Marlon Trottmann

Introduction

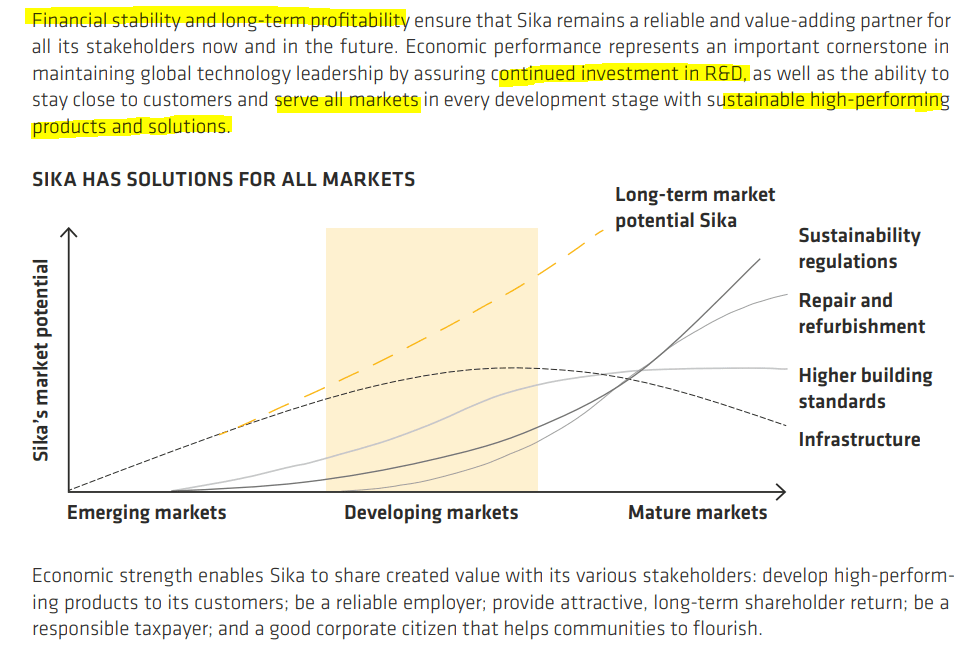

Despite the ebbs and flows of global growth, one industry has a pattern of fairly stable linear growth: construction. Whether the work is to develop critical infrastructure for emerging markets, establish higher building standards in developing markets, or allowing for sustainability and refurbishment of mature developments, construction never truly gets put on the back-burner despite lack of government funding. This article will highlight one major player in the industry and provide industry data that will influence the investment opportunity.

Sika AG (OTCPK:SXYAY) is a Swiss chemicals conglomerate that provides products and solutions for the entire industry, and all areas of the market around the world. As such, Sika is a clear beneficiary of growing populations, renewed infrastructure investment, and the even movement towards more sustainable developments. With a range of products and global diversification, the company has a pattern of fairly stable financials, and the low cyclicality is a key feature. I believe Sika is worth consideration for investors looking to leverage the ever-lasting global need for construction materials, and the low volatility supports recurring investments.

