Sundry Photography/iStock Editorial via Getty Images

Thesis

Palo Alto Networks’ (NASDAQ:PANW) stock has seen a modest decline over the past year and investors may be tempted to step in and buy the dip. The company has been executing well but we believe the stock is still too expensive for this macroeconomic environment and for their decelerating revenue growth rate. Investors may want to wait on the sidelines for now.

Continued Execution

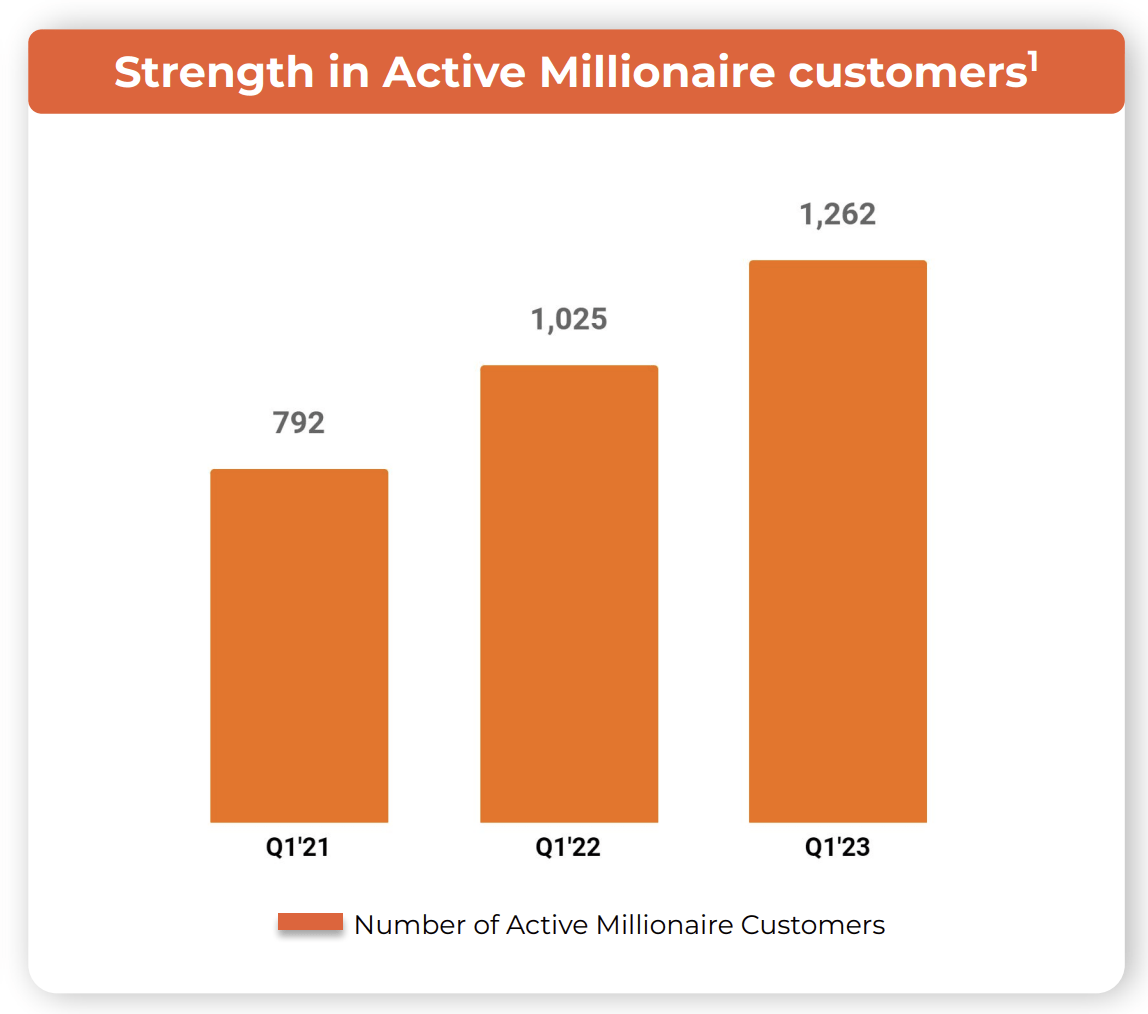

The company has been doing a good job with their land and expand strategy. The number of customers that spent $1 million or more over the past year has seen a healthy increase.

Growth in Number of High Spending Customers (Palo Alto Networks’ Q1 2023 Earnings Presentation)

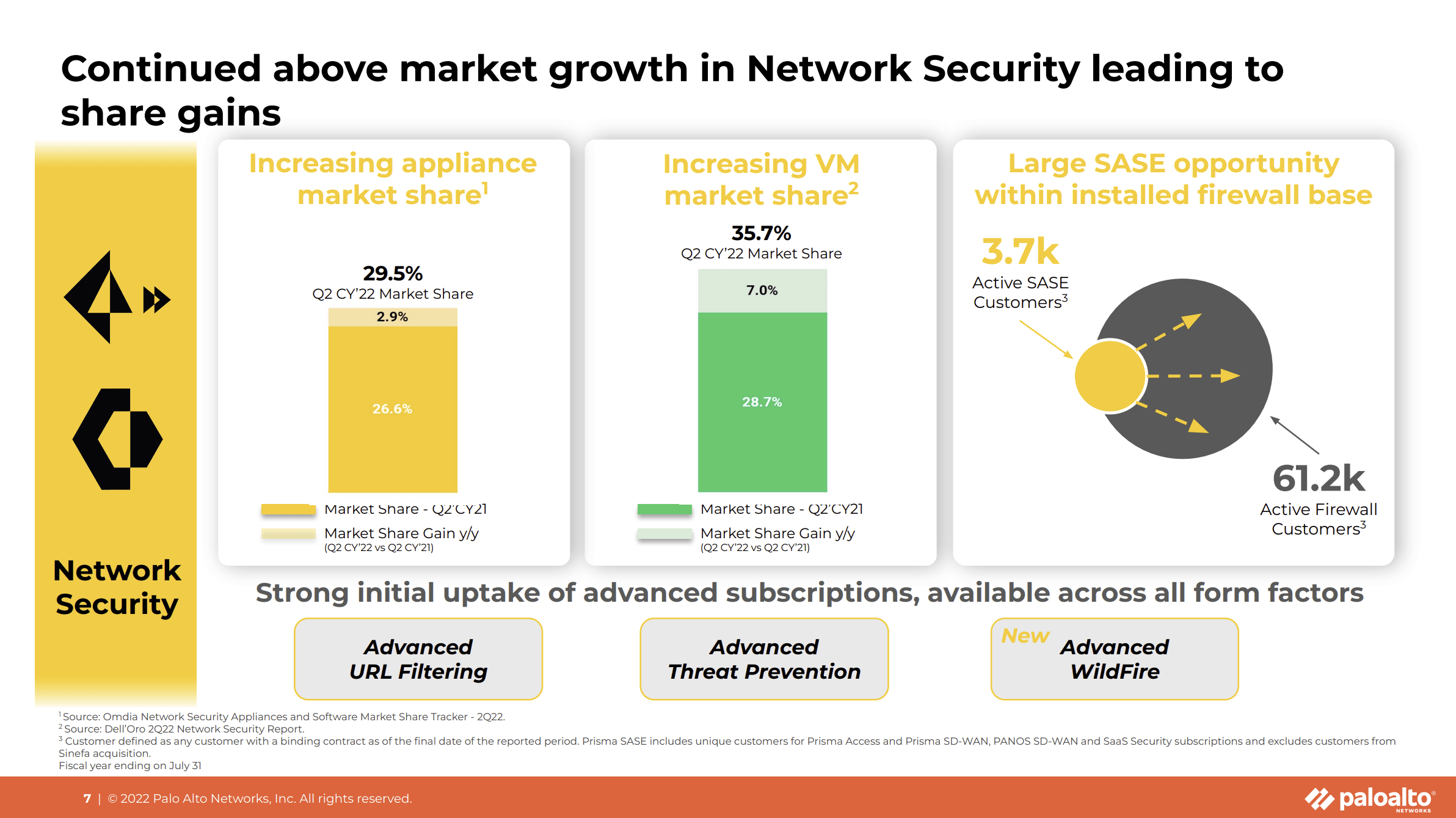

Palo Alto Networks has been gaining market share in their network security segment. This is good news for investors and it shows that they have a superior offering and a durable competitive advantage.

Network Security Segment Growth (Palo Alto Networks’ Q1 2023 Earnings Presentation)

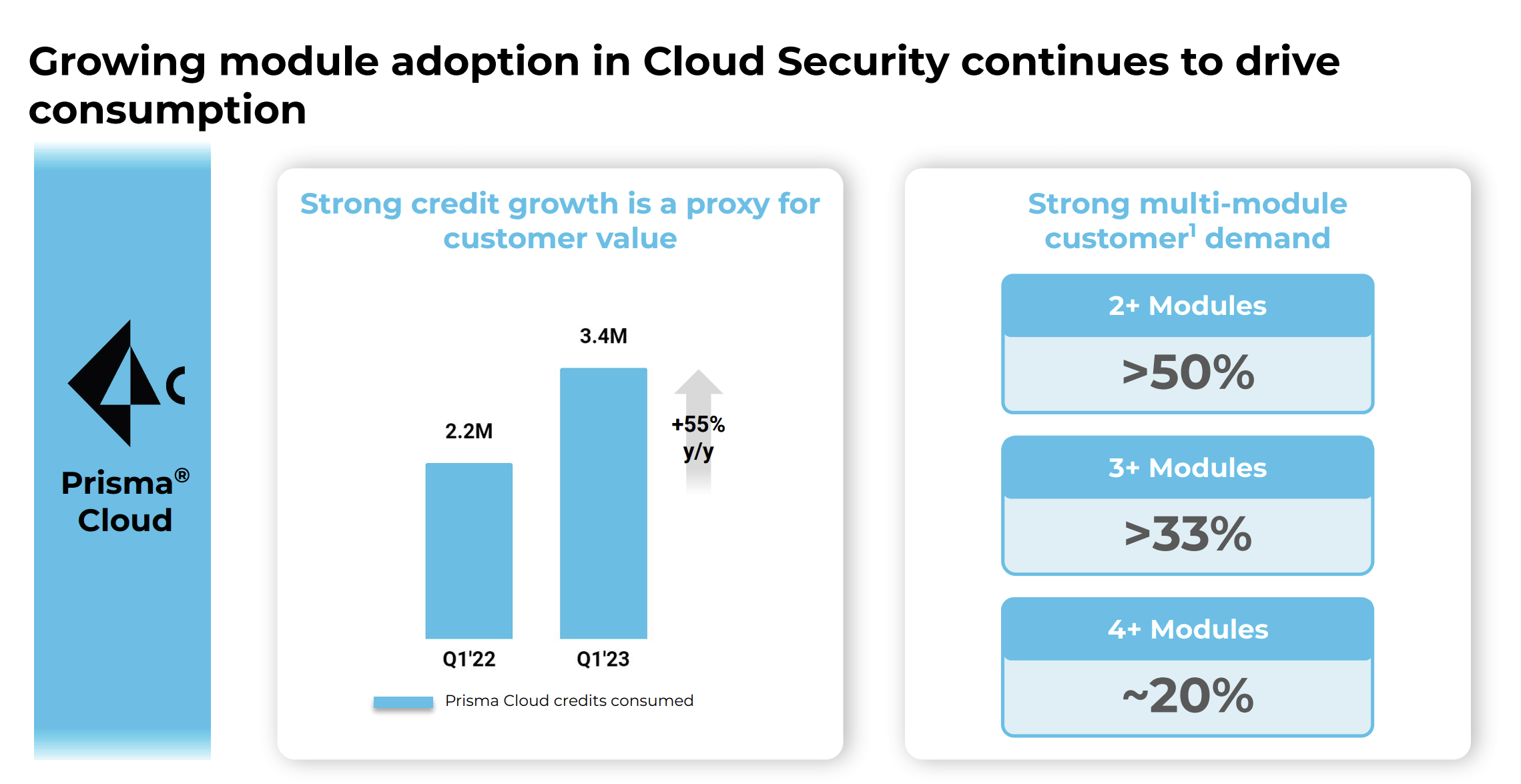

Regarding their cloud security segment the company states in their 10-Q that “Prisma Cloud secures hybrid and multi-cloud environments for applications, data, and the entire cloud-native technology stack across the full development lifecycle; from code to runtime.” This part of cybersecurity becomes more important by the day as additional access points are opened in a development/deployment ecosystem. They showed strong results in this segment and it’s likely this growth can continue.

Prisma Cloud Growth (Palo Alto Networks’ Q1 2023 Earnings Presentation)

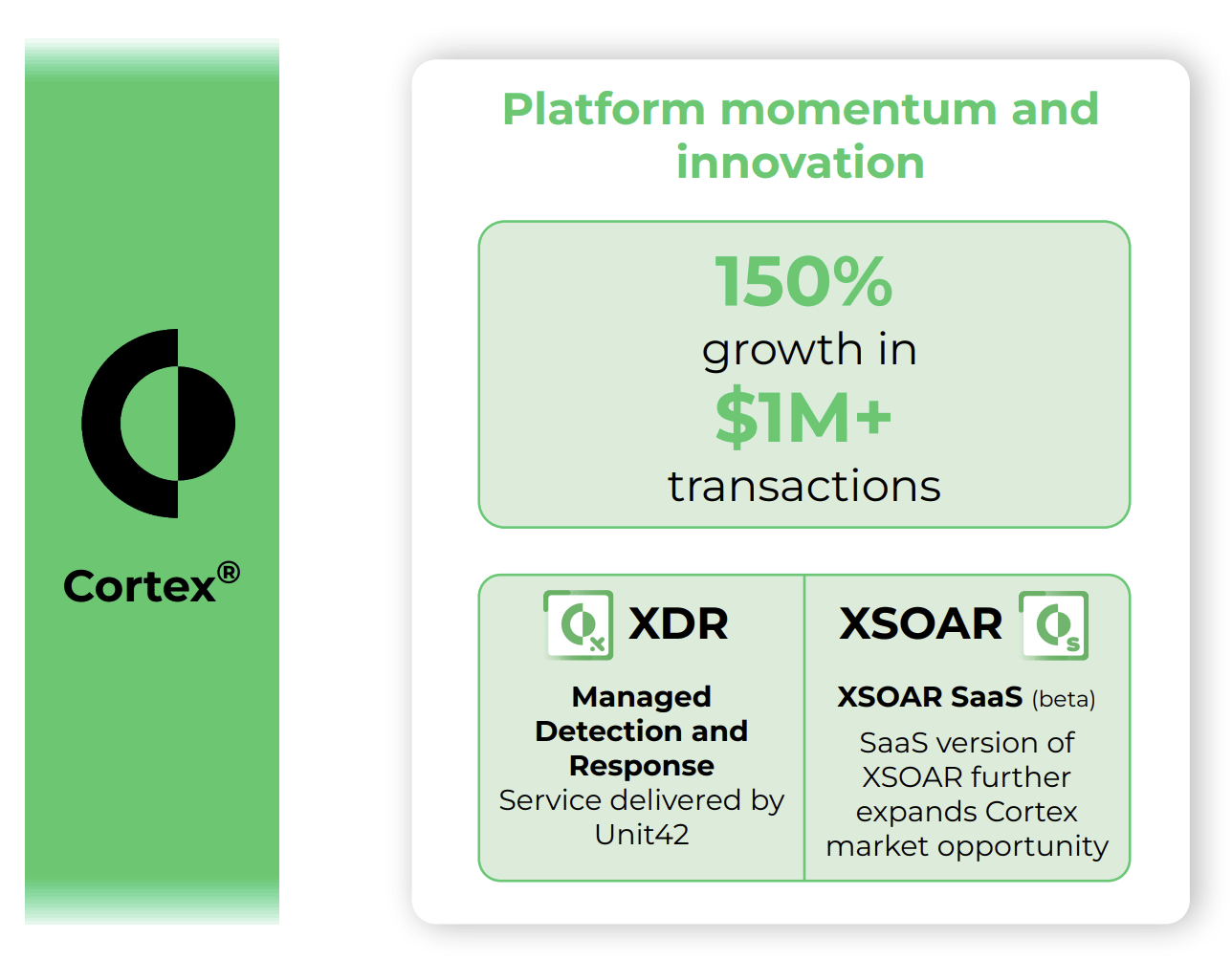

Their Cortex portfolio covers endpoint security, security analytics and security automation. Customers are adopting this solution in droves and this should continue to be a growth engine for the company.

Cortex Growth (Palo Alto Networks’ Q1 2023 Earnings Presentation)

Palo Alto is making good progress on their goal to develop an all in one cybersecurity solution. This operational success has translated to better financial results. Unfortunately the company focuses on non-GAAP measures of profitability and their GAAP profitability is lacking.

Financial Metrics

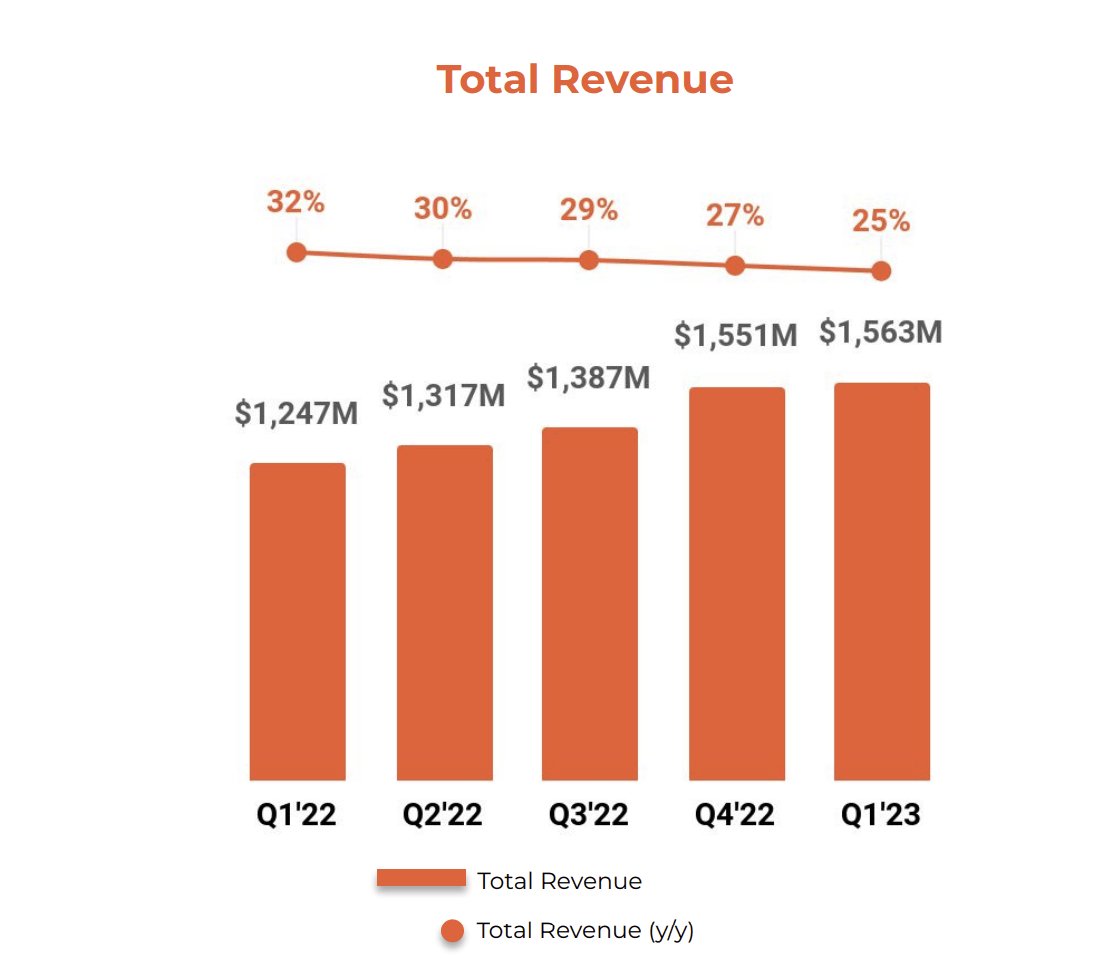

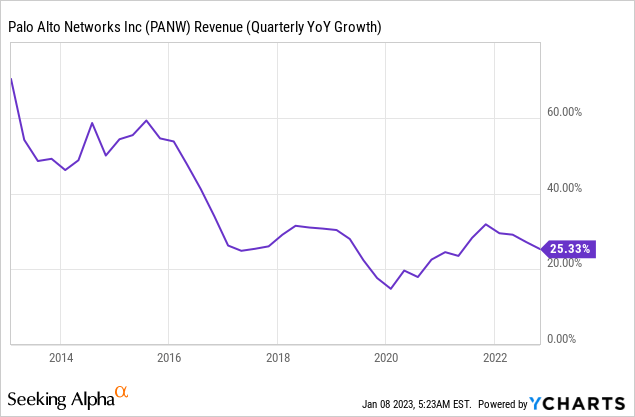

Palo Alto Networks reported a solid fiscal first quarter with revenues growing 25% year over year to $1.6 billion.

Revenue Growth (Palo Alto Networks’ Q1 2023 Earnings Presentation)

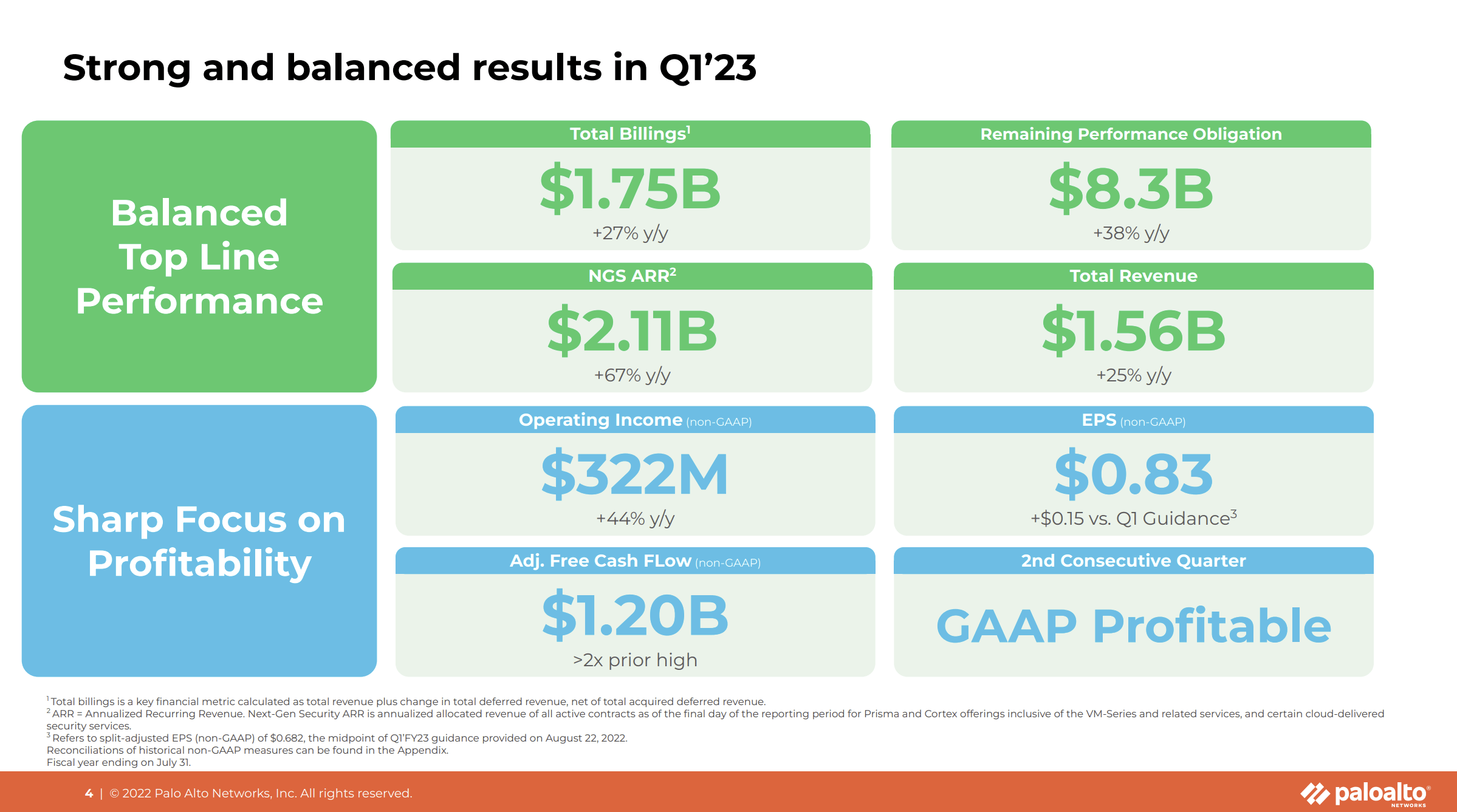

Their operating income for the quarter was $20 million, which is a step in the right direction when compared to their net loss of $103.6 million in the year ago period. The company references Non-GAAP numbers when discussing profitability and from their point of view operating income was $322 million and increased 44% year over year.

Financial Performance (Palo Alto Networks’ Q1 2023 Earnings Presentation)

Claiming they earned $322 million in operating income is very generous and for valuation purposes we will be looking at GAAP numbers. The non-GAAP figures conveniently ignore the $266 million spent on SBC in the quarter as if employees would not need to be compensated in cash if the SBC disappeared.

For investors that defend stripping out SBC when looking at mature tech companies let’s consider a thought exercise. If an employee is making $200,000 in cash payments and $100,000 in SBC and that SBC is removed, do you think the employee would accept the $100,000 pay cut? Or would they expect the $100,000 shortfall to be made up in cash? Non-GAAP treats this employee as costing the company only $200,000 but their real cost is always $300,000.

Another thought exercise. Let’s say a company is spending way too much money on headcount and investors are complaining about it. Let’s also assume these investors are okay with measuring profitability using non-GAAP numbers. The managers of the business become heavily incentivized to shift compensation to SBC instead of actually trimming headcount and right sizing operations. Investors will see non-GAAP profitability increasing and be satisfied but the original problem remains. In this example management didn’t actually increase profitability or fix a problem.

Palo Alto Networks has been executing well on their long-term vision and their valuation looks attractive relative to the cybersecurity sector and when looking at non-GAAP P/E. The problem is that GAAP earnings paint a different picture, especially when considering their decelerating rate of growth.

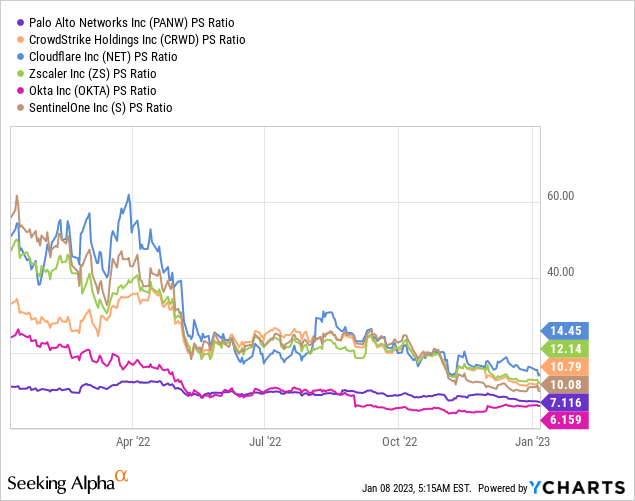

A Steep Valuation

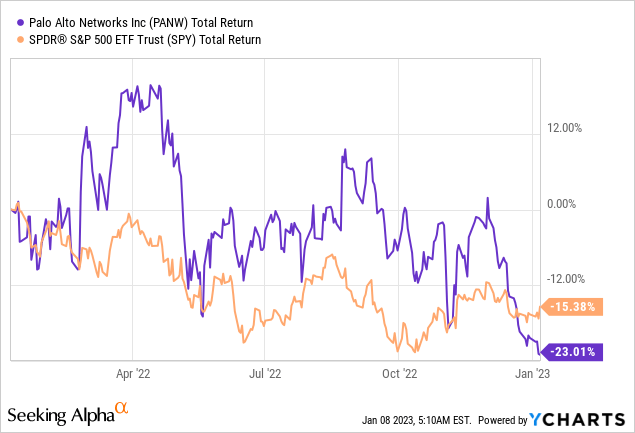

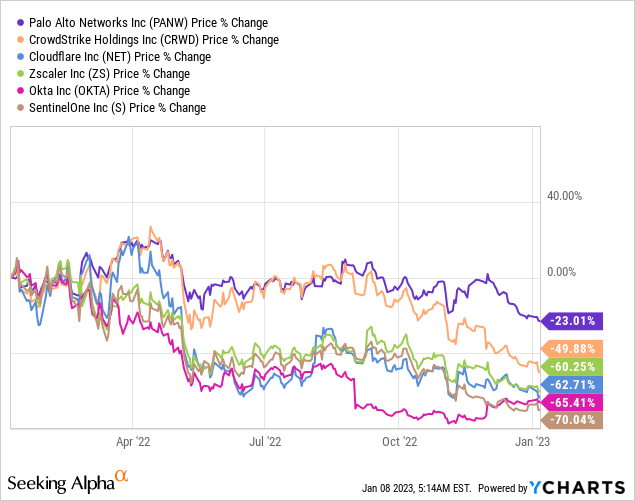

Palo Alto Networks has held up pretty well all things considered, with the stock off by only 23.01% over the past year. This is much better than many other companies in the cybersecurity space and PANW investors have benefited from the company’s size and maturity.

On a price to sales basis PANW is trading below many of their sector peers. These price to sales multiples have come down rapidly over the past year, and a multiple of around 10 times isn’t unreasonable for a tech company with high margins. The problem is that Palo Alto Networks’ actual net margins are low.

Over the trailing twelve months PANW has been unprofitable. In their most recent quarter they turned profitable and made $20 million in net income. Annualizing that gets us to $80 million but let’s give them the benefit of the doubt and say that they can earn $200 million in net income over the next year. Using the current diluted market cap of $45,633,240,000 this gives us a forward PE ratio of 228.166. While some companies with rapid revenue growth can justify a high PE ratio, the revenue growth rate of Palo Alto Networks has been decelerating.

A forward PE ratio of 228 is astronomically high given a revenue growth rate of 25%. The risk/reward in Palo Alto Networks still doesn’t look appealing despite the drop in the stock. Investors can wait until management demonstrates that they are able to activate the operating leverage in their model and show a focus on generating GAAP profits.

Risks

The risk to this thesis is that Palo Alto Networks outperforms our expectations. Here are some ways they can do that:

They begin to rapidly improve profitability and investors that were not in the stock would miss out if it rebounded sharply.

Their revenue growth could accelerate, justifying a premium multiple.

We have been looking at PANW for a while and are fans of their long-term strategy and competitive positioning. We are looking to jump into the stock once the risk/reward becomes better and they begin to show more financial discipline, but for now we will watch and wait.

Key Takeaway

Palo Alto Networks has been executing well and is an attractive business. As is often the case, investors are willing to pay a high price for high quality companies. On a GAAP basis the stock looks too richly valued and investors may want to wait on the sidelines for now, especially in this market environment.

Be the first to comment