Justin Sullivan

Thesis

Snap Inc. (NYSE:SNAP) has recovered remarkably from its post-Q2 earnings malaise in July even as the ad industry headwinds intensified. Moreover, we observed that the market’s positioning on SNAP has become so pessimistic in August that we posit that its valuation has likely been adequately de-risked to reflect its near-term challenges.

It’s arguable whether Snap has sustainable long-term competitive moats as it faces off with TikTok (BDNCE) or even its dominant digital ad peers in Meta (META) or Google (GOOGL) (GOOG).

However, Snap’s engagement metrics remain healthy in Q2. Furthermore, its new Snapcnat+ service reached 1M paying subscribers within six weeks of its launch. Therefore, we posit that Snap’s thesis remains relevant at the correct valuation, even though it needs to demonstrate more robust profitability metrics moving forward.

Notwithstanding, we are confident that the damage to SNAP’s price action has dissipated much of its growth premium, as the stock seems to hold its July lows robustly. However, we need to remind investors that Snap’s headwinds will likely continue through Q3, which could add potential downside volatility. Still, we are confident that its July lows should hold, in line with our assessment of the market’s medium-term bottom.

Therefore, we revise our rating on SNAP from Buy to Speculative Buy, with a medium-term price target (PT) of $14.5 (implying a potential upside of 30%).

Snap’s Growth Should Normalize Moving Forward

Snap’s valuation was configured for a high-growth thesis. Therefore, Snap’s execution and the gamut of macro headwinds outside of its control have damaged its growth profile.

Furthermore, intense competition from TikTok has exacerbated its challenges, as it had to monetize on a lower ad-load Spotlight. Therefore, we believe the battering by the market is justified, as Snap’s competitive moats remain questionable.

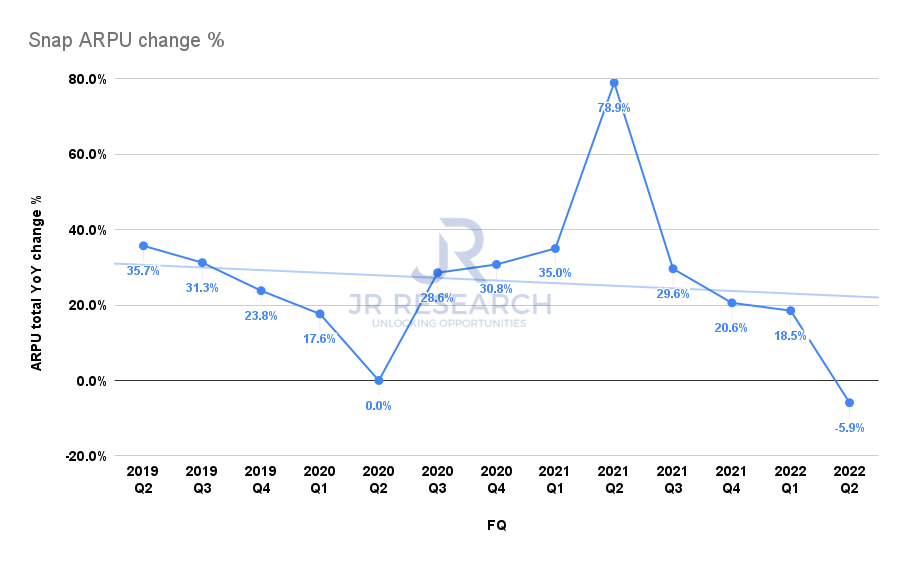

Snap ARPU change % (Company filings)

Snap’s average revenue per user (ARPU) growth fell dramatically to -5.9% in Q2, reflecting the severity of the downturn in the ad industry, worsened by its execution, monetization, and competitive challenges.

Therefore, we can understand why investors have become so pessimistic, as Snap registered its first negative ARPU growth in three years. However, we need to emphasize that the ad industry is cyclical. Therefore, we don’t think it’s reasonable to expect that Snap’s growth trajectory would not find a bottom, even though it has been battered. Instead, we posit that Snap’s below-trend growth could start normalizing through FY23 as macro headwinds subside and advertisers resume spending.

