NicoElNino

Smartsheet (NYSE:SMAR) is a leading software platform that is focused on the work management industry. The company’s products are utilized by 90% of the Fortune 500 and its notable customers include; Uber, GM, Cisco, Peloton, American Airlines, Proctor & Gamble, and many more. The Task management software market is forecast to grow at a 13.3% compounded annual growth rate [CAGR] and be worth over $4.5 billion by 2026. Therefore, Smartsheet has long runway for potential growth ahead. The company recently beat its Q3, FY23 estimates for both top and bottom-line growth. In addition, Smartsheet has a super high dollar-based net retention rate of 129%, which means customers are staying with the platform and spending more. In this post I’m going to break down its business model, financials, and valuation, let’s dive in.

SaaS Business Model

Smartsheet is a work management platform that was founded back in 2005. This is three years earlier than competitor Asana (ASAN) which was founded in 2008. In addition, it was founded a substantial seven years earlier than monday.com (MNDY), which was founded in 2012. Therefore Smartsheet is a true pioneer in the industry, despite the other companies being more well-known by many. Independent reviews on Gartner also indicate Smartsheet is a leader by both a star rating (4.5 stars out of 5) and a number of reviews. Competitor monday.com has the same star rating but a lower number of reviews overall, which is why it is second on the Gartner review list.

The value proposition of Smartsheet is it basically improves workplace productivity and team alignment. Its software platform acts as a “single source of truth”, where specific tasks can be assigned to team members.

Team Collab feature (Smartsheet )

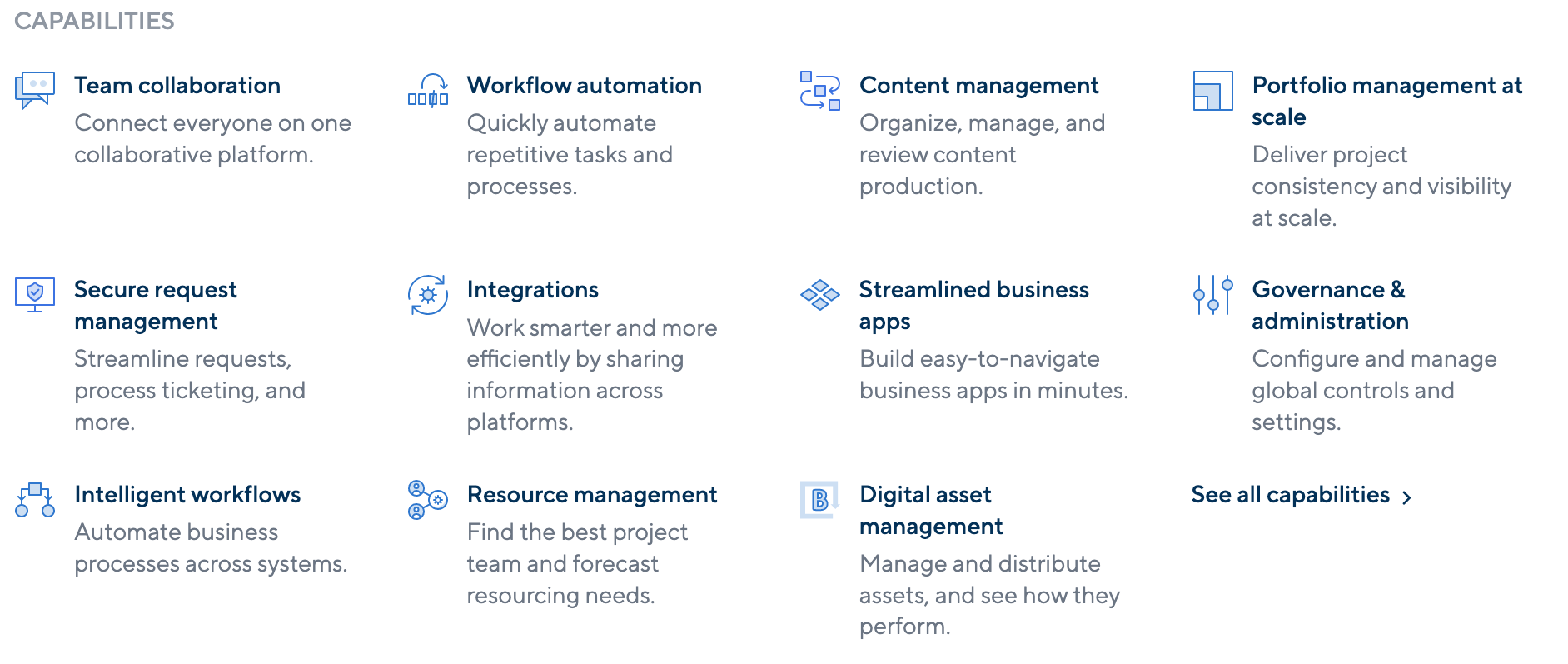

Apart from team management, the main capabilities of Smartsheet include; content management, request management, workflow automation, and much more. Its automation tools are particularly useful, as they can be used to automate repetitive tasks with integrations. An example would be to alert a Slack channel when specific criteria are met.

Capabilities (Smartsheet)

Smartsheet sells its platform through a low-friction, self-service model. It costs just $7 per user at the cheapest package or $25 per user at the more expensive package. This is similar pricing to platforms such as monday.com and fairly reasonable for most teams. The idea is the cheap price per user will encourage early adoption by small teams in an organization, which will then allow further expansion through osmosis. This is a brilliant strategy as a small team adopting the platform, will likely not need to seek large-scale approval from a senior buying committee, which means fairly short sales cycles.

