Torsten Asmus/iStock via Getty Images

Novartis (NYSE:NVS) recently reported positive results from two registrational trials of iptacopan in PNH patients. We are yet to see the results from the second trial in patients naïve to C5 inhibitors, but the first trial has demonstrated that iptacopan is much better than AstraZeneca’s (AZN) C5 inhibitors Ultomiris and Soliris in PNH patients with residual anemia. I was very impressed by the data presented at ASH and now believe iptacopan could be a significant threat to Ultomiris and Soliris in the PNH market and especially so to Apellis Pharmaceuticals’ (APLS) Empaveli. Empaveli achieved similar efficacy to iptacopan in the same population, but iptacopan has a significant convenience advantage as it is a twice-daily oral drug while Empaveli needs to be administered as a subcutaneous infusion twice a week.

Cross-trial comparisons

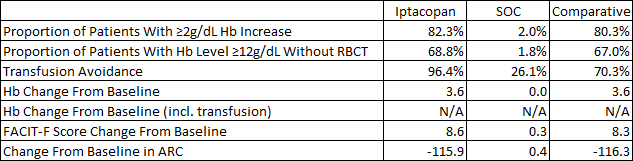

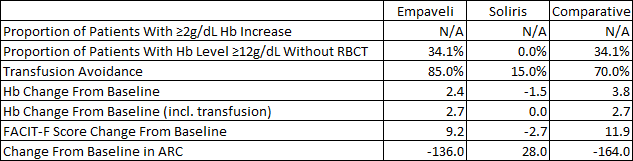

The phase 3 results of iptacopan in patients not well controlled on C5 inhibitors were impressive. With the limitations of cross-trial comparisons in mind, below is a table comparing the results iptacopan and Empaveli achieved versus the standard of care in iptacopan’s case (Ultomiris or Soliris) and Soliris in Empaveli’s case. As you can see, the results mostly favor iptacopan on a cross-trial basis – greater absolute increases in hemoglobin and a far greater proportion of patients achieving hemoglobin levels equal to or greater than 12g/dL.

Iptacopan ASH abstract Empaveli product label

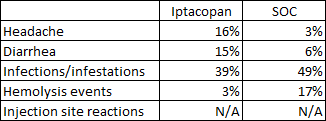

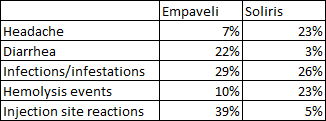

Safety and tolerability look similar across the two trials. Both Empaveli and iptacopan had lower rates of hemolysis events compared to C5 inhibitors, iptacopan had greater rates of headaches while Empaveli had lower headache rates than Soliris and convenience is a major advantage of iptacopan as it is an oral medication taken twice daily versus twice weekly subcutaneous infusions of Empaveli that result in injection site reactions in 39% of patients taking it.

Iptacopan ASH abstract Empaveli product label

We are yet to see the phase 3 results of iptacopan in treatment-naïve PNH patients as those results will be more representative of its effect in the overall population, but we know it achieved the primary endpoint and based on the strong effects in patients not well-controlled on C5 inhibitors, I expect similarly strong results in the overall PNH population.

Based on the strength of the data, I believe iptacopan has a strong chance at taking the majority market share from Empaveli in patients not well-controlled on C5 inhibitors, and that it can likely take decent market share in the overall PNH market from AstraZeneca’s Ultomiris and Soliris.

Implications for Novartis and other shots on goal for iptacopan

I believe Novartis has another blockbuster in its hands and that iptacopan can be a $1 billion+ drug for the company in PNH alone. For that to be the case, it will need to capture more market share in patients that are well controlled on Ultomiris and Soliris and that means we need to see robust data from the second phase 3 trial that was just toplined. But I expect that to be the case and that iptacopan should work similarly well as it did in patients who are not well-controlled on C5 inhibitors.

But iptacopan’s potential utility goes beyond PNH. It could be similarly successful in the aHUS indication which is also dominated by Ultomiris and Soliris and where there will be fewer competitors. And the other indications of interest are IgA nephropathy, C3 glomerulopathy (‘C3G’), both of which could be approved as soon as 2024 – IgA nephropathy (‘IgAN’) if the 9-month interim readout is successful next year and the C3 glomerulopathy readout is also expected next year.

And finally, there are additional shots on goal that could meaningfully increase iptacopan’s peak sales potential later this decade – idiopathic membranous nephropathy (‘iMN’), lupus nephritis, immune thrombocytopenia (‘ITP’), and cold agglutinin disease (‘CAD’). The proof-of-concept trials in these indications have only recently started and I would not expect approvals in any of these indications before 2026. Below is a pipeline slide of iptacopan showing the expected clinical timelines for each indication and the estimated U.S. prevalence in thousands.