Sika 2021 Annual Report

Sika’s Opportunity

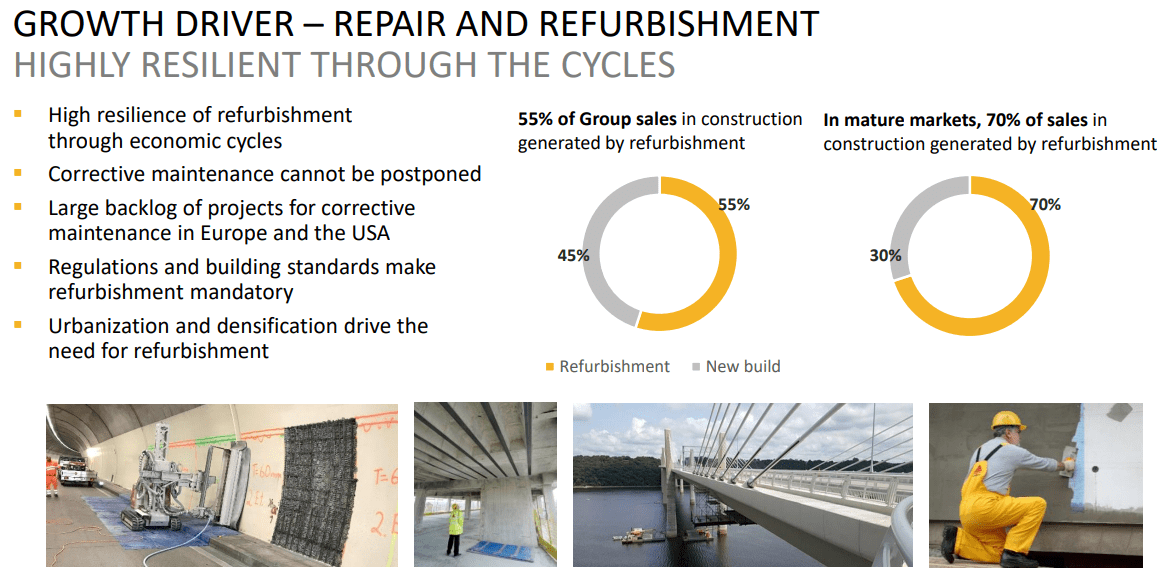

While new construction is clearly an opportunity around the world, a catalyst for the next few years is based on repair and refurbishment. With major governments allocating billions for infrastructure projects in developed nations, Sika is a clear beneficiary. The company also offers competitively sustainable products that meet regulatory ambitions for low environmental impact, further suggesting success is in the future. As I will discuss with the financial data, Sika really seems like the industry leader.