Growing Financials

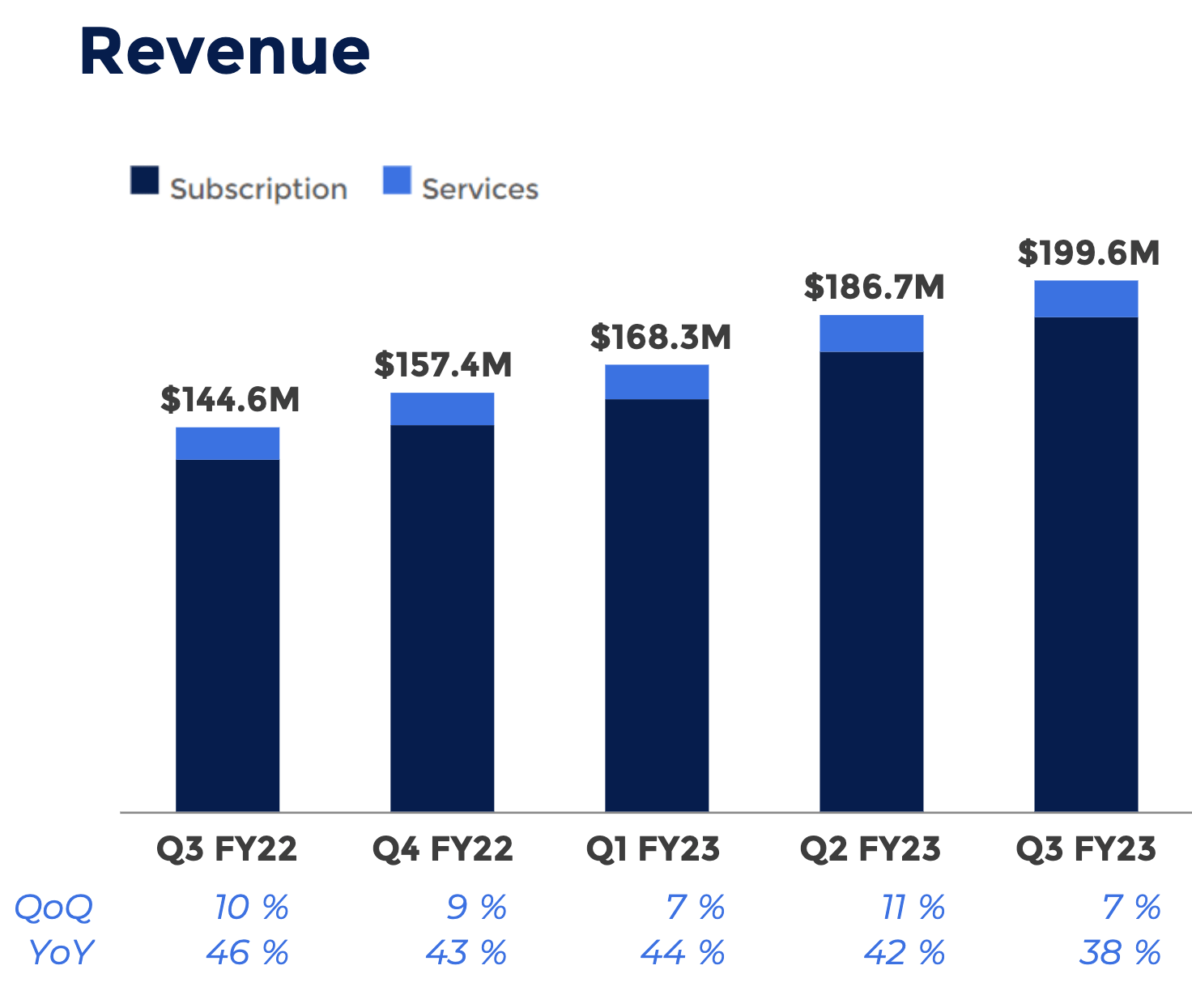

Smartsheet reported strong financial results for the third quarter of fiscal year 2023. Revenue was $199.58 million which beat analyst estimates by $4.88 million and increased by a rapid 38% year over year. Subscription revenue drove the majority of its revenue and increased by 40% year over year to $186.1 million, which was great to see. Subscription models are my favorite type of business model, as they often result in greater customer retention and offer account expansion opportunities. Services revenue also improved by 12% year over year to $13.5 million.

Revenue (Q3,FY23)

