AlexSecret/iStock via Getty Images

SoFi Technologies, Inc. (NASDAQ:SOFI) stock is a trading stock right now. While we have previously outlined ways to play it long-term, using house money, the stock has now given back all the gains it had seen after it reported Q3 earnings which were much better than expected. This is a high beta stock, it moves a lot, and that makes it great for getting in and out. We remain bullish long term, but in the short run, time for new money to come back in here at $5 and below.

BAD BEAT Investing

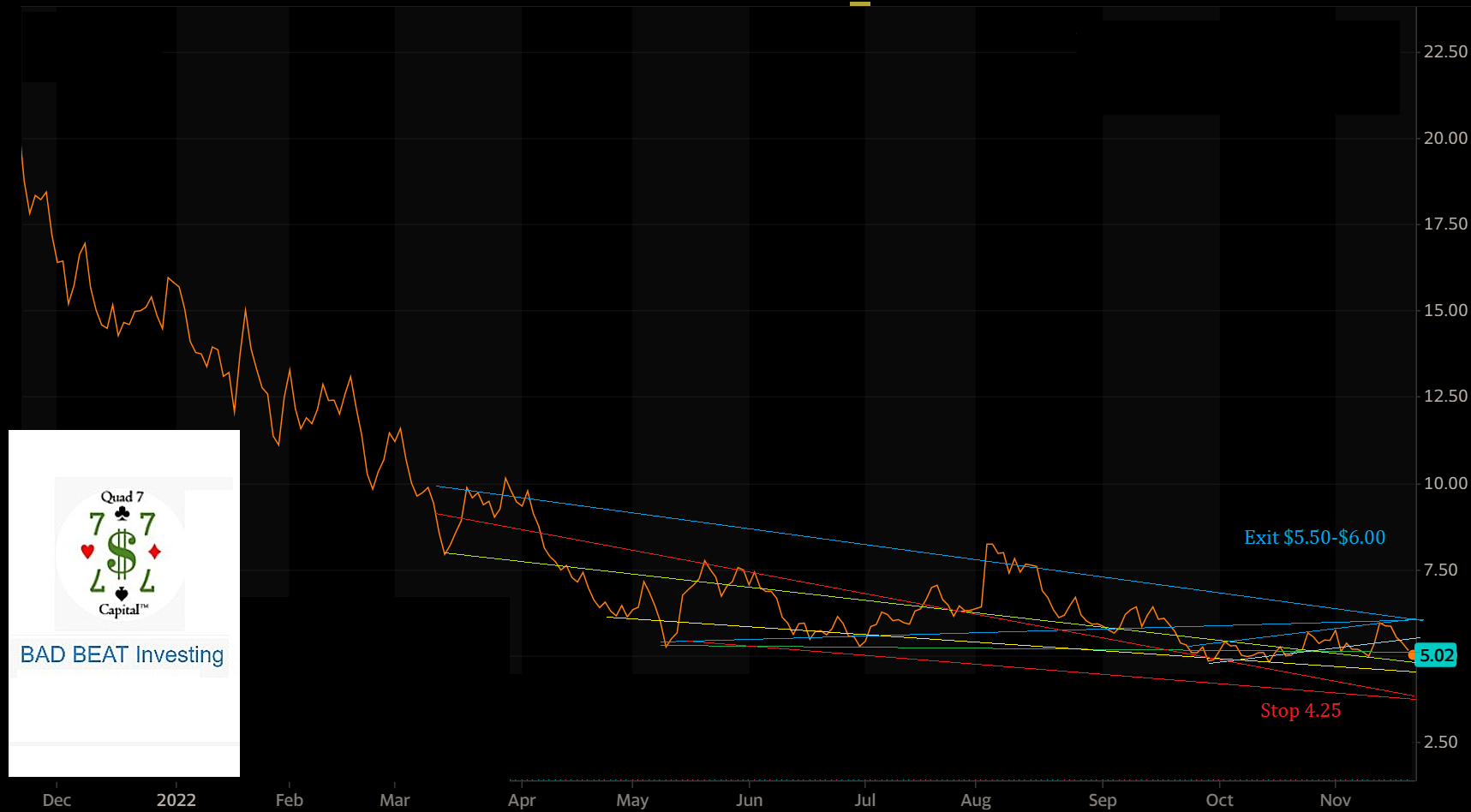

The play

Target entry 1: $4.95-$5.05 (30% of position)

Target entry 2: $4.80-$4.85 (30% of position)

Target entry 3: $4.70-$4.75 (40% of position)

Stop loss: $4.25

Target exit 1: $5.50-$5.60 (50% of position)

Target exit 2: $5.90-$6.00 (50% of position)

Discussion

This lays out the type of trades we make in our service, and generally, we often recommend options approaches as well. In this case, we like selling front month puts to define entry. There are also several straddle approaches to consider, such as selling $4.00 or $4.50 puts, buying $5 calls, and selling $7 calls two months out for income. There are many approaches to consider. That said, the company itself is executing about as best as it can be, accelerating growth, expanding EBITDA, but net income evades it. Short interest remains high, and the stock has now spring loaded to explode again.

