SimonSkafar/E+ via Getty Images

Investment Thesis

PPL Corporation (NYSE:PPL) is an American energy company based in Allentown, Pennsylvania. In this thesis, I will be analyzing the strategic acquisition of Narragansett Electric Company and its impact on the future of PPL. This acquisition is a part of PPL’s strategy to expand its operations in the United States and reposition itself as a U.S.-focused energy company. I will also discuss the company’s dividend yield and its growth prospects. As per my analysis, PPL is on a growth track and has a strong balance sheet to support this growth. I assign a buy rating for PPL after taking into consideration all the growth and risk factors.

Company Overview

PPL is an essential energy service provider, currently serving 3.5 million customers. PPL has its presence in four states: Pennsylvania, Rhode Island, Virginia, and Kentucky. The company provides electricity in all four states and also provides natural gas in Kentucky and Rhode Island. PPL Corporation is a parent company with four subsidiaries operating under its name. The four subsidiary companies are Louisville Gas and Electric and Kentucky Utilities, PPL Electric Utilities, Rhode Island Energy, and Safari Energy. Safari Energy is engaged in providing solar power solutions across the United States, while the other three companies are primarily electricity and natural gas providers. The company is focused on providing renewable energy solutions and is trying to adopt new energy solutions through continuous innovations.

Narragansett Electric Company Acquisition

PPL completed the acquisition of Narragansett Electric Company on May 25, 2022. PPL then renamed Narragansett Electric Company to Rhode Island Energy. PPL acquired the Narragansett Electric Company from National Grid in a deal valued at $3.8 billion.

Rhode Island Energy is the primary electricity and natural gas provider in the state of Rhode Island. Rhode Island Energy currently provides energy and related services to around 770,000 homes and businesses in the state. This acquisition is a part of PPL’s strategy to position itself firmly in the U.S. and expand its operations across the country. As a part of this U.S.-focused strategy, the company sold its UK utility business to National Grid in June 2021 for $11 billion. As per my analysis, this acquisition will positively impact the firm’s revenues and profit margins, the result of which we will witness in the upcoming quarters. This acquisition is expected to increase the profit margins of the firm significantly. More importantly, I believe this is a start of a bigger expansion plan of PPL in the U.S. energy market.

After the completion of this acquisition, Moody’s upgraded the rating of PPL and PPL Capital Funding, including its senior unsecured rating, from Baa2 to Baa1. Moody’s has also upgraded the senior unsecured and issuer ratings for Narragansett Electric Company, now Rhode Island Energy, from Baa1 to A3. I believe these rating upgrades are a reflection of PPL’s improved risk profile in the U.S. energy market.

PPL President and Chief Executive Officer Vincent Sorgi, stated,

These ratings upgrades reflect the improved financial strength of the new PPL following the sale of our U.K. utility business in 2021 and our recent acquisition of Narragansett Electric. As a result of our strategic repositioning, today’s new, U.S.-focused PPL has one of the utility sector’s best credit profiles, a balance sheet capable of supporting robust growth without equity needs for the foreseeable future, and a de-risked business plan to drive significant value for our shareowners and customers moving forward.

Dividend Yield Growth Prospects

PPL declared a quarterly dividend of $0.225 on 9th June 2022, a 12.5% increase from the last quarter. At the current price level, the dividend yield stands at 3.31%. The company slashed the dividend by 52% in Q4 from $0.415 to $0.20, owing to the cash management exercise. I believe with the acquisition of Narragansett Electric Company and improved margin in the existing business, the dividend payment can attain its previous levels of $0.415. The management has also given a positive future outlook and expects the earnings to increase significantly in the coming quarters. The company has been consistent in dividend payments, with a consistent quarterly dividend of $0.415 since 2020. I believe the reduction in the dividend payout in the last quarter was temporary, and we will see an increase in the dividend payout in the coming quarters.