Sika 9M22 Presentation

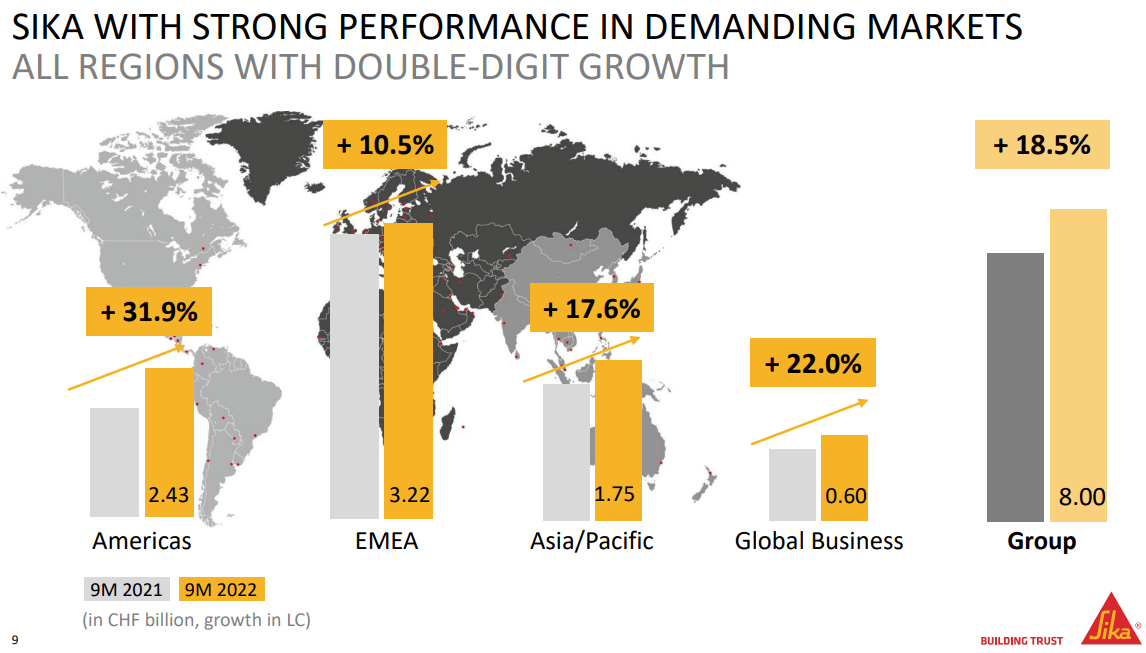

Sika is currently seeing a favorable bull market after the pandemic, despite supply chain issues, slowing demand, and inflation. The first 9 months of 2022 saw strong growth in all revenue regions, highlighting success across all construction formats. However, it is important to note that not all growth is organic, and approximately 50% of all revenue growth is anticipated to be the result of acquisitions. Thankfully, this also comes with a healthy amount of lagging asset divestiture and internal R&D, leading to a more sustainable growth pattern. In fact, opportunity is present in emerging market expansion as evident by recent plant openings in Ivory Coast, Tanzania, and Bolivia. Balancing these growth opportunities will be difficult, but I believe the historical data will suggest that Sika can succeed.

Sika 9M22 Presentation Sika 9M22 Presentation

Financials

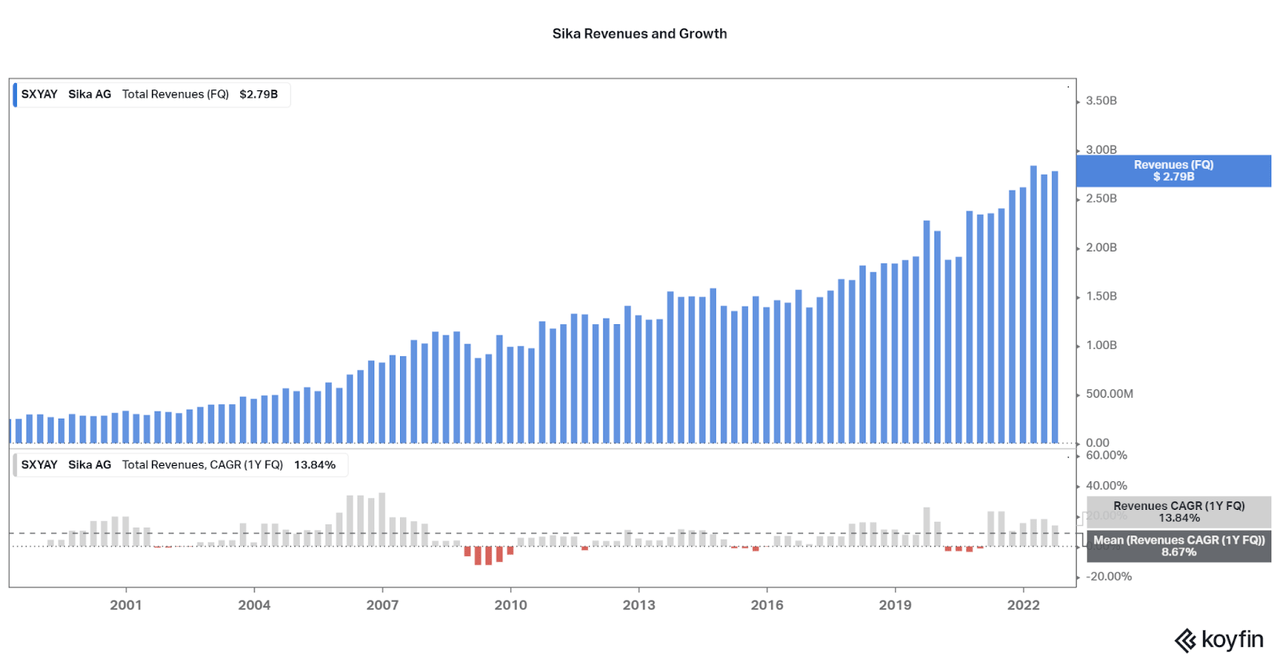

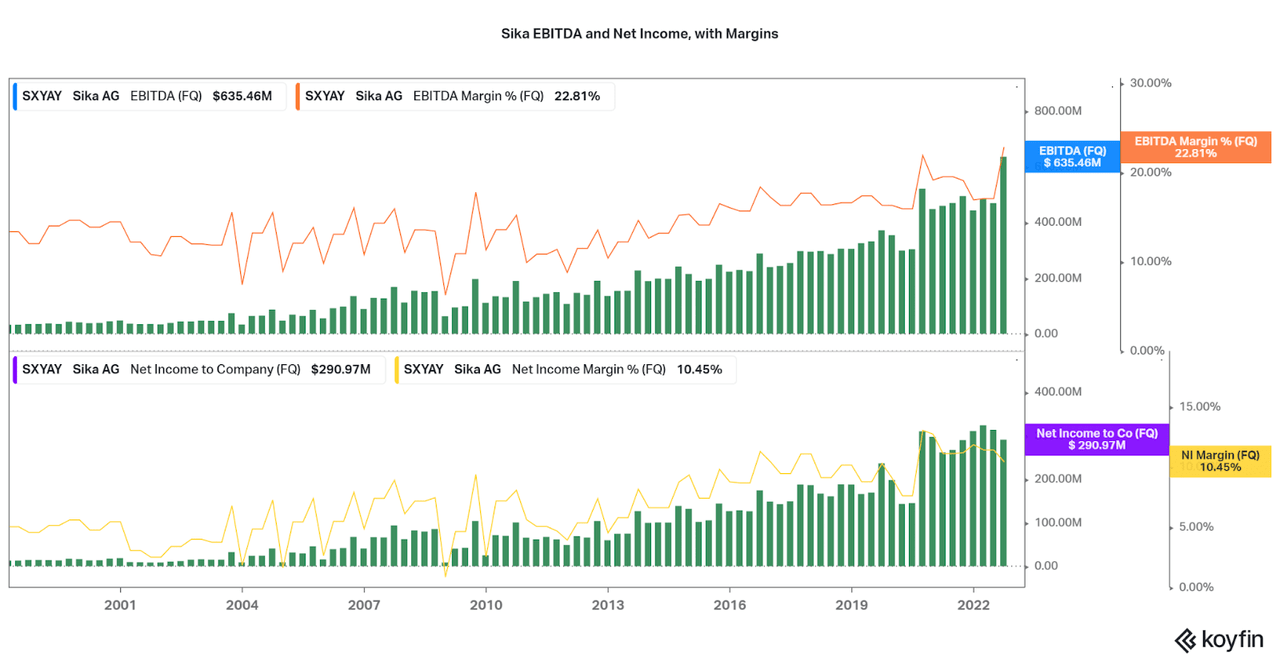

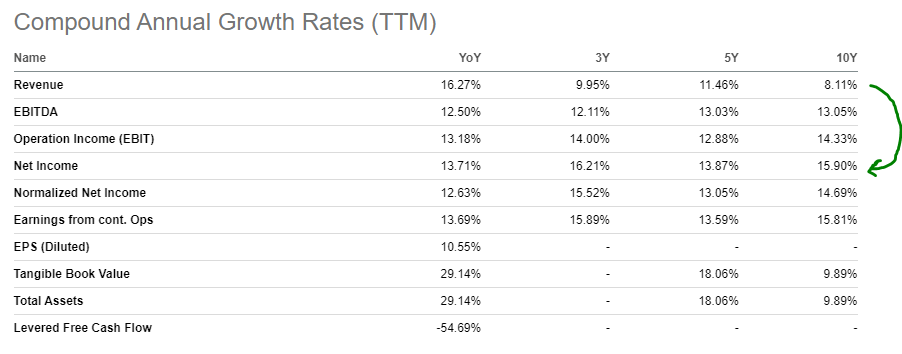

As investors have access to over 20 years of financial data, one pattern is clear: low cyclicality revenue growth. Apart from a few periods of negative growth in 08-10, the mid-2010s, and the pandemic, Sika has strong forward momentum. The long-term mean growth rate is over 8%, driven by the organic and inorganic growth factors I have discussed. The revenue data looks far less cyclical than other commodity and materials peers, and highlights the company diversification and strength of the construction industry. An average revenue growth rate of 8% is a good target to meet moving forward. I would look for Sika to maintain these levels.

