photobyphm

Verizon Buy Thesis

Verizon Communications Inc. (NYSE:VZ) is currently showing tremendous relative strength today as the market is getting hammered at the time of this writing. I believe this is a strong signal that the stock has bottomed and presents an outstanding buying opportunity for those looking for a substantial dividend yield with little chance of downside in the stock price. In the following sections, I will lay out my bull case for Verizon Communications stock.

Showing significant relative strength today

Verizon Communications stock has barely budged while the market is selling off hard. This is a strong indicator that the stock has bottomed and there is little to no downside left.

CNBC

Consolidating above major support

In fact, this has been the case for the past quarter. Verizon stock has been consolidating just above major support for the past three months. This is a very positive development.

Finviz

Down 30% while S&P 500 is flat

The stock has fallen to decade lows presently after reporting approximately 200,000 in subscriber losses back in July. This was attributed to Verizon not budging on the pricing, while AT&T (T) was running several specials. AT&T actually increased subscribers by 800.000 during the same time frame. Yet, Verizon reported improvements in the last earnings release.

Seeking Alpha

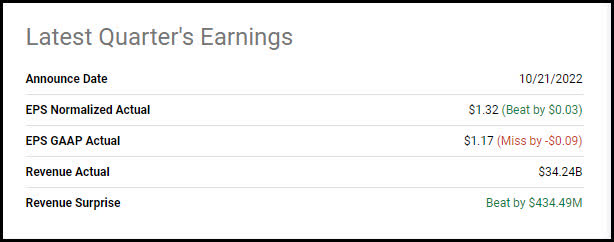

Verizon beat on top and bottom lines

The company beat on the top and bottom lines last quarter. Yet, it still had further to fall, as the macro outlook for markets in general is poor due to the Fed continuing to raise rates. CEO Hans Vestberg actually sounded quite positive on the latest conference call.

Seeking Alpha

CEO Conference call statement

CEO Hans Vestberg had a positive outlook on latest conference call and reaffirmed 2022 guidance.

Verizon Communications Chairman and Chief Executive Officer Hans Vestberg stated on the conference call:

“We ended the third quarter with wireless service revenue growth up 10% year-over-year and 2% sequentially and adjusted EBITDA grew sequentially by almost 3% to $12.2 billion. We had total phone gross adds of nearly 2.6 million and about 5% year-over-year increase. This includes an increase in consumer of 1.3%, a significant improvement from minus 11% in the second quarter.

These results are early indicators that the actions we are taking across our businesses to build momentum are gaining traction. Of course, we are not done yet. I continue to work with my team to take actions to grow revenue and to take cost out of our business to unlock the full potential of Verizon. I am glad to see sequential improvements based on our efforts, but there is more to do. Based on our momentum and plans, our financial guidance for 2022 remains unchanged.”

Several improvements were noted

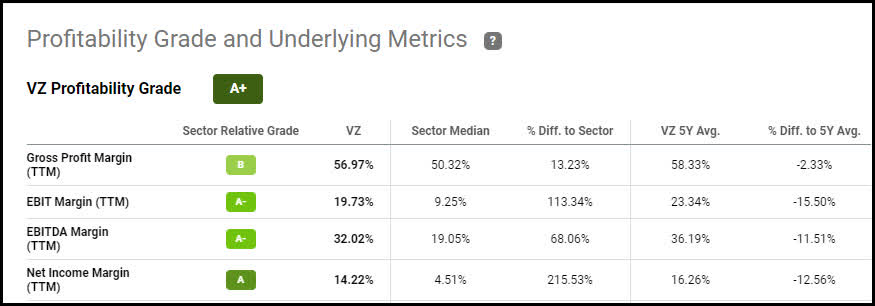

The company highlighted several improvements and areas of progress that were made over the last quarter in the financial, operational, and network categories. This led to profit margins improving, yet still below the five year averages.

Verizon

Seeking Alpha Profitability Metrics score A+

Verizon is highly profitable across the board. The trailing two month profit margins are very healthy when compared to the competition, yet are still lagging the five year averages for the company. Even so, these levels provide plenty of cover to pay the dividend and planned capital expenditures.