Novartis investor presentation

The IgAN market is becoming increasingly competitive and iptacopan will need to show good data because it will not be able to compete on convenience with drugs like sparsentan, atrasentan, or even off-label Farxiga (dapagliflozin). You can read more about the IgA nephropathy landscape in my recent article on Travere Therapeutics (TVTX). Iptacopan itself generated decent proteinuria reductions in IgAN patients in the phase 2 trial – up to 40% after six months of treatment and longer exposure may generate additional reductions. Longer-term, there may also be room for drug combinations with these different classes that could produce even better outcomes for IgAN patients.

C3G is a much smaller market than IgAN, but it could be a nice addition to iptacopan’s product label. In the phase 2 trial in 16 patients with C3G who have not had a kidney transplant, iptacopan showed a 45% reduction in proteinuria, and in 7 patients whose C3G had returned following a kidney transplant, iptacopan showed significantly reduced C3 protein deposits compared to baseline.

And to date, iptacopan was generally safe and well-tolerated across these trials.

Overall, I see iptacopan as a $4 billion+ product at peak for Novartis in PNH, C3G, and IgAN, and longer term and in a blue-sky scenario, this could be a $10 billion+ product. But to get there, it would need to work well in at least five or six indications.

Of course, for a company of Novartis’ size and more than $50 billion in annual sales, iptacopan will probably not create a lot of shareholder value, but it is one of the more promising growth products in the next 5-7 years, and it could really move the needle for the company later this decade if the trials in iMN, lupus nephritis, ITP and CAD are successful as all four are potentially billion-dollar-plus indications.

Impact on Apellis and AstraZeneca

I previously expected Apellis’ Empaveli to generate between $400 million and $500 million in global peak annual sales in PNH, but that has come into question lately given the slower-than-expected uptake in the last two quarters, especially now that iptacopan has delivered excellent data and has a significant convenience advantage and no infusion reactions either since it is taken by mouth. I now believe Empaveli will peak in PNH in the following quarters and that sales could start to erode once iptacopan hits the market and that its global peak sales potential will be $100-150 million at most, reserved for patients who do not respond well to iptacopan or Ultomiris/Soliris.

Apellis will have to rely on intravitreal pegcetacoplan in geographic atrophy, and potentially on other indications if it can generate differentiating data to iptacopan, C5 inhibitors, and/or other complement candidates in development.

And for AstraZeneca, I do not believe iptacopan will make much of a difference to its C5 franchise. I do not know the revenue split anymore since it is not being disclosed, but given the size of the PNH population and the growing uptake in NMOSD and generalized myasthenia gravis, I suspect the contribution of PNH is less than 30% of the combined net sales of Ultomiris and Soliris.

I expect iptacopan to get decent market share (and that is assuming data in treatment-naïve patients look similarly impressive) and that the addition of AstraZeneca’s factor D inhibitor danicopan to Ultomiris will not make a significant difference on efficacy, and no difference at all on the side of convenience since it adds the pill burden of danicopan to Ultomiris.

However, AstraZeneca has another shot on goal with factor D inhibitors – vemircopan is an improved factor D inhibitor compared to danicopan, but the preliminary data does not look as convincing as the data iptacopan generated. It looks like iptacopan generated better data in difficult-to-treat PNH patients than vemircopan did in treatment-naïve patients as vemircopan fell short of achieving normal hemoglobin levels. But it is still early days for vemircopan and additional dose-escalation could lead to better efficacy in PNH patients and could lead to it being a formidable competitor to iptacopan.

And given the growth in other indications, iptacopan taking PNH market share may not even register in AstraZeneca’s quarterly reports as the impact will likely be gradual rather than immediate, perhaps like Empaveli’s impact but with three to four times the uptake due to the significant convenience advantage.

Conclusion

Iptacopan should become a decent growth product for Novartis in the following years and I expect it to disrupt the PNH market by taking more significant market share from Ultomiris and Soliris, and I expect Empaveli will have a hard time continuing to grow or even maintain the existing revenue base when iptacopan reaches the market. Iptacopan is also a true pipeline in a drug with significant potential beyond PNH. The near-term opportunities are C3G and potentially IgAN, and longer-term opportunities are iMN, aHUS, lupus nephritis, ITP, and CAD.

I do not believe AstraZeneca will suffer a lot as the growth of Ultomiris in other indications such as NMOSD and generalized myasthenia gravis should more than make up for the potential losses in PNH (and/or aHUS longer term) and it has an oral factor D inhibitor vemircopan in development that could turn out to be a formidable competitor to iptacopan itself.

Be the first to comment