JHVEPhoto

Dear readers/followers,

Novo Nordisk (NVO) really is one of those companies we want to own. Danish – and I don’t own many Danish stocks, because they’re typically priced very expensively overall – and qualitative, with a world-leading position in an absolutely crucial segment.

Since writing about Novo Nordisk last, the company has continued to outperform broader market averages despite what I view as a massive premium and a continued massive premium.

The market is taking into account that the company will succeed here (at least as it believes), and continue to deliver double-digit EPS growth rates. If the company does this, the company may be worth 25-28x P/E, but no matter how you view it, I cannot, and will not get behind a 40x normalized P/E for a (simple) pharma business.

Let’s revisit Novo Nordisk.

Novo Nordisk and its massive valuation & quality

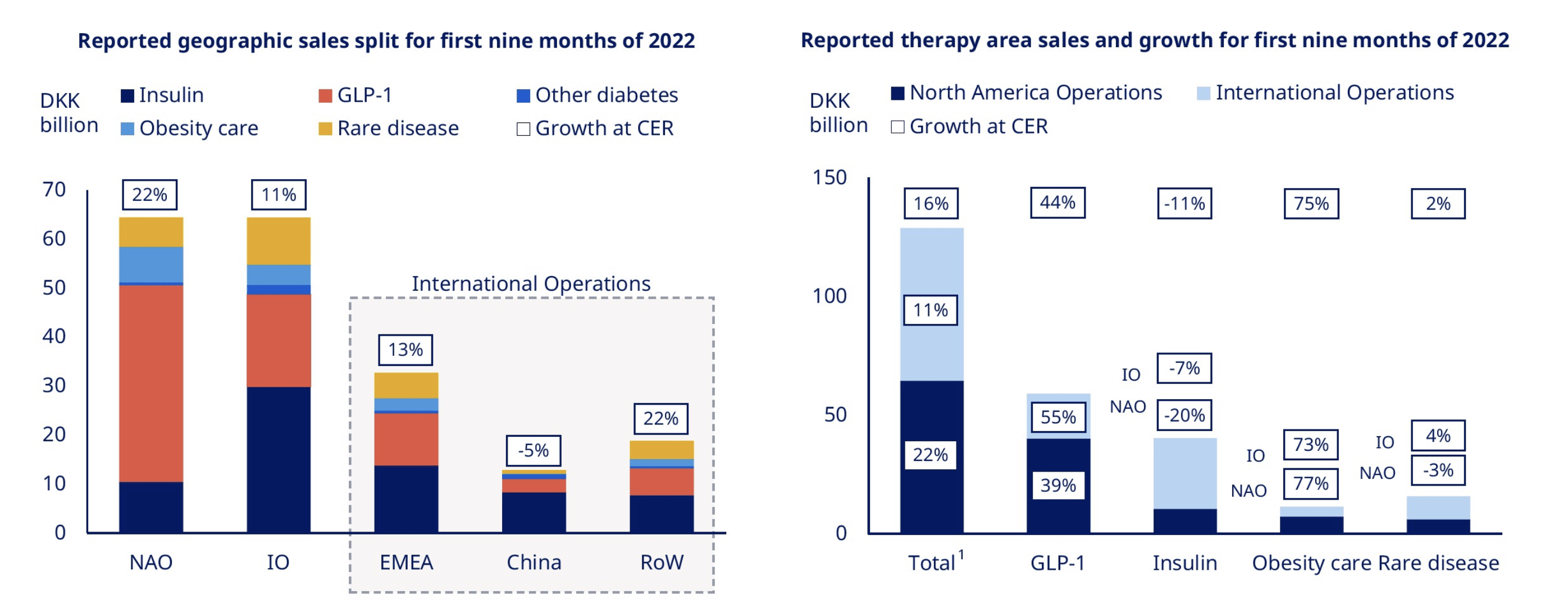

3Q22 is the latest set of results we have for Novo Nordisk. While these company results were in no way bad, they don’t justify 40x P/E. The company is the global leader in diabetes treatment, with a global market share of 31.6%.