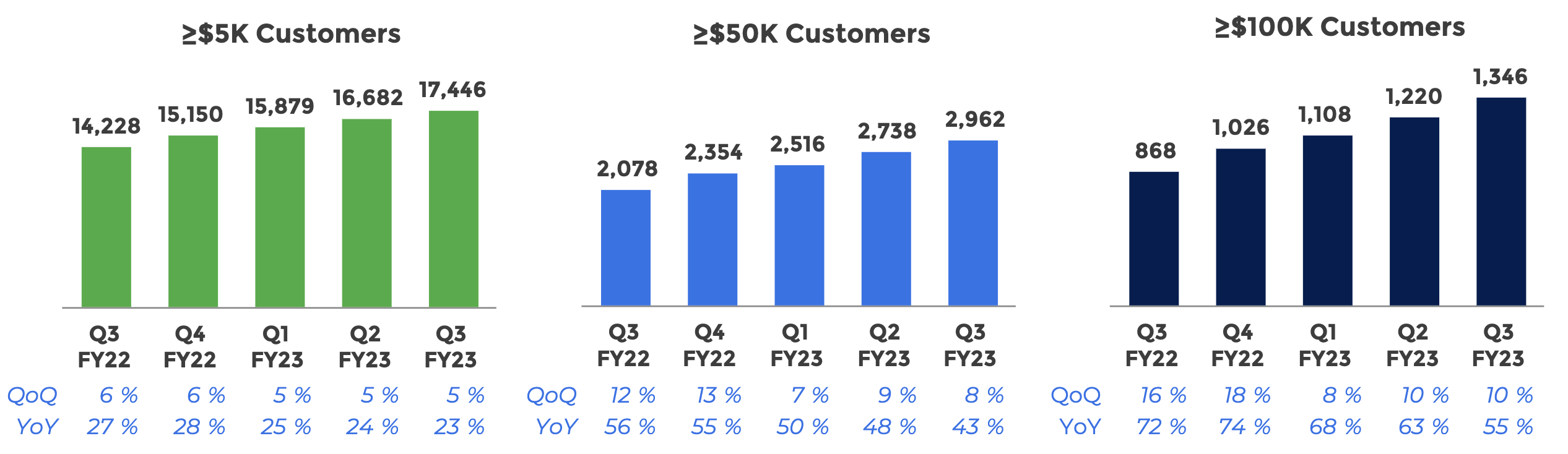

The top-line growth was driven by strong growth in its customer base. The company reported 17,446 customers with an annual contract value [ACV] greater than $5,000 in Q3, FY23. This metric increased by a solid 23% year over year. Notable customer wins included Monster Energy, Arizona Beverages, and even Seattle Children’s Hospital. Smartsheet is already utilized by the largest government healthcare service in the world, the NHS in the U.K. Therefore its movement into the hospital market looks to be a huge but also niche opportunity I haven’t seen its competitors talking about in past reports.

The company has also continued to expand “upmarket” and increased its customers with over $50,000 in ACV by a rapid 43% year over year. Its customers with over $100,000 in ACV increased at an even faster rate of 55% year over year to 1,346. Growing “upmarket” and targeting more enterprises is a solid strategy as larger organizations tend to have higher retention and more upsell opportunities. For example, Smartsheet reported 40 customers with Annual Recurring Revenue [ARR] of over $1 million. These gigantic and engaged customers act as proof of concept for other customers. Smartsheet’s “enterprise-grade security and compliance” offers peace of mind to large organizations, which acts as a barrier of entry to smaller upstarts.

Customer Contract Value (Smartsheet)

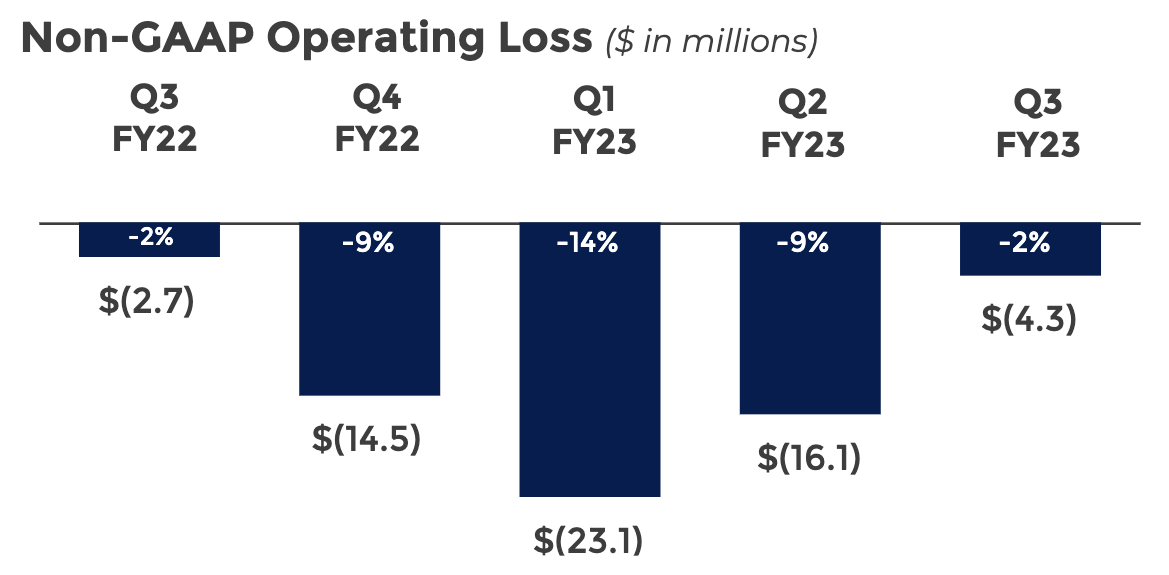

Onto to profitability metrics for Q3,FY23, Smartsheet reported a non GAAP gross margin of 81%. This was down 1% year over year but I noticed its margin generally fluctuates by this amount between quarters, thus it is not an issue. The company did report a non-GAAP operating loss of negative $4.3 million, this was worse than the prior year when negative $2.7 million was reported. A positive is this metric was greater than management guidance and had a 7% quarter-over-quarter improvement. This improvement was mainly driven by hiring plan adjustments and stricter financials. Earnings per share [EPS] was negative $0.31, which beat analyst estimates by $0.21.

Non GAAP Operating Loss (Q3,FY23)

Smartsheet has a solid balance sheet with $434.7 million in cash and short term investments. In addition, the company has just $70.5 million in total debt.

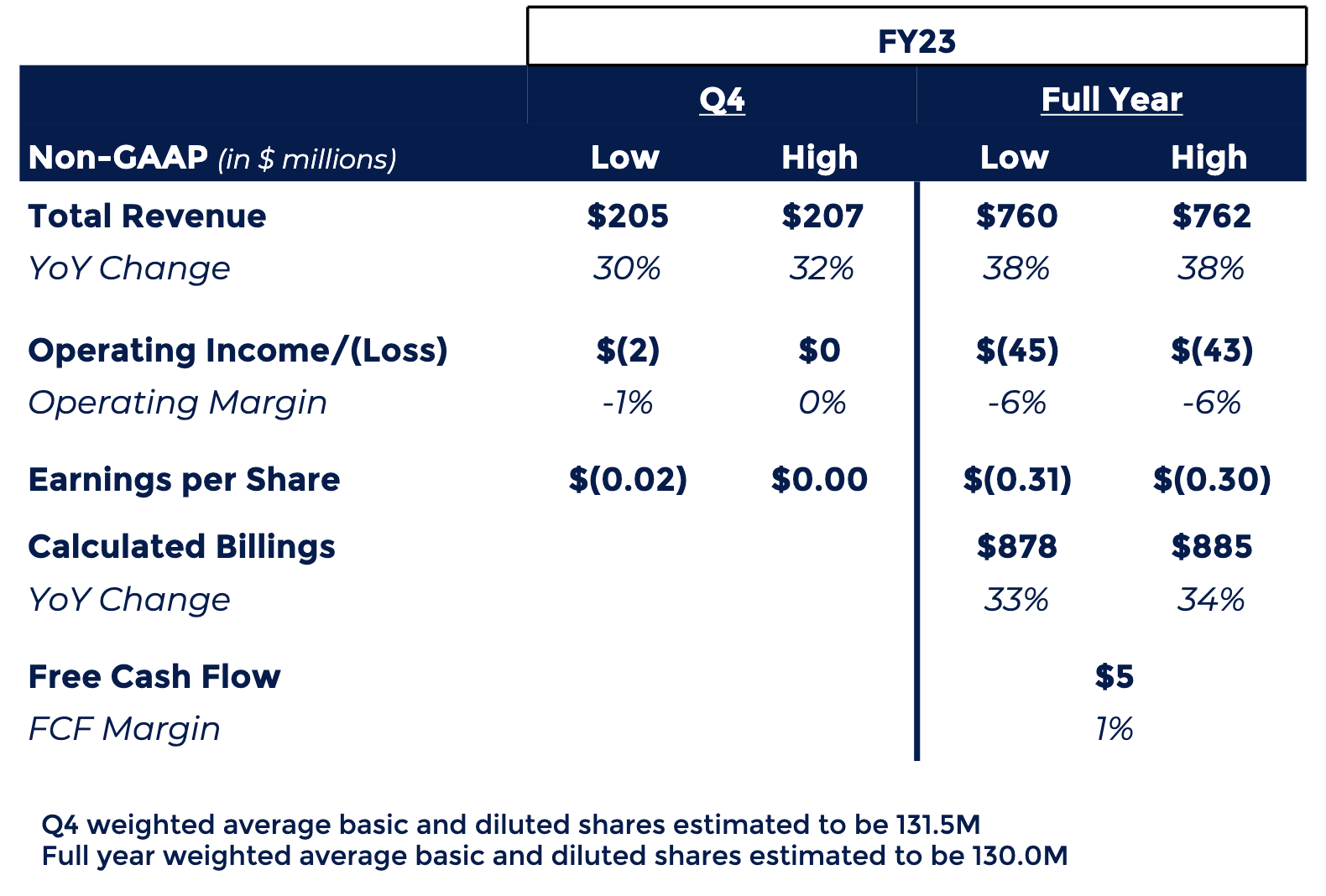

Moving forward, management has forecast 38% revenue growth for the full fiscal year of 2023. Its operating margin is forecast to improve in Q4 to break even at the high end of the range. This is a positive sign and demonstrates the business’s cost-cutting is working.

Guidance (Q3,FY23 report)

Advanced Valuation

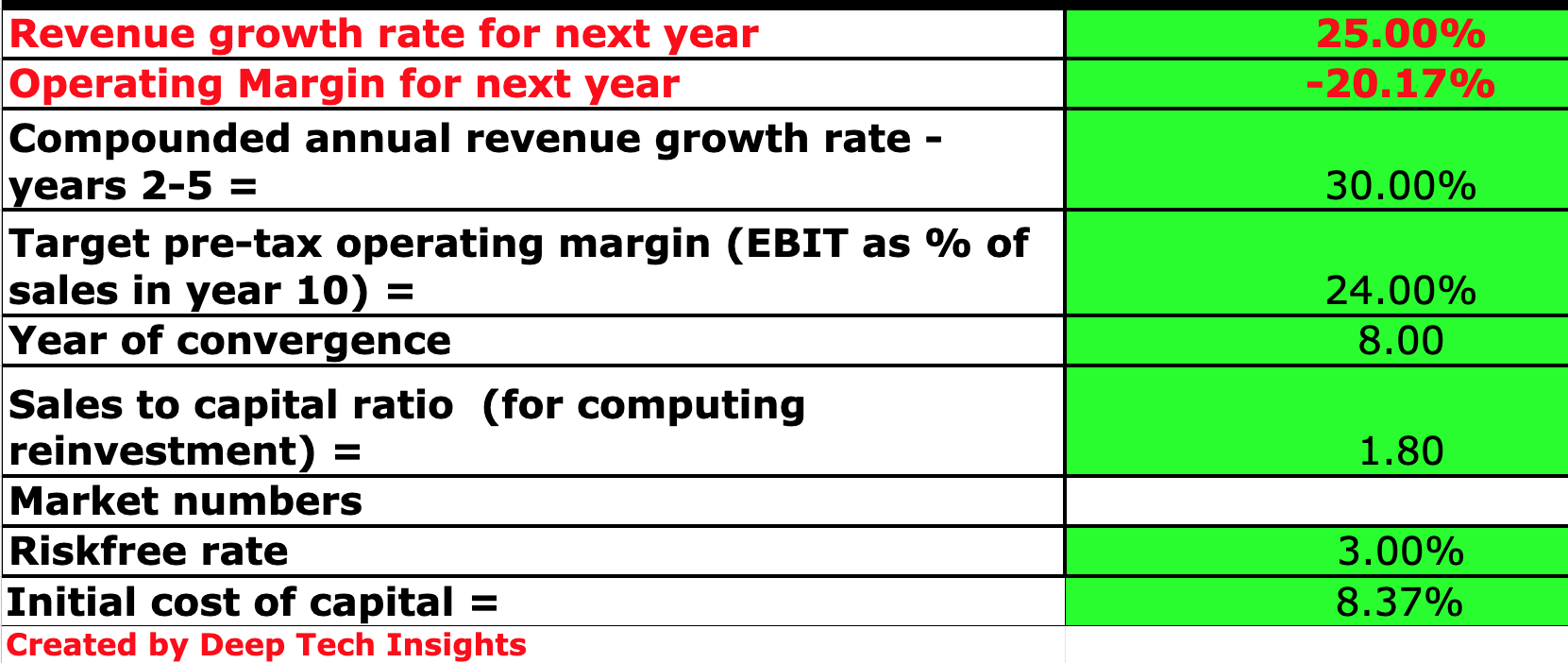

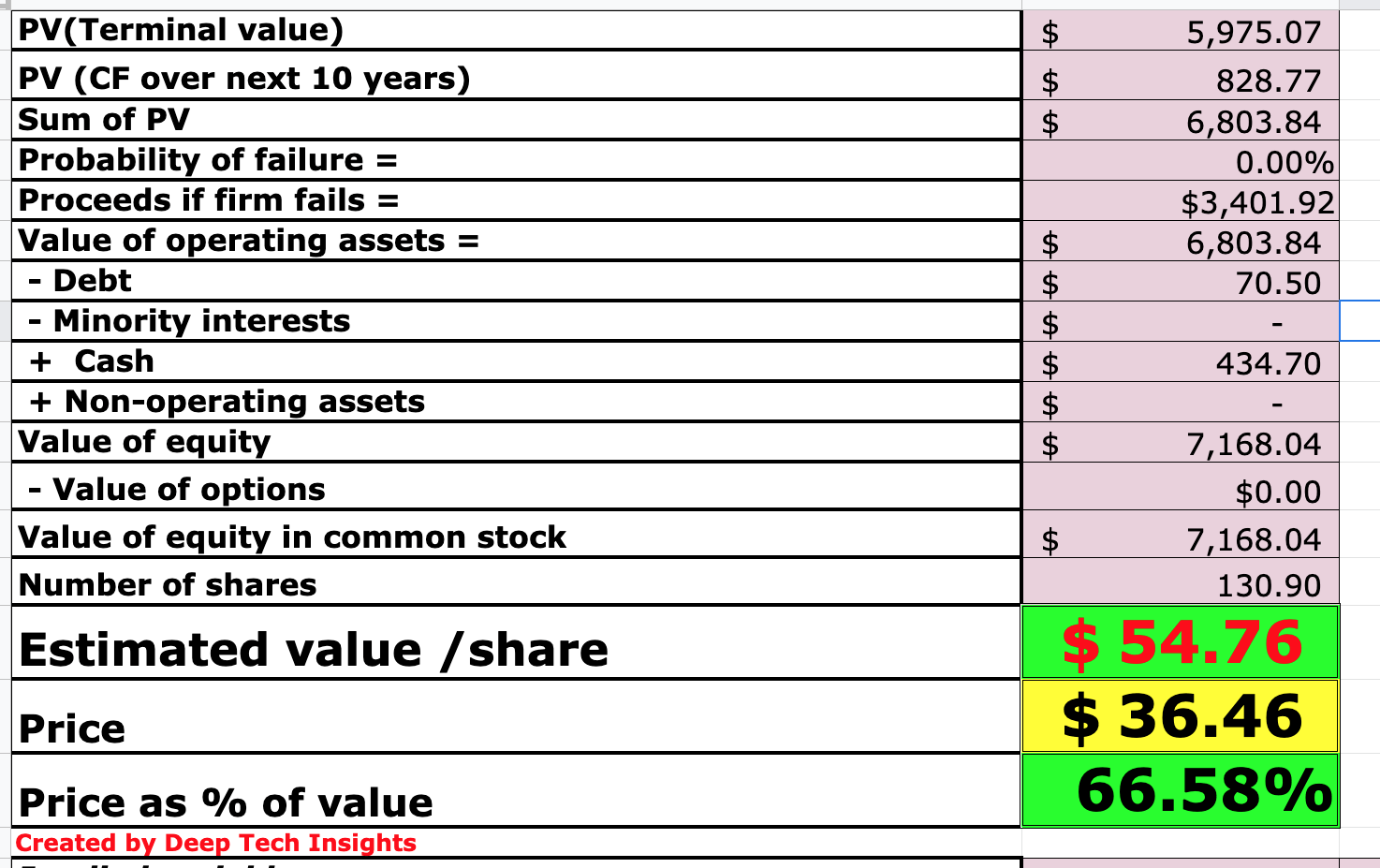

In order to value Smartsheet, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow method of valuation. I have forecast 25% revenue growth for next year, which is much lower than the 38% forecast for the full year FY23. I am being very conservative due to the macroeconomic environment and forecasted recession (discussed in the “Risks” section). In years 2 to 5, I have forecast a faster growth rate of 30% per year, as I expect economic conditions to improve.

