Joe Raedle

The past year has been particularly challenging. But not every company has fared the same way. One firm that has been completely decimated over the past year or so is specialty retailer Bed Bath & Beyond (NASDAQ:BBBY). A combination of factors, including the pandemic, management’s decision to engage in certain divestitures, ill-timed share buybacks, inflationary pressures, and more, have all coalesced to create the perfect storm for the business. It’s because of these factors that shares of the business are down roughly 92% over the past year. Some investors might now be worried that the end for the company is nigh. There is most certainly a chance of this kind of situation playing out. Even if the firm does survive, its debt situation is bad enough to warrant a high probability of downside than of upside from here.

Major changes and challenges alike

Back in 2019, the management team at Bed Bath & Beyond decided to significantly reinvent the business. This led to, amongst other things, the divestiture of five non-core banners under the company’s umbrella during the 2020 fiscal year alone. Collectively, these sales, which included One Kings Lane, PeronalizationMall.com, Linen Holdings, Christmas Tree Shops, and Cost Plus World Market, resulted in $534 million in net proceeds for the business. Management’s primary idea behind this is that the company would be able to focus more on its core operations centered around the company’s position as an omnichannel retailer for home, baby, beauty, and wellness products, amongst other things. It would also allow the company to invest more in its Owned Brands, while also focusing on share buybacks and debt reduction.

All of this sounds great. But unfortunately, fate has had other plans in store for the business. Although the company has continued to invest in the brands in its own portfolio, even launching 8 new brands during the 2021 fiscal year alone, most of the cash it generated seems to have gone to the repurchase of additional stock. In 2021 alone, the company bought back $574.9 million worth of shares. This was followed up by another $40.4 million worth of stock buybacks in the first six months of the company’s 2022 fiscal year. Bed Bath & Beyond is no stranger to share repurchases. Since initially buying back its own stock in December of 2004, the company has repurchased $11.73 billion worth of shares. In my opinion, it’s unfortunate that the company was not wiser with the use of its funds. If it had been, it likely would be in a far better position today.

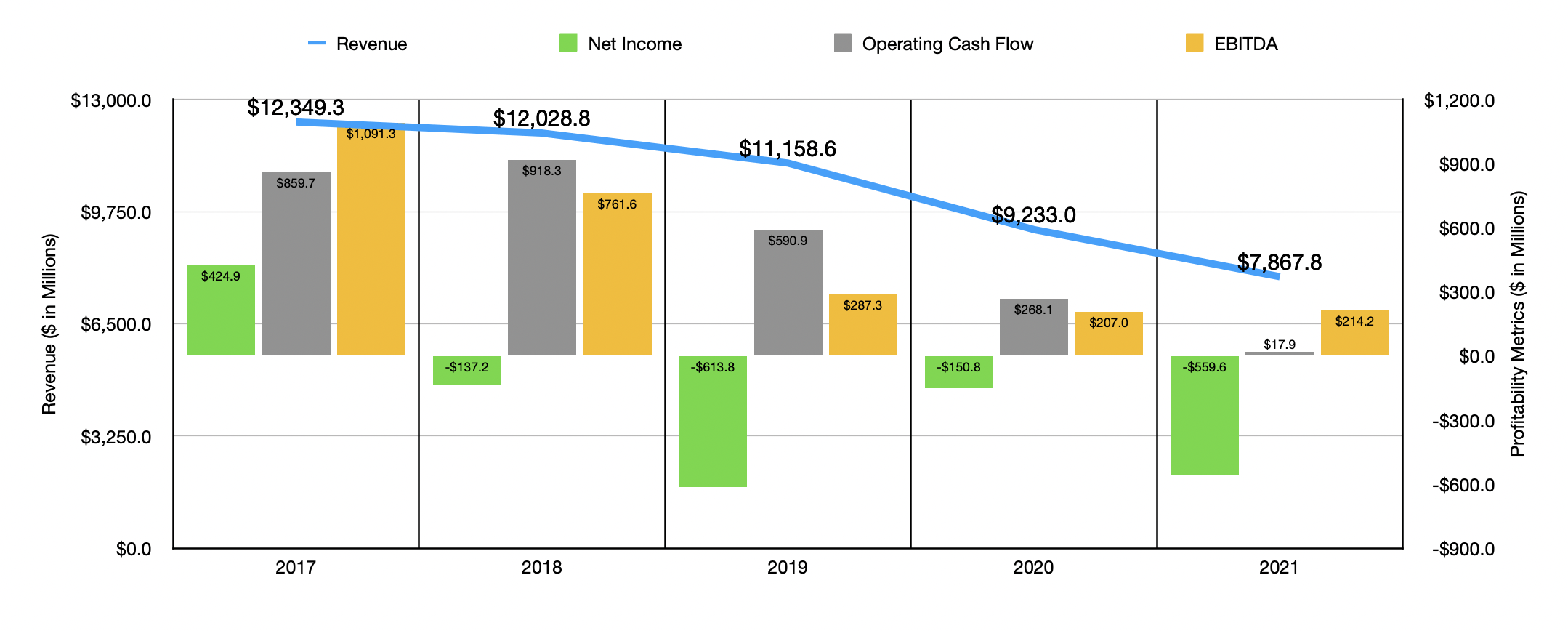

Author – SEC EDGAR Data

The trouble for the business really did begin in 2021. Sales for the year came in at $7.87 billion. That was down significantly compared to the $9.23 billion generated only one year earlier. And it was also down from the $11.16 billion generated in 2020. To be fair, most of this decline came from the aforementioned divestitures that the company engaged in. Removing these from the equation as if they had never existed at the company to begin with, we would have actually seen sales in 2021 drop by only about 1%, with a mixture of store closures, reduced traffic, and supply chain disruptions all negatively affecting the company’s top line. Unfortunately, this 1% adjusted sales decline also brought with it significant profitability issues. A plunge in the company’s gross profit margin from 33.8% in 2021 to 31.6%, driven by markdown activity associated with inventory being removed in connection with the launches of new brands under its own portfolio, combined with inflation and supply chain-related costs, resulted in the company incurring a net loss in 2021 of $559.6 million. This is compared to the $150.8 million loss experienced in 2020. Other profitability metrics also showed signs of worsening. Operating cash flow went from $268.1 million to $17.9 million in just one year. If we adjust for changes in working capital, it would have been even worse, dropping from $421.4 million to negative $58.4 million. Only EBITDA showed some improvement, inching up from $207 million to $214.2 million.

Fast forward to the present day, and the company is still experiencing a great deal of pain. Unlike in the prior year, the pain seen in 2022 was largely driven by weakening demand for the company’s offerings. Sales dropped from $3.94 billion to $2.90 billion in the first half of the current fiscal year, driven almost entirely by a plunge in comparable store sales as continued downward trends in customer traffic that was reflective of weaker consumer spending patterns and demand significantly harmed the company. A lack of inventory availability and assortment in key product areas, as well as the impact associated with the closure of certain stores in 2021, all played a role in the company’s troubles as well. This drop in revenue brought with it horrible profitability figures. The company went from generating a net loss of $124.1 million in the first two quarters of 2021 to generating a net loss of $723.8 million the same time this year. Operating cash flow went from $46 million to negative $582.4 million, while the adjusted figure for this went from negative $0.8 million to negative $487 million. Even EBITDA took a beating, plunging from $171 million to negative $392 million.

Author – SEC EDGAR Data

In response to these troubles, the company has embarked on some major initiatives. In August, for instance, the company announced planned workforce reductions, with reductions across the company’s corporate operations and in its supply chain expected to be around 20%. The company’s expectation was that these cost reductions would reduce total selling, general, and administrative costs for the company for the 2022 fiscal year by $250 million. Some of these savings will likely come from the company’s decision to close around 150 stores for the year as well. On top of this, the company also cut back its capital expenditure budget by $150 million. It’s unclear exactly what the long-term impact of all of this would be. But between these cost-cutting initiatives and the expectation that comparable store sales should improve in the second half of this year such that total comparable store sales for 2022 should only be down in the 20% range, the expectation is that total operating cash flow for this year should be roughly break even.

In addition to seeing profits and cash flows suffer, the company also deals with the unfortunate fact that, as of the end of its latest quarter, it had $1.59 billion in net debt on its books. This compares to the $288.2 million market capitalization of the business as of this writing. Although the company is currently in compliance with all of its covenants, that may not remain the case for long if current conditions persist. Understanding that this is now an issue, the company has made some interesting moves. At the end of August, the company issued $75 million worth of shares. They also, on October 28th, increased their at-the-market share plan by $150 million. Unfortunately, this kind of strategy comes at the cost of significant dilution for shareholders. As of the end of August, for instance, the company had 80.4 million shares outstanding. Today, that number stands at 117.3 million (which includes somewhere around 22.5 million shares from its two ATM programs combined). To put this in context, in just a few months, shareholders have been diluted by 68.5%. That might be one of the reasons why shares have taken such a beating.

The company is also engaged in some interesting debt initiatives. Some of the increase in shares outstanding, for instance, came in response to the business swapping out 14.39 million shares of stock in exchange for $51.1 million worth of debt. This also occurred at a time when the company initiated an offer to exchange certain nearer-term debt in exchange for debt that has radically more generous terms for the company. The current offers have been extended multiple times now. At present, shareholders of senior notes that come due in 2024 and that bear an annual interest rate of 3.749%, have the opportunity to exchange those notes for either senior second lean secured non-convertible notes that come due in 2027 and that carry a 3.693% or in exchange for senior second lien secured convertible notes due in 2027 that have a much higher 8.821% interest rate. The big difference between the two is that the lower-rate notes will see an exchange dollar for dollar with the notes that the company is seeking to take off the market, while the higher interest-rate notes only carry $410 in par value for every $1,000 that the new notes have. Unless there are specific bets that investors are making or specific tax implications that they have, I don’t see the choice of notes here varying significantly. This is because, after the one-year anniversary of the issuance of the notes, the lower interest ones can be redeemed by the company at 40% of par value.

Bed Bath & Beyond

For investors who have the 4.915% senior notes, the offer involves senior third lien secured convertible notes that carry a 12% annual interest rate and that come due in 2029. The same kind of offer is being made for the 5.165% senior notes that are due in 2044. In both cases, these are being done at $217.50 for every $1,000 of par value that the senior notes have. Perhaps unsurprisingly, there have not been many takers on these note issuances. But this doesn’t mean the company is not getting some benefit. As of this writing, the company has gotten holders of $158.88 million worth of senior notes to pledge their units in exchange for the new notes. By my estimate, this should save the company around $3 million in interest expense annually and should reduce overall debt for the firm by as much as $116.76 million. That’s still only a drop in the bucket. But when added to the fact that the company also unlocked an extra $500 million in new financing under its debt agreements, including $375 million under a FILO facility, the hope is that the firm can ride out these difficult times without taking too much more pain.

Because the company should be, at best, cash flow neutral for the current fiscal year and will certainly generate significant net losses, it really is impractical to try and value the firm. Clearly, the divestitures management made over the past couple of years means that the company will certainly not grow back to the kind of revenue and profits that it generated in prior years. But even generating operating cash flow that is one-third of what the company achieved during its 2020 fiscal year would still imply that the company is trading at a price to operating cash flow multiple with only 2.1. This excludes recent ATM offering impacts. Unfortunately, a 50% reduction in its EBITDA from that year would imply an EV to EBITDA multiple of around 17.3, meaning that shares might still be considered quite pricey in the grand scheme of things, particularly when it comes to a firm that is operationally not the most stable.

Takeaway

Based on all the data provided, I will say that I find what Bed Bath & Beyond is going through to be rather interesting. For investors who like to live dangerously with their money, it is possible that a nice recovery in its core operations will lead to meaningful upside. But even with recent moves, shares would be rather pricey should we see anything other than a full recovery that almost certainly won’t happen because of said structural changes. While I can appreciate investors who might want to get in on this and I wouldn’t be surprised if the end result does end up being favorable, I personally view this as a far riskier play than is warranted. As such, until I see further clarity, I cannot rate the business any higher than a ‘sell’ at this time.

Be the first to comment