Mario Villafuerte

Pilgrim’s Pride Corporation (NASDAQ:PPC) had a solid third quarter of 2022 when considering the headwinds it faced in Mexico and Europe as inflation pressures changed the consumption habits of many consumers in the protein market.

In regard to the effect of inflation on consumer consumption of protein, they have been transitioning from lamb and beef to chicken and pork, of which both of the latter PPC offers to consumers.

As for potential worsening economic conditions in the markets PPC competes in, its strong and diversified portfolio in its chicken business provides not only growth potential during difficult times, but also support on the downside.

Since the company offers a variety of chicken products at different price points, it can perform well in good times and bad times, although it of course will not do as well when the market turns down. That said, its earnings were a blow out in the third quarter, and if it can maintain sales at a decent level, I think it is positioned to outperform the sector into 2023 and beyond.

In this article we’ll look at some of the latest numbers, the strength of its business model, and why it’s a top pick in the protein sector.

Latest numbers

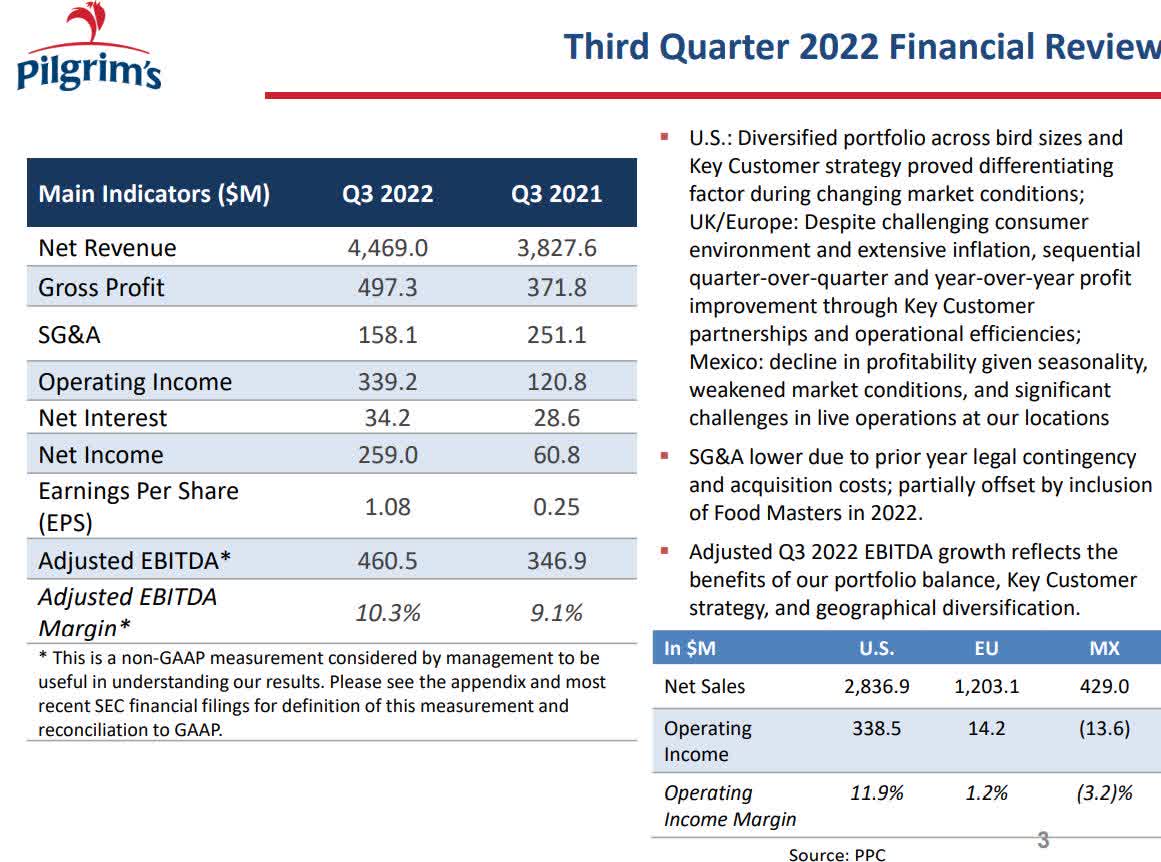

Revenue in the third quarter of 2022 was $4.47 billion compared to $3.83 billion in the third quarter of 2021.

Management stated that market pricing had fallen from the all-time highs reached in May 2022 but were still above historical averages for most of the reporting period.

Adjusted EBITDA in the quarter was $406.5 million, up approximately $114 million from adjusted EBITDA of $346.9 million in the same reporting period of 2021.

Adjusted EBITDA margins in the third quarter were 14.7 percent compared to 10.7 percent year-over-year.

Investor Presentation

Net income in the reporting period was $258 million or $1.08 per share.

Europe and Mexico weighed on the performance of the company in the third quarter, with adjusted EBITDA margins in Europe at 4 percent. It was improvement over the 3 percent in adjusted EBITDA margins from the third quarter of 2021. Europe has been improving by finding ways to lower operational costs and offset input inflation.

Mexico vastly underperformed in the third quarter with adjusted EBITDA of negative $(6.3) million, compared to the $56.3 million in adjusted EBITDA it made in the third quarter of 2021. That was attributed to lower volumes in association with breeder mortality and unfavorable fundamentals in the market.

While disappointing, investors shouldn’t consider this something unusual, as the Mexican market has historically been very volatile on a quarterly basis; its performance tends to level out over time. For example, in the first nine months of 2022 adjusted EBITDA in Mexico was $128.9 million, with 9.3 percent adjusted EBITDA margin during that period.

Even so, a better quarter from Mexico would have made a good quarter a very good one under challenging economic conditions.

Cash and cash equivalents at the end of the third quarter was $654 million, with long-term debt (minus current maturities) of $3.18 billion.

Business model, chicken and the economy

With chicken increasingly becoming the go to meat in the challenging economic conditions, PPC is well positioned to benefit from that growing trend. The reason why is its business model incorporates a diverse portfolio of chicken products at different price points that target different demographics, which provides growth potential and support for the downside.

Not only can it compete at the top end of the chicken market, but it has also entered into partnerships that allow it to compete in the low-priced commodity chicken market as well.

This should allow it to generate modest growth in 2023, and if the economic gets worse to the point the market transitions to a large degree out of higher-price brands, it has the lower end of the chicken market covered too.

If the latter happens it would put some downward pressure on margins and earnings, but it’ll also support the company from falling off the cliff.

But as of the third quarter, management said its brands were seeing strength, specifically with Food Masters. The UK is an exception to that rule, where consumers are seeking out private label chicken options in response to high inflation.

So with the business model of PPC and its ability to compete at different price points with a variety of products, it should be able to ride out weak economic conditions in 2023 if things get worse before they get better.

Another step the company is taking to improve competitiveness and reduce the impact of inflation is to invest more in its largest plants in order to better support its “key customers.”

Share price movement

Compared to other industries, the share price movement of PPC over the last year has been somewhat mild, falling to its 52-week low of $20.23 on March 8, 2022, and reaching a 52-week high of $34.66 on June 3, 2022.

It appears to have found support with a double bottom of approximately $21.00 per share. Since hitting $21.00 per share on October 13, 2022, it has climbed to a top of about $26.20 before falling back to $23.30 as I write.

Unless something unforeseen and extraordinary happens, I think the $21.00 per share mark is the likely bottom for the company, and if it’s able to continue to do well in the chicken market in 2023, it’s likely to generate modest growth during that time, and probably will have a solid foundation to outperform in 2024.

TradingView

But as always with living things, there are always risks associated with it such as avian flu and crop shortages that have an impact on prices and the size of the number of birds the company raises in any one quarter.

Geographic diversity with its plants helps mitigate the risk, but it still could have an impact on the company in the short term.

But with the visibility we have today, I think that $21.00 per share is a good way to model support for PPC’s share price.

Conclusion

Pilgrim’s Pride has come off a good performance in the third quarter under difficult economic conditions. Even though it had a slight revenue miss, it was far above the level it was a year earlier, and EPS blew it out of the water.

Looking ahead, I think a market to watch is the UK to see if it’s a bellwether for the 2023 chicken market. If other markets behave in a similar manner, PPC could be in for a tough year, and the $21.00 per share support level I mentioned above wouldn’t hold.

On the other hand, if its diversified chicken products continue to maintain brand strength in key markets and its private label products make up for customers transitioning to low-cost options, the company will likely surprise to the upside and its share price will respond accordingly.

I don’t see any real big move on either side of the play, but the probable outcome is going to be either for the company to trade rangebound throughout 2023, or for it to maybe test the $30.00 per share mark as a ceiling.

Either way, the fundamentals of PPC look good and whatever happens in the short term it’s prepared to be a top performer in its sector because of its diversified business model.

Be the first to comment