Seeking Alpha

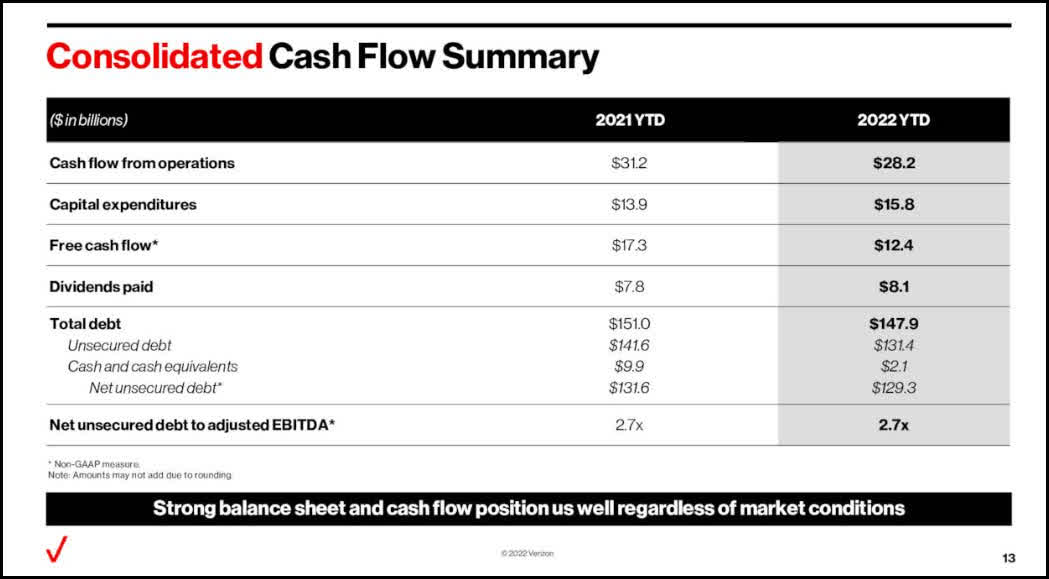

Cash Flow down year-over-year, yet adequate

Cash flow from operations is down slightly year-over-year, from $31 billion to $28 billion. Free cash flow (“FCF”) has dropped from $17 billion last year to $12.4 billion this year, yet is still more than adequate to cover the dividend payout of $8 billion and continue to pay down the debt. The balance sheet has remained strong through thick and thin times. The company has reaffirmed 2022 year-end guidance, in fact.

Verizon

Reaffirmed 2022 guidance

The company reaffirmed 2022 guidance on the last quarter’s earnings conference call. I believe this is one of the main reasons Verizon stock has stopped dropping. It’s always good to hear management has faith in their projections. With the market acting the way it has lately, it would be easy for management to take a “mulligan” and lower guidance. Now, let’s get to the meat of the article, the healthy dividend payout for income investors.

Verizon

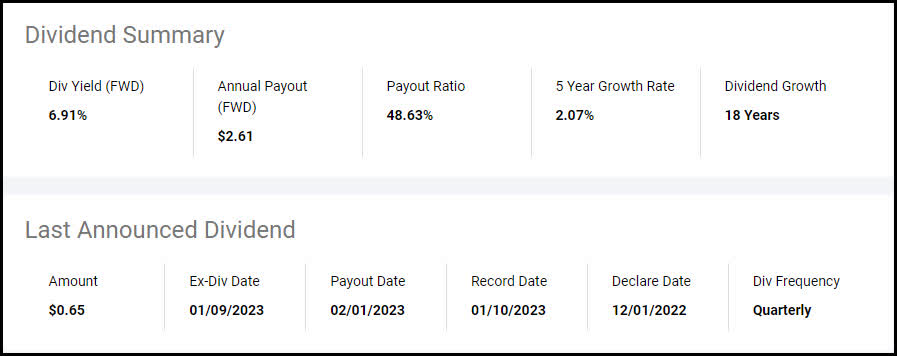

Verizon’s solid, well-covered dividend

The major reason to buy Verizon stock here is to lock in a solid, safe, well-covered dividend payment. Please review Seeking Alpha’s dividend summary below.

Seeking Alpha dividend summary

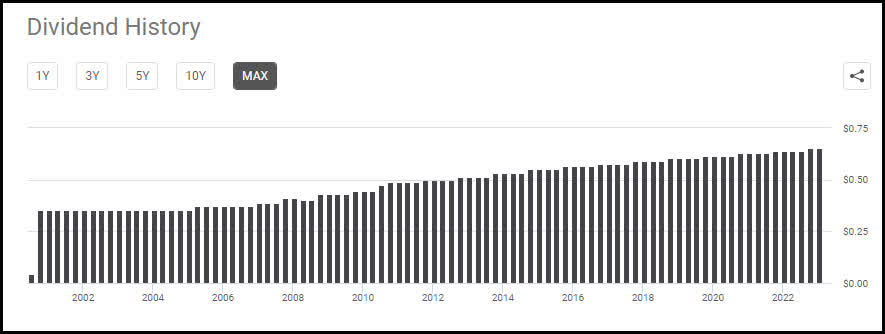

The current yield is 6.91% with a 48.63% payout ratio. Furthermore, the company has grown the dividend for the past 18 years. This has produced some excellent grades from Seeking Alpha’s quantitative metrics for the stock when it comes to dividend growth, safety, yield, and consistency.

