HeliRy

Note:

I have covered Performance Shipping (NASDAQ:PSHG) previously, so investors should view this as an update to my earlier articles on the company.

Earlier this year, small Greece-based tanker operator Performance Shipping joined peer Imperial Petroleum (IMPP, IMPPP) and sister company OceanPal (OP) in diluting common shareholders at a tiny fraction of net asset value for the sole purpose of growing their respective fleets.

Controlling Shareholder Remains Dilution-Protected

Keep in mind that controlling shareholder Aliki Paliou recently opted for converting her common shares into newly issued 4.0% Series B Convertible Cumulative Perpetual Preferred Stock (“the Series B Preferred Stock”) thus protecting her holdings against future dilution in the common equity.

Even better, owners of the Series B Preferred Stock will soon have the option to convert their holdings into newly issued supervoting 5.0% Series C Convertible Cumulative Perpetual Preferred Stock (“the Series C Preferred Stock”):

Each Series B Preferred Share is convertible, at the option of the holder and for additional cash consideration of $7.50 per converted Series B Preferred Share, into two shares of the Company’s Series C Convertible Cumulative Perpetual Preferred Stock (the “Series C Preferred Shares”), par value $0.01 per share and liquidation preference of $25.00 (the “Series B Conversion Right”)

(…)

While our common shares have one vote per share, each Series C Preferred Share shall be entitled to a number of votes equal to the number of Common Shares into which the share is then convertible multiplied by 10. Holders of the Series C Preferred Shares shall be entitled to vote with holders of Common Shares, voting together as a single class (with certain exceptions), with respect to all matters presented to the stockholders.

Even further massive dilution won’t have a major impact on her supervoting rights (emphasis added by author):

Each Series C Preferred Share will be convertible to Common Shares, at the option of the holder at any time and from time to time after 18 months from the date of issuance of such Series C Preferred Share, in whole or in part, at a conversion price equal to $5.50 per Common Share (adjusted for any stock splits, reverse stock splits or stock dividends). The conversion price shall be adjusted to the lowest price of issuance of common stock by the Company for any registered public offering following the original issuance of Series B Preferred Shares, provided that, such adjusted conversion price shall not be less than $0.50.

Should Aliki Paliou and her spouse, CEO Andreas Michalopoulos, elect to convert their preferred shareholdings back into common shares at some point going forward, outstanding common shares would approximately double from current levels.

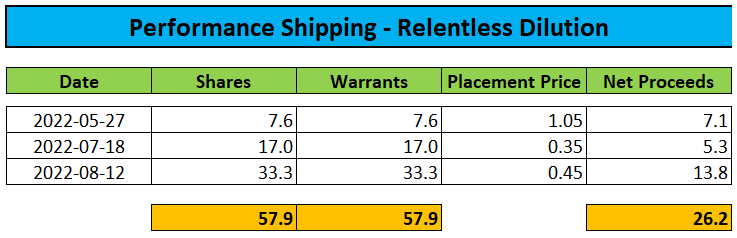

Relentless Dilution Continues for Common Shareholders

Over the past three months, the company has raised approximately $26.2 million in net proceeds from additional equity offerings including warrant sweeteners:

Company SEC-Filings

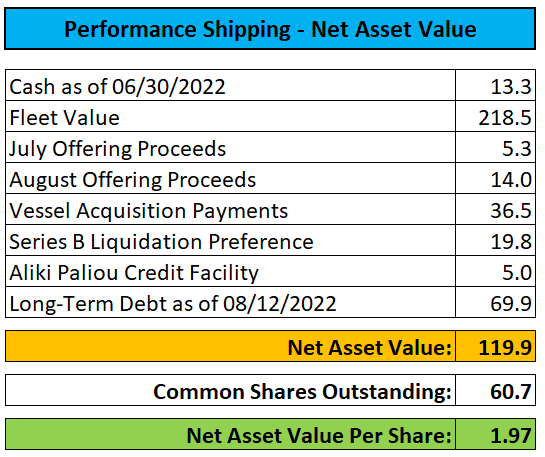

As a result, net asset value (“NAV”) per share has been reduced by 85% from approximately $13.70 at the beginning of the year to below $2 today while outstanding common shares ballooned by more than 1,000%:

Company SEC-Filings / Compass Maritime

Fleet Expansion

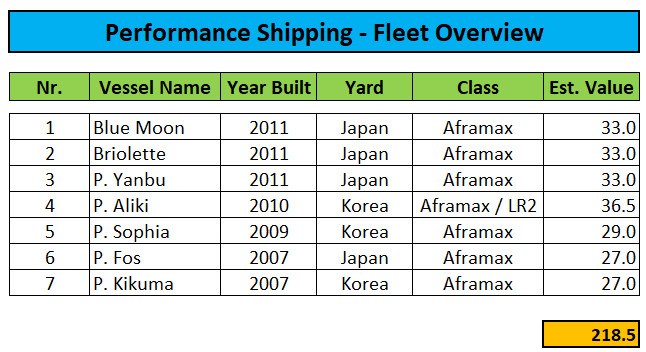

Given management’s stated target of doubling the fleet within the next 12-24 months, Performance Shipping has wasted no time putting the newly raised funds to work.

Last month, the company took delivery of its sixth Aframax tanker and on Wednesday announced the acquisition of its first LR2 product tanker thus increasing its fleet from five to seven vessels:

Company Press Releases / Compass Maritime

Strong Tanker Markets

As evidenced by the company’s recent Q2 results, tanker market fundamentals have improved considerably following the Russian assault on Ukraine and charter rates are likely to remain strong for at least the next couple of quarters.

Discounted Valuation For Good Reason

Under normal circumstances, a profitable tanker operator trading at a 85% discount to NAV per share would make for a screaming buy but given the very high likelihood of further, dilutive equity offerings, investors shouldn’t touch the common shares with a ten foot pole, particularly given the likely requirement to conduct another reverse stock split by January 9, 2023 at the latest point to regain compliance with the Nasdaq’s $1 minimum bid price requirement.

Bottom Line

Like a number of other Greek shippers, Performance Shipping continues to grow the company at the expense of common shareholders.

Given management’s stated target of expanding the fleet even further, additional dilution is likely to occur sooner rather than later.

Similar to peer Imperial Petroleum, Performance Shipping’s common stock might still provide some decent trading opportunities going forward, but it remains imperative for long-term investors to avoid the shares for the time being.

Be the first to comment