NVO IR (NVO IR)

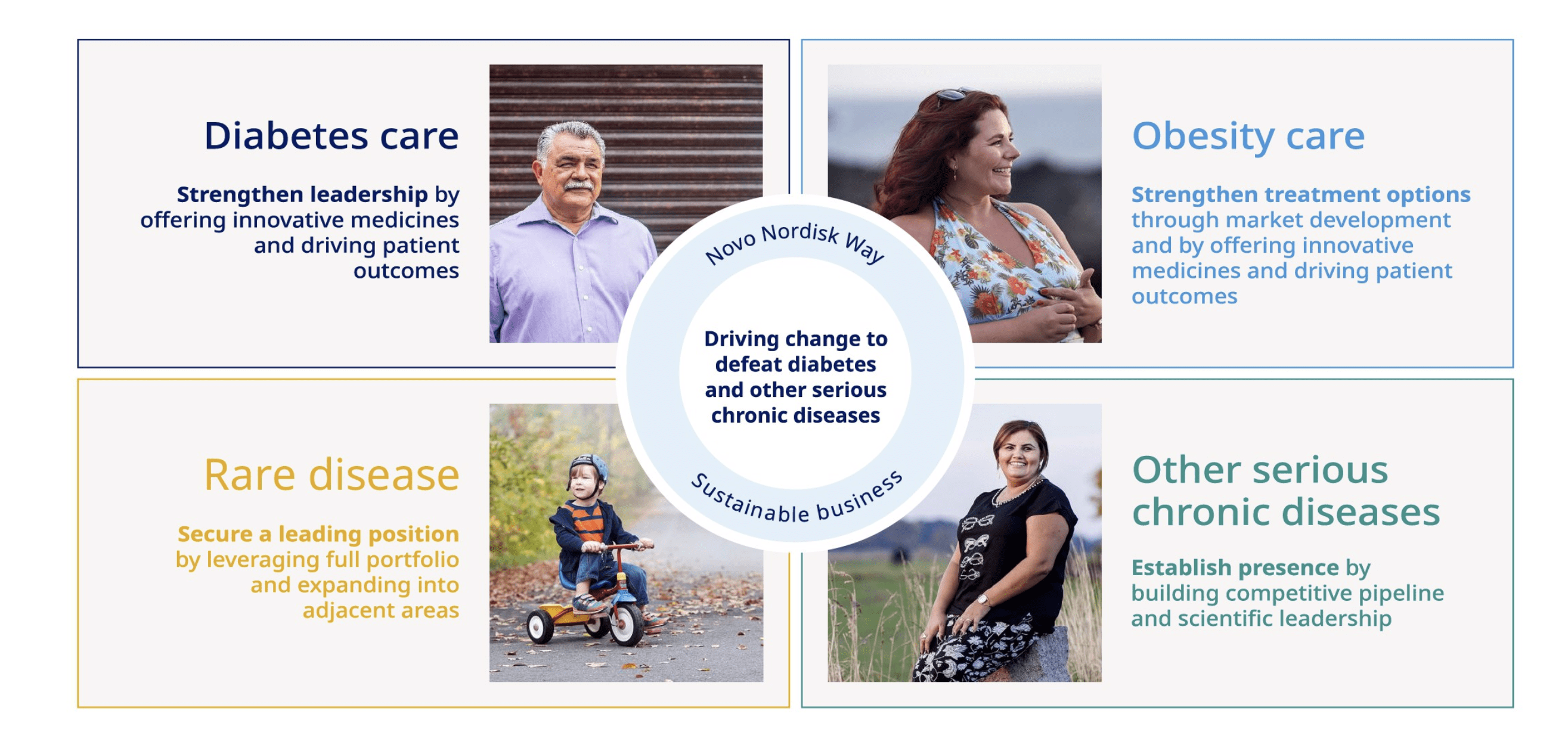

The company is mixing this legacy appeal, where it continues to develop modern and better treatments, with a foray into two relatively interesting areas that have impressive potential growth rates – this being the reason of course that Novo is going into them.

