RomoloTavani/iStock via Getty Images

Right now is a great time to buy triple net lease REITs in general. With interest rates and inflation rising, investors are fleeing the sector since it is often closely linked to bonds. Given the lengthy leases, very conservative contract structure, and low annual rent escalations, triple net leases are typically viewed as a hybrid between equity and fixed income.

While this view is not entirely inaccurate, we believe that triple net lease REITs offer compellingly attractive risk-reward right now for the following reasons:

(1) They have proven to be one of the most recession-proof equity investments. With expectations of a recession rising, these REITs are one of the best places to “hide.”

(2) If a recession does hit, inflation will likely fall considerably. This is already being priced in across several sectors, particularly energy and mining. This in turn should enable the Federal Reserve to reverse its course on interest rate hikes and therefore boost the multiples commanded by triple net lease REITs.

(3) The valuations offered by many REITs in the sector are historically cheap.

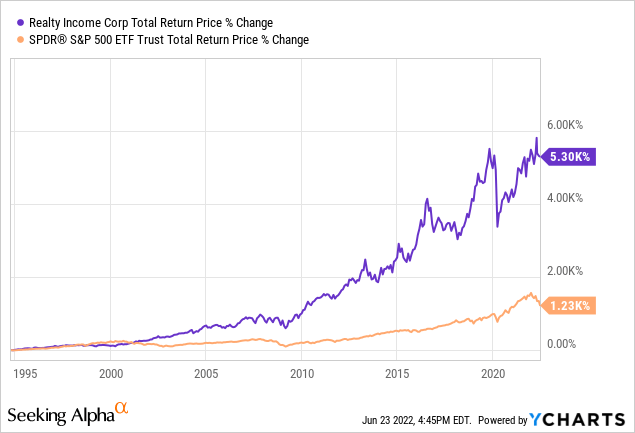

When selecting which triple net lease REITs to buy, many investors go for the premier blue chip pick by default: Realty Income Corporation (NYSE:O). It is certainly true that O has a tremendous long-term track record of compounding shareholder wealth and growing its monthly dividend, which has crushed the broader market (SPY) over time:

However, investing is about effectively positioning yourself to maximize risk-adjusted returns in the future, not about merely admiring the scene in the rearview mirror. As a result, we believe investors should invest in Agree Realty Corporation (NYSE:ADC) instead of O right now for the following reasons.

#1. Agree Realty Has A Better Portfolio Than Realty Income Does

The biggest reason why ADC has a better portfolio than O does is that it leads the triple net lease sector in exposure to investment grade tenants, with 67% of its ABR coming from them compared to just 44% of O’s ABR coming from investment grade tenants.

On top of that, ADC’s largest investment grade tenants are not only investment grade, but they are some of the strongest and most prosperous tenants in the retail industry today. For example, its largest tenant – representing a whopping 6.7% of total ABR – is Walmart (WMT), which boasts a stellar AA credit rating. Its number two tenant – representing 3.9% of total ABR – is Tractor Supply (TSCO), a company that has been generating massive shareholder returns, is growing rapidly, and boasts a solid BBB credit rating. Its third largest tenant – representing 3.8% of total ABR – is Dollar General (DG), a very recession resistant company that continues to put up solid growth numbers and has a solid BBB credit rating.

Their list of top tenants also includes the likes of TJX (TJX) (A credit rating), Kroger (KR) (BBB credit rating), Lowe’s (LOW) (BBB+ credit rating), and Home Depot (HD) (A credit rating). On top of that, 10.6% of its ABR comes from recession, pandemic, and ecommerce resistant grocery stores, its largest individual tenant type.

Even its unrated tenants include the likes of high quality private companies such as Chick-fil-A and Hobby Lobby, so the investment grade number actually understates the strength of its tenants.

On top of that, ADC also derives 14.3% of its ABR from ground leases. These leases are extremely conservative because the tenant is only leasing the land from ADC, but if the tenant defaults on the lease then ADC gets the building as well.

Clearly, ADC’s cash flow stream is very conservative.

In contrast, while O also has impressive grocery story exposure at 10.4%, it also has substantial exposure to riskier theaters (3.3% of total ABR), while WMT, TSCO, and DG only combine to generate 7% of its total ABR, less than half of what they contribute to ADC’s ABR. O also lacks the ground lease portfolio that ADC boasts, further reducing its relative strength.

#2. ADC Has A Stronger Growth Outlook Than O Does

In terms of growth, despite being far more conservative in its structuring, ADC also boasts a stronger near-term growth profile, partially due to its smaller size. This makes it easier for it to find acquisitions. In 2022, analysts expect ADC’s AFFO per share to increase by 10%, whereas they forecast O’s AFFO per share growth to come in at 8.6%. On a dividend per share level, ADC’s growth potential is even stronger, with analysts expecting its dividend per share to grow by 8.2% this year compared to O’s expected dividend per share growth rate of 4.6%.

This growth is not simply backloaded from a weak 2021, either. In 2021, ADC hiked its dividend by 8.3% and grew its AFFO per share by 9.7%. In contrast, O grew its dividend by a measly 1.4% and grew its AFFO per share by 5.9%.

Looking ahead, ADC is well-positioned to continue investing in growth acquisitions despite recent interest rate hikes as it has very low leverage and no meaningful debt maturities prior to 2028. On top of that, its credit facility gives it $1 billion in additional liquidity and does not expire until 2026 while the company issued a $341 million equity offering last December, positioning it well with roughly $1.5 billion in total liquidity to fund its expected acquisition volume of up to $1.3 billion in 2022. Given that this volume is near its acquisition volumes in recent years and that cap rates should only be increasing in the near term given where interest rates are headed, we expect ADC to be able to sustain its elevated growth rate for the foreseeable future.

In contrast, while O has been able to close massive deals like the acquisition of VEREIT on such accretive terms (10%+ accretive to AFFO per share immediately upon closure, with $45-$55 million in annual G&A synergies expected) and has a great balance sheet with substantial liquidity, given how massive it has become, it will be difficult for it to match ADC’s growth rate on a risk-adjusted basis.

#3. ADC Stock Offers A More Attractive Total Return Than O Does

Despite boasting a convincingly superior property portfolio and posting stronger growth rates than O, ADC’s stock currently trades at a slightly lower premium to NAV than O’s does based on analyst consensus estimates.

As a result, when combined with its meaningfully higher growth profile and 3.9% dividend yield, it offers a ~14% yield plus growth total return profile with less multiple contraction/portfolio risk than O. Meanwhile, O’s 4.35% dividend yield combines with its expected growth rate to ~13% yield plus growth total return potential with greater multiple contraction/portfolio risk.

Investor Takeaway

Both O and ADC look like very attractive buys to us right now and it is hard to argue against O’s track record. However, ADC has amassed a much more conservatively positioned portfolio than O has even as it is growing faster. On top of that, shares trade at a slightly better price to NAV than O’s shares do. Finally, for those that value O’s monthly dividend paychecks, ADC offers those too. As a result, we view ADC as the no-brainer pick between these two attractively priced REITs, though we like STORE Capital (STOR) the most in the sector at the moment.

Be the first to comment