Portra/E+ via Getty Images

Dear readers/followers,

Centene (NYSE:CNC) is a great business. What we have here is one of the market leaders in the healthcare space. I’ve been neutral on Centene for a long time despite what some have said is an upside to the business. The problem here is the absolute lack of dividends for the company – now or in the future. It’s all capital appreciation for this business.

Centene isn’t the oldest business – it has somewhat over 30 years in the business, but age isn’t the deciding factor here, because the company has a very unique history.

Let’s revisit Centene and look at what is actually a double-digit potential upside.

Looking At Centene Again

Centene is an absolutely-solid healthcare company with roots in the non-profit sector, going public about 20 years back.

My own personal background actually lies in public work – prior to my career in stocks and as an analyst, I worked on the state and equivalent to the federal level with questions that often touched on healthcare for individuals – so a company like Centene that solves a very basic problem is close to my own heart – though I don’t make investments decisions based on that feeling.

The way healthcare is structured in the USA means that there can sometimes be difficulties for some gaining access to adequate care in times of need, because they may not have the money to pay for this. This is evidenced by the simple fact that prior to the introduction of the Affordable Care Act, tens of millions of citizens were without basic health insurance – which is very strange to me as someone from a nation where everyone has access to “everything” essentially for free in terms of healthcare, even if the waiting times have grown over the past few years.

Anyway, Centene works with this by being a market leader in Medicaid and Medicare, with over $120B in annual revenues, and a top #25 rank on the Fortune 500.

It provides healthcare coverage to close to 8-9% of the American population, and it’s by far the #1 leader in the aforementioned Medicaid segment, with continued growth in Medicare.

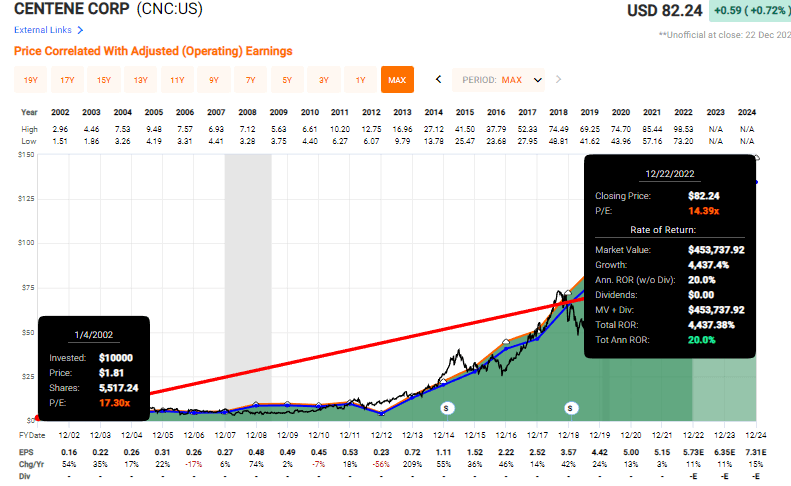

The fact that it offers healthcare to more disenfranchised populations doesn’t mean it doesn’t have impressive margins or growth. Centene has provided very impressive returns over time. Despite some volatility, a $10,000 investment in Centene would have more than doubled most index CAGR/RoR in 20 years.

Centene RoR (F.A.S.T graphs)

It’s sort of the easiest measure of success in investment. No matter the dividends, no matter what the company does, or how dubious I find the idea – show me these sorts of numbers over a 20-year period and you’re left tipping your hat – because very few companies I have ever invested in have managed 20% CAGR RoR over time – over a longer time.

The company’s recent results more or less confirm the current upside to the company. Centene reported revenue growth in the double digits, 11% YoY for 3Q22, with an HBR ratio of 88.3%, a line in the superb trend for the company.

Centene is battling current trends in inflation and cost with bid discipline, real estate dispositions/efficiencies and cost rationalizations as well as debt down payment.

Centene has also bought back $1.7B in shares this year alone, and the company’s excellent performance can be expressed in the 4Q22 guidance increase where it now expects a full-year EPS up to $5.75.The company has a very conservative ratio of costs and administrative – 8.4% SG&A from revenues.

The company has divested PANTHERx, and has begun the new PBM contract beginning in 2024. In addition, the company has been awarded multiple contracts across its various operating areas and subsidiaries, including in Mississippi, California, Texas, and Nebraska, and has announced Ambetter expansion into the state of Alabama, expanding its footprint by more than 60 counties across the current 12 existing states.