First, there is Obesity, which is seeing sales growth of 75%.

Second, there are Rare diseases, which are seeing very little sales growth – no more than 2%.

Novo Nordisk from a high level is a play on how efficiently the company can continue to maintain its market leadership in diabetes care using its scale and expertise to fend off competition across the globe, while at the same time growing its diversification potential in order to not be quite so dependent on that.

If you think AbbVie’s (ABBV) dependence on Humira is a mark against the company as an investment, and the potential that would result from a sales decline, I want you to consider carefully what would happen if a serious contender or a sales decrease started impacting Novo Nordisk’s legacy diabetes sales.

Remember, that as little ago as 6 years, the company traded below 15x P/E at times, when it was facing more trouble. That is what makes the spike in valuation that we’re seeing here so very pronounced, and to me, so worrying.

As I said, recent results were good. Both sales and operating profit saw growth, and I have little doubt we’ll see a continuation of that within the next month when the company reports FY22.

novo nordisk IR (novo nordisk IR)

This sales growth was driven by good results both from a good geographical split (ex-China), and from an appealing mix in terms of therapy areas. Though, I really want to take the opportunity to point out just how small the company’s Obesity care and rare disease still is, despite how fast it is growing. While the company may be able to rely on this going forward, I would be extremely careful assuming anything in relation to its GLP-1 and Insulin as well as other diabetes areas.

Obesity and Rare Diseases are minuscule. It’s a potential – no more than that in the larger picture.

Novo Nordisk IR (Novo Nordisk IR)

That is why a market leadership increase, even 1.7%, is more important to me than any advances in Obesity or rare diseases at the moment. Until those manage to deliver profit or sales of around 20-25% of the total, Diabetes treatment is what “writes the checks” for this company. And market leadership here looks fine.

NVO IR (NVO IR)

The company continues its milestones in all areas. 4Q22 will see a phase 3 for the Obesity project CagriSema, with several results from Oral and other Obesity projects coming in during 1H23. The year has also been busy for the rare disease segment, with plenty of submissions, phase 3 treatment results, and upcoming submissions.

I don’t expect that the company will have trouble fulfilling its 2022 ambitions and updated goals. The foundations upon which Novo Nordisk builds its currents investment case, and its R&D remains solid.

The use of GLP-1 treatments is already increasing on a global level, yet only 6 million are, as of yet, being treated, meaning only 3% of all diabetes scrips use the technology, leaving a huge potential market to address – and NVO, in most geographies, own the leading GLP-1.

China continues to be a massive opportunity, but one I’m more hesitant about than I was 6 months back. As things stand right now, I’d prefer to discount and impair any expectations that center around China, based on the sheer uncertainty in the nation as an investment geography. That includes these sorts of treatments. China is different for NVO than for other companies – because 140 million people in China live with ongoing diabetes, coming to nearly 25% of the worldwide number of patients – which is why NVO, despite the multitude of challenges hailing from China, cannot afford to ignore the geography. You don’t ignore a quarter of your potential customers.

However, risks remain – and with the valuation at levels that they currently are, it puzzles me how positive the market is considering some of the risks that I see with NVO. One of them is insulin pricing. While NVO has the scale, this pricing is set to come under pressure in the USA, with the resent presidential cycles all being about medication and healthcare costs.

Despite the companies already offering discounted refills, the pressures in this segment are definitely here to stay. Besides pricing, competition has intensified via Eli Lilly’s (LLY) competition through its GLP-1 candidate Trulicity, which has been in the market since 2014 and is taking market share (primarily new patients) from Novo’s Victoza (2010 US approval).

And China, while having plenty of customers, also comes with risks that the US market never did. The fact that we’re now at valuation levels for Novo Nordisk that we have never seen before, not for at least 15+ years. Not during the financial crisis, not during any time I can find – that gives me worry.

It gives me worry for those that own, or invest in NVO at this price – and I know there are those.

So let me break this down further for you.

Novo Nordisk Valuation

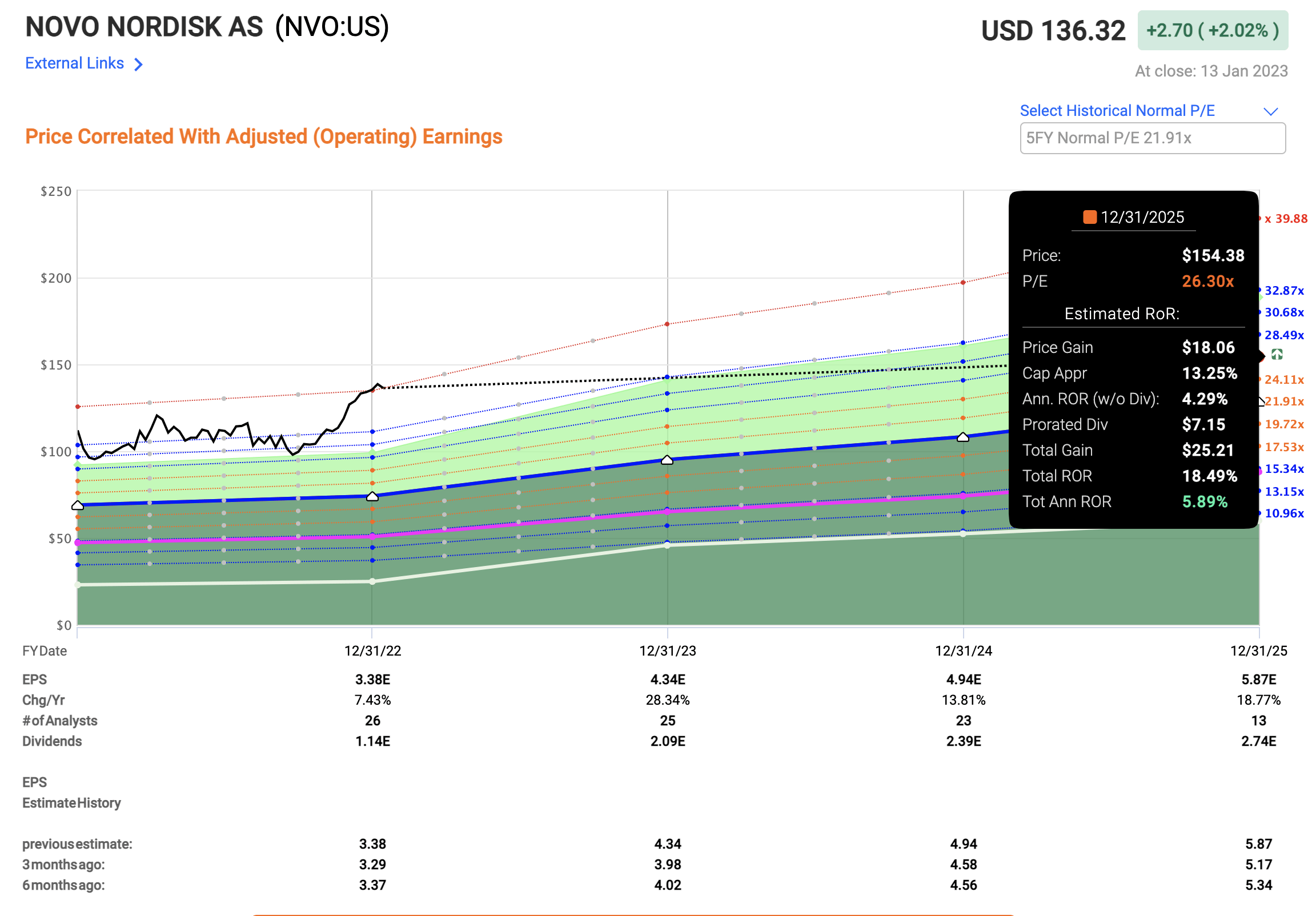

I wrote in my last article that Novo Nordisk remains at record-high valuation ranges. Looking at where the company, AA-rated, is trading, I’m continually unwilling to pay this sort of premium for this company. This was true 3 months back, and it remains even more true at this point.

NVO Forecast (F.A.S.T graphs)

I am not exaggerating when I say that at this point, I would rather put capital in my interest-protected 2.25% savings account than invest in Novo Nordisk. This company at 40x, or 39.88x if we want to be precise on a normalized basis, is reaching proportions of irrationality that we saw during the dot-com bubble, or during recent tech froth.

The company’s yield is now less than 0.85% for the ADR, a 1x of ORD. Despite an amazing low debt, an AA- rating, and growth expected, 19-25x P/E is the highest I would give Novo. At the current 40x, the current forward RoR based on a 25x P/E is less than 3% per year, even with EPS growing at 17% CAGR until 2025E. Even on a 26x P/E, its barely 5.5% per year – and that’s really pushing it.

NVO forecast (F.A.S.T graphs)

History has shown us that whenever the company reaches such highs as we have here, it will eventually drop back down. I don’t see any fundamental change in the thesis that would justify a development such as this one either. The company still does the same thing it did 5, or 10 years ago – only better. This does not mean its suddenly worth twice as much. Nor is there a fundamental change in the capital stack that would imply a change in the added market value for the company, that we could use to justify this trend.

Novo Nordisk is a very good example of a massively overvalued company.

If you own it – my rating is to “SELL” it – or to write some very aggressive Covered Calls.

If you don’t own it – my rating is to stay away – to “HOLD” your ground, and to not approach Novo Nordisk with a 10-foot pole. In its own way, this company is as dangerous as an inflated tech stock – for it has the very real potential to halve or to 3/5th whatever you invest into it in very short order.

A drop back down to 25x marks a loss of capital of 22+%, and that’s even with the increased EPS of ~30% that’s expected for 2023.

Allow me to reiterate and update my previous stance on the current circumstances. Even if this company’s average 15-18% currently assumed growth rates do materialize (and I believe closer to 4-7%), there’s no way I’m paying a 40X P/E premium for a company like this. Not even one that’s AA-rated. I continue to forecast NVO at closer to 5-year averages, which come to around 22X P/E. Based on a 22X P/E forward valuation, the company’s potential RoR is actually negative there – even for future years with more EPS growth.

S&P Global analysts have had their upper-range targets broken here as well. The current average is 928 DKK for the native NOVO-B share in Copenhagen. That’s a 0.9% overvaluation – so even the 10 analysts who consider it a “BUY” have had their average (from 22 analysts in total) seen exceeded, even if at least one of those analysts gives the company a 1,200 DKK price target (and I’d love to see his work and how he reached that one…)

Any target above 720 DKK for the native, and above 30x P/E for the NVO ticker assumes a premium for the company that I’m very uncomfortable with – and would not invest in. That’s why I myself sold the company after waiting around for a long time, at close to 800 DKK some time ago. I will continue to wait for the company to drop to a level that I consider more interesting prior to getting “back in”.

I have long considered how to get “in” to NVO. I’ve looked at options for the native, extremely long-dated out-of-the-money PUT options, only to reach the conclusion that the RoR and risk profiles available for this investment remain as they have been since I started writing about it.

“Not for me”.

Here’s my updated thesis for NVO for 2023.

Thesis

My thesis for Novo Nordisk is as follows:

- Novo Nordisk is a great business that can really be bought into virtually any long-term investor’s portfolio. However, the company’s specifics dictate that you should be careful about NVO and when to buy it.

- I believe Novo Nordisk will come down from its lofty heights, and normalize closer to 20-25x P/E, at which point savvy valuation investors, such as myself and yourself, potentially can pick it up if our portfolio allows for it. I see no reason to go in at this time.

- My target for the company is no more than 720 DKK here – so still an overvaluation in the double digits. I’m not changing my PT here.

Remember, I’m all about:

-

Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Novo Nordisk does not fulfill any of my valuation-specific criteria, and therefore cannot be anything except a “HOLD” here.

Be the first to comment