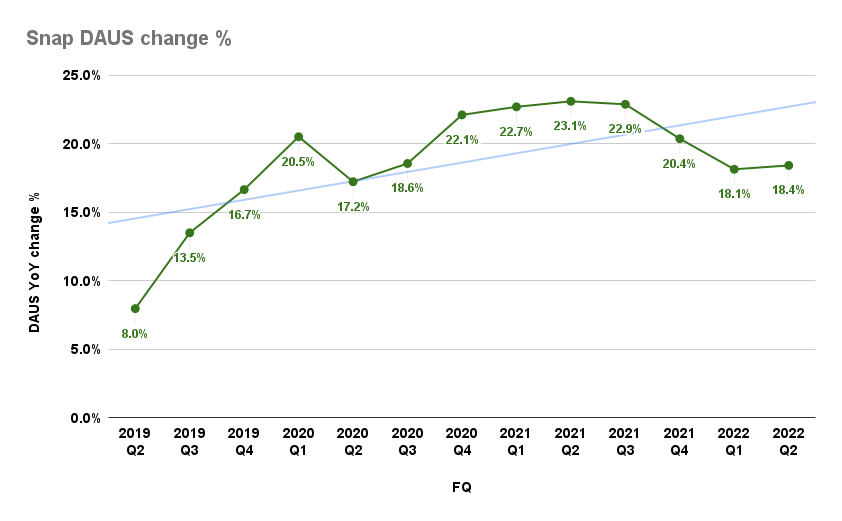

Snap DAUs change % (Company filings)

Furthermore, the company’s engagement metrics remain relatively healthy. Despite navigating its monetization challenges, Snap posted a daily active users (DAUs) growth of 18.4% in Q2. Hence, we are confident that Snap remains a relevant platform for active users, which augurs well when its growth trajectory normalizes.

Furthermore, management’s commentary suggests that Snap’s revenue profile should recover robustly as ad spending headwinds improve over time. Management articulated:

We’re hearing supply chain pressure and inflationary costs. They’re [also] getting pressure from the cost of capital, [as] capital being more expensive as well as drying up in different areas. But what we’re hearing from advertisers, is that they are taking this time to reevaluate their priorities to ensure that they’re making the right investments in the right places. And when we talk about digital advertising, it is the easiest thing to turn off. But it is also one of the most performant tools in their tool chest. So as things start to rebound for some of these advertisers in the areas where the macro pressures are a little bit more transitory, it’s also the first thing to get turned back on. So we remain optimistic that as things hopefully start to improve in the macro we can capture that opportunity. (Snap FQ2’22 earnings call)

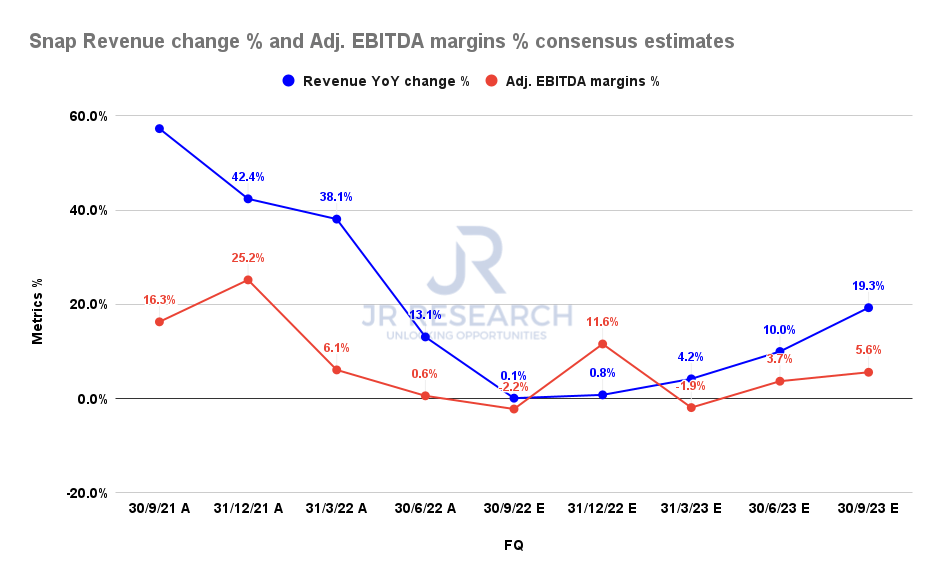

Snap revenue change % and adjusted EBITDA margins % consensus estimates (S&P Cap IQ)

Moreover, the consensus estimates (bullish) suggest that Snap’s revenue growth and adjusted EBITDA margins profile should recover robustly through FY23. Therefore, we are confident that Snap’s operating performance should emerge from its nadir as it laps a challenging FY22 moving ahead.

Consequently, it should spur a medium-term re-rating in Snap’s valuation, given the significant battering that it has endured.

SNAP’s Valuation Has Been De-risked

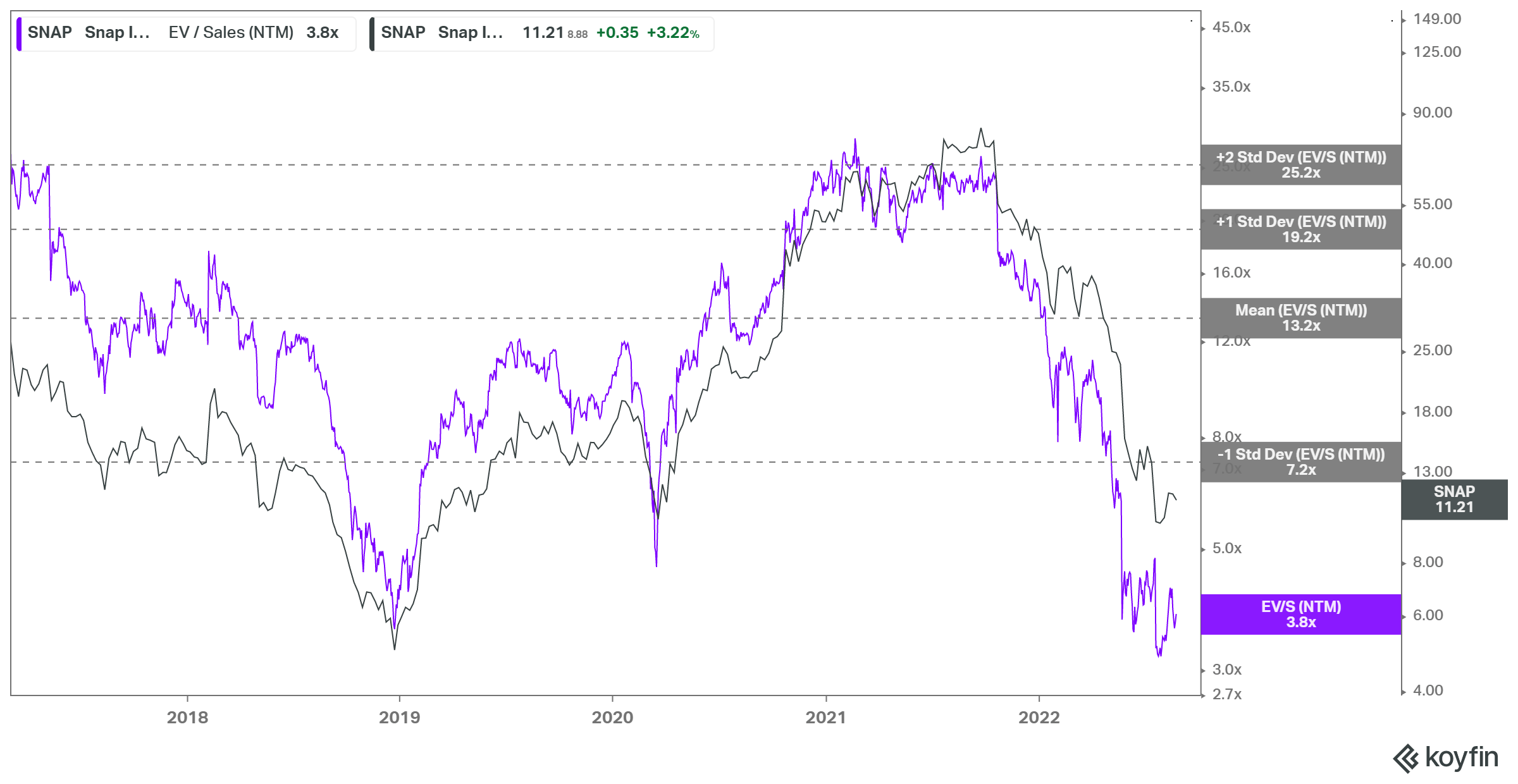

SNAP EV/NTM Revenue valuation trend (koyfin)

As seen above, SNAP’s NTM revenue multiples likely reflected its near-term challenges, as it last traded at more than one standard deviation below its all-time mean.

Therefore, we posit that it’s arguable that the market has de-risked SNAP’s growth premium sufficiently for investors to bet on a re-rating as its underlying performance improves.

Is SNAP Stock A Buy, Sell, Or Hold?

