guvendemir

Introduction

When last discussing the long-struggling NOV (NYSE:NOV), there were emerging green shoots that my previous article highlighted, along with the accompanying improved outlook for dividends. Thanks to their share price rallying almost 30% higher in the subsequent months, it now seems to be time to lock in some profits.

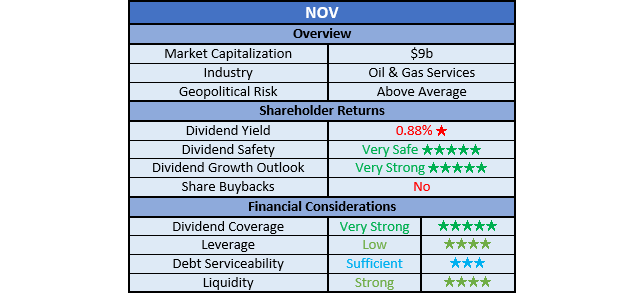

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

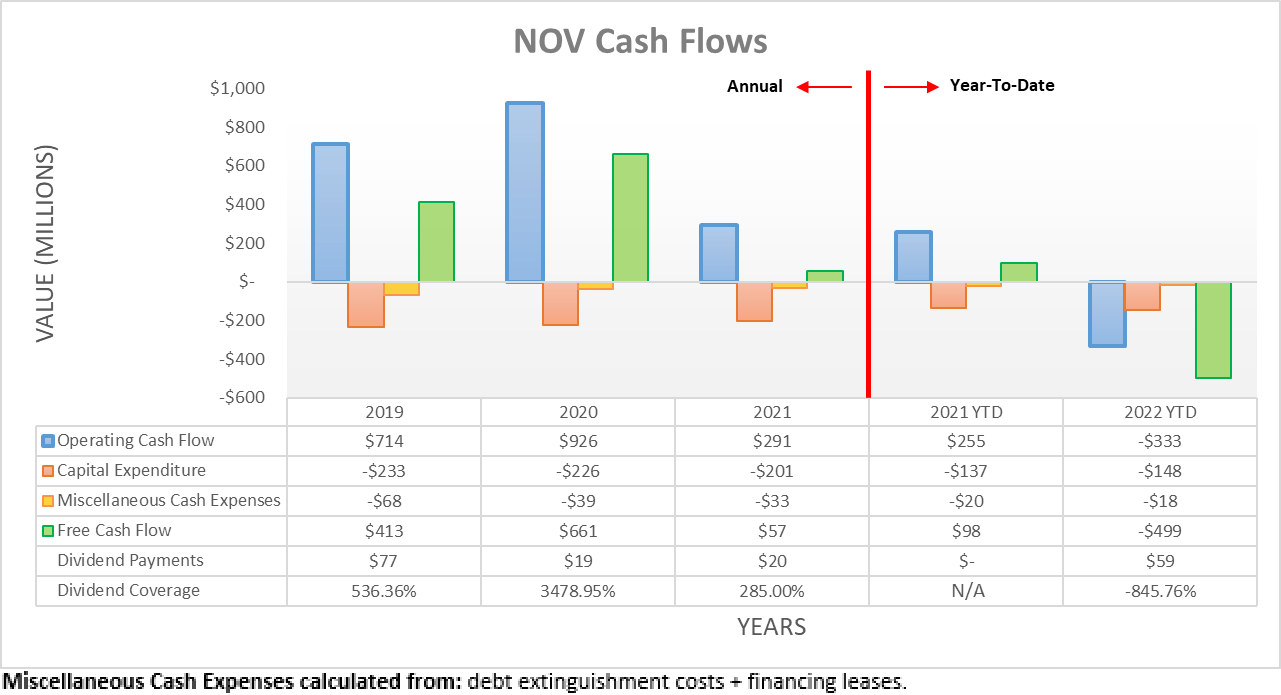

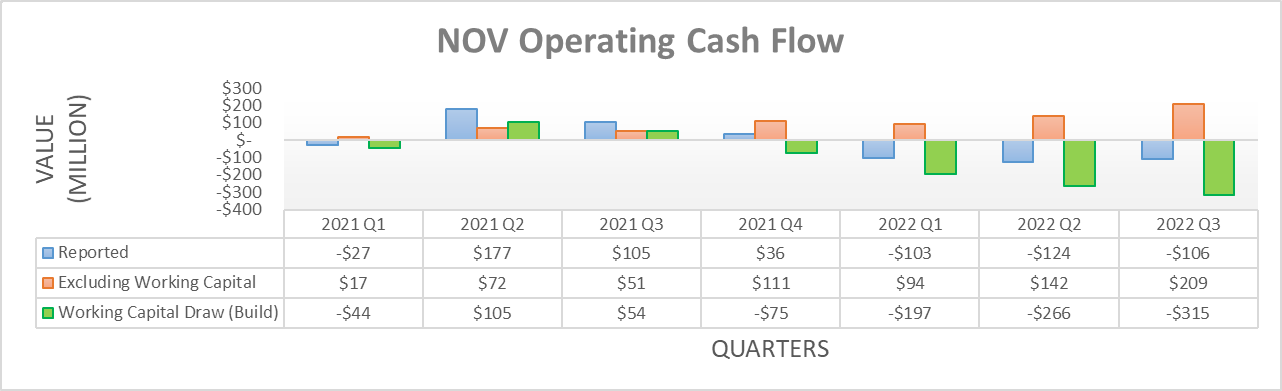

The first half of 2022 was marred by a sizeable working capital build that left their operating cash flow negative, despite seeing improvements beneath the surface. To my surprise, this continued once again into the third quarter with their operating cash flow plunging even lower to negative $333m for the first nine months, thereby down from the previous $227m during the first half. Obviously, this resulted in negative free cash flow and thus a continued cash burn, which stems from one of two reasons. Either, they saw an increasingly large working capital build or much worse, their financial performance suddenly fell off a cliff, metaphorically speaking.

Author

Thankfully, after zooming into their quarterly results, it shows they saw an increasingly large working capital build during the third quarter of 2022 that reached a rarely seen level for their company of $315m. If excluded, their underlying result lifts to $209m and thus easily surpasses their previous equivalent result of $142m during the second quarter, which at the time was already their strongest result since at least the beginning of 2021.

