Mario Tama

Altria Group, Inc. (NYSE:MO) stock pulled back significantly last week but was well-supported, with MO finishing the week robustly.

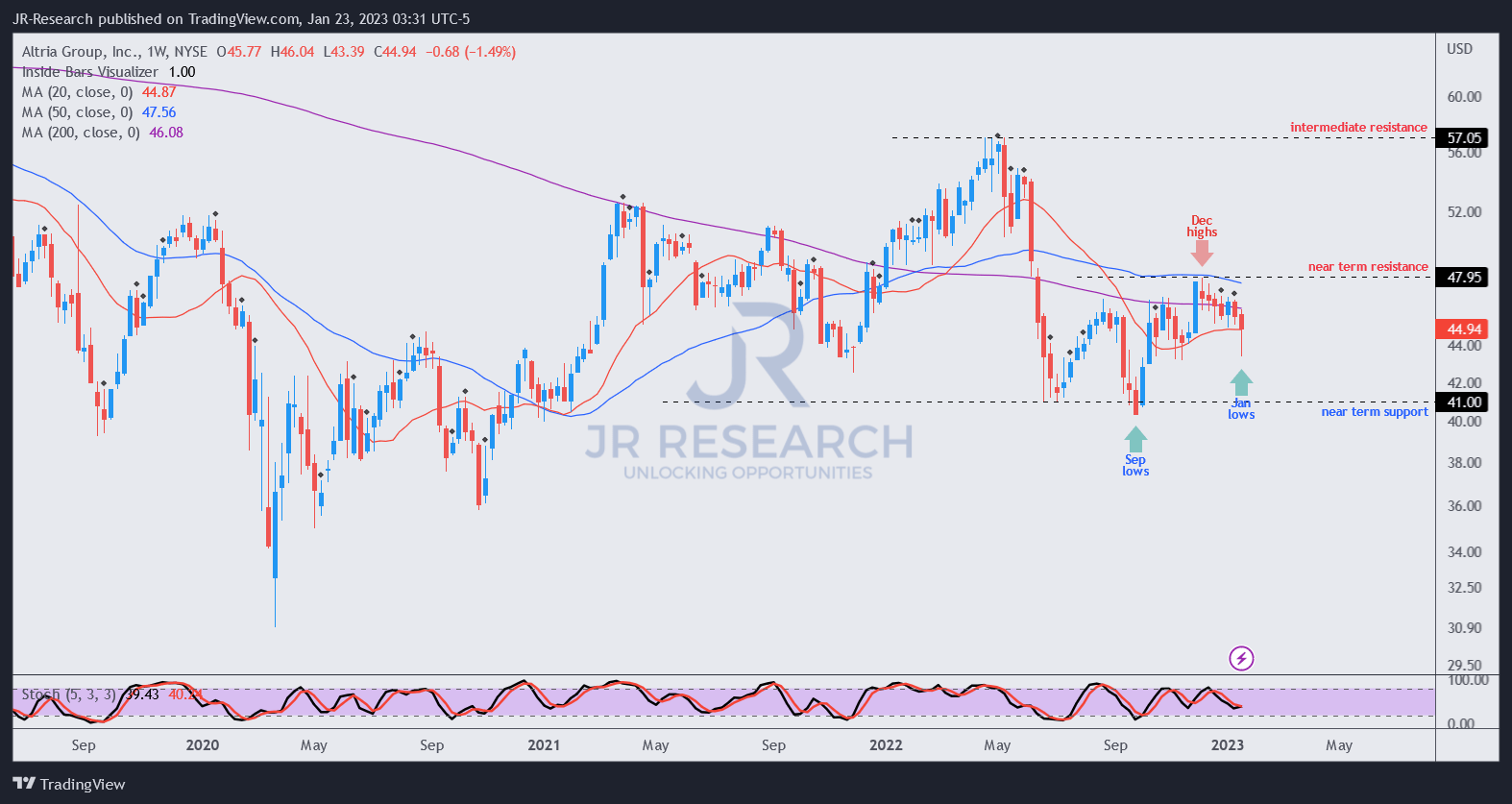

However, MO has struggled to regain its upward momentum since topping out in early December.

With an NTM dividend yield of 8.4%, well above its 10Y average of 5.8%, bulls could argue that significant pessimism is reflected.

However, the critical question about a structural slowdown in its tobacco products could be holding long-term investors back from capitalizing on its seemingly attractive yield.

Moreover, Cowen analysts highlighted in an early January report that Philip Morris (PM) is the market leader in the global smokeless tobacco market, garnering a market share of 59%. With PM expected to release its IQOS products in the US in 2024, investors need to know that Atria’s joint venture with Japan Tobacco (OTCPK:JAPAF) can prove to be a credible competitor against PM. Hence, it’s possible that market operators need to reflect an appropriate level of execution risks, suggesting that a higher-than-average dividend yield should be expected.

Moreover, the macroeconomic outlook has worsened since our previous update in November. Even though inflation rates have continued to decline, consumer spending has also been crimped, beset by still high inflation rates and a more challenging employment outlook.

Moreover, Fed officials are likely still concerned with the job market’s resilience and its impact on sustaining higher inflation rates. As such, MO investors are likely faced with a slew of headwinds relating to the economy, smokeless tobacco rivalry, and weaker consumer spending.

UBS (UBS) also highlighted that consumers have continued to trade down, moving away from premium products, given the weaker macro conditions.

Wall Street analysts remain lukewarm over the company’s medium-term prospects, likely modeling for a difficult transition from its tobacco products.

Accordingly, Altria is projected to report revenue growth of 1.3% in FY23, accompanied by adjusted EBIT growth of 2.1%. While there is inherent operating leverage in Altria’s operating model, its topline growth seems unconvincing relative to its market leadership.

Despite that, Altria boasts a solidly profitable business model, as it’s still expected to report an adjusted EBIT margin of 58.4% in FY23, slightly ahead of FY22’s 58%.

Therefore, investors should expect Altria to maintain its pricing leadership and not anticipate adverse pricing action to protect its market share.

Moreover, the macroeconomic doom and gloom may have been overstated. There are signs that the global economy may not experience a hard landing. In addition, a recent Fed study also enunciated that the US economy could potentially avoid a recession. Moreover, the consensus view of a hard landing has downshifted recently, with economists less pessimistic.

As such, we believe the consensus estimates are credible, as Altria has proved its profitability over the past five years, including during the COVID pandemic.

MO price chart (weekly) (TradingView)

MO buyers need to return with more conviction to push past the December resistance zone, which saw sellers rejecting further upside.

However, we gleaned constructive price action last week, despite the steep selloff. Buyers returned to help stanch further downside, recovering more than 50% of the losses from the pullback.

Hence, we believe it suggests that buyers are confident in supporting MO at its currently battered valuation. Moreover, we believe the steep pullback last week has likely flushed out some weak holders, de-risking the entry levels for patient buyers.

Rating: Buy (Revise from Hold).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment