Dilok Klaisataporn

Introduction

The start of 2022 was a time that CVR Partners (NYSE:UAN) will likely never forget, as fertilizer prices surged to levels never thought possible after Russia attacked Ukraine, thereby setting off a chain of reactions still impacting the world today. By the middle of the year, it seemed timely to double down with their fundamentals up but their unit price down, as my previous article highlighted. Even though their unit price subsequently climbed higher, the latest wave of selling across the market sees it back around this same level once again. Despite this bumpy ride, management continued taking prudent measures to line everything up and thus when looking ahead, their year of work is coming together in 2023.

Coverage Summary & Ratings

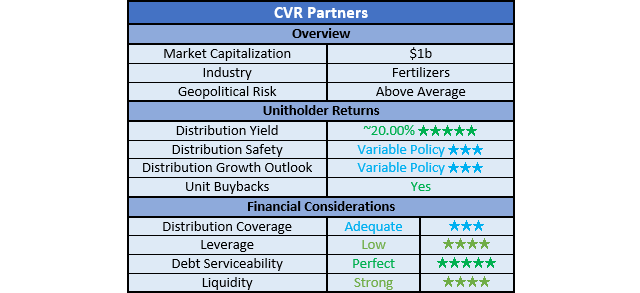

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

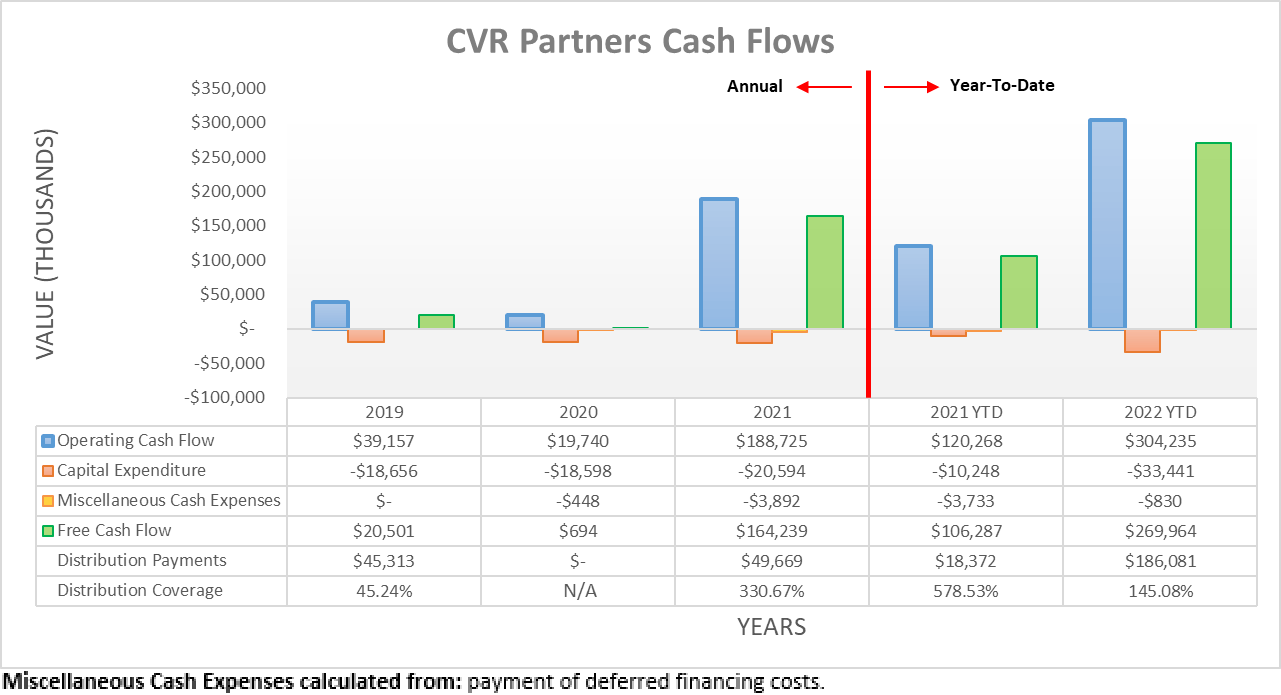

Following their record-setting operating cash flow during the first quarter of 2022 on the back of booming operating conditions, their subsequent results during the second and third quarters have continued powering onwards. As a result, this now sees their operating cash flow rising to $304.2m during the first nine months of 2022. Whilst this is unsurprisingly more than twice their previous result of $120.3m during the first nine months of 2021, it clearly represents a slowdown sequentially versus their result of $166.9m during the first quarter of 2022 alone.

Author

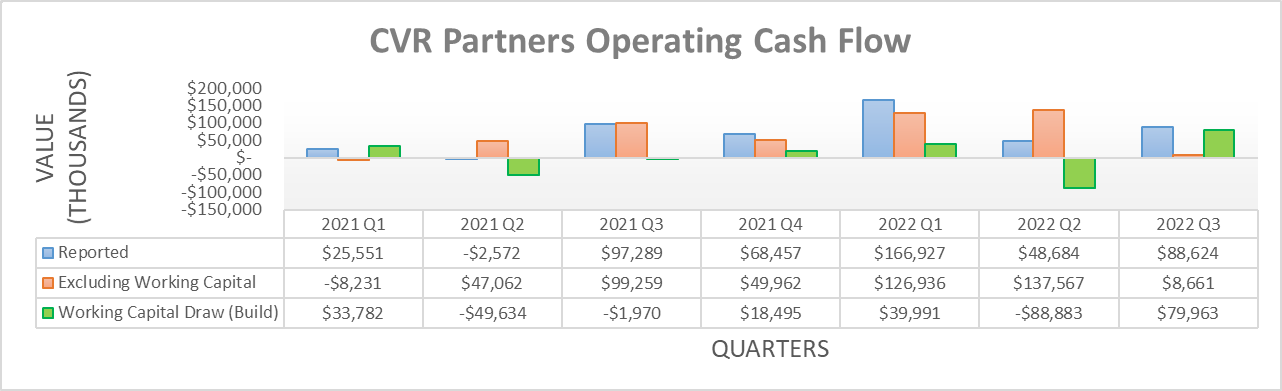

This dynamic is more visible when viewing their operating cash flow on a quarterly basis, as their results during the second and third quarters dropped to $48.7m and $86.6m respectively, which were down significantly versus their first quarter result. Thankfully, this does not mean the good days are in the past because the former two quarters were each skewed by different short-term impacts and operational events.

In the case of the second quarter of 2022, they endured an abnormally large working capital build of $88.9m that hindered their reported operating cash flow. If excluded, their underlying result surges to $137.6m and thus, it actually surpasses their previous equivalent result of $126.9m during the first quarter.

Whereas in the case of the third quarter of 2022, this abnormally large working capital build reversed into a similar sized draw of $80m that had the opposite effect, thereby boosting their reported operating cash flow. If excluded, their underlying result plunges to only a mere $8.7m, which is nearly wiped out. Whilst not ideal, fear not because this stems from the completion of maintenance work at their facilities, which heavily impacted their production. Due to this interruption, their ammonia available for sale fell to only 36,000 net tons versus 65,000 net tons one year prior during the third quarter of 2021, as per their third quarter of 2022 results announcement. When half of sales volume is shaved away and costs obviously rise in conjunction with the associated maintenance work, it is not surprising to see their underlying operating cash flow was almost completely wiped out.

Since their maintenance work is now completed, the fourth quarter of 2022 should not see impacts of this magnitude and therefore, their quarterly distributions should bounce back from the depressed $1.77 per unit attributable to the third quarter. Even though this was down massively versus earlier quarters, it was nevertheless positive to see management returning as much cash as possible after achieving their debt target earlier in the first quarter, as expected when conducting my previous analysis. Plus, it should not be forgotten the second quarter saw a massive quarterly distribution of $10.05 per unit that was a record for their partnership, by a wide margin. Furthermore, if annualizing their most recent depressed quarterly distribution, it still produces a high yield of slightly over 7% against their current unit price of $96.82.

Whilst worthwhile to understand, the past is the past and, as always, their outlook for 2023 is far more important. Even though the inherent volatility of their commodity-based partnership precludes any exact earnings guidance, at least they have no further maintenance work planned and excitingly, their facilities should now run at higher utilization rates going forwards, as per the commentary from management included below.

“During the turnarounds we completed an extensive amount of work that should allow facilities to run higher utilization rates than they have over the past year. We currently do not anticipate any additional planned turnaround activity until the fall of 2024.”

-CVR Partners Q3 2022 Conference Call.

Whilst fertilizer price indexes have eased since their record-setting levels earlier in 2022, they are still historically elevated given the game-changer following the Russia-Ukraine war. As my previous article and earlier article discussed in detail, this otherwise tragic event brought about structural changes to the fertilizer industry, not only directly relating to Russian and Ukrainian exports but also European production in light of the resulting natural gas crisis. Furthermore, their generalized sales guidance heading into early 2023 is promising with not only strong demand but also, equally as strong pricing versus 2022, as per the commentary from management included below.

“Looking ahead, we believe the strong market for nitrogen fertilizers will persist through 2023 as a result of continued tight market conditions globally…”

“We currently have sold forward product through year-end 2022 and into the first quarter of 2023. Year-over-year product prices are expected to be higher for the next couple of quarters, but pricing for the spring of 2023 likely to be comparable to the high seen in the spring of 2022.”

-CVR Partners Q3 2022 Conference Call (previously linked).

Recession or not, this strong outlook should continue being underpinned by the structural changes from Eastern Europe as well as the never-ending basic human need for food that ultimately drives fertilizer demand. Despite not necessarily knowing exactly where their financial performance will land, this nevertheless points towards another strong year ahead that, in turn, means a very high 10% distribution yield should continue, if not even more, as they no longer face maintenance work nor debt repayments.

The other piece of interesting news is their parent company, CVR Energy (CVI) potentially spinning off their fertilizer business segment, which is obviously, CVR Partners. In case any new investors are uncertain, this would not impact their existing investments into the latter, as their proposed plan centers on creating a newly listed company serving as a holding company for their ownership in CVR Partners along with their accompanying General Partner interest. Oddly, this would effectively see two listings for the same underlying fertilizer business, CVR Partners. Whether this messy proposal moves forwards is unknown, but if forthcoming, I would not be surprised to see the two listings eventually rolled together into one company down the track for simplification and cost savings.

Author

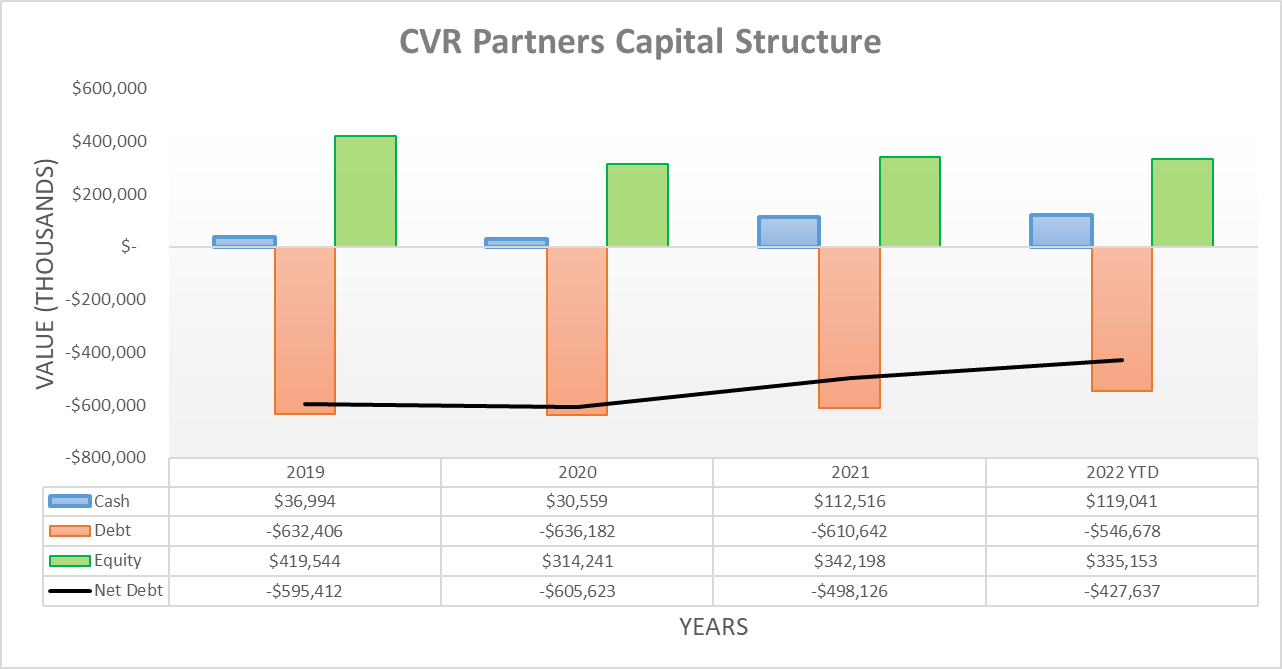

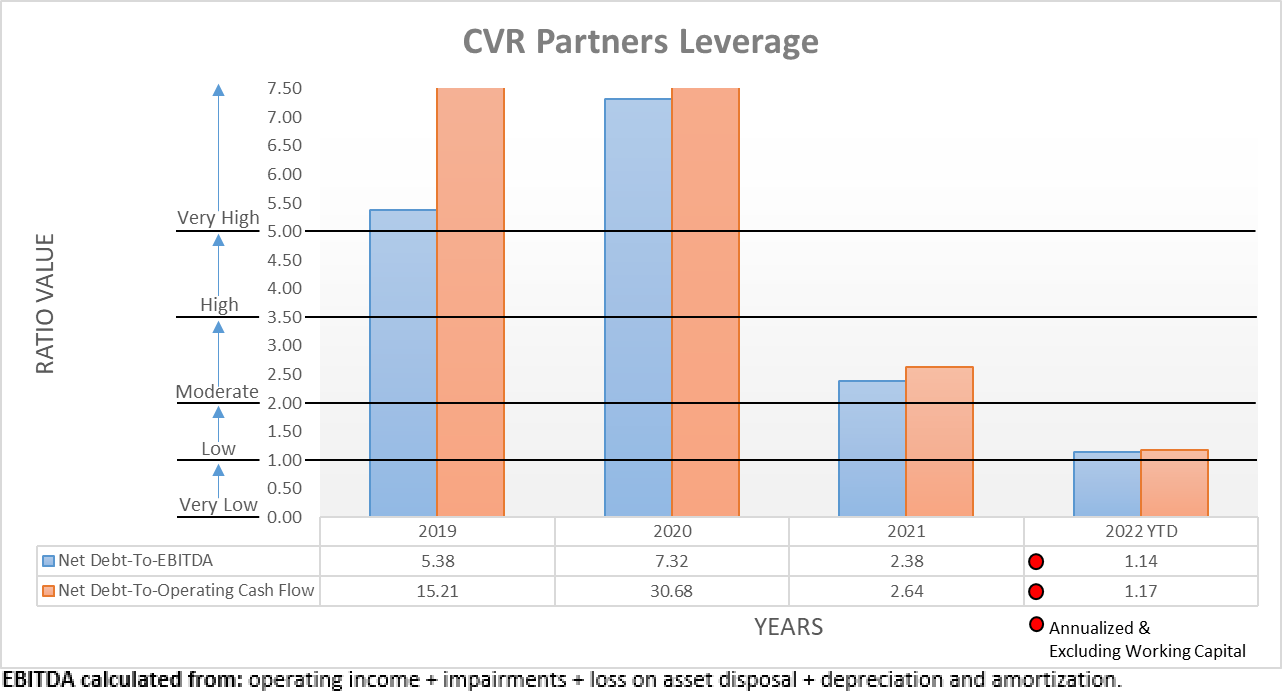

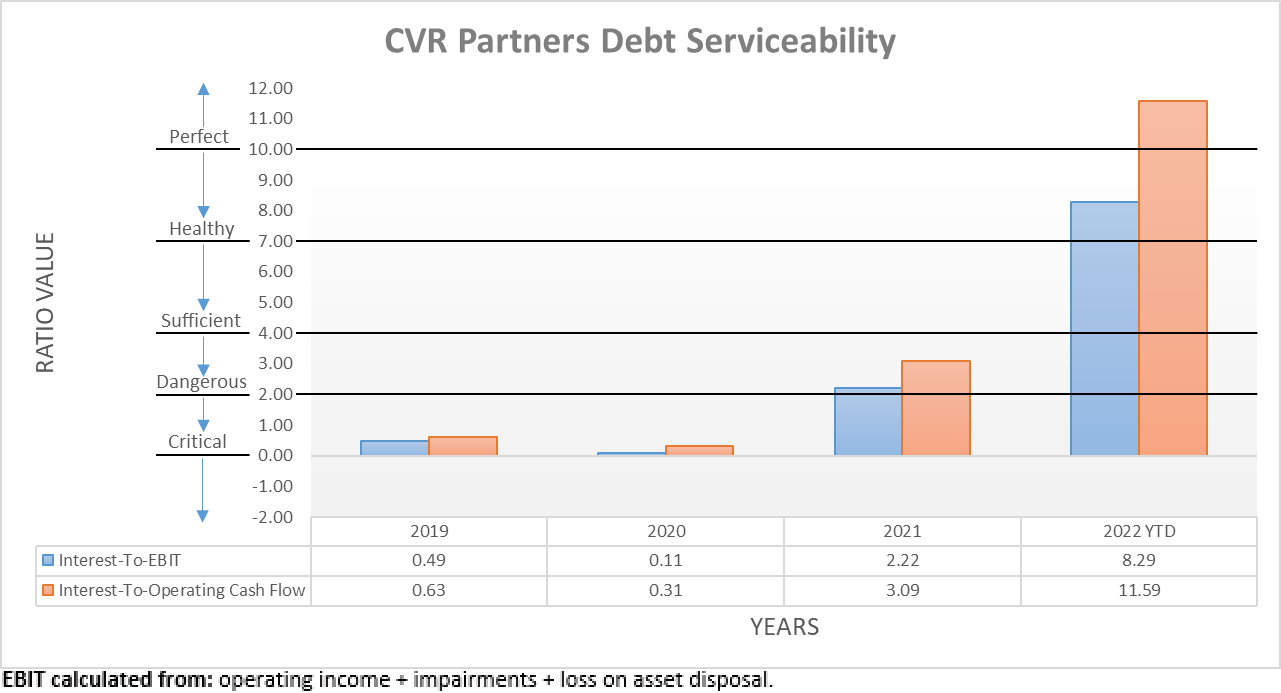

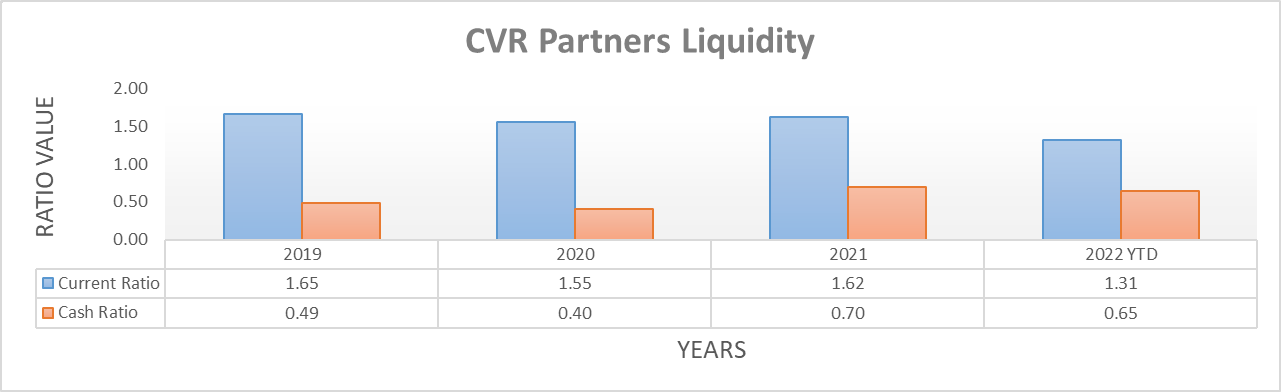

After hitting their debt target during the first quarter of 2022, they were free to return as much cash as they wished during the second and third quarters and as we know, they certainly did not ignore the opportunity. As a result, their net debt finished the third quarter at $427.6m and thus very similar to its previous level of $409.1m following the first quarter. Since this only represents an immaterial difference, it would be redundant to reassess their leverage or debt serviceability in detail, especially as their outlook for 2023 was the primary focus of this analysis. Additionally, as their cash balance of $119m following the third quarter of 2022 is fairly close to its previous balance of $137.3m following the first quarter, the same can also be said for their liquidity.

The three relevant graphs are still included below to provide context for any new readers that, as expected, show their financial position remains solid. On the leverage front, it is firmly within the low territory, with their respective net debt-to-EBITDA and net debt-to-operating cash flow at 1.14 and 1.17. Meanwhile, their debt serviceability is perfect with interest coverage of 8.29 and 11.59 when compared against their EBIT and operating cash flow, respectively. Elsewhere, their liquidity remains strong, with a current ratio of 1.31 and an accompanying cash ratio of 0.65. If interested in further details regarding these topics, please refer to my previously linked article.

Author Author Author

Conclusion

Notwithstanding the bumpy third quarter of 2022, management continued taking prudent measures during the year to line everything up heading into 2023 and beyond. Firstly, their expensive debt was addressed and subsequently, they endured the short-term pain to complete maintenance work that should now see their facilities more productive and able to operate throughout 2023 without any hindrance. When wrapped together, their year of work is coming together in 2023 and given their continued prospects for a double-digit distribution yield on the back of a strong fertilizer market, I unsurprisingly believe that maintaining my strong buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from CVR Partners’ SEC Filings, all calculated figures were performed by the author.

Be the first to comment