Whilst not necessarily ideal, it nevertheless is much preferable to their financial performance falling off a cliff and sees their previously highlighted green shoots growing larger and stronger. In fact, if annualizing their underlying operating cash flow from the third quarter of 2022, it would see a result of circa $800m that is even higher than their full-year result of $714m during 2019, before the last severe downturn struck.

If subtracting their usual circa $200m to $250m per annum of combined capital expenditure and miscellaneous cash expenses, as listed beneath the first graph above, this would leave their underlying free cash flow at circa $600m to $550m per annum, respectively. Accordingly, after seeing their share price rally following my previous analysis, it leaves their current market capitalization at approximately $9b and thus at the upper end, it would see a high free cash flow yield of circa 6.50%. Whilst this is not bad per se, at the same time, it is not necessarily too appealing nor offers desirable value in light of the volatility their industry inherently carries, especially as the oil and gas rig count stagnates in the United States.

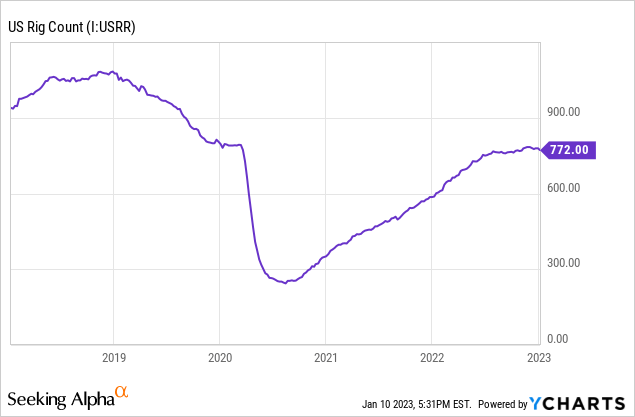

YCharts

When conducting the previous analysis back in early August 2022, the United States saw an oil and gas rig count of 767, but even all these months later, it is only marginally higher at 772. Whilst this indicates their financial performance may not strengthen materially in the coming quarters, at the underlying level it appears to have already recovered back around its level from 2019. In my eyes, this is the best that investors could have realistically expected given the clean energy transition that caps the medium to long-term growth potential for oil and gas production and thus, by extension, demand for their products.

