MarsBars

It pays to build a basket of dividend payers, as not all stocks in a portfolio have to be high yielders. For example, there are a number of 3%+ yielding stocks that have strong dividend growth track records and durable business models, like Corning (GLW) and Comcast (CMCSA), both of which I like.

This brings me to Bank of New York Mellon (NYSE:BK), which remains attractively valued with a low PE, despite having a storied history and strong business model. BK stock has done well since I last visited it back in October, giving investors a 16% total return since then, far surpassing the 5% return of the S&P 500 (SPY) over the same timeframe.

However, as shown below, BK is still well off its 52-week high of $65, achieved earlier this year. In this article, I highlight why BK remains a solid bargain for value-minded investors.

BK Stock (Seeking Alpha)

Why BK?

BNY Mellon is a global financial services company that provides wealth management and investment services to clients in 35 countries and over 100 markets. It’s one of the oldest banks in the world, having been around for over two centuries. It’s also the largest custody bank, with $42 trillion in assets under custody and/or administration, and has $1.8 trillion in assets under management.

One of BK’s key advantages is its wide reaching investment services, which include corporate trustee and American Depository Receipts on foreign shares, such as that of the popular tobacco stock, British American Tobacco (BTI). Having scale serves as a competitive advantage for BK, as this “network effect” enables it to spread fixed costs over a wide asset base. This, combined with customer switching costs, serves as a barrier to entry.

Meanwhile, BK appears to be doing fine, as its revenue was up by 6% YoY, or 5% excluding impact of one-time items during the third quarter.. This was driven in part by loan growth of 11% YoY, and higher interest rates, with net interest revenue rising by an impressive 44% YoY. Plus, expenses were kept in check as they were up by just 4% YoY excluding one-time effects.

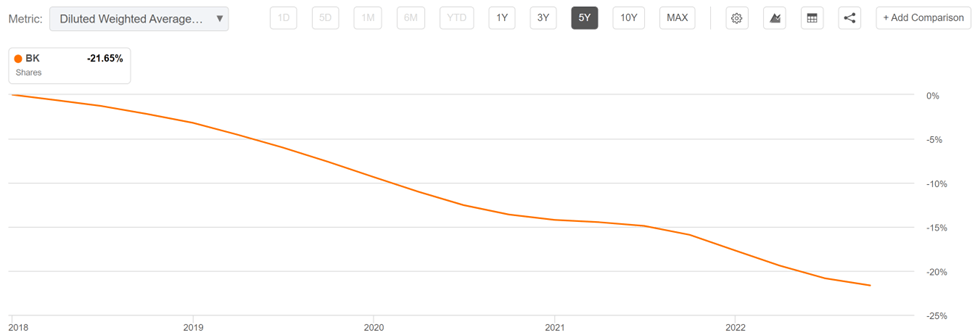

Importantly, BK exhibits the hallmarks of a mature company that returns a substantial amount of free cash flow to shareholders. This is reflected by the $0.3 billion worth of share buybacks during Q3 alone. As shown below, BK has retired 22% of its share count over the past 5 years alone.

BK Shares Outstanding (Seeking Alpha)

Plus, true to form, BK raised its dividend last quarter by 9% to $0.37 per quarter. The dividend is well covered by a 32% payout ratio, and comes with a 10.6% 5-year CAGR and 12 years of consecutive growth. Notably, BK also carries capital reserves, with a CET1 ratio of 10.0%, well in excess of the 4.5% requirement by the Federal Reserve for large U.S. banks.

Looking forward, BK’s new CEO Robin Vince expressed his intent on improving pretax margins over the medium term through operating efficiencies. BK also got a recent win, being appointed to provide both front and back office support for the large European-based global asset manager, Aviva Investors.

Moreover, with all of the turmoil and meltdown of the once-giant crypto custodian FTX, BK appears to be well positioned to serve as a digital asset custodian, considering its long-standing history and reputation, following its recent entry into the space. This was highlighted by the new CEO during the recent conference call:

And finally, following the formation of our digital assets unit in 2021, we are now live with our digital asset custody platform in the U.S. To this point, we continue to see significant institutional demand for resilient, scalable financial infrastructure built to accommodate both traditional and digital assets.

And we see digital asset custody as an important foundational capability for the future of financial markets as blockchain technology allows for tokenization of all kinds of assets and currencies. But just to be clear, we did not invest in this space just for the purpose of custodying crypto. We see this as the beginning of a much broader journey.

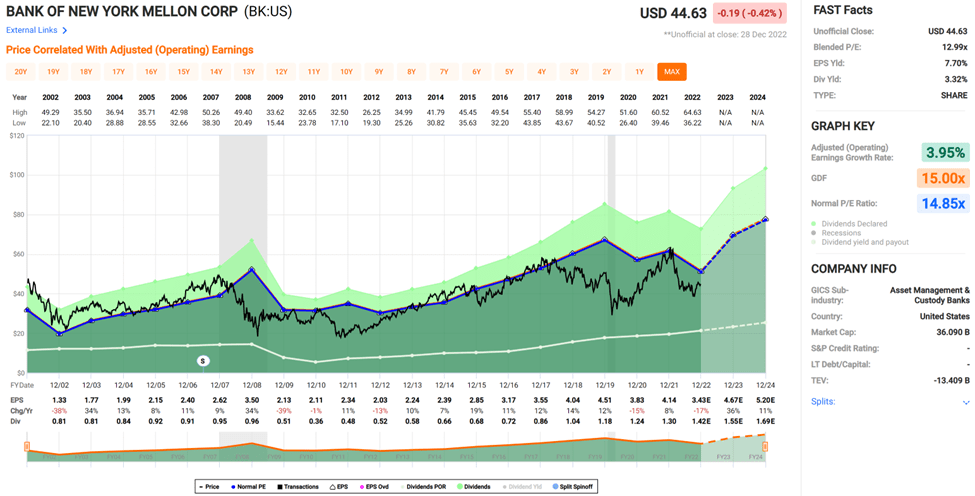

Lastly, I continue to find value in BK at the current price of $44.63 with a forward PE of just 10.1, sitting well below its normal PE of 14.9. Analysts estimate 6% to 9% annual EPS growth over the next two years and have a consensus Buy rating with a conservative average price target of $50, which still translates to a potential total return in the mid-teens over the next year.

BK Valuation (FAST Graphs)

Investor Takeaway

BNY Mellon continues to demonstrate steady operating fundamentals, with loan growth and higher interest revenue. Its scale and diversification give it an advantage over competitors, as does its long track record of returning cash to shareholders.

Looking forward, it’s well positioned to leverage its reputation and capitalize off the recent FTX debacle with its entry into the digital asset custodian space. Lastly, BK remains attractive priced, giving investors potential for strong returns going forward.

Be the first to comment