andresr

Investment Thesis

Powell Industries (NASDAQ:POWL) develops and sells electrical equipment. They posted excellent annual and quarterly results. In this report, I will analyze their financial results. POWL has recovered well from the Covid pandemic and received record new orders since FY20. Their revenues and net income are growing rapidly. I believe they will continue to do better financially, and it is the right time to buy POWL.

About POWL

POWL develops and manufactures custom-engineered solutions to control and monitor electrical energy. They provide products like custom-engineered modules, medium voltage circuit breakers, motor control centers, electrical houses, and control gears. The products are used in oil and gas refining, petrochemical, mining and metals, electric utility, and light rail traction. They operate in the U.S., Canada, Europe, Mexico, and the Middle East. The company was founded in 1947 and is headquartered in Houston, Texas.

Financial Analysis

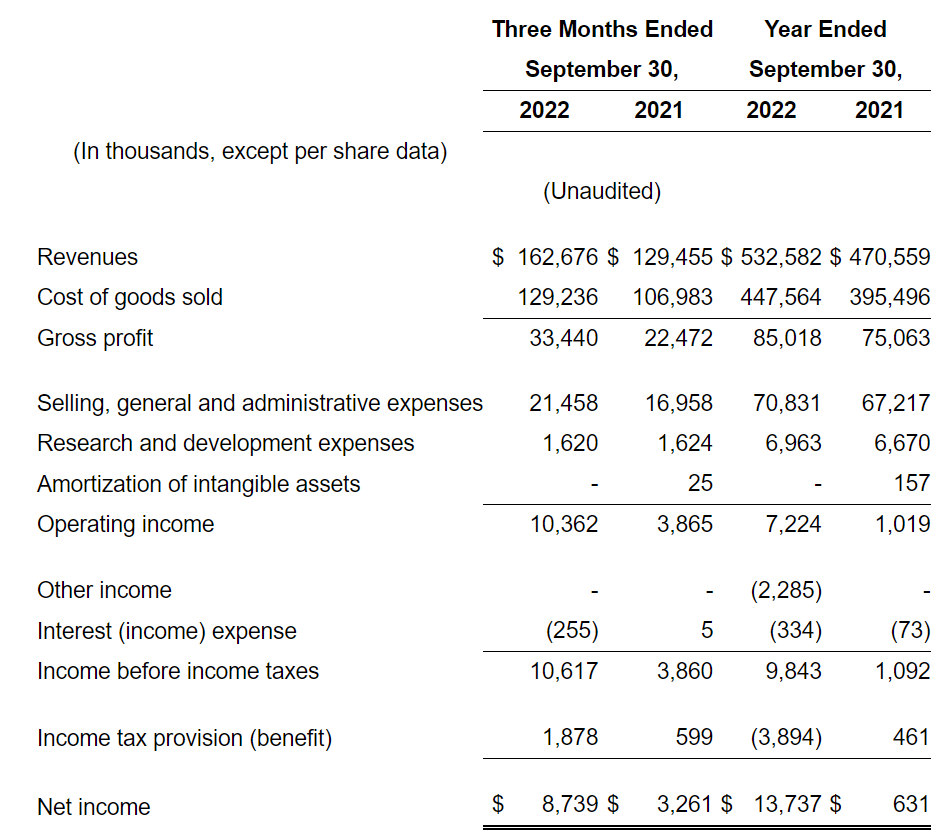

POWL recently posted solid Q4 FY22 and FY22 results. They beat the market EPS estimate by 202.7% and the market revenue estimate by 15.3%. The reported revenue for FY22 was $532.5 million, an increase of 13.1% compared to the revenue of FY21. I believe the primary reason behind this increase was the improvement in the oil and petrochemical market, and they booked a large order to support the production of liquefied natural gas. The reported net income for FY22 was $13.7 million compared to a net income of $0.6 million in FY21. I believe the increased income in FY22 resulted from new orders they received in FY22 worth $719 million. The reported diluted EPS for FY22 was $1.15 compared to the FY21 diluted EPS of $0.05.

POWL’s Investor Relations

Their Q4 FY22 results were also quite impressive. The reported revenue for Q4 FY22 was $162.6 million, an increase of 25.6% compared to Q4 FY21. I think the primary reason behind this rise was an increase in the new orders received in the gas segment. They received new orders worth $259 million in Q4 FY22 compared to the $129.5 million worth of orders received in Q4 FY21. The net income for Q4 FY22 was $8.7 million, a significant increase of 168% compared to Q4 FY21. I believe the main reason behind the increase was strong project execution and recovery of municipal projects. The reported diluted EPS for Q4 FY22 was $0.73, an increase of 160.7% compared to Q4 FY21. In my opinion, the financial performance of POWL in FY22 was quite impressive. They have recovered well from the pandemic, and I think they will continue to do better in upcoming quarters.

Technical Analysis

Trading View

POWL is trading at a price of $35.63. As we can see, the stock has been facing major resistance from the trend line since May 2021. It tried five times to break it, but it failed; recently, it gave a big breakout from the trend line, and after giving a breakout, it is now consolidating. Generally, when a stock gives a breakout, it comes for a retest, and after the retest is done, a breakout stock gives a huge target. In my view, one should wait for the stock to retest the trend line, and if the stock forms a bullish candle near the trend line, one can enter the stock with an upside target of up to 40%.

Should One Invest In POWL?

The company reported its highest revenue since 2017. The management has provided revenue guidance for FY23; they expect FY23 revenues to be around $573.1 million, which is 7.6% higher than the FY22 revenue. I believe they will achieve the revenue target as they continuously receive new orders and are experiencing growth in the commercial and light industrial markets. The Chief financial officer of POWL Michael Metcalf, commented,

we are very encouraged by the commercial activity that we’re experiencing across our core end markets. Considering this, and in addition to our current order book at $592 million, we anticipate revenue growth in most of our key market sectors versus the prior year. Additionally, as a result of the pricing and cost actions that were implemented throughout this past fiscal year, we expect continued improvement in project quality resulting in increased profitability in fiscal 2023. Based upon these dynamics, and accounting for the typical seasonality that we experience during the first fiscal quarter, we anticipate earnings in fiscal 2023 to significantly improve versus fiscal 2022, excluding the non-recurring items.”

A Price / Sales ratio below one is considered good for a company, and POWL has a Price / Sales ratio of 0.73x compared to the sector ratio of 1.25x. It shows that they are undervalued and have great growth potential. In addition, they have $116.5 million in cash with a minimal debt of $2.3 million, which is a great sign for investors.

Seeking Alpha

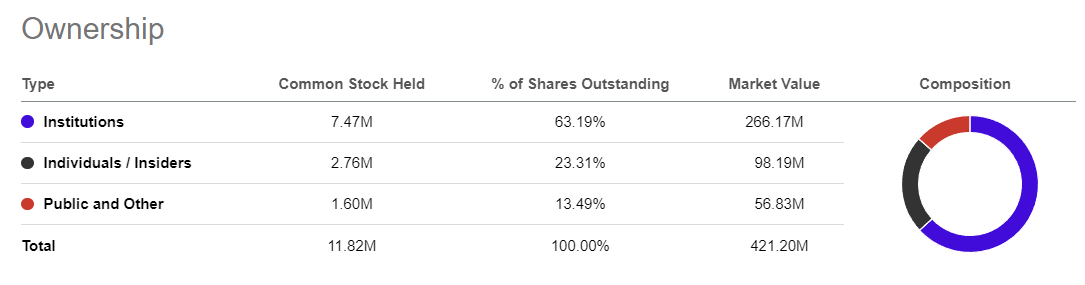

The shareholding pattern of POWL looks decent. Generally, it is considered safe when institutions own more than 60% of the stake in a company in my opinion. In the case of POWL, institutions own 63.1% of the stake in the company, which is a positive sign, which could be why we see less volatility in price fluctuations.

Risk

Powell generates a significant portion of their revenue through various small non-recurring customers. In FY22, only 15% of their revenues came from a large industrial project awarded to them in FY20. The rest came from various small projects, creating uncertainty because it becomes difficult to win customers in this highly competitive market. If they fail to attract customers, then it could severely impact their balance sheet. I think every company should have some big recurring loyal customers that contribute to a company’s business.

Bottom Line

The company has delivered strong annual and quarterly results and is constantly performing well financially in the last four financial years. Technically, the stock has given us a solid breakout, and Powell is looking fundamentally strong. The management also appears optimistic about the company’s growth potential. So after analyzing all the parameters and risk factors, I believe POWL is a great investment opportunity right now, and I assign a buy rating on POWL.

Be the first to comment