Pgiam/iStock via Getty Images

Almost a year ago, I reiterated my bullish thesis on Parker-Hannifin based on its reliable growth trajectory, its impressive business momentum and its cheap valuation. Since my article, the stock has outperformed the broad market by a wide margin, as it has declined only 10% whereas the S&P 500 has shed 20%. Even better, despite the global economic slowdown, the industrial manufacturer has maintained its strong business performance. Given also its promising acquisition of Meggitt and its cheap valuation, Parker-Hannifin remains highly attractive.

Business overview

Parker-Hannifin (NYSE:PH) is an industrial manufacturer that is focused on motion and control technologies. It has a history of more than a century, it has operations in 45 countries and has grown to a large-cap stock, with a market capitalization of $38 billion.

Most industrial manufacturers are cyclical companies that are vulnerable to recessions. Whenever a recession shows up, commercial production tends to decrease and thus these companies incur a steep decrease in the demand for their products. Parker-Hannifin is a bright exception to this rule. Its products are complicated but critical for the operations of the customers of the company. As a result, the demand for these products remains strong even during rough economic periods.

The resilience of Parker-Hannifin has been evident throughout the coronavirus crisis. Despite the severe recession caused by the pandemic in 2020, the company incurred just a 9% decrease in its earnings per share in that year. Given the severity of that downturn, the performance of the industrial manufacturer is certainly impressive.

Parker-Hannifin is currently facing strong business headwinds due to the surge of inflation to a 40-year high, which has greatly increased the operating costs of most companies. In addition, central banks have raised interest rates aggressively in order to restore inflation to their target range and thus they have caused the global economy to slow down. As if these headwinds were not enough, the dollar has remarkably strengthened this year, thus exerting pressure on the revenues and earnings of multinational companies, such as Parker-Hannifin.

Despite all these headwinds, Parker-Hannifin has maintained its positive momentum this year. In the first quarter of fiscal 2023, the company enjoyed strong demand for its products in every operating region and thus it grew its revenues 12% over last year’s quarter. It also offset high cost inflation with material price hikes and thus it grew its earnings per share 11%, from $4.26 to $4.74, thus exceeding the analysts’ estimates by an impressive $0.57.

Parker-Hannifin has beaten the analysts’ earnings-per-share estimates for 29 consecutive quarters. This is certainly an exceptional achievement, which is a testament to the strength of the business model of the company and the quality of its management.

Even better, thanks to its sustained business momentum, the company recently raised its guidance for its full-year earnings per share, from $18.10-$18.90 to $18.60-$19.30. It is also worth noting that management has always tried to be conservative in its guidance. As a result, it has raised its guidance several times in recent years. This helps explain why analysts expect Parker-Hannifin to achieve earnings per share of $19.15 in fiscal 2023, close to the upper limit of the guidance of management. If the company meets the consensus, it will grow its earnings per share 2%, to a new all-time high, in a year characterized by exceptionally adverse business conditions.

Growth

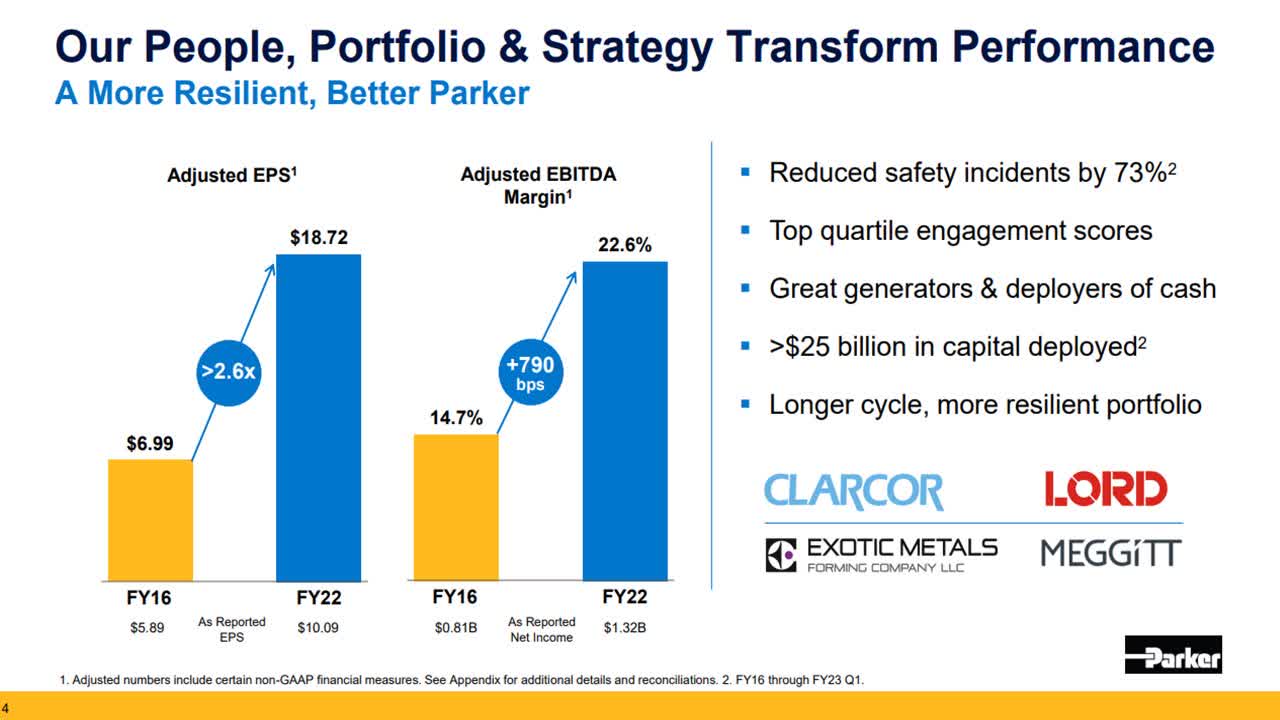

Parker-Hannifin has exhibited an impressive performance record. During the last six years, it has enhanced its EBITDA margin from 14.7% to 22.6% and has grown its earnings per share by more than 2.6 times.

Parker-Hannifin Growth (Investor Presentation)

The company has exhibited such an admirable growth record thanks to its proven ability to acquire other industrial manufacturers and achieve great synergies.

Even better, Parker-Hannifin has ample room for future growth. It currently has a market share of 13% and aims to grow it to approximately 20%. Given the quality of its management and its record of successful integration of acquired companies, it is reasonable to expect the company to achieve its goal.

It is also important to note that Parker-Hannifin acquired Meggitt for $8.8 billion in cash three months ago. Meggitt, which is a global leader in aerospace and defense motion and control technologies, sells technology and products on every major aircraft platform and has annual sales of $2.3 billion. It is thus a great fit to the business of Parker-Hannifin. As the transaction value is 23% of the market capitalization of Parker-Hannifin and the revenues of Meggitt are 15% of the revenues of Parker-Hannifin, the acquisition is likely to become a major growth driver for Parker-Hannifin in the upcoming years.

Analysts seem to agree on the promising growth prospects of Parker-Hannifin. They expect the company to grow its earnings per share by 8%-11% per year over the next three years, from $19.15 in 2023 to $24.87 in 2026.

Valuation

Since I first recommended purchasing Parker-Hannifin, about four years ago, the stock has rallied 76%. Despite its rally, the stock remains attractively valued. It is currently trading at a forward price-to-earnings ratio of 15.2, which is lower than the 8-year average earnings multiple of 15.7 of the stock.

Moreover, this valuation level is markedly cheap for a company with such a reliable growth trajectory. If the company meets the aforementioned analysts’ estimates in the upcoming years, it will almost certainly prove its current valuation too cheap. To provide a perspective, the stock is currently trading at only 11.7 times its expected earnings in fiscal 2026.

The cheap valuation of Parker-Hannifin has resulted primarily from the impact of inflation on the valuation of growth stocks, as high inflation greatly reduces the present value of future cash flows. However, the Fed has clearly prioritized restoring inflation to 2%. Thanks to its aggressive interest rate hikes, the central bank will almost certainly achieve its goal sooner or later. Whenever inflation subsides, the market will probably reward Parker-Hannifin with a higher price-to-earnings ratio.

Dividend

Parker-Hannifin has paid a dividend for 72 consecutive years and has raised its dividend for 66 consecutive years. It is thus a Dividend King. There are only 48 stocks that have achieved such long dividend growth records. The accomplishment of Parker-Hannifin is undoubtedly admirable, especially given the cyclical nature of the industrial sector.

Parker-Hannifin is currently offering a dividend yield of only 1.8%. However, investors should not dismiss the stock for its modest dividend yield. The company has grown its dividend by 12.0% per year on average over the last decade and by 13.7% per year on average over the last five years. Notably, the company raised its dividend by 29% this year. Given the aforementioned major acquisition of Meggitt, the 29% dividend raise is impressive, as most companies would have preserved cash to fund the major acquisition.

Moreover, Parker-Hannifin has a payout ratio of only 26%. Thanks to its healthy payout ratio and its reliable growth trajectory, the company can easily continue raising its dividend at a fast pace for many more years. Therefore, the stock is suitable, not only for growth-oriented investors, but also for income-oriented investors with a long-term investing horizon.

Final thoughts

The ongoing bear market is offering an ideal opportunity to purchase stocks with solid business fundamentals at bargain prices. This rule certainly applies to Parker-Hannifin. Thanks to its reliable growth trajectory, its resilience to downturns and its cheap valuation, the stock is likely to highly reward patient investors, who can maintain a long-term perspective in the ongoing bear market.

Be the first to comment