ipopba

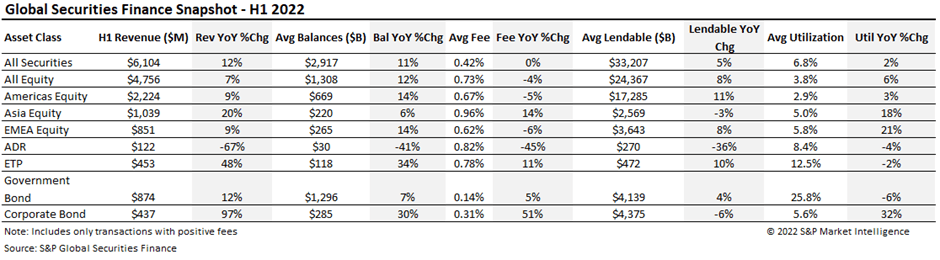

Securities finance revenue $6.1bn in H1 2022, best half-year performance since 2008

- H1 revenue increased 12% YoY

- ETP special balance hit 4-year high

- Corporate bond revenues continue to set blistering pace

- US Equity special balances hit 4-year high

Global securities finance revenues reached $6.1bn in the first half of 2022, an increase of 12% YoY. Utilization and lendable assets saw marginal increases, while average loan balances continue to surge, increasing 11% YoY. Average fees showed mixed results but were led by Asian Equity specials in South Korea and Taiwan, in addition to corporate bonds pairing rising balances with growing fees. US equity special balances rebounded strongly from a poor H2 2021, posting a 4-year quarterly high. ETP average special balances crossed the $2bn mark for the first time in 4 years, driving a strong first half of the year, resulting in revenues increasing 48% YoY. Corporate bond earnings climbed the most YoY, rising 97% whilst ADR revenues faltered, declining 67% YoY.

Americas equity finance revenues came in at $2.2bn for H1 2022, a 9% YoY increase. Special balances rebounded powerfully, crossing $18bn on average as Q2 set a 4-year quarterly high. Both US and Canadian Equity balances rebounded, posting revenue gains of 8% and 5%, respectively. The increases were driven by growing balances (14% and 23% YoY) that offset the declines seen in average fee spreads. Lucid Group, Inc. (LCID) was a top performer in H1 2022, generating $150mn in revenues and ranking as one of the highest revenue generators over the past several years.

Equity finance revenues in Europe rebounded strongly during the first half of 2022, increasing 9% YoY. This growth was supported by a recovery in specials and an increase of 14% in average balances which outweighed a decline of 6% in fee spreads. Lendable assets continued their rise, with an increase of 8% YoY, and much like balances, utilization rose an impressive 21%. While two key markets in the region, France and the UK, saw revenues decrease 15% and 10% respectively, several markets prospered in the first half of 2022. Norwegian equities led the charge as revenues surged 60% over the previous year, while Swedish, Swiss, and Italian equities saw their revenues grow in excess of 30% which was largely driven by a combination of significant increases in average balances and fee spreads. German equity revenues grew by a modest 16% over the period, driven by two of the top three earners in European equities Varta AG (OTC:VARGF, OTCPK:VARTY) and Mercedes Benz Group AG (OTCPK:MBGAF, OTCPK:DMLRY).

While APAC equities did not match the performance of H2 2021, the region returned over $1bn in revenue representing a 20% YoY increase. This was driven in large part by the fee spreads jumping 14%. Special balances retreated compared with H2 2021 levels but maintained their strong recovery following the lifting of short sale bans. South Korea and Taiwan delivered the highest YoY returns, with returns close to doubling compared to the prior year. Australia was the only market to exceed returns compared to H2 2021 as fee spreads jumped 68%. Australia’s top earner, BHP Group Ltd (BHP) claimed the 4th place out of all Asian equities, generating $12.65mn in revenues while three Korean names, Krafton Inc, LG Energy Solution Ltd, and Kakaobank Corp grasped the top 3 spots.

Global ETP lending revenues were $453mn for H1, continuing to set new all-time highs, representing a 48% YoY increase. March set the mark as being the top revenue-generating month, crossing $85mn. There were several drivers contributing to the record-breaking numbers, but the rise of special balances set the blistering pace. ETP average special balances in Q2 crossed the $2bn mark, setting a new high across several years and a 52% increase when compared with Q2 of 2021. Fixed Income ETP lending generated $167mn in H1, representing 37% of global ETP returns. Maintaining consistency, 9 of the top 10 revenue generating assets were US ETPs as the iShares iBoxx $ High Yield Corporate Bond Fund (HYG) held onto its top rank as the best earner for the 3rd consecutive half-year period generating $66mn in fee spread returns.

With no top earner to lead the charge, unlike prior half-year periods, Depository Receipt returns fell to $164mn representing a 60% YoY decrease. ADRs represented 74% of the total Depository Receipts revenues with $122mn generated, a 67% YoY decrease. ADR underperformance was comprehensive, as average balances decreased 41% alongside a similar decrease in fee spreads of 45%.

Corporate bond lending revenues continued their ascension in the first half of 2022, reaching $437mn, boasting a 97% YoY increase. Sparked by increasing balances (up 30% YoY) and fees (up 51% YoY), H1 2022 marks the highest lending revenue for corporate bonds since the start of the pandemic. Average loan balances reached $285bn, the highest since the 2008 financial crisis. Q2 delivered stellar returns, with May revenues reaching just under $74mn, the highest monthly revenue in several years.

Fee-based revenue for government bond lending came in at $874mn for H1, the largest in several half-year periods and up 12% YoY. Government bond borrow demand remained robust, with $1.3bn in positive-fee global balances for H1, reflecting a 7% YoY Increase improving upon 2021 H2’s lofty mark. Securities finance returns from lending US Treasury securities in H1 2022 represented 52% of the positive fee-spread income. Revenues from European sovereigns were $317mn, up 27% YoY driven by a robust increase in average balances and fees of 11% and 15%, respectively. Emerging Market bond fee spread returns eclipsed $37mn posting a strong increase of 59% when compared with the previous year. The highest revenue-generating bond was the UST due Feb 2024 (CUSIP 91282CEA5) which generated $10.9mn in revenue, which was better than any government issue over the past 12 months. Much like H2 2021, 7 of the top 10 revenue-generating bonds are USTs.

Conclusion

2022 is off to an impressive start for Securities Finance revenues, clearing $6.1bn in fee spread returns, which is the highest for a half-year period since H1 of 2018. Whilst not quite at the pace needed to eclipse 2008 full-year revenues, 2022 is well poised to deliver the strongest performance since the global financial crisis. All core asset classes supported robust returns except for ADRs which declined. Exchange-traded products and corporate bonds remained the top performers for the second consecutive half-year period, delivering considerable returns. Fixed income assets were key, as the top 3 performing ETPs were bond related. Overall, increasing balances across the main asset classes were the key linchpin to a strong H1 2022.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment