Thapana Onphalai/iStock via Getty Images

We continue to be buy-rated on the cloud identity company, Okta (NASDAQ:OKTA). As we kick off 2023, we believe OKTA’s challenges have been predominantly laid out on the table; investors are in the know. In our opinion, OKTA faces two major headwinds as it enters the year: slowing spending from companies on cloud infrastructure and the integration of Auth0. Our bullish sentiment on the stock is based on our belief that the company is using a sniper approach to resolve its near-term headwinds.

OKTA is down nearly 66% over the past year but up almost 10% since we wrote on it last at the start of December. We believe OKTA is well-positioned to grow as it works through its integration of Auth0 and shrinks operating losses. OKTA operates in a highly lucrative niche within cloud security: Identity, and Access Management (I(AM)), forecasted to grow at a CAGR of 14.54% between 2021-2028. From a valuation perspective, we believe the stock is relatively cheap and recommend investors buy the dip to enjoy profitability in 2H23.

The worst is behind

OKTA had a rough 2022 with the breach in January by Lapsus$ hackers, bumpy integration of Auth0, and macroeconomic headwinds causing weaker IT spending on cloud infrastructure; our bullish sentiment on the stock is because we believe it’s a rebound pick in the tech space. We expect OKTA to resolve its near-term headwinds and position itself toward profitability in 2023 on two fronts:

1. Integrating Auth0 into the IAM portfolio

OKTA completed its acquisition of Auth0 a while back in May 2021, but the company has yet to enjoy the benefits of its $6.5B acquisition. We believe Auth0 will add another layer of leverage to OKTA once it’s successfully integrated. Auth0 builds and operates a cloud-based identity platform for developers, which complements OKTA’s customer identity access management (CIAM). We believe OKTA struggled to integrate Auth0 into its product portfolio. However, we believe OKTA is now reworking itself to incorporate its CIAM products with Auth0 and expect this to boost OKTA’s market share in the IAM space.

While Auth0 has brought headaches to management at OKTA, we believe the acquisition was smart as it steered OKTA to take a bigger part of the market. We believe OKTA is working to become a one-stop shop for cloud identity services.

2. Weaker IT spending on cloud infrastructure

OKTA has not been spared from the broader sell-off of tech stocks due to macroeconomic headwinds. We believe higher inflation and spiking interest rates have caused companies to reduce spending on cloud infrastructure amid market uncertainty. We believe the weaker IT spending has negatively impacted cloud service providers, but only in the near term. The annual growth rate of cloud infrastructure fell below 30% for the first time in 2022. While bears expect the macroeconomic headwinds to continue causing customers to drop their IT spending, we disagree. We believe the grunt of weaker IT spending passed in 2022. We expect increased demand in 2023 as companies re-organize their budgets and allocate necessary budgets to the IAM space. We’re also constructive on OKTA taking more cost-efficient measures. In its 3Q23 earnings call, CFO Brett Tighe discussed reining in spending to maneuver its operating losses caused by macroeconomic headwinds. We expect OKTA to grow more rapidly in 2023 and recommend investors buy the stock at current levels.

Bright future in the cloud identity space

We’ve been bullish on OKTA since early 2021, but we believe the stock’s current valuation provides an unprecedented window to invest in the booming IAM market. We continue to be of the mindset that OKTA shares overcorrected late last year on lower guidance for Q4. Despite the near-term challenges, OKTA’s 3Q23 earnings report achieved a 38% Y/Y increase in subscription revenues. With the de-risked guidance and all the issues in the open, we believe OKTA is better positioned to outperform in the cloud identity space.

We expect OKTA to have a bright future in the cloud security space as the growing threat of data exposure, leaks, loss, and insider attacks increase, fueled by the global adoption of new cloud-based technologies. We expect demand for OKTA’s services only to increase as it figures out how to integrate Auth0 successfully. We believe OKTA also has the advantage over the competition in its nature as a horizontal company, making its products applicable to any sized company across the spectrum. We’re specifically constructive on OKTA’s position in the mid-market segment of the cloud security industry.

We analyze OKTA through the broader prism of cloud infrastructure in the cloud security market. While OKTA has been down significantly across the past year, so has its competition in cloud security. Microsoft (MSFT) Azure, Amazon (AMZN) AWS, and Alphabet (GOOG) Google Cloud have their own integrated IAM solutions and have all suffered significant stock dips amid macroeconomic headwinds. While Azure, AWS, and Google Cloud dominate the cloud infrastructure space, we believe there’s plenty of room for competition. We expect OKTA to have the advantage of adequately utilizing Auth0 in 2023 to grow more rapidly and outperform expectations.

Valuation

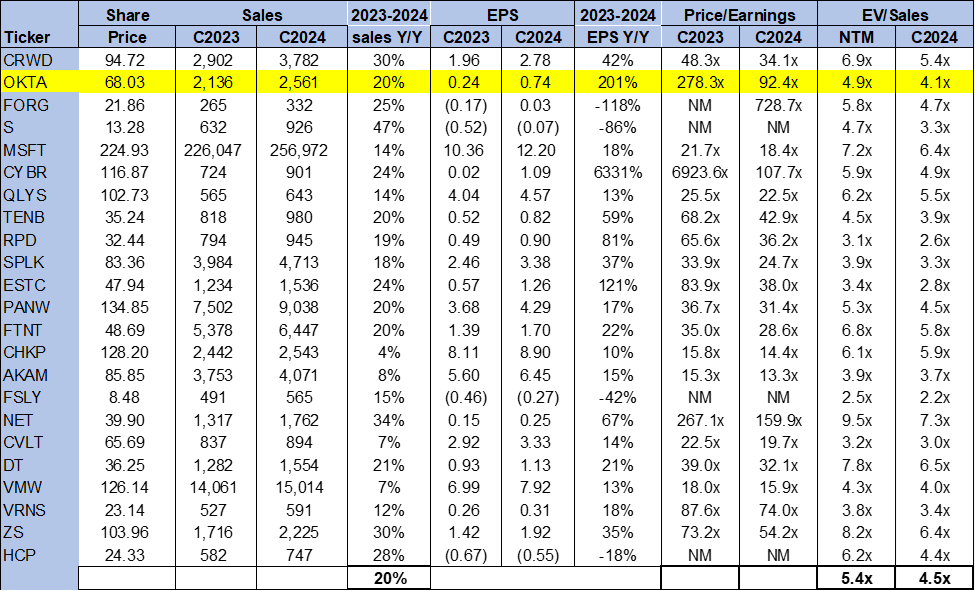

OKTA is trading at a lower multiple than the peer group, and we recommend investors buy the stock sell-off. The stock is trading at 4.1x EV/C2024 Sales versus the peer group average of 4.5x. On a P/E basis, OKTA is trading at 92.4 C2024 compared to the peer group average of 79.4x. We recommend investors buy the dip as we expect OKTA is ironing out its near-term challenges.

The following graph outlines OKTA’s valuation compared to the peer group.

TechStockPros

Word on Wall Street

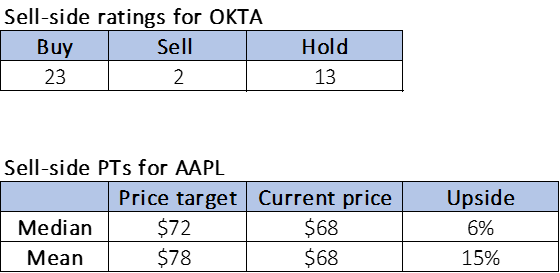

Wall Street is bullish on OKTA. Of the 38 analysts covering the stock, 23 are buy-rated, 13 are hold-rated, and the remaining are sell-rated. The stock is currently trading at $68. The median sell-side price target is $72, while the mean is $78, with a potential upside of 6-15%.

The following graph outlines OKTA’s sell-side ratings and price targets.

TechStockPros

What to do with the stock

We believe OKTA provides a highly compelling valuation after last year’s stock sell-off. We expect OKTA to rebound in 2023 as it lays out its biggest risks on the table and de-risks guidance for 4Q. We believe the worst is behind for OKTA and expect the company to grow meaningfully in 2023 as a leader in the cloud identity space. We recommend investors buy the stock at current levels.

Be the first to comment