Financials

SEC:10Q PPL Corporation

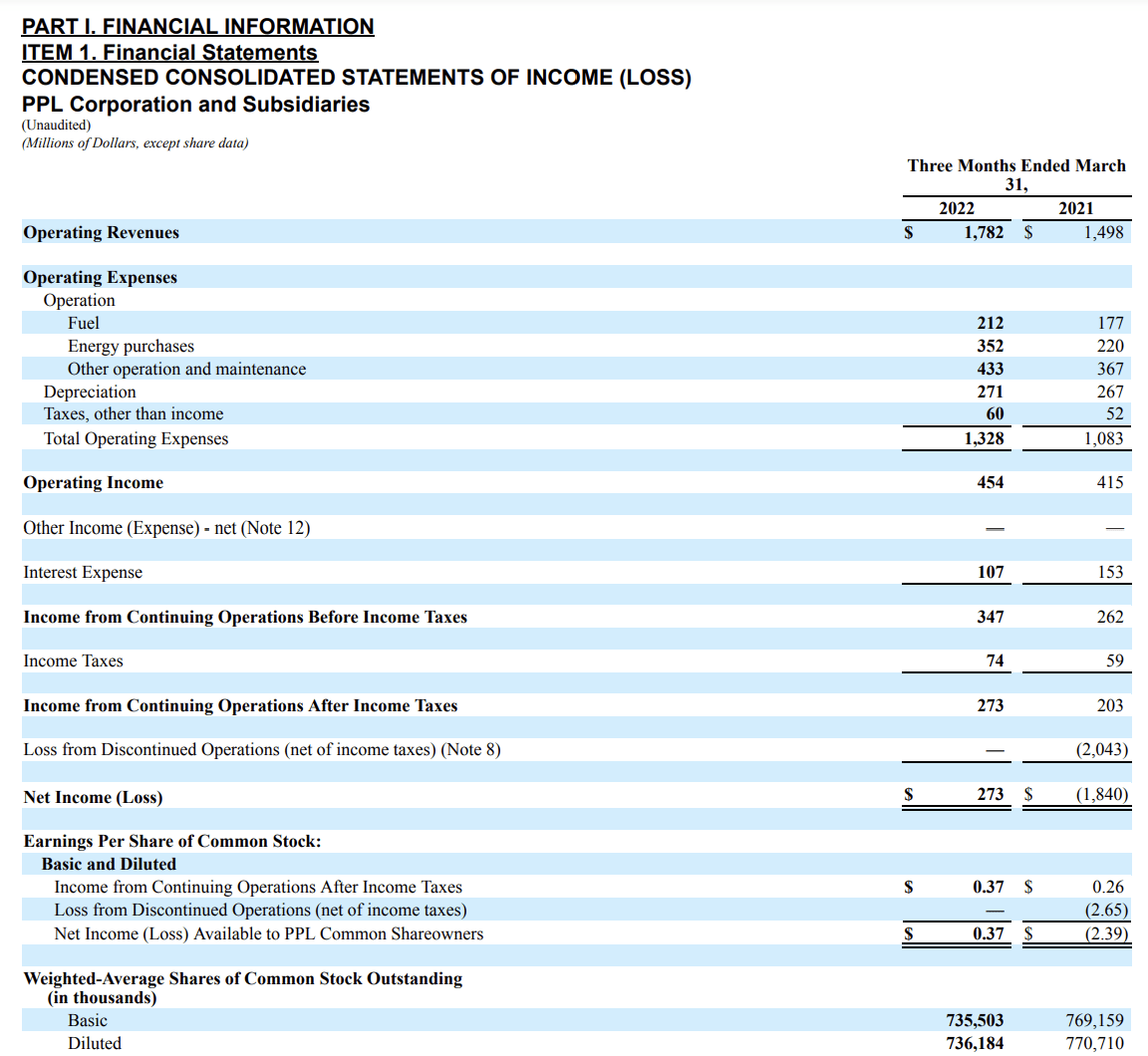

Recently, PPL Corporation announced its Q1 FY2022 results. The company reported operating revenue of $1.8 billion, which is a 19% increase as compared to the $1.5 billion of Q1 FY2021. The company reported operating expenses of $1.3 billion, which is 23% higher than the $1.1 billion in the same period of the last quarter. The company’s operating income has increased by 9.3% in the last 12 months. I think, despite a 23% increase in the operating expenses, the operating profit has increased moderately, which is a sign of good operating leverage of the company. The company reported net earnings of $273 million, which is a significant improvement as compared to the net loss of $1.8 billion in the previous year’s same quarter. The loss of the last year’s quarter was mainly driven by the