Koyfin

Along with stable revenue growth over the past 25 years, margins have been steadily improving since 2010. As a chemical company, the current 22.8% EBITDA and 10.45% Net Income margin levels are not the highest, but well positioned for further expansion. The improvements over the last few years can be attributed to the culling of weak product lines and subsidiaries, along with investments in higher margin products. I expect that this pattern of success can continue despite any market weakness that occurs in the coming years. At any rate, I do not fear operational losses anytime soon, and look forward to the returns based on margin expansion.

Koyfin

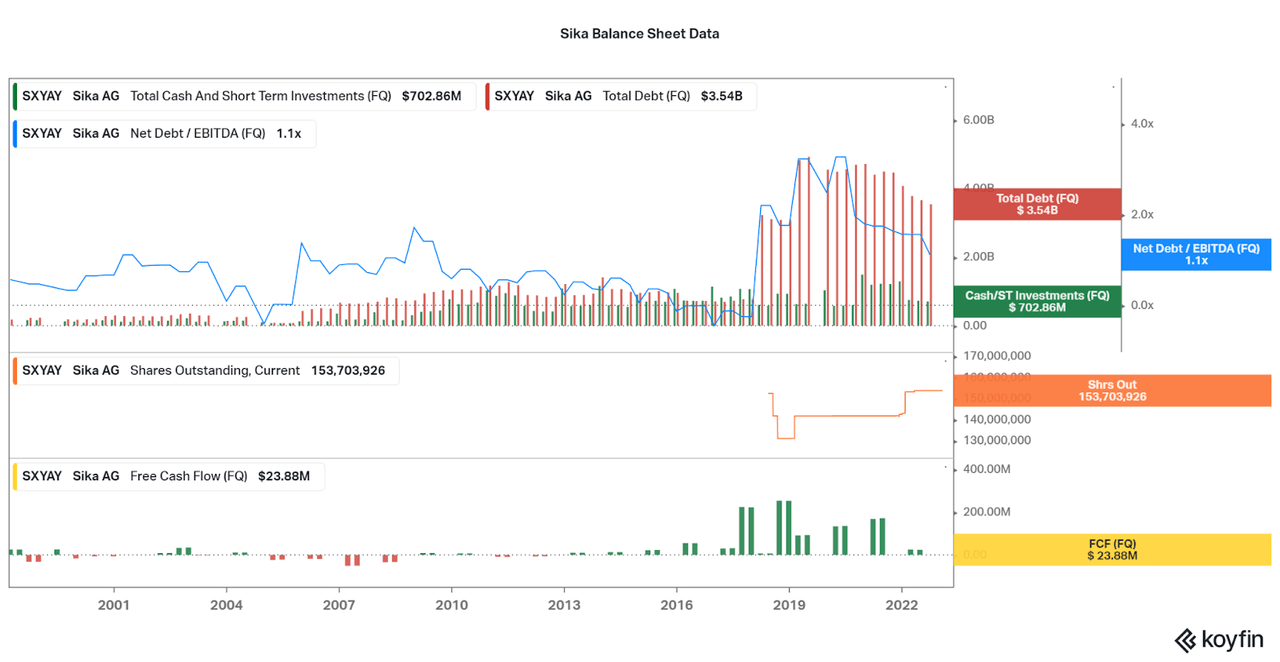

There is one weak point to consider. Despite the strong profits, Sika has taken on debt over the past 3 years, partly to pursue acquisitions. Now, the total debt is reaching $3.5 billion USD, while cash is at $700 million. Thankfully, leverage remains low at 1.1x net debt / EBITDA. Also, we have little insight into how the company manages their shares due to the recent listing. Currently, some dilution is occurring, partly to fund the acquisition of the former BASF (OTCQX:BASFY) construction chemicals segment, MBCC. Upon completion of the deal, which requires selling off assets, we should have more clarity on the balance sheet. At the moment, I would not worry about the leverage, but will frown upon additional dilution.

