designer491

Co-produced with “Hidden Opportunities”

Preferred securities are an essential class of investment instruments for a diversified income portfolio. These securities are more defensive than equities and provide relatively better protection from market volatility. This is because most preferreds are senior to equities but subordinate to senior corporate debt from a capital structure standpoint.

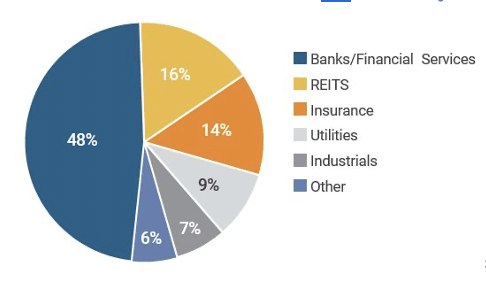

Preferreds are not new in the financial world. The first use of these instruments can be traced back to 16th century England. However, the modern version of tradable preferreds began being widely issued in the 1980s by U.S. financial firms to build capital structures to meet ever-changing regulatory requirements. Today, preferreds are widely issued by banks, REITs, insurance companies, utilities, industrials, and other sectors of the economy to raise capital.

Advisor Perspectives

I have invested $1 million in preferred securities and continue to add to my position during this market volatility. That investment at an average 8% yield will produce $2 million in dividend income over 25 years. Thanks to the market’s fears, I can buy higher quality and well-covered preferreds with a significant capital upside. We have two excellent preferred picks to get you started down the path of building a more robust and reliable income stream.

SPNT-B Preferred Stock – Yield 9.3%

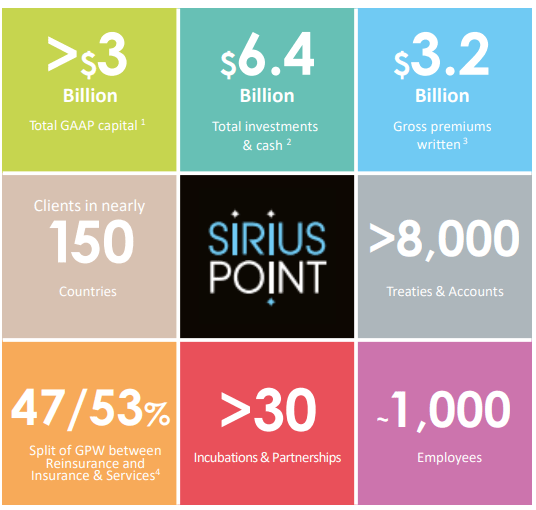

SiriusPoint Ltd. (SPNT) provides multi-line insurance and reinsurance products and services worldwide. The company operates through two primary segments – Reinsurance and Insurance & Services. They provide insurance solutions to clients and brokers in almost 150 countries. (Source)

SirusPoint

SPNT was formed in February 2021 due to a merger between Third Point Reinsurance and Sirius Group. As a business, SPNT is on a transformative path, with a strong focus on the improvement of its reinsurance underwriting results and the growth of the Insurance & Services segment. In the first half of 2022, SPNT reported a combined ratio of 93.4% and is on its path toward sustained profitability.

The company maintains a strong balance sheet with a financial strength rating of A- from AM Best, S&P, and Fitch. But we are less interested in SPNT common stock. Our eyes are on the prize that is the SiriusPoint Ltd 8% Series B Cumulative Resettable Fixed Rate Preference Shares (SPNT.PB). This security carries a BB+ credit rating from S&P and Fitch and presents a compelling opportunity for several reasons. Let us explore them.

For more than 40 years, the London Interbank Offered Rate (known as LIBOR) was a key benchmark for setting the interest rates charged on adjustable-rate loans, mortgages, and corporate debt. However, LIBOR has been burdened over the last decade by numerous scandals and crises. Effective December 31, 2021, LIBOR will no longer be used to issue new loans in the U.S. The sunset of LIBOR is unleashing a new trend of issuing resettable preferred stocks whose coupons are adjusted based on the generally higher-yielding 5-year U.S. Treasury Note.

This brings us to why SPNT-B is a rare golden nugget in the basket of preferred securities. This preferred has a high coupon at present (8%) and can have an even higher coupon after its call date since it is a resettable fixed-rate security. Current price levels give it an attractive 9.3% yield. After Feb 2026, SPNT-B’s coupon will be 7.298% + the 5-yr Treasury yield on the calculation date. SPNT-B may be called on 2/26/2026 or on any subsequent 5-year Reset Date. Every 5-year anniversary, SPNT will have the option to call SPNT-B or to commit to another 5 years at a new rate.

Author’s Calculations

The average 5-Year Treasury yield in the past 20 years is 2.27%, and its minimum yield in the same period is 0.19% (during the beginning of the COVID-19 crisis). In either case, after the call date, if the security is not called, we are looking at a coupon that is producing a high yield relative to interest rates, making SPNT-B a great pick for income investors.

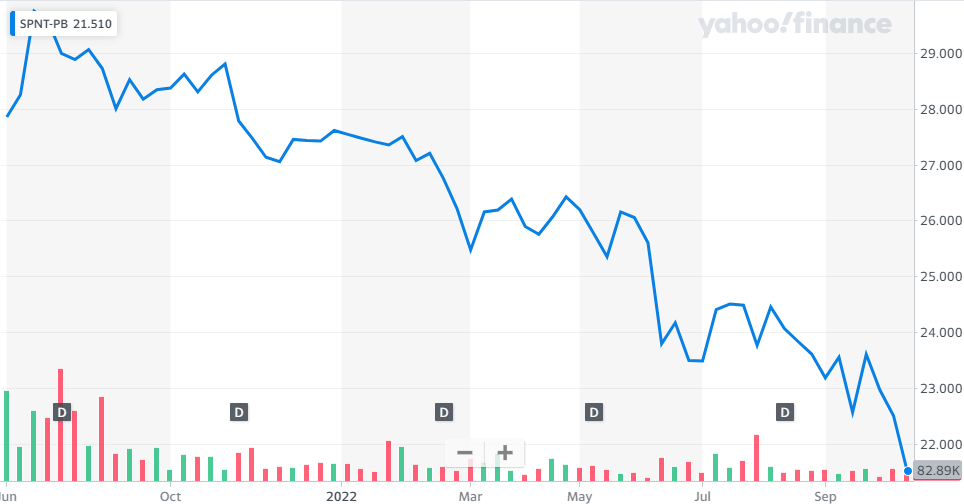

What makes SPNT-B even more attractive is the fact that this golden nugget is significantly undervalued. The stock is trading at a 14% discount to its par value of $25, making it a compelling buy at current levels.

Yahoo Finance

The cherry on top is that SPNT-B dividends are “qualified” for a lower 15% tax rate for most investors, when held in a taxable account.

SPNT-B dividends cost the company $4 million per quarter. It is noteworthy that SPNT ended Q2 with ~$1.4 billion in cash on their balance sheet. Considering their ~$10 million in annual interest expenses and improving business fundamentals, it is safe to say that SPNT-B dividends are well protected.

SPNT-B is a relatively new preferred stock that is undervalued, pays qualified dividends, and has among the highest coupons in its league. Take advantage of this market selloff and add this resettable rate preferred to your portfolio for ultimate inflation and rate hike protection.

AHL-D Preferred Stock – Yield 7.4%

Apollo Global Management, Inc. (APO) acquired Aspen Insurance Holdings in 2018 in an all-cash transaction. APO is one of the largest asset-management firms in the world, and both APO and its subsidiary Aspen maintain healthy “A” rated balance sheets.

Aspen provides reinsurance and insurance coverage to clients in various domestic and global markets through wholly-owned subsidiaries and offices in Australia, Bermuda, Canada, Singapore, Switzerland, the United Kingdom, and the United States. While Aspen ceased operating as a publicly traded firm in 2019, its preferreds remain public. We are particularly interested in Aspen Insurance Holdings Ltd, 5.625% Perpetual Non-Cumulative Preference Shares (AHL.PD), which presents a meaningful income opportunity with a sizable capital upside.