loss from discontinued operations of PPL’s former U.K. utility business. The EPS of continuing operations of Q1 FY2021 was $0.26 while the EPS loss of discontinued operations was $2.65. The EPS of the Q1 FY2022 is $0.41 per share, and after adjusting for the expenses that occurred while integrating the acquisition of the Narragansett Electric Company, the EPS for the quarter is $0.37.

Investor Relation of PPL Corporation

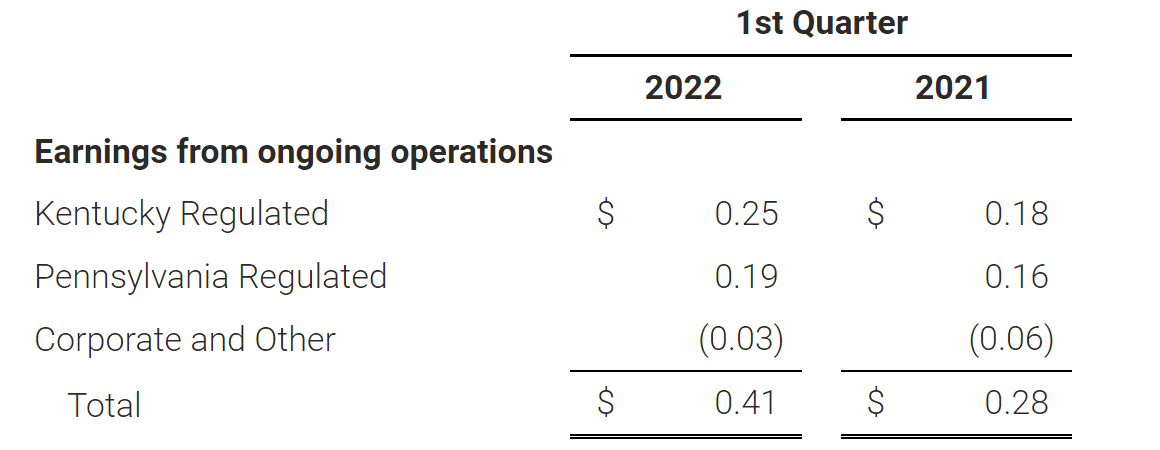

The contribution of Kentucky regulated earnings is 61%, and the contribution of Pennsylvania Regulated earnings is 46%. The corporate and other has generated a loss of $0.03. The rising retail rates, higher peak transmission demand, returns on additional capital investments in transmission and higher sales volumes are the main factors behind the growth in Kentucky and Pennsylvania Regulated operations.

SEC:10Q PPL SEC:10Q PPL

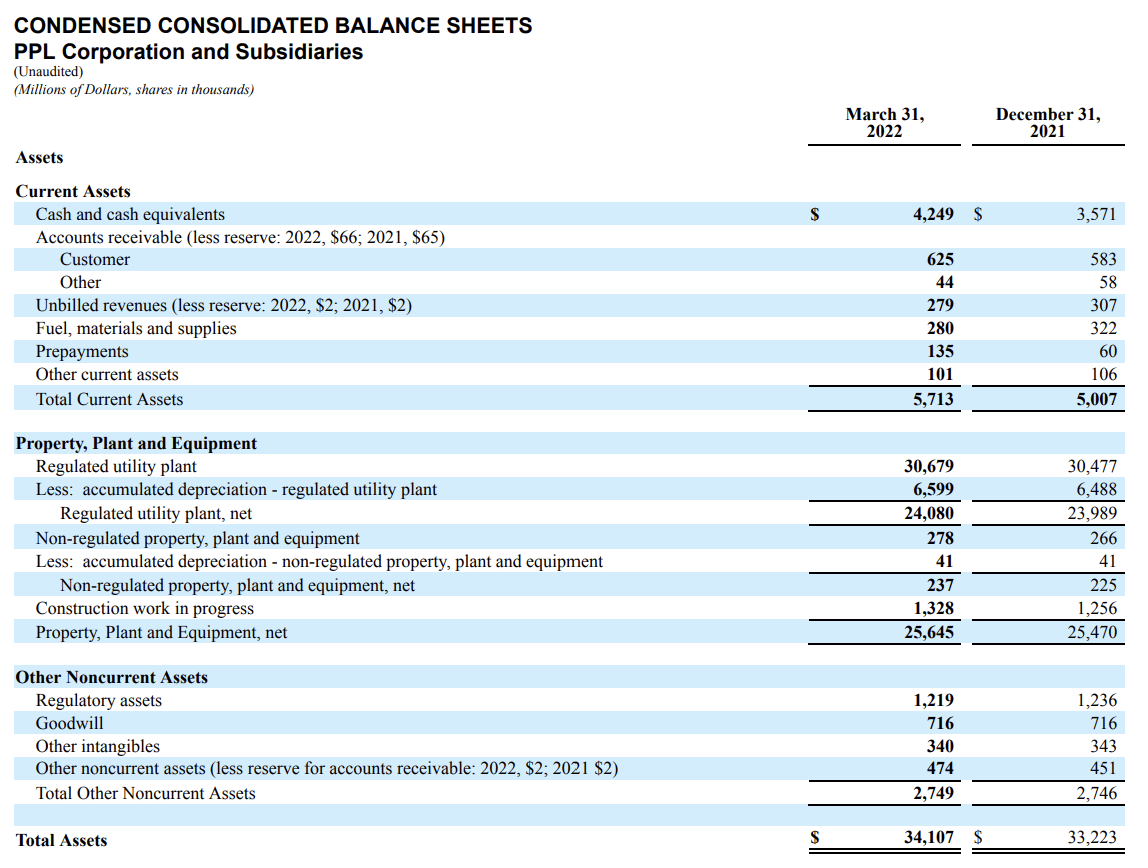

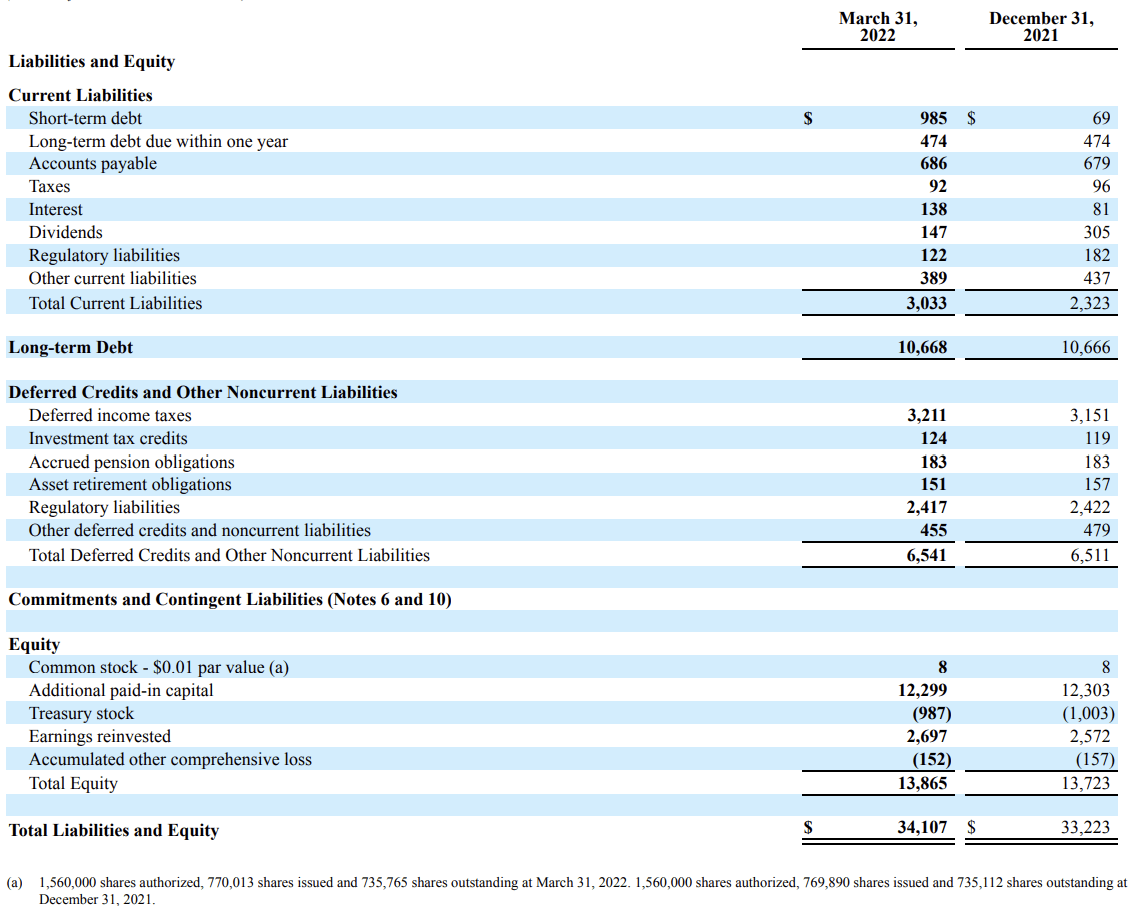

The company has a huge debt of $10.6 billion. This is quite high as compared to the cash and cash equivalent of the company. The debt to cash ratio of the company is 2.52x, which is very concerning. However, I think with the current revenue flow, the company can easily manage the timely payments of the long-term debt.

I estimate the full-year EPS to be in the range of $1.55 to $1.95, which is significantly higher than the last year, as the effects of the integration of Narragansett Electric will be reflected in the coming quarters.

Risk Factor

Rising Interest Rates: The company is in a capital-intensive business, and hence it needs to borrow long-term loans to meet the capital expenditure needs. Currently, we know the interest rates are continuously increasing, which can result in an increased cost of capital. The rising fixed financial cost can affect the net earnings adversely. The rising interest rate can decrease the availability of credit which can disrupt the operation of the company.

Valuation

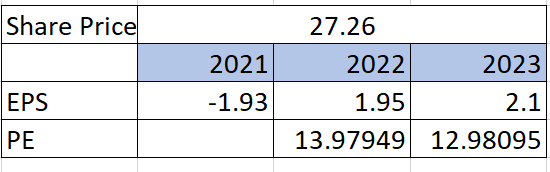

PE Model by Author

Currently, the company is trading at a share price of $27.26. The company is currently trading at a P/E multiple of 18.8x. I believe the company, with the successful integration of Narragansett Electric, will show a significant jump in the earnings of FY22. I estimate the leading EPS to be $1.95, which gives the leading P/E of 13.9x, which I think indicates the stock is undervalued. I think the company will trade at a multiple of 20x with the estimated EPS of $1.95, which gives us a target price of $39. The target price represents that the stock is trading below its intrinsic value and has a potential upside of 43%.

Conclusion

PPL has a well-defined strategy to become a U.S.-focused energy company, and it is taking active steps to achieve that goal. The latest acquisition reflects the company’s expansion plan, and I believe it will be the primary driver of company’s growth in the near future. I think the company is undervalued at current price levels given its growth plans, positive quarterly results and strong future outlook. After analyzing all these factors, I assign a buy rating for PPL.

Be the first to comment