bunhill

Teladoc Health, Inc. (NYSE:TDOC) investors recently received a boost from management. It communicated a solid Q4 preliminary earnings release that will likely come in at the higher end of its guidance range.

Accordingly, the company expects $636.5M (midpoint) in Q4 revenue while keeping its adjusted EBITDA guidance unchanged. Its full-year revenue outlook also includes a $1B contribution from its consumer-focused BetterHelp, “a company that provides therapy remotely and promises ‘a personalized therapist match’ that is tailored to your preferences and needs.”

Investors still holding the bag after a massive post-pandemic battering are likely hoping that the company’s positive commentary could mark its ultimate bottom.

We assessed there are reasons for optimism for Teladoc to stage a recovery from here. TDOC indeed rode the pandemic surge, which ultimately proved unsustainable after the economy reopened.

As such, the normalization in its valuation has likely stunned investors who bought at its 2020/21 highs. But the crash back to earth is justified, as Teladoc can no longer claim its high-growth cadence, as its revenue is expected to increase by only 18.3% in FY22, in line with the company’s revised outlook.

As such, it marks a significant decline from FY20’s 98% and FY21’s 86% surge. In a way, savvy market operators were astute in their assessment that Teladoc couldn’t sustain its growth momentum as it formed its top in early 2021.

Then, why should investors still consider telehealth, which remains a fragmented field, as a viable investment opportunity? Management highlighted that it has continued to gain momentum in H2, as demonstrated in its ability to promulgate a solid FY22 outlook.

Nevertheless, questions remain about whether its FY23 guidance could clear the analysts’ bar. However, we assessed that Wall Street analysts have likely penciled in prudent projections, as they expect Teladoc to post FY23 growth of 13.1%.

Teladoc’s whole-person care value proposition should see it gain market share against smaller companies as the funding environment has proved challenging. As such, the company’s free cash flow (FCF) profitability should help steer it forward even as macroeconomic conditions would continue to worsen.

Moreover, the Fed’s rate hikes cadence should moderate moving ahead, even though it’s expected to stay high. While we don’t expect TDOC to recover its pandemic highs anytime soon, we believe the rate hikes headwinds should normalize for TDOC. Hence, it should help alleviate some of the downside volatility it experienced over the past year.

Furthermore, continued investments by CVS Health (CVS) and Amazon (AMZN) in the healthcare space are a boon and a bane. While it introduces more intense rivalry as they compete to define their leadership in value-based care, it also highlights the immense opportunity available in the space.

Hence, we believe Teladoc’s leadership through its telehealth roots puts it in a solid position to further integrate virtual medicine with the “physical delivery system“, despite facing stiffer competition.

Despite that, investors are urged to watch the developments in BetterHelp, as the WSJ ran an exclusive recently highlighting consumer dissatisfaction with the company’s business model.

WSJ’s article questioned the quality of the therapists matched by BetterHelp, and whether using contractors instead of employees could have also impacted the quality of delivery. Given the importance of BetterHelp as one of the company’s most promising growth drivers, investors should continue to pay attention to these developments.

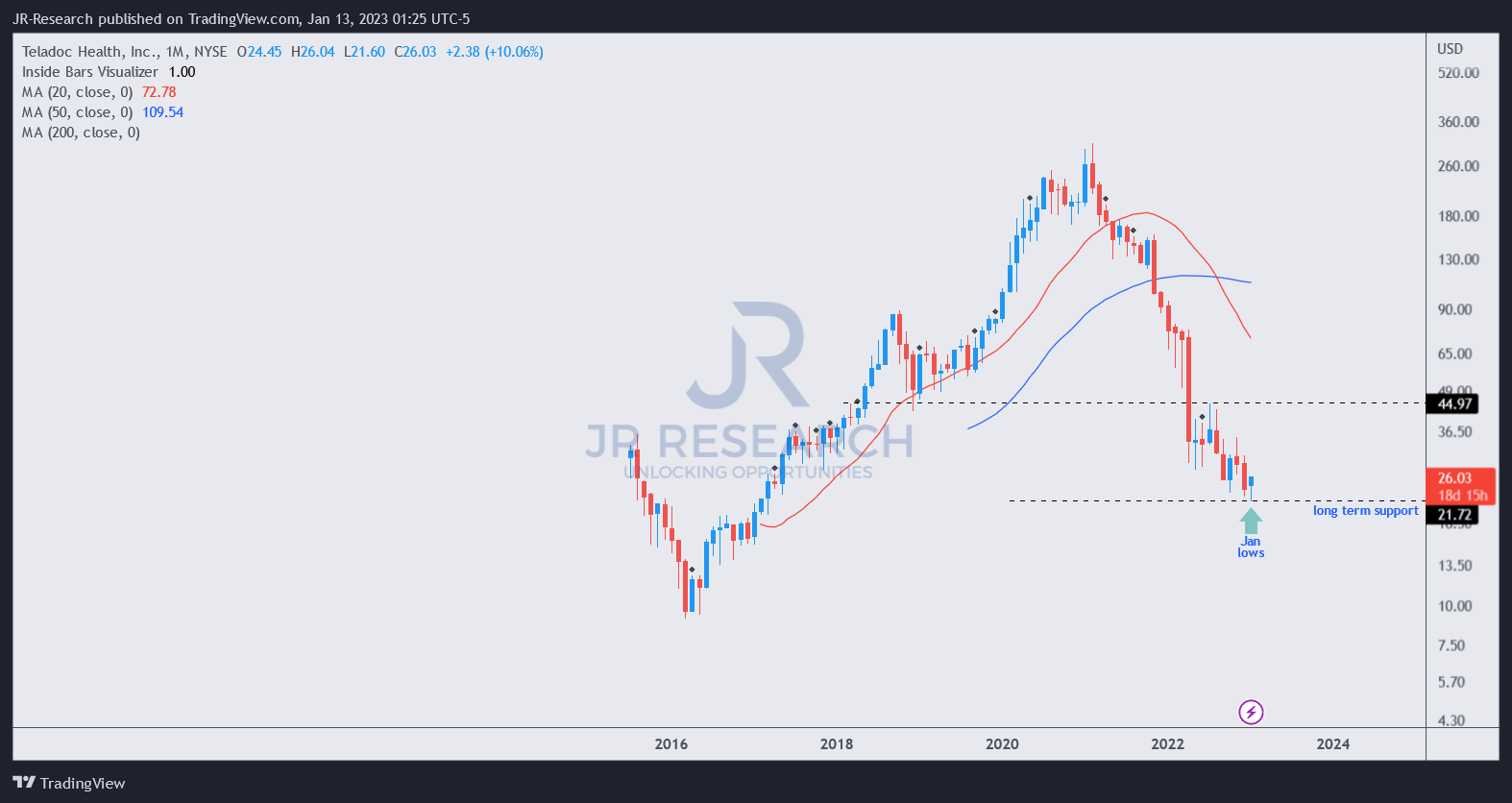

TDOC price chart (monthly) (TradingView)

With TDOC more than 90% below its 2021 highs, could its recent lows finally mark the bottom in TDOC?

We had expected TDOC to bottom earlier, but the thesis didn’t pan out. TDOC last traded at an NTM EBITDA multiple of 16.8x, which is still a premium against its peers’ median of 8.4x (according to S&P Cap IQ data). Hence, the “leadership premium” has likely been baked into its valuation as the industry got de-rated.

Despite that, Teladoc’s better H2 execution indicates that the company’s ability to improve its performance in a more challenging macro backdrop should be viewed constructively. Hence, a speculative opportunity with a price target in the $40+ level is still possible.

Rating: Speculative Buy (Reiterated).

Note: As with our cautious/speculative ratings, investors must consider appropriate risk management strategies, including pre-defined stop-loss/profit-taking targets, within an appropriate risk exposure.

Be the first to comment