Seeking Alpha

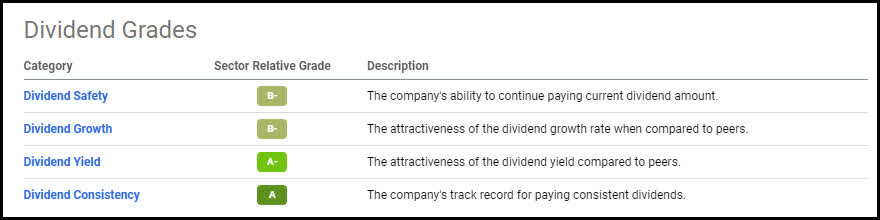

Seeking Alpha dividend grades

According to Seeking Alpha’s quantitative analysis regarding Verizon’s dividend history, the company scores very well. Let’s zero in on the A scores and take a closer look at the yield and consistency compared to peers and the company’s own 5 year average.

Seeking Alpha

6.91% Dividend yield gets an A- grade

The 6.91% yield is more than double that of the peer group at 3.1%, and 50% higher than the company’s 5 year average.

Seeking Alpha

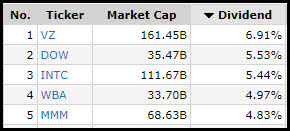

Highest Yielding DJIA blue chip

Verizon is actually the highest yielding stock out of all the Dow Jones Industrial Average blue chips presently, and not just by a little, either. Furthermore, Verizon has been paying out a solid growing dividend for nearly two decades.

Finviz

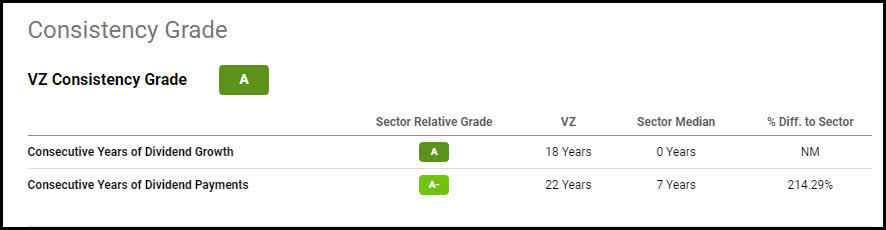

Dividend paid 22 years with 18 years of growth

The company scores an A on Seeking Alpha dividend consistency grading scale. Verizon has paid a dividend for the past 22 years straight, nearing dividend aristocrat status.

Seeking Alpha

18 years of steady dividend growth

On top of that, the company has steadily increased the dividend over the past 18 years. So Verizon pays a solid, safe, well-covered dividend that is increasing as time goes on. You can’t ask for more than that. Now, let’s turn our attention to the valuation metrics.

Seeking Alpha

Valuation Analysis

With Verizon stock down 32% from its 52 week high and trading at decade lows, it’s understandable that it is trading for a bargain-bin price. The stock presently has a forward P/E ratio of 7.28, which is 50% lower than the competition and 33% below its 5 year average. Verizon stock is definitely out of favor at present. I see this as a major buying opportunity for those looking for solid dividends with the opportunity for capital gains as well. Now let’s wrap this piece up.

Seeking Alpha

The Wrap-Up

Verizon’s stock is trading at a rock-bottom low while providing a 6.91% dividend yield. This seems like a no-brainer buy to me for prospective dividend and income investors. Everyone always quotes Buffett when it comes to these types of opportunities. I’m not going to do that. I have my own axiom for you, “Buying opportunities and bad news come hand in hand.”

The fact of the matter is that making money in the stock market is hard. This is due to the fact that it is more often than not completely counterintuitive to human nature. Buying low and selling high are the hardest decisions to make because you have to go against the grain. When you do, you will more often than not be heckled by the crowd of investors that either just sold out at the bottom or are still long at the top. You have to have courage in your convictions and believe in your thesis or you will most likely fold due to the pressure. With Verizon showing solid relative strength as the market sells off, already down 30%, having consolidated at the lows for the past three months, paying a 6.91% well-covered dividend, and being substantially undervalued both compared to its peers and on a historical basis, I’d say Verizon is a screaming buy at present.

Even so, everyone had their own suitability and risk tolerance levels. We may be in for further downside if the recession everyone is predicting materializes next year. I always suggest layering in to new positions over time to reduce risk. This improves your odds of building a new position with a decent basis. Those are my thoughts on the matter. I look forward to reading yours.

Be the first to comment