pinkomelet

Co-produced with “Hidden Opportunities.”

If you grew up back in the ‘50s and ‘60s, getting a good education and, consequently, a good job was highly emphasized in the community. The epitome of a “good job” was working in the public sector, in the local, state, or federal government.

You went to work wearing a suit and tie and earned paychecks that were reliable, if not good. You stayed with the same employer for decades, and for these years of continuous work, you were rewarded with a pension. This was also a time when long-term, good employees received a gold watch upon retirement.

This tradition was started in the ’40s by the management of PepsiCo, Inc. (PEP), who embraced the concept:

you gave us your time, now we are giving you ours.

General Motors (GM) was the nation’s largest employer in the ’50s, the ’60s, and most of the ’70s, and the automotive giant was also a major participant in attractive pension plans and gold watches for long-term employees.

Fast forward ~75 years and the employment scene is drastically different. The median number of years a wage and salary worker stayed with their current employer is ~4 years. Today’s workforce is highly mobile, and many individuals will change employment in a heartbeat. And it works both ways, there is limited loyalty from both parties. Employment in the U.S. is largely “At Will” and an employer can terminate an employee at any time for any reason. Businesses don’t hesitate to cut down on their staff or shutter divisions at the slightest pressure on profits.

Sorry millennials and Gen-Z, no gold watches or pensions for you. But we have another way for you to build passive income in retirement. We discuss two discounted preferred picks with up to 9% yields. With an adequately diversified portfolio of income producers, you can create your own pension and not trade your time for money.

Pick #1: OXLCM Term-Preferred, Yield 6.9%

Oxford Lane Capital Corp., 6.75% Cumulative Series 2024 Term-Preferred Stock (OXLCM)

Collateralized Loan Obligations (“CLO”) are among the most misunderstood securities in the market. Investors either draw parallels with CDOs and MRBs that were at the heart of the Great Financial Crisis, or they look at the expense ratio of the Closed-End Funds (“CEF”) that invest in them and run away. It’s ok, their loss is our gain; we will invest towards growing our income from these well-managed and closely regulated instruments.

CLOs have covenants that require the fund manager to test the portfolio’s ability to cover its monthly interest and principal payments. These coverage tests are a vital mechanism to detect and correct collateral deterioration, directly affecting the allocation of cash flows. The most common are interest coverage and over-collateralization tests. If the tests reveal deficiencies, the manager must take cash flows from the lowest debt and equity-tranche holders and divert them to retire the loan tranches in order of seniority.

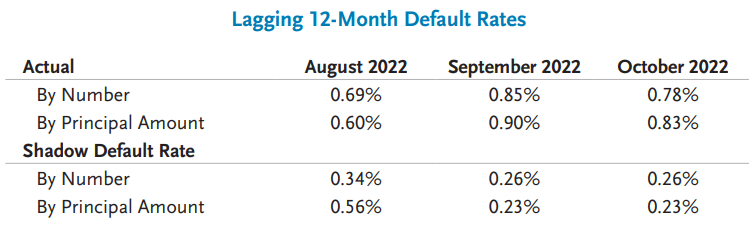

This way, in their +30-year existence, CLOs have exhibited meager default rates. Notably, zero of the CLOs initially rated investment grade have defaulted over the last decade, according to S&P Global Ratings. Out of ~11,400 CLO securities across the credit rating spectrum, only five portions have defaulted as of Jan. 1, 2022. Through this bear market, CLOs continue to maintain meager default rates. Source.

TCW

Today, we discuss the preferred security issued by OXLC, one of our favorite CLO CEF, Oxford Lane Capital Corp. OXLCM Term-Preferred Shares are currently at a slight discount to NAV and have a mandatory redemption date – of June 30, 2024.

Author’s calculation

As described earlier, CLOs are highly regulated, but OXLCM offers additional protection for shareholders. If the fund’s asset coverage ratio drops below 200%, it must redeem a portion of the preferred stock to meet that coverage requirement.

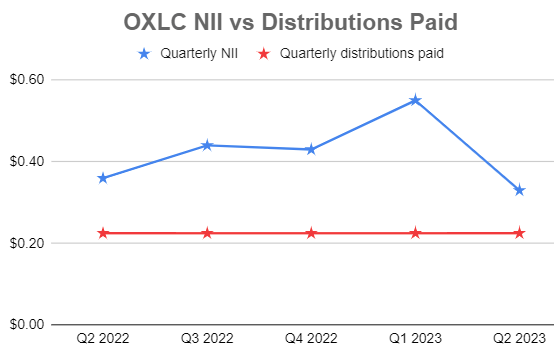

CEF Net Investment Income (“NII”) is calculated after subtracting preferred distributions. Looking at several quarters of financial data, we can see that the common unit distributions are well covered by NII, indicating adequate safety for preferred shareholder income. Notably, OXLCM is a cumulative preferred that requires any missed distribution to be paid in full before common distributions can be made.

Author’s calculation

OXLCM is a monthly pay preferred that pays $0.140625/share on the last business day of every month. This calculates to a 6.9% annual yield and a YTM of 8.1%. CLOs have shown resilient performance through multiple economic downturns and are closely regulated instruments. Their floating-rate coupon makes them a natural inflation hedge, and OXLC is well-positioned in this rising rate environment. Its preferred offers a safe and stable income opportunity for risk-averse investors.

Pick #2: Agency mREIT Preferreds, Yield 9%

Residential mortgage REITs invest primarily in residential mortgage-backed securities (“MBS”). These instruments are issued and guaranteed by U.S. Government-sponsored entities, such as Fannie Mae, Freddie Mac, or Ginnie Mae.

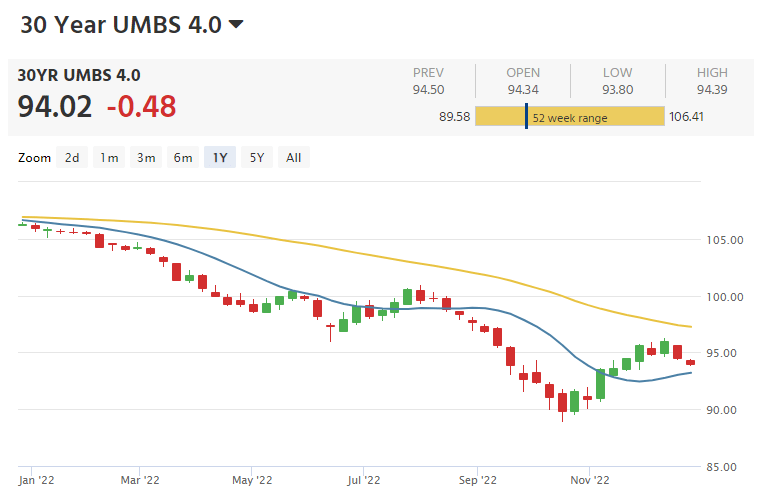

Let’s begin by looking at the 4% coupon Uniform Mortgage Backed Securities (“UMBS”) prices in the past ten years. While they have exhibited movement around the par value, the drop we see in the current market has been exceptional and will go down in history as one of the steepest declines in MBS.

UMBS 30 Year 4.0 – MBS

As with many large declines in the market, they are followed by large rallies. This is especially true for MBS, since the mortgages are guaranteed. When these mortgages are repaid, the holder will receive the par value ($100) regardless of what price the bonds are selling at. Mortgage bonds are close to the cheapest since the financial crisis, and leading institutions like PIMCO, DoubleLine Capital, Vanguard Group, and Morgan Stanley Investment Management are piling into the debt from these government-backed entities.

Mortgage real estate investment trusts (“REITs”) generally are sensitive to interest rate spreads, and their operating leverage being so high can shake the average investor out of their comfort zone with significant volatility in book value and the common shares. mREIT preferred securities, on the other hand, present attractive discounted opportunities with a significantly lower risk profile.

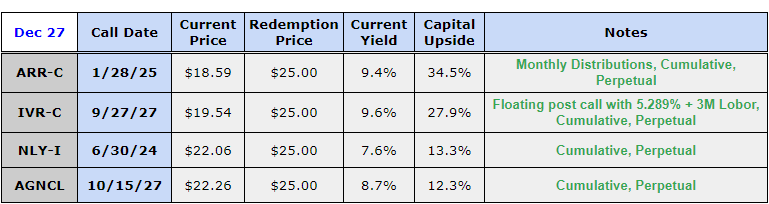

Below are a set of safe residential mREIT preferreds from Annaly Capital (NLY.PI), AGNC Investment Corp (AGNCL), Invesco Mortgage Capital Inc (IVR.PC), and ARMOUR Residential REIT (ARR.PC) that you can buy and lock in a rich income stream.

Author’s calculations

Mortgage REIT preferreds are excellent income investments for more risk-averse investors to benefit from the massive mispricing in MBS. Investors can collect up to ~9% yields at these prices and get set for substantial capital upside upon redemption. These preferreds are cumulative, providing much-needed shareholder protection and increasing the safety of your income prospects.

Shutterstock

Conclusion

Over three-quarters of a century ago, people used to work their entire adult life for a secure retirement with a reliable pension income. Today, very few organizations pay a pension, and you are on your own when securing your retirement.

We at HDO believe in securing our retirement by investing in cash-producing assets. Our objective is to organize portfolios to generate dependable paychecks with minimal intervention. During your working years, you can use this strategy to grow your portfolio through dividend reinvestments. You can use the proceeds towards your living and lifestyle expenses during your retirement. With a well-diversified dividend portfolio, there is no need to invest and sit with hope and prayer that your stocks go up; you can easily predict how much you will make at the end of the month.

There are several commodities we interact with in our daily lives. Oil, gold, silver, money (currency), and time…… Yes, time is the most valuable and finite commodity in this universe, and you must manage it wisely. Unlike all other commodities, you can’t exchange anything to get one extra nanosecond for yourself. Invest for income so you can invest your time in things that give you joy. We have two discounted preferred picks with up to 9% yields to get you started.

Be the first to comment