cgbaldauf/iStock via Getty Images

Workhorse Group (NASDAQ:WKHS) is quickly falling into the group of EV stocks overhyped during the SPAC flood of 2020 that failed to deliver on their promises. The company has made some progress on manufacturing EV vans, but the progress isn’t enough to save investors before dilution hits. My investment thesis remains Neutral on the stock due to the price dipping below $1.50 possibly limiting the downside.

Source: FinViz

Slow Deliveries

A lot of the EV firms are making a race towards producing and delivering new electric models to customers. Companies like Workhorse surged on the promise to start producing EV vans in volume over the next year or so, but the time has flown by, and the company is struggling some 18 months later to get the vehicles manufactured and out the door.

For Q3, Workhorse reported revenues of only $1.55 million and guided to full-year revenues of $15 to $25 million. The company cut the range of delivered vans for the year to between 100 and 200 based on supply chain disruptions. The previous target was up to 250 EVs.

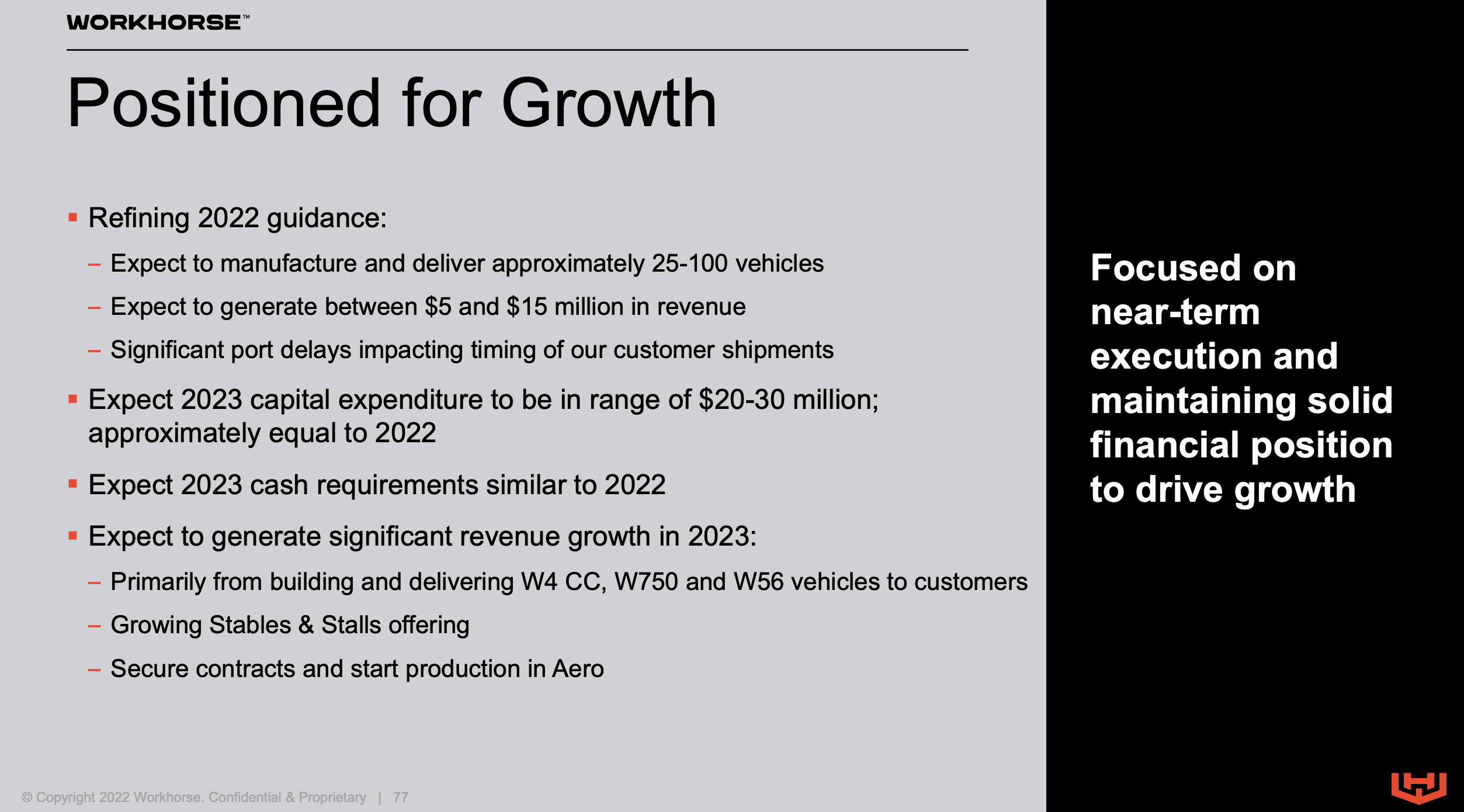

During Q3’22, Workhorse built 10 W4 CC vehicles and had built another 13 during Q4 by the Q3’22 report on November 8. At Analyst Day 2022, Workhorse further lowered the 2022 target to only 25 to 100 vehicles, producing revenues between $5 to $15 million for the year.

The company apparently ran into port delays, but the biggest question for investors is how much Workhorse can ramp up sales when unable to get a limited number of cab chassis on time. The revenue figure for Q4 could be as low as $3.5 million.

Considering Workhorse generated similar revenue levels back in 2021 selling the C1000 vans, further delays just crush the stock. The new executive team has to now deliver consistent and material vehicle growth after announcing the end of the C1000 program only days after meeting with analysts.

At the 2022 Analyst Day, Workhorse didn’t provide financial targets for 2023 despite the year starting weeks after the presentation. The lack of guidance won’t attract investors in the short term.

Source: Workhorse ’22 Analyst Day presentation

Dilution On The Way

The company has a whole host of new vehicle launches in the next year, highlighting a lot of the problems with the industry. Workhorse has a cash balance of only $120 million and monthly net cash requirements of $9 million.

The cash will quickly disappear, requiring the company to access the $175 million ATM offering while the stock trades below $2. Workhorse will end up diluting investors at a low price while attempting to build multiple vehicles plus drones without ever delivering a profitable vehicle to customers.

The W4 CC is ready for production now and the W750 step vans will be available just in January. Workhorse should have more projections for these vehicle sales in the next year.

Source: Workhorse ’22 Analyst Day presentation

If this isn’t enough, Workhorse plans to launch the W56 van in the next year. The prototypes are in the works, with plans for 12 vehicles built this year. The company will launch the van in Q3’23 placing 3 different vehicles in production going into Q4 next year, after ending the C1000 program. The company is also working on drones and the ‘Stables & Stalls’ business platform in order to service the EVs for small businesses.

The EV sector is definitely interesting and worth watching. If Workhorse does improve production in 2023 with multiple EVs having strong orders, investors can revisit the stock knowing share dilution in the next year will likely constrain any rally in the stock.

Takeaway

The key investor takeaway is that Workhorse hasn’t made enough progress to warrant an investment here. The company has a lot of irons in the fire that could eventually work out into a valuable business, but management has a ton of work to accomplish before shareholders would ever be rewarded.

If you’d like to learn more about how to best position yourself in undervalued stocks mispriced by the market heading into a 2023 Fed pause, consider joining Out Fox The Street.

The service offers model portfolios, daily updates, trade alerts, and real-time chat. Sign up now for a risk-free, 2-week trial to start finding the next stock with the potential to generate excessive returns in the next few years without taking on the outsized risk of high-flying stocks.

Be the first to comment