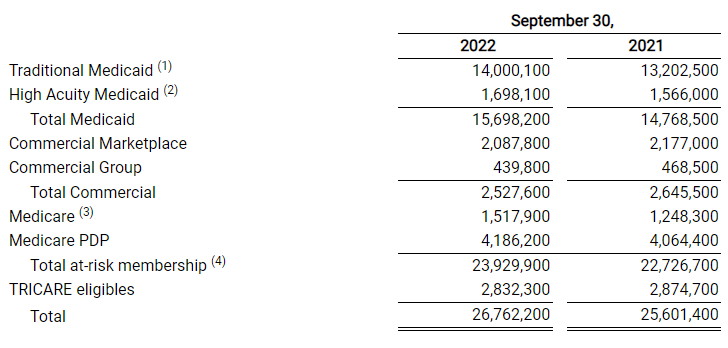

Here are the updated membership numbers for Centene – and you see despite the company’s high historical growth rates, the growth seems far from done at this time.

Centene IR (Centene IR)

Increasing the bottom range of its guidance, the company now expects to do a lot better than initially forecasted, confirming the otherwise solid outlook we can see here.

Some drawbacks to Centene – because they’re there. The company is still only a BBB- rated company with no dividend. The company’s differentiating factor – what makes it worth looking at for us as an investment, is its extensive expertise in government-sponsored healthcare, where it has 35 years of expert experience.

Where Centene shines is in the capital allocation and execution departments. Its priorities are clear. First, Organic growth. Second, Capital management and M&As through debt reduction, M&As, and finally, share repurchase to increase returns. The company keeps delivering on this strategy, and this is far from a bad strategy, all things considered because the current target for 2024E is an adjusted EPS growth of almost 50% in less than 3 years from 2021.

Still, you’re never likely to see a dividend here – not just because of current management, but in some ways, this company is a business that exists to serve its clients, not shareholders. If the company were to have dividends to consider, this might be contrary to the company’s actual mission.

There are other risks too. Because the company is Medicaid/Medicare-focused, any changes in eligibility determinations have the potential to seriously harm operations here. The same is true if political climates would somehow change the way these programs are managed or handled. However, despite very different political realities since the programs were introduced, no one has come close to touching or threatening to dismantle this – and I don’t see it likely that this will happen going forward.

I, therefore, consider potential downside risks here to be somewhat manageable – the trouble is found in a different place when looking at Centene – namely that valuation.

Centene’s Valuation

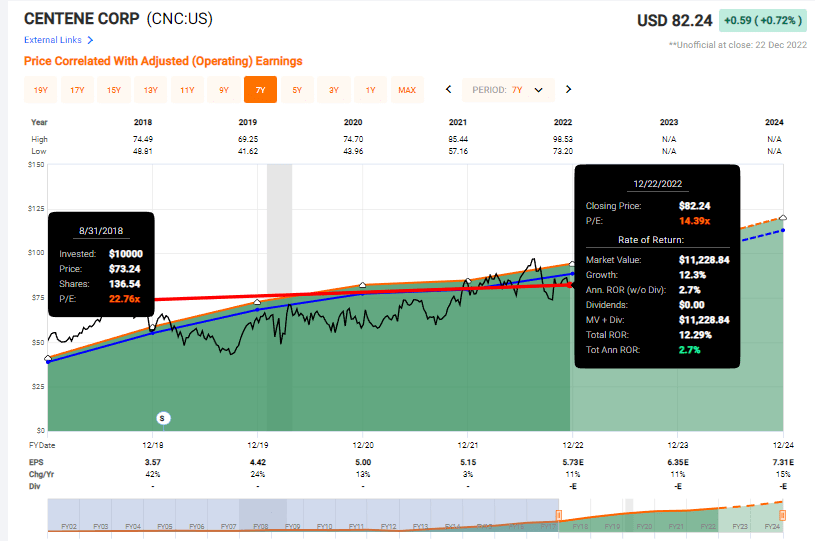

Centene’s valuation hovers around the 15-17x mark on a normalized basis, but there’s plenty of volatility going into the company here. The potential for significant underperformance here is high if you buy at too-high multiples, such as we saw in 2018.

What do you think would have happened, if you bought Centene at 22.7x as some analysts recommended back in 2018?

Centene RoR (F.A.S.T graphs)

That’s an underperformance “hole” that you still haven’t dug yourself out of. Because of the lack of a dividend, it’s even more important than usual that you only buy the company at market-beating undervaluations, to make sure that you’re in a good place to outperform.

However, thankfully, we’re not at 20x+ today – we’re well below this. But I also want to draw your attention to the significant amount of volatility that the company does have, which presents you with plenty of opportunities for some play here.

Previously, I targeted Centene as an options investment, and this is still possible. Instead of going for the common share, you can sell “put” options – and this is a play I will look at in this article, for the first time in several months (I haven’t reported on options potentials for a long time). In my previous article, I called Centene a better investment in terms of the common, but given the volatility, we have here, I’m no longer sure that this is actually the case.

If the company had even a slight dividend, I’d be willing to accept a somewhat bullish thesis for Centene here. But the fact is we’re talking about a company that typically trades below 15X P/E, and currently trades at around 14.4x.

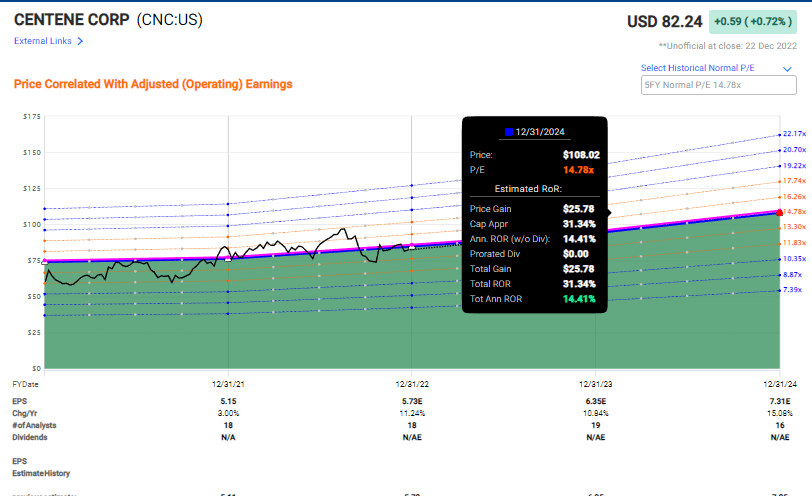

There is a slight discount here – and I’ll tell you right now, I am changing my thesis to “BUY”. My price target for Centene as a business was $83/share. I’m not shifting that price target in this article, and currently, the company has a small upside to this target, trading just north of $82/share.

The normalized upside on a 14.78x P/E for a 3-year period is 14.41% here. Typically I would say the absolute minimum conservative upside for an investment like this without a dividend is 15%.

So you can see why the company is basically on a razor-thin margin of error in terms of my PT, and why, when this article is published, it may have already gone beyond that and gone to a “Hold”.

But as I am writing it though, this company is a “Buy” – I’m shifting my target based on the pure share price here.

But I personally would not invest in the common at this time – the margin is too small, and I see better and safer plays out there.

Centene Upside (F.A.S.T graphs)

Analysts have an unfortunate tendency to allow for a premium here, with S&P Global averaging at about 10-15%. That’s exactly the sort of premium in its targets that would have prevented investors from selling and making money here. The current S&P Global targets for this company come to close to $100 per share on average, based on 19 analysts. It’s my view that these analysts do “not learn”. Their range starts at a low point that’s below my own PT, at $85/share, and goes all the way up to $115.

I believe such targets to be remnants of the era of low interest – we need higher returns or potential dividends to allow for such targets.

Here is my thesis on Centene.

Thesis on Centene’s common shares

- Centene is a class-leading managed healthcare company in several key segments that aren’t going anywhere. It has proven, historically, that it can effectively allocate capital and outperform over time no matter the market. It is, however, BBB- rated and has no dividend – and losses or underperformance is a very real possibility if you don’t pay attention to valuation.

- For that reason, my conservative view on Centene is that it should not be bought above $83/share, and that’s where I put my PT.

That makes the company a “Buy” here, but with a razor-thin margin that may disappear at any time.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

There is a razor-thin positive margin for Centene that I consider to be valid at this time, making it a technical “Buy”.

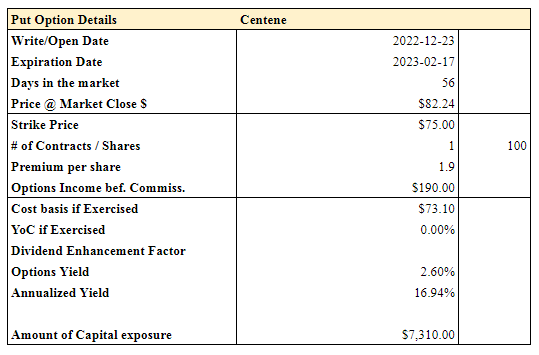

The Options Play for Centene

As I said, I will also take a look at a different way to approach Centene here. You could, if you have the capital, write a cash-secured put that grants not only an annualized yield but a potential to buy Centene far cheaper than currently available on the open market with its common share.

Here is one such possibility I found that I myself am considering at market bell if the premiums stay at similar levels.

Option Details (Author’s Data)

You would be exposing around $7,300 for 56 days at an annualized yield of close to 17% for a chance to buy Centene at $75. That, to me, is a superb RoR for a superb company, at a very solid price.

I may play this option today – and if you want Centene, that’s what I would be looking at.

Be the first to comment