Koyfin

Outlook

While the financials are competitive, healthy, and indicate success despite economic headwinds, it is also important to assess current outlook data. The limited cyclicality suggests recurring investments are favorable for the company, but the broader market certainly is expecting a recession. However, there is a variety of information we can look at to temper our expectations for the construction market.

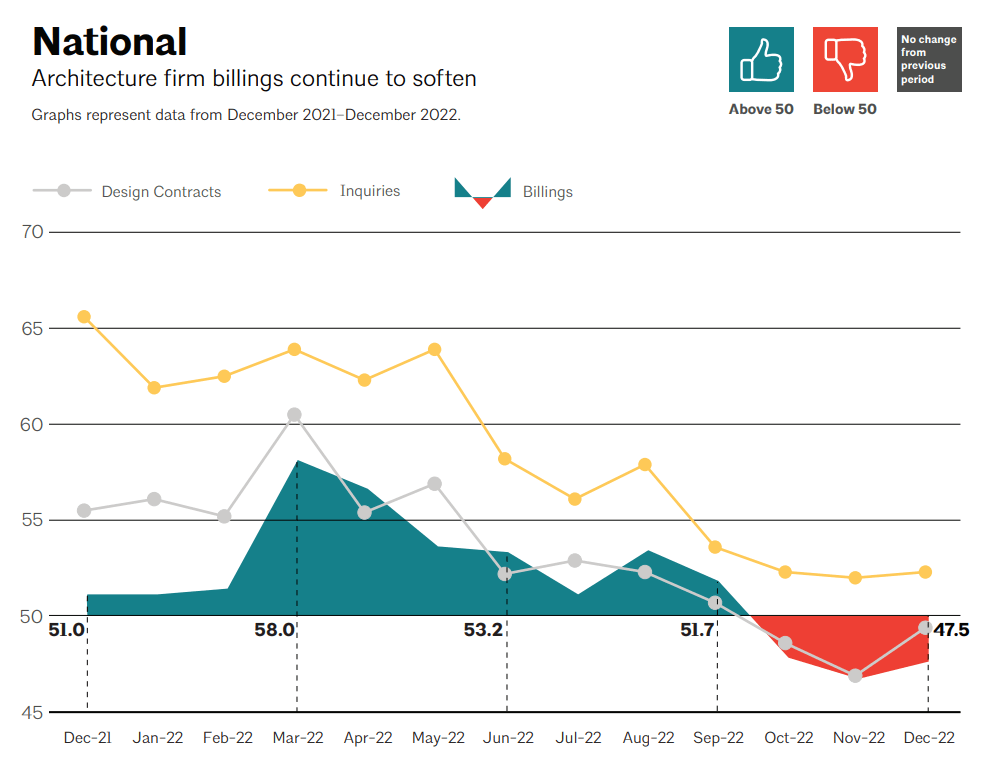

First, there is the data provided by the AIA who poll architectural firms around the world on their contracts and billings. While 2022 saw a rebound from pandemic headwinds, the past three months have seen poor market conditions of lower contracts, inquiring, and billings. Sentiment is currently poor, and this may suggest trouble over the coming project lifecycles, or 6 months to multiple years. Although, this data is only based on US architecture, and Sika is diversified around the world. Also, periods of weakness are opportunities for investors to capitalize (although this means the next few earnings may be poor).