Lot of short interest could spark (another) short covering rally

This stock has a high degree of short interest, and today’s rally is certainly fueled by some covering. The short interest is quite high, at the mid-teens as a percent of short interest at last check. When heavily shorted stocks fall like they have in the last week or two, they become springloaded for a bounce on any good news or positive market shift. There also appears to be a loose correlation with the chart of cryptocurrency, and much less so than banks.

Valuation and growth

The stock is very expensive relative to a legacy bank, but as a tech stock, valuation is not as horrible as many similar innovative names. We are talking about the little to no-earnings type names. The ones with high-revenue growth that are investing in themselves. Most of these stocks have been smashed, but SoFi seems to have found a base of comfort around the $5 mark. This comes despite solid growth metrics.

SoFi’s recent results were solid

In the recently reported third quarter, SoFi’s top line growth ramped up. In fact, the company saw record adjusted net revenue of $419 million. Folks this was up 51% year-over-year from the same prior-year period, and way above the high end of management’s guidance. Further, it surpassed consensus estimates by $32.2 million.

Revenue growth is always welcomed but it needs to come with rising earnings power. In this case, we have a conundrum, because the company is profitable before interest and taxes, but loses money net. Look, we like to look at adjusted EBITDA. And this came in at $44 million and this crushed expectations. This was the ninth consecutive quarter of EBITDA growth with a 332% rise year-over-year, and this also set a new record.

Frankly, it was a quarter of several records, and yet the stock has sold back off to about where it was before they reported.

Key segment trends are improving for SoFi

In Q3, there was strength across all three reporting segments. There was strong personal loan originations. In fact, there were a record of $2.8 billion of loans, up 71% from last year, and even rising 14% sequentially. Following what we knew regarding home sales, housing loan demand fell 73%. But margins were pretty good, and we suspect them to continue to remain so.

The lending business saw $181 million of profit, stemming from a 61% margin, up from 55% margins a year ago. Lending products as a whole were up 24% from last year.

SoFi has invested heavily in its platform. The integration of Technisys and Galileo to support multiple products has helped grow revenues. Technology platform enabled accounts jumped by 40% year-over-year to 124.3 million. There was both new clients and cross-selling among existing clients. In fact, Q3 revenue of $84.8 million here in this segment in the quarter was up 69% from last year.

Further, there was also record Galileo revenue, which jumped 29% from last year. We anticipate the growth rate to start to normalize in Q4 year-over-year, as the big gains have been had and there is pressure on consumers. However, we expect the company to focus on growing EBITDA margin.

The financial services segment continues to grow but is also a loss leader right now, losing $52 million as the company builds up reserves, but revenue is exploding higher. In Q3, this segment reported $49.0 million of revenue. This is crazy good growth. That is the technical term on the Street. We digress. The revenues are sick, with 66% sequential growth from Q3, and 288% growth from last year. Within this segment both SoFi Invest and SoFi Money products have been great. Total financial services products grew by approximately 2.7 million, or 83%, year-over-year up to 5.9 million. SoFi Money added another 166,000 products while SoFi Invest products increased by over 106,000. Simply put, the market of consumers is responding as SoFi’s market share expands. Yet the stock is still in the toilet.

Going forward, the situation is still strong

So, if you were not paying attention weeks ago when the company reported, management raised guidance. We love beats and raises. Goes well with the BAD BEAT approach to investing, finding companies doing everything right (or almost everything) while the stock suffers. Eventually, the stock will find a bid longer-term, but for now, it’s great for trading. For the year the company now expects revenue of $1.517-$1.522 billion for 2022. This would be up from $1.508-1.513 billion previously. The company also boosted its EBITDA outlook. For 2022, adjusted EBITDA will be between $115 and 120 million, up about $10 million from the prior view at the midpoint. Strong.

Readers, this was the third time in a row the company raised guidance after results. This is what happens though when companies are not seeing positive net income. Despite being in strong growth mode, the Street does not care that so many other metrics are strong. Shares are great for trading, but the shares have not done anything for investors yet but cause pain. So why not trade with us. Buy, sell, rinse, and repeat.

Risks remain, such as the extreme competitions in the space. Shares are loosely correlated with crypto stocks too, but it really simply offers such trading. For the longer-term, we still would like stock-based compensation to come down as, quarter after quarter, shareholders are being diluted. There has been over $235 million in new shares issued in 2022, which is 50% higher than last year. The market is not pleased, as evidenced by all the gains from the earnings report having been given back.

Trade the stock

Look, our members will tell you, we tell it like it is. We are clear and honest. We do not dance around the issues. SoFi had a great quarter, and a solid outlook. While trading is some work, you can crush those who have invested and are hoping for gains years down the road. With the constant back and forth, we think this stock as perfect for trading around a core position. This remains a key tenet to our investing philosophy that we teach.

Be the first to comment