remains at 7.9%. Inflation has traditionally been driven higher as more money chases a finite number of assets; the increased rate of interest reduces demand as more money is needed to pay interest and demand drops due to this opportunity costs.

I believe that inflation this time is being less driven by this dynamic and more due to a massive decent in available supply. The worldwide government reaction to COVID, impairing the flow of goods and supplies, combined with the geopolitical response of the West to the Ukraine War, is drastically impairing the flow of goods, reducing the supply available. This should be a shorter-term headwind, assuming there is a resolution of some kind that will once again normalize supply chains. However, a longer and more devastating trend has been in place where the environmental movement has been systemically attacking both energy producers and material producers due to their perceived impact on the environment, best epitomized by the current ESG movement. This macro backdrop has meant companies that would traditionally invest to bring additional supply of commodities online have curtailed or ceased investment. These are capital intensive projects but if there are punitive tax measures or price caps to bringing supply online, companies in the commodities spaces are unlikely to bring these on due to the sheer risk. Add in a higher interest rate on debt needed to build the infrastructure to bring these products online, and this supply constraint is unlikely to change. No matter how high the Fed jacks interest rates, higher prices are here for at least the next 12 months, which is the scope of this article.

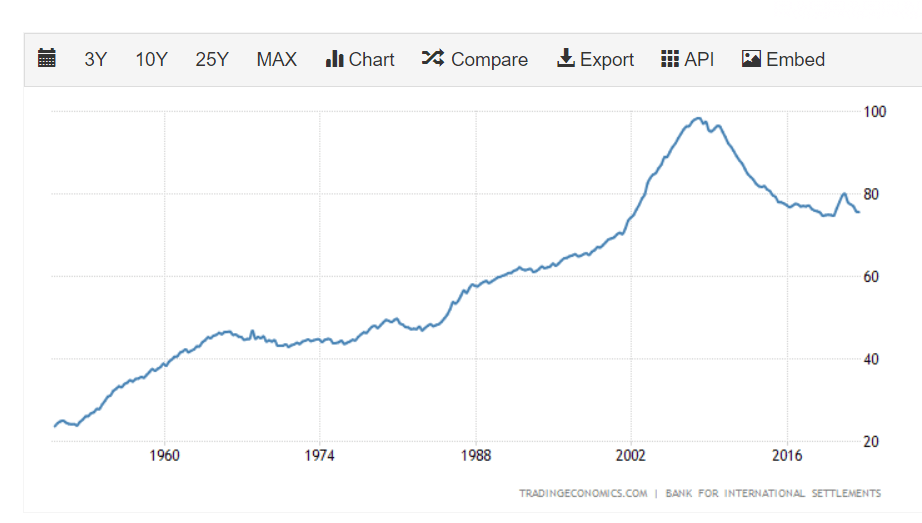

As noted above, higher interest rates are not going to fix the inflationary levels, at least as they have in the past. Interest rates are also going to be more punitive due to the massive debt levels that are now in place throughout all levels of society, from individuals to corporations to sovereign nations. Even the US, which is not as egregious as other western nations, have seen the average household debt to income almost double from the time of the Volcker interest rate hikes in the early ‘eighties.

US Debt to Income Levels (Trading Economics)

The Fed is now into the policy mistake area where they have increased rates to the point, they are extremely harmful to both individuals and corporations. I think they are going to continue with raises at least through the start of 2023, which is going to end up causing an earnings recession as company costs increase, both through the systemic inflation as well as their debt servicing costs.

I also believe we can expect continued high wage inflation. After years of depressed real wage growth, we have seen a dramatic reduction in available workforce. Some of this is due to demographics, with the baby boom generation now in their late 60s and 70s but some is also due to aftereffects of the fear from COVID-19 which has seen a large number of people leave the workforce. This demographic cliff was well-known, but it has finally arrived and will not reverse itself, even though immigration could help buttress its impact.

Add all this up, and all I see are massive drags on consumption for both individuals and corporations as their collective cost bases increase due to persistent inflation. This is not bullish for earnings in either direction.

S&P Earnings

Currently, the forward forecast from analysts expect earnings to be $232.53 for CY 2023. This is assuming a 5.5% increase in earnings from 2022 on an increase in revenues of 3.3%. This would seem to indicate that the entirety of the S&P is reaching critical mass with additional revenue giving rise to increasing margins. It also included a net profit margin of 12.3% which would be the second highest on record in the last 25+ years.

With massive number of companies announcing layoffs, it would seem that they do not see a lot of revenue growth in the near term which would be at least in the 6-12 month timeframe. If we assume flat revenue growth for next year (with a potential recession in H1 2023 offset by moderate growth in H2), that takes us down to an earnings estimate of $220.41 for CY 2023, assuming costs stay the same. Most consensus seems to think that the Fed’s rate increases are going to tame inflation; as I noted above, I think that they may be able to curb some discretionary spending but both wages and material costs are not going down anytime soon and may become more problematic with continued reduced capital investment hindered by the Fed’s interest rate policies.

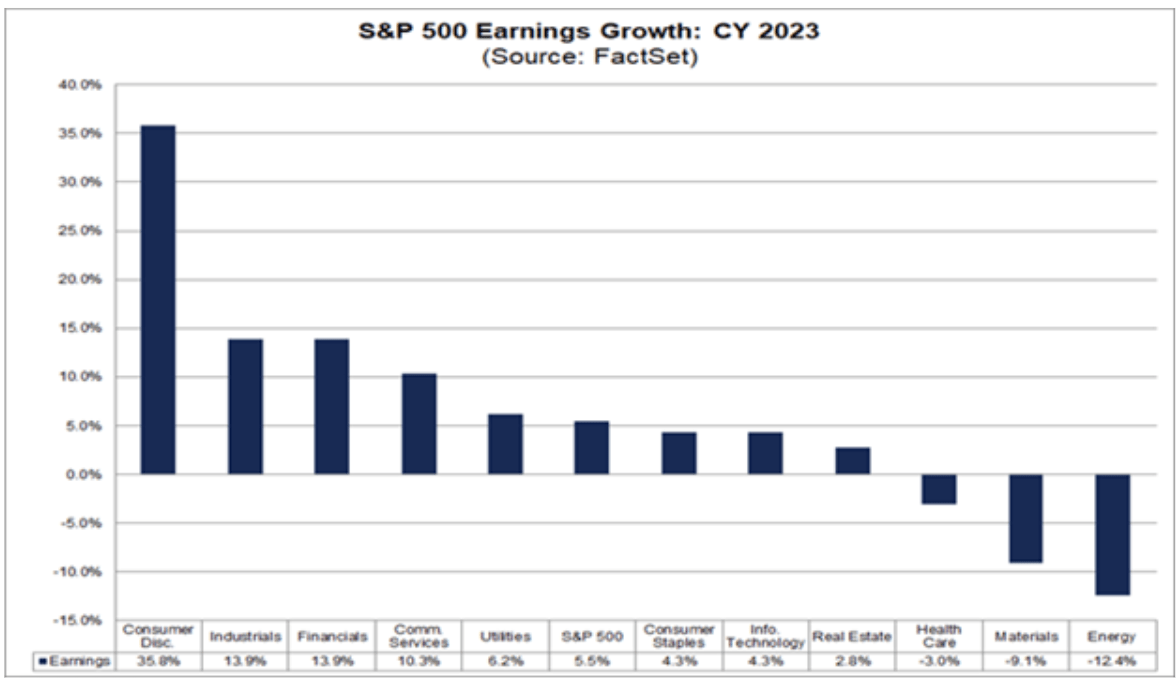

The Federal reserve currently is forecasting a drop in inflation to 3.4%. As noted above, I think that until the supply issues are alleviated, either through capital investment or improved policy, I have difficulty seeing how inflation can come anywhere near this target. Discretionary items have already but cut out of individual and corporate income statements already but the simple lack of supply for everything from food to energy and materials is not going to go away with interest rates. This becomes more concerning when we look at the earnings growth estimates for next year by sector:

2023 S&P Earnings Estimate by Sector (FactSet)

From this estimate, we can see that consumer discretionary (the thing to be cut from income statements) is making up a large part of the current estimate. Paradoxically, the items most likely to make profits from inflation are forecasted to be a drag on earnings. For simplicity, let’s assume inflation stabilizes at around 6.0% for the year; this is still 2.6% higher than estimates. If we add this to the cost base and reduce earnings by a commensurate amount, we produce an earnings estimate of $220.41 x (1 – .026) = $214.68 for 2023.

S&P Year End Multiple & Value

The important thing to remember is that the stock market is a forward-looking indicator. As bad as the earnings I am projecting above are, I think 2023 will see the bottom in stocks in H1 2023 as the implications of a higher inflation number, a mistake in Fed policy and an earnings recession in company Q4 2022 and Q1 2023 reports reveal how ugly things are going to be in the real economy. With this I can see the earnings multiple contracts from the current 17.8X Forward multiple to a much lower number. A comparative period would be the early eighties after the Carter Stagflation and the Volcker rate hikes when the P/E ratio was in the single digits. Because we still have a less restrictive interest rate environment (assuming rates are not hiked further than this), I could see the S&P bottom in H2 at a multiple around 10x, which would give a value of 2,146.80.

The intent here is to estimate where the index will be at the end of 2023. I think during the year the Fed realizes the error of its policies and will begin to cut rates in H2 which will improve everyone’s cash flows which should lead some re-rating. This will allow companies to also increase prices which should help pass on some of the structural inflation that will be built into the system. I do not expect any change to government policy, especially with a split House/Senate in the US so these inflationary policies should continue through 2023. I think you could then see a multiple bump up to 12-13x, which at 12.5x would give a year end value of 2,683.50.

Risks

The biggest risk to this forecast is the Fed’s policy. There is a chance they could reverse course and begin cutting immediately; this would not impact the H1 low but would certainly provide a tail wind to a higher multiple at year end as well as improved earnings if rates return closer to the zero-bound again. Alternatively, if the Fed does not realize it cannot impact inflation as much as previously thought and hikes anywhere close to past highs, it could really impair earnings and be very calamitous to the overall (and global) economy.

There is also a chance that the geopolitical environment alleviates itself; I think this unlikely as all sides seem very dug in and it more likely that a scenario where one or more of the combatants end up unable to contribute to the world economy which will only impact supply chains on a greater scale. I also do not see any move in the environmental mandates with Western nations as they are willing to inflict substantial short-term costs on their constituents despite an uncertain future return.

Be the first to comment