Smartsheet stock valuation 1 (Created by Deep Tech Insights)

To increase the accuracy of the valuation, I have capitalized R&D expenses which has lifted net income. In addition, I have forecast a pre-tax operating margin of 24% over the next 8 years, which is 1% higher than the software industry average. I expect this to be driven by increasing operating leverage, cost discipline, and upsell opportunities with enterprises.

Smartsheet stock valuation 2 (created by Deep Tech Insights)

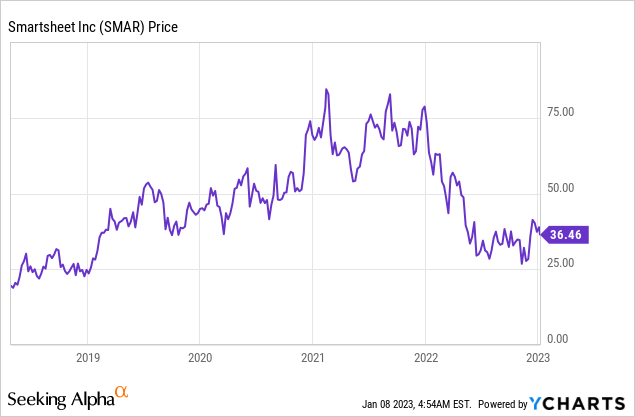

Given these factors, I get a fair value of $54.76 per share, the stock is trading at $36.46 per share at the time of writing and thus is ~33.42% undervalued.

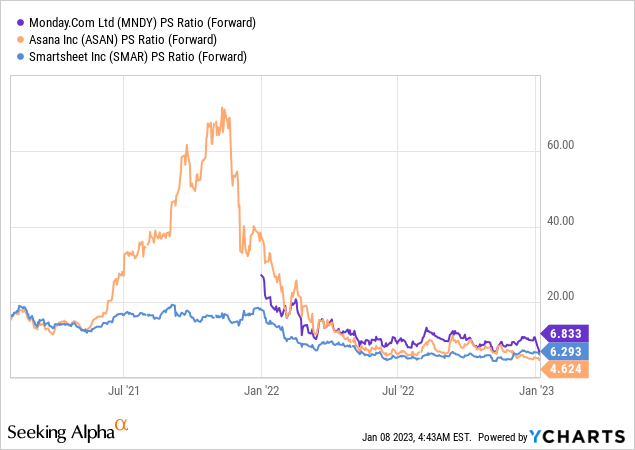

As an extra data point, Smartsheet trades at a price-to-sales ratio = 6.6, which is 58% cheaper than its 5-year average. Relative to other team management SaaS companies, Smartsheet is trading at a mid-range valuation. Asana is trading cheaper with a PS ratio = 4.6, but that company is burning much more cash and has worse margins. However, Asana does have a billionaire CEO and founder (who is also the co-founder of Facebook). Its CEO has been buying millions of dollars’ worth of Asana stock, and has the financial firepower to keep the business afloat. You can read my full report on that company here.

Risks

Recession/Competition

As mentioned prior many analysts have forecast a recession and thus I expect longer sales cycles and slowing growth for at least the rest of 2023. Smartsheet also faces intense competition from rivals such as monday.com, Asana, and even Atlassian. I have discussed the reviews and dynamics with these competitors previously.

Final Thoughts

Smartsheet is a leader in the team management software industry and has an established list of enterprise customers. The company has been growing its revenue at a rapid rate, and its margins are also forecast to improve which is a positive sign. Its stock is undervalued intrinsically and relative to historic multiples, thus it could be a great long-term investment.

Be the first to comment