At the end of 1H 2022, Aspen reported double-digit top-line growth and very healthy underwriting performance, resulting in a 6.5% improvement in their combined operating ratio to 88.2% from 94.7%. The company also reported an investment income of $88.7 million during this period, a 30% improvement YoY.

The company paid $22.2 million towards preferred dividends during 1H 2022, a sum that is well covered (218%) by their net income of $48.4 million during the same period. AHL-D trades at a 25% discount to par value and comes with a 7.4% yield. To sweeten the pot, these preferred dividends are qualified, making them eligible for favorable tax treatment when held in a taxable account.

Author’s calculations

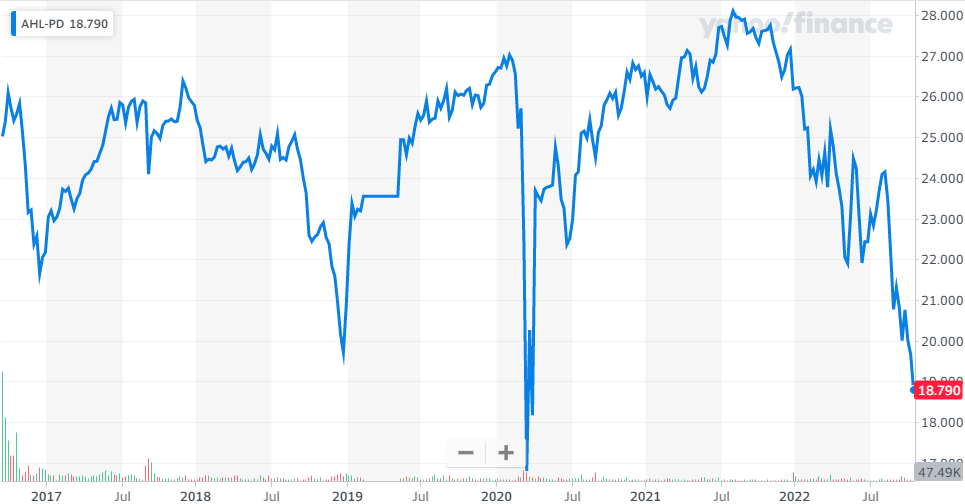

Additionally, AHL-D is rated Ba1, BB+ by Moody’s and S&P. What makes this preferred attractive today is its attractive valuation. AHL-D has experienced a sharp drop in recent weeks, resulting in a price level that we have only seen three times since its inception. For net buyers of quality income, this is a solid opportunity to pick up shares, collect dividends and set yourself up for up to +30% upside to par.

Yahoo Finance

It is noteworthy that AHL-D has traded at healthy premiums to par during past bull market cycles. Rising interest rates are generally favorable for the insurance industry. When rates rise at a reasonable pace, portfolio yields also rise. With these new, higher-yielding corporate and other bond purchases, insurers’ investment income also increases, providing better earnings coverage for preferred investors. AHL-D presents a quality preferred by a firm with solid credit ratings and business fundamentals. Well-covered 7.4% yields to keep calm, ride this roller coaster market, and set yourself up for a significant upside.

Shutterstock

Conclusion

Preferred securities may seem complicated, but we are here to demystify their potential. The average investor often overlooks these valuable income generators due to their perceived complexity. A basket of fixed and variable-rate preferred instruments becomes a strong ally for income investors, particularly when they are purchased at discounted prices amidst broader market weakness. The HDO model portfolio has over 60 preferreds and baby bonds, and we provide regular updates to our subscribers. Since these securities are thinly traded, not all of our coverage and analysis are shared with the public.

Preferred securities issued by high-quality companies are usually rated a step or two down from their debt. For example, an entity issuing preferred security with a BB would typically have investment-grade senior unsecured debt rated BBB or higher. As such, they provide a high degree of safety and are among the best risk-reward opportunities in this market sell-off. I am adding more reliability, stability, and consistency to my income stream with discounted preferreds. Two picks with up to a 9% yield to get you started.

Be the first to comment