Srinuan Hirunwat/iStock via Getty Images

Investment Thesis

I recently made the case to DVR members that CF Industries (NYSE:CF) is very well positioned for high nitrogen prices.

Here’s the context, with natural gas prices in Europe sky-high there’s simply no way for European fertilizer producers to compete against US-based manufactured fertilizer. Even if at the start of 2022 investors came to realize that, capital flows have still pulled back and have migrated away.

This has left CF priced at 5x this year’s free cash flows. I lay out different scenarios to help readers think through some of the positive and negative considerations affecting this investment.

Ultimately, I’m confident you’ll agree, that this is a particularly interesting and exciting investment opportunity.

Putting Recent Insider Sales in Context

There was a big deal made on Seeking Alpha that insiders sold $18 million worth of stock. However, keep in mind that the biggest sale, $11 million worth of stock, was made by CEO Tony Will.

And despite CEO Will selling such a chunk of his holding, he still has $32 million worth of CF stock.

Indeed, if the CEO and others didn’t sell his stock their stock from time to time, how else would they diversify their holding? Having $32 million worth of equity in a company is plenty of skin in the game. Particularly given that management will get further stock-based compensation over time.

I personally don’t see these equity sales in a negative light.

Why CF Industries? Why Now?

CF Industries produces nitrogen fertilizer products.

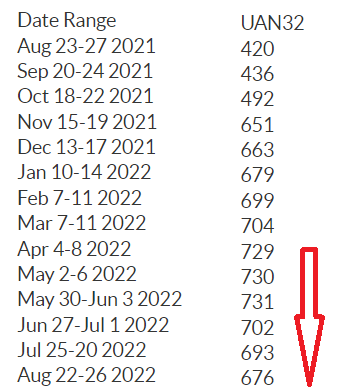

DTNPF.com

As you can see above, nitrogen prices, those of concentrated ammonium nitrate solution (”UAN”) have come down in the past few months.

The reason for this is that nitrogen prices are so high relative to last year that many farmers are now working very hard to put off buying more until next year.

But the reason why I’m bullish on CF is that I recognize that with energy prices so high in Europe, there’s simply no way for European peers to profitably produce fertilizer.

However, the demand for fertilizer hasn’t gone away. It’s simply that it’s much cheaper for farmers to get the fertilizer from the US and ship it across rather than buy it from local farmers at exorbitant prices.

This leaves North American fertilizer producers with a moat around their fundamentals, as companies elsewhere in the world don’t have access to the very cheap natural gas feedstock that North American producers such as CF Industries have. Even though, it should be noted that CF Industries also has some minor exposure to Europe.

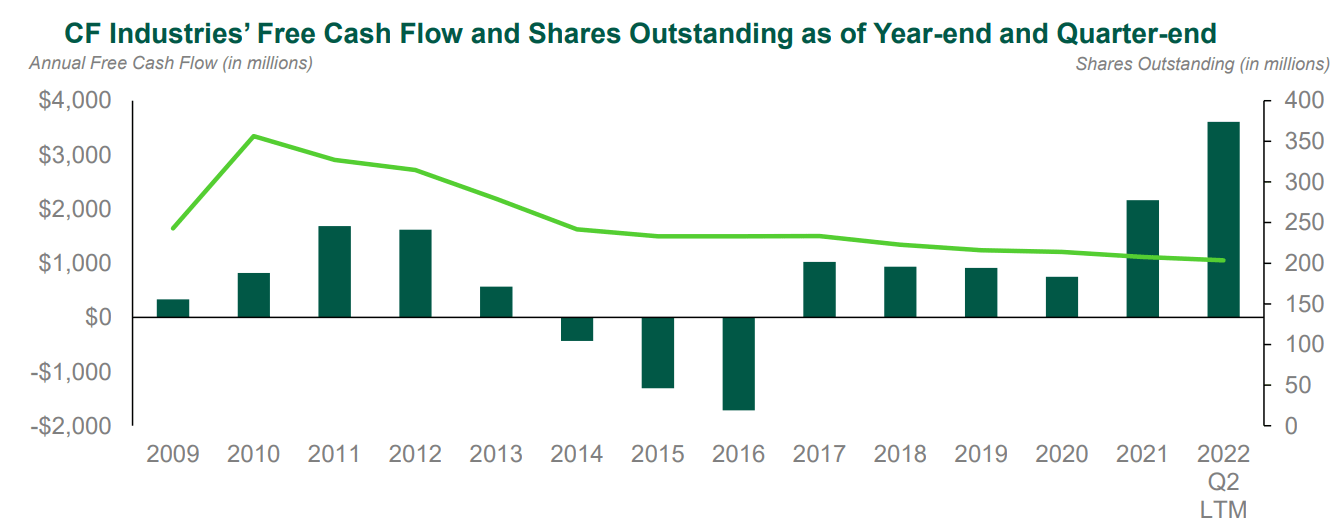

A Picture Worth a Thousand Words

CF Industries Q2 2022 presentation

Altogether, through CF’s strong free cash flow generation, together with consistent buybacks, CF Industries has been consistently reducing the total number of shares outstanding.

The bars show free cash flow increasing significantly in the past two years, while the total number of shares outstanding, the green line, is coming down.

That means more free cash flow per share. Along these lines, CF’s management said during their Q2 2022 earnings call,

Given this outlook, we expect to generate substantial free cash flow for an extended period. This will enable us to return significant capital to shareholders, while we also make disciplined investments to grow our low-carbon ammonia production footprint.

CF Stock Valuation – Approximately 5x FCF

The reason why CF isn’t more expensive is that it’s difficult to get much visibility right now into what price nitrogen will be at in 2023.

Simply put, there’s a lot of uncertainty in the market, and investors hate uncertainty second only to bad news.

That being said, even if in 2023 prices come down around 15% to 20%, that wouldn’t take away from the fact that CF is still very attractively priced.

In fact, if CF Industries’ free cash flow only increases slightly from $3.6 billion over its trailing twelve months, to $4 billion by year-end, this would still leave the stock priced at just 5x this year’s free cash flows.

Now, as noted above, this does not detract from the fact that investors right now have absolutely no visibility into 2023.

That typically wouldn’t be a huge problem. But given that the market is so stretched and volatile investors are probably worried that nitrogen prices could seriously sell-off.

However, even if I simply don’t see that as a likely scenario, I should still give myself a margin of safety for unlikely events.

The way I get comfortable with this is this. If I assume that nitrogen prices were to come down by approximately 30%, that would have an impact of as much as 50% on the free cash flow line. This is assuming that CF isn’t able to mitigate the lower costs, given its high fixed cost structure.

That would still allow CF to print around $2 to $2.2 billion of free cash flow in 2022. That would still leave the stock priced at less than 10x its 2023 free cash flow.

The Bottom Line

Like any investment, there are many moving parts and no guarantees here.

Presently, nitrogen prices are proving to be quite sticky. And even though I believe that many farmers will do everything they can to extend their fertilizer inventory, my thesis is contingent on the fact that farmers in North America and Europe simply can’t do without fertilizer to adequately grow crops.

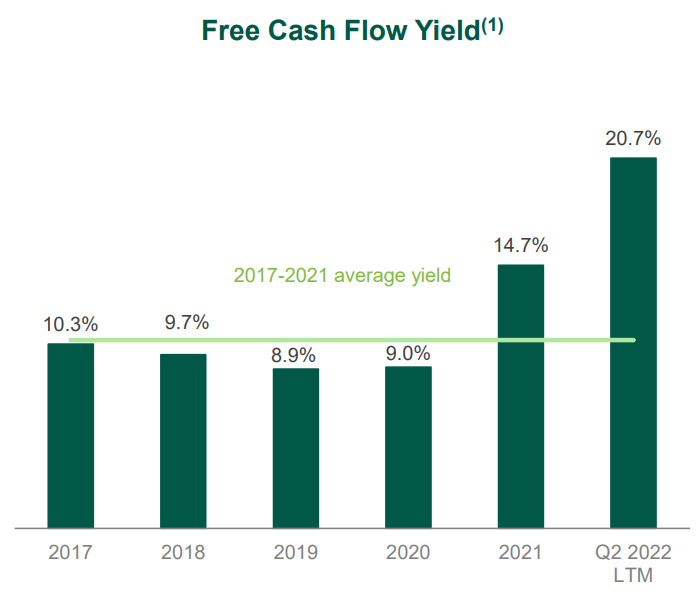

CF Q2 2022 presentation

What’s more, I contend that even if nitrogen prices were to sell off in 2023, CF Industries would still be priced at approximately 10x free cash flow. Offering investors a 10% yield on their holding.

In that event, if CF’s free cash flow did get cut in half, CF’s shares would simply revert back to the long-term average. This perspective will go some way to add support to the investment case.

Finally, I’ll conclude with one final comment from management,

And you’re looking at a situation with $60 at TTF (European natural gas prices) plus as Bert said, it’s $2,000 ammonia (the cost to produce ammonia) that’s not where the market is trading right now ($2000 is a lot higher than the price of ammounia, that’s less than $700).

So, in our view this is actually pretty constructive about the go forward. It means that the amount of production in those high-cost regions [Europe and Asia] is going to be somewhat limited.

The challenge there, of course, is it means the world is going to be incredibly tight availability of product as we get into both the winter and then into the spring next year, particularly if the situation in Europe is not resolved in the coming months because that just further pressures the whole system with winter coming.

The paragraphs above succinctly describe the thesis. There are high energy costs facing CF’s peers in Europe and Asia, that’s leading to a constructive market for CF, and a very tight nitrogen supply market headed into next spring.

Be the first to comment