AIA

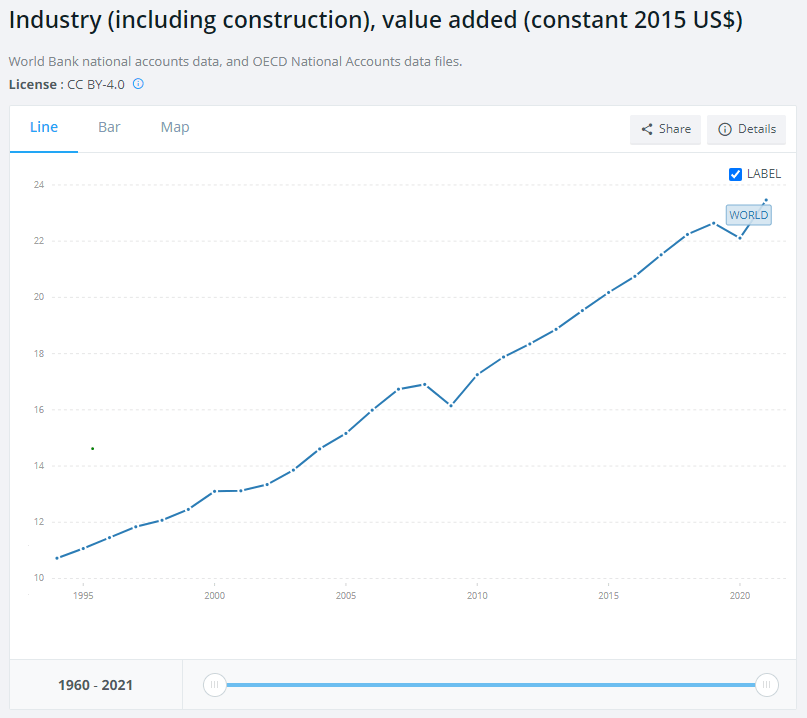

While the next few months may be difficult for earnings, there is plenty of long-term data to rely on. According to the World Bank, industry growth has been fairly consistent over the past 30+ years, despite temporary black swan events. This suggests that even if there are a few quarters of a bear market, things turn around quickly. Sika’s historical financial data leads me to believe this thesis is true. Therefore, there is little reason to trade the cyclicality, and investors should just continue accumulating shares for the long term.

The World Bank

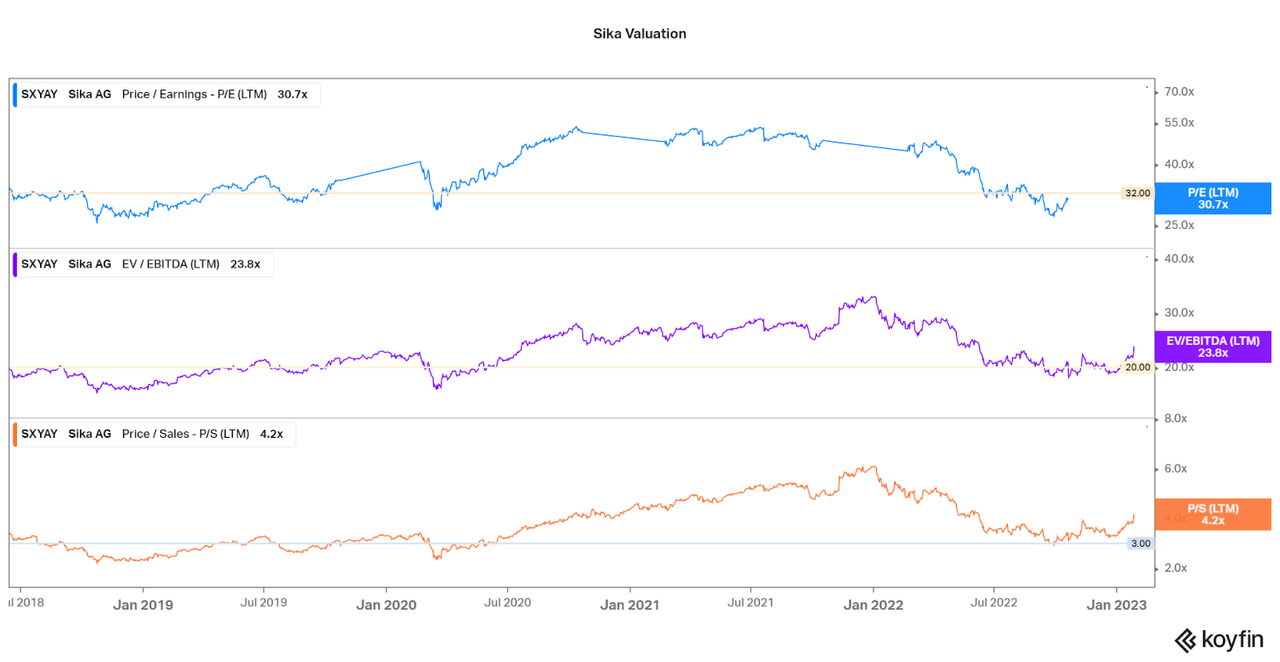

Valuation

The last consideration is whether the valuation supports the current investment. While the financials support long-term additions, regardless of price, shares have been volatile the past few years. In fact, shares fell over 50% from highs seen in 2022, although they are rebounding of late. However, there are a few factors to consider. First, due to higher profitability, the P/S seems high, but the P/E and EV/EBITDA are more acceptable. We also have to consider the underlying strength of the business, which is strong, allowing for a higher valuation. Then, we also have to consider the peer group, which underperforms while also being just as expensive.

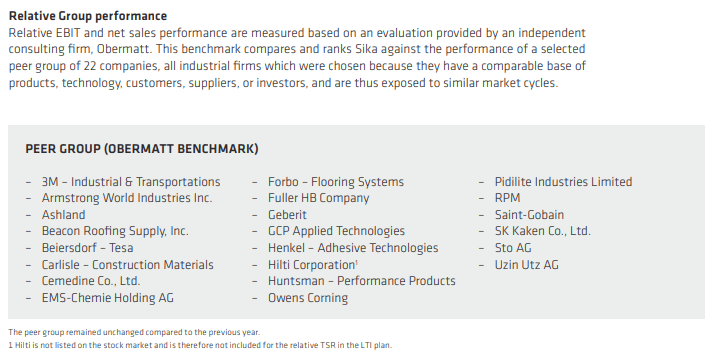

For an idea of the peers, please see the image below. While I believe recurring investments will pan out well, risk-averse investors can wait to see how the next few months pan out. The AIA data on architectural billings certainly allows for downside opportunity, but this may be baked into the price already. Then, there is the potential for the large MBCC acquisition to be approved, leading to a jump in inorganic growth to make up for the high valuation.

Koyfin Sika 2021 Annual Report

Conclusion

The key differentiation in opportunity for Sika when compared to the chemical peers above is growth. While some like 3M (MMM) have larger moats and diversification, Sika offers more stable and faster growing revenues and earnings. Only one company on the list is similar over the past 10 years, Owens Corning (OC), although cyclicality is more volatile for the insulation makers. Even strong performers such as Ashland (ASH), who have shed billions worth of lagging assets to drive earnings growth, offer less stability and positive outlook when compared to Sika. Therefore, I will continue to believe that with recurring investments, Sika is worth any price.

Seeking Alpha

I am sure some may hesitate to invest at current levels, and that is fine. Each investor must consider their own circumstances and risk tolerance. For me, I have a long-term mindset and will prefer slowly accumulating for years to come. I believe that Sika will provide a stable cornerstone of most portfolios and offer exposure to the world’s ever-growing construction industry. With the well-managed combination of organic and inorganic growth, I believe that Sika will continue to outperform the US-Large Cap market via (SPY)(VOO). Sika will help lead Swiss ETFs such as the iShares MSCI Switzerland Capped ETF (EWL) where they are currently weighted 9th. In the end, betting on humanity’s construction is always a sure bet, and far less speculative than other future facing bets.

Thanks for reading.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment