sykono

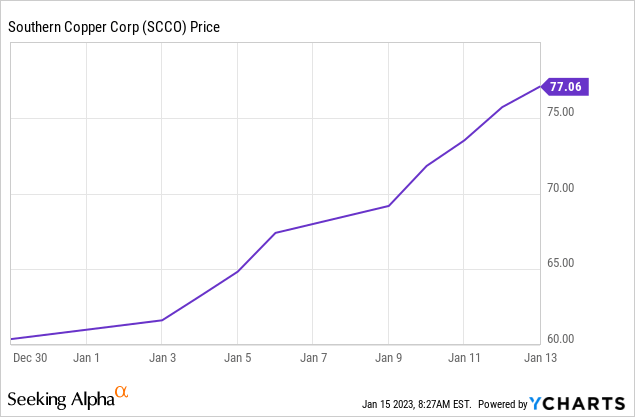

The U.S. dollar is falling, the price of copper is rising, and Southern Copper (NYSE:SCCO) stock is already up 25% over the first two weeks of this year (see below). Yet despite the stock’s meteoric rise, and the very strong fundamental backdrop, SCCO still trades with a forward P/E of only 23.7x while the $2.00/share annual dividend is good enough for a 2.6% yield. China is opening up, and the EV transition is accelerating. The point is the bull-run in copper – and SCCO stock – is likely far from over. Let’s take a look.

Investment Thesis

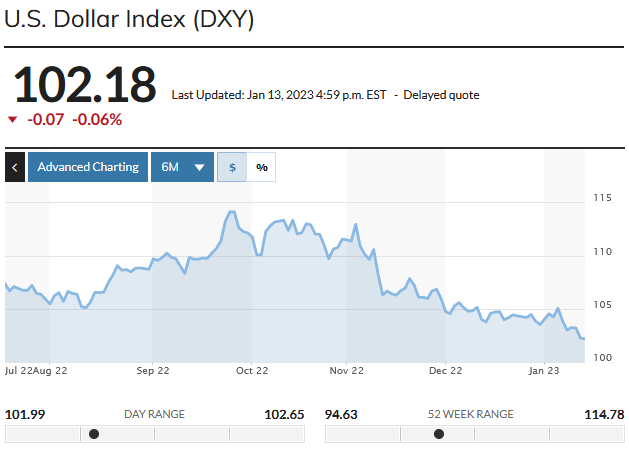

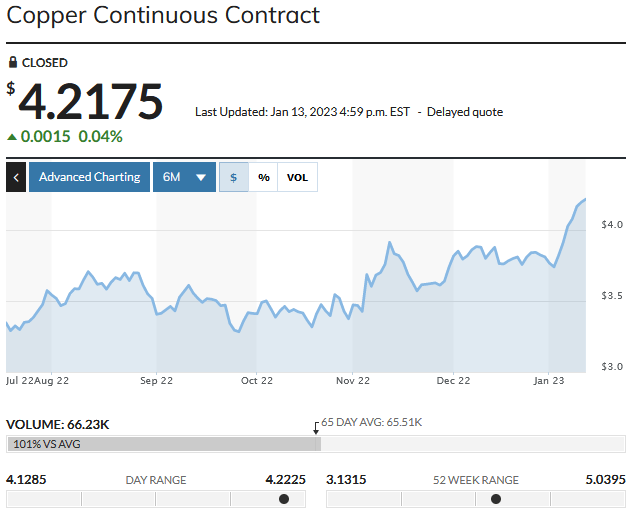

As most of you probably know, the U.S. dollar has been dropping since the high set in late September:

MarketWatch

That is likely due to recent and positive trends in inflation data and the general consensus that the Federal Reserve will likely pare-back its interest rate hikes to 0.25%. Regardless, the fall in the U.S. dollar has caused the price of copper – which is generally priced the world-over in U.S. dollar – to rise in sympathy:

MarketWatch

However, note that the U.S. dollar has only fallen 2.24% YTD while the price of copper has risen 12% over that same time frame. That being the case, something else is obviously at play here. That “something else” is the reopening of China. China consumes ~50% of the world’s copper production. Indeed, the Wall Street Journal reports that Chinese imports of copper concentrate are up 9% YTD and that:

Fitch raised its copper-price expectations for the year to $8,500 from $8,400 on the more positive sentiment, and expects copper consumption to rise 3% this year above 26 million tons. The firm forecasts copper demand and supply to be roughly equal at 26.5 million tons.

Estimates are that the global copper supply will be relatively equal to demand indicates a tight market given relatively low copper inventories. Meantime, on a mid- to long-term basis, the Biden administration’s ability to get a long-overdue and bi-partisan Infrastructure Act passed is a strong tailwind for copper given the Act has $7.5 billion for building out an EV-charger network across the country and $65 billion to build out the electric grid to be more resilient, support renewable power generation, and to build thousands of miles of new transmission lines. In addition, the CHIPs & Science Act has already put the building of several large new semiconductor plants in motion – each of which will require significant electrical infrastructure to be built. Lastly, the Biden Administration’s IRA Act (which I like to call the “Clean Energy Act”) has incentives to build and power homes, businesses, and communities with much more clean energy by 2030, including:

- 950 million solar panels

- 120,000 wind turbines

- 2,300 grid-scale battery plants

In addition, the Clean Energy Act has up to $7,500 in tax credits for new EVs and $4,000 for used EVs. All of these tax-incentives are going into products that will require a lot of copper, especially for the windings on wind turbines and EV electric motors.

Earnings

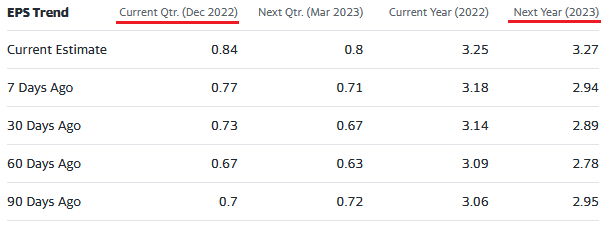

These bullish developments have not gone unnoticed by investors. Indeed, Southern Copper’s earnings estimates have been rising significantly of late:

Yahoo Finance

Indeed, as you can see from the graphic above, Q3 earnings estimates have risen 20 cents per share over the past 90-days, and by 9% over the past week alone. Meantime, FY23 EPS estimates are now $3.27 – up 11% over the past week. (Note: while I don’t have a Q4 release date, last year the Q4 report was released on February 1st).

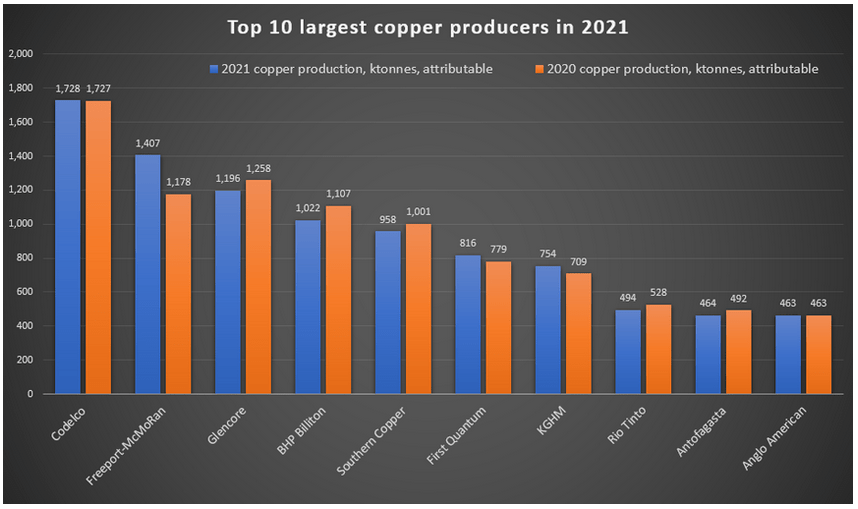

SCCO is one of the largest copper producers in the world. Although 2022 numbers are not yet in the books, SCCO was the 5th largest global producer of copper in 2021:

Kitco.com

Note that – other than Freeport-McMoran (FCX), the #2 copper producer and which significantly grew production yoy in 2021, many of the top-10 copper producers actually saw production decline yoy. (Consider reading my popular Seeking Alpha article: Freeport-McMoRan: Why ConocoPhillips CEO Sold Oil And Bought Copper).

Southern Copper is known for being one of the most efficient producers of copper. In FY21, operating cash-costs (including by-product credits) actually declined by 3% compared to 2020 (from $0.69/lb to $0.67/lb).

The following slide – taken from Southern’s November presentation – gives a broad overview of the company, which has the highest copper reserves of any listed company:

Southern Copper

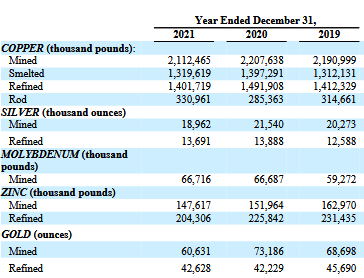

In addition to copper, Southern also produces silver, moly, zinc, and gold:

FY21 10-K

That being the case, it certainly doesn’t hurt SCCO that the price of gold closed Friday at $1920/oz – up 6% over the past month. The price of silver (5% of revenue in FY21) has also been strong of late – another positive catalyst for SCCO.

Risks

One obvious risk is that SCCO stock has risen too-far too-fast and is now susceptible to a pull-back.

Another risk is that FY23 is likely to see substantially higher production costs due to global inflation and still relatively high diesel prices (a key fuel used in production). Indeed, as can be seen in the Company Overview graphic above, cash costs in FY22 are estimated to be $0.90/lb, up from $0.67/lb in 2021.

In addition, copper supplies should increase this year. As pointed out in the previously referenced article in the WSJ, Standard Chartered analyst Sudakshina Unnikrishnan said:

On the supply front crucially, a projected strong rise in global mine supply in 2023 will take the global copper concentrate market into a meaningful surplus and tip the refined copper balance into surplus.

Downside risks also include a potential recession in Europe, weaker construction activity in the U.S., and worries over China’s property sector which equates to ~20% of domestic copper demand.

While SCCO was incorporated in Delaware back in 1952, the company is majority owned – through an indirect subsidiary – by Grupo Mexico. However, I generally view that as a positive considering the number and size of the mines SCCO has in Mexico.

Lastly, as an international player, Southern Copper faces geopolitical risks, specifically in Peru – home of the Toquepala and Cuajone mines. Peru might try to raise taxes and royalties on SCCO’s production.

Summary & Conclusion

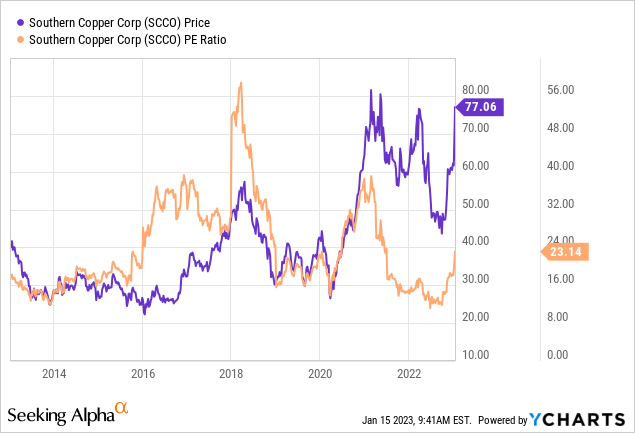

Overall, and for the reasons stated in the article, the fundamental backdrop for copper is still bullish in my opinion. SCCO should see higher production and higher copper prices in 2023. If SCCO hits current FY22 estimates and earns $3.25/share, at Friday’s close of $77.06, that equates to a TTM P/E of 23.7x. That is arguably a rich valuation for a miner. However, mining is a cyclical industry and the PE ratios can swing wildly, and in that context SCCO’s current P/E is actually toward the low-end of its past 10-year history:

While I am bullish on SCCO stock, I would HOLD at the current level as it is likely the stock will pull-back this coming week after its recent bull-run. I would try to accumulate shares at $70 and should market volatility take the stock down further, would establish a full-position at $65.

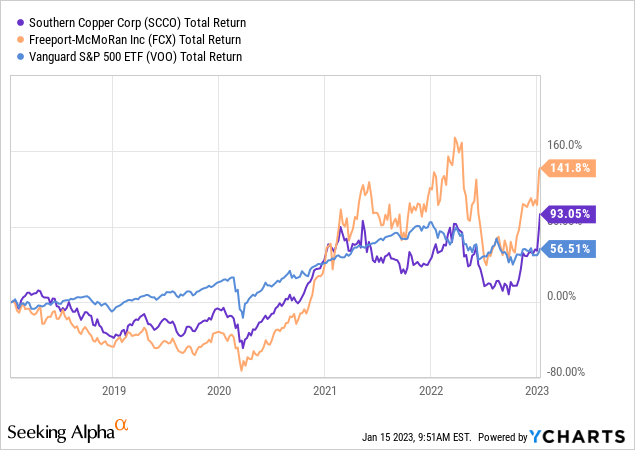

I’ll end with a 5-year total returns chart comparing SCCO with Freeport-McMoran and the broad S&P500 as represented by the Vanguard S&P 500 ETF (VOO):

Be the first to comment