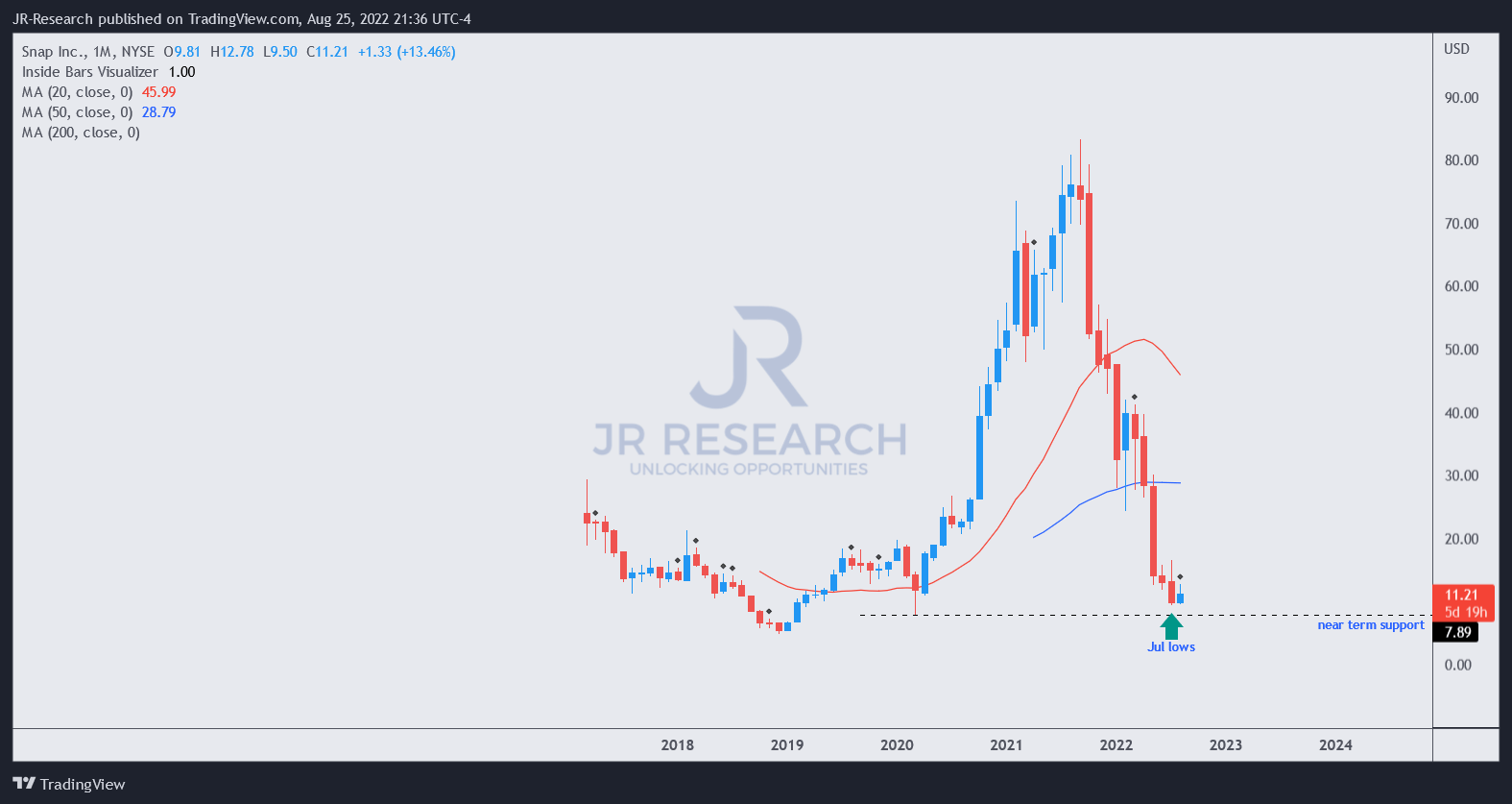

SNAP price chart (monthly) (TradingView)

We postulate that SNAP has likely staged its long-term bottom in July as it attempts to recover through August. The rapid collapse from its September 2021 highs has likely wiped out many bullish shareholders/investors as it closes in on its July lows.

Therefore, we are confident that the high level of pessimism seen in SNAP portends well for the medium-term recovery in its buying momentum.

We revise our rating from Buy to Speculative Buy, with a medium-term PT of $14.5.

Be the first to comment