Given the prospects for a recession on the horizon in 2023 or, if not, weaker economic conditions, it decreases the likelihood that the oil and gas rig count will increase materially from this point, as producers understandably remain cautious. That said, as OPEC is actively managing supply and the world is facing an energy shortage, the downside risk is not too steep and thus in my eyes, makes for a broadly flat outlook ahead. Even if oil and gas drilling flatlines throughout 2023, its present rate still marks an improvement versus recent years, as evidenced by their aforementioned underlying operating cash flow that in theory, should be broadly sustained in tandem.

Author

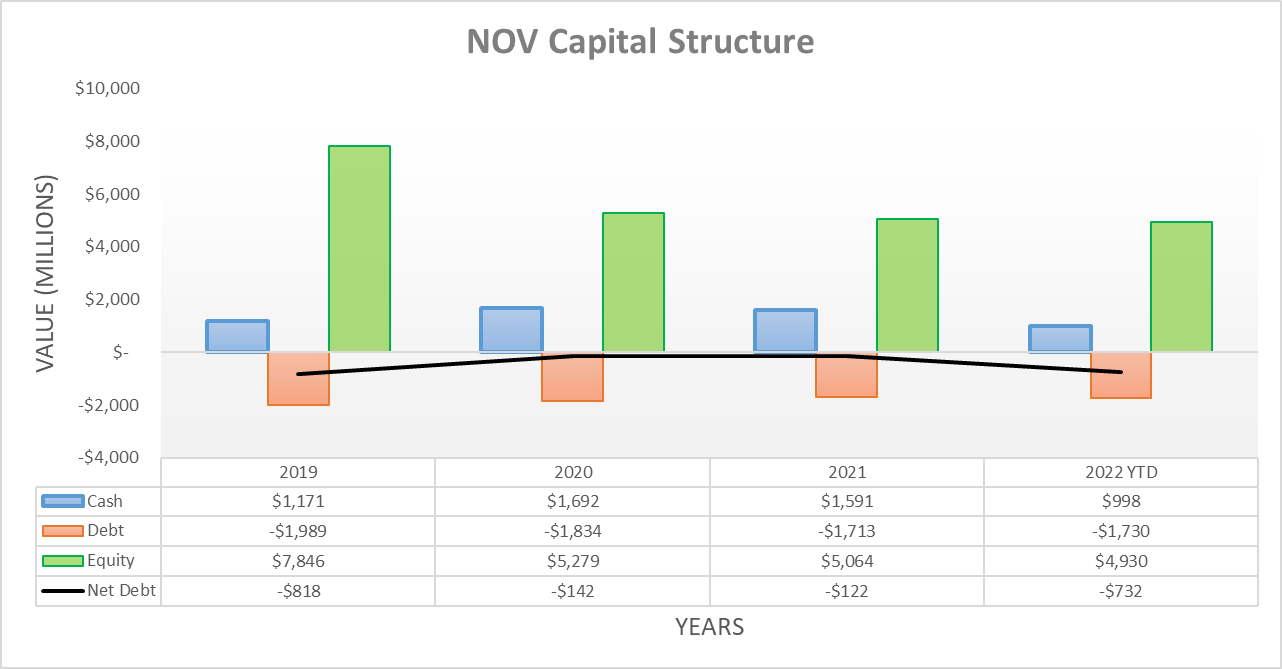

Once again, their net debt climbed higher during the third quarter of 2022 due to their increasingly large working capital build. As a result, it now lands at $732m and thus, unsurprisingly, up noticeably from its previous level of $496m following the second quarter. Interestingly, when their results for the recently ended fourth quarter are released, they could potentially see the entirety of their net debt eliminated if their working capital build of $778m during the first nine months reverses into a draw.

When it comes to the year ahead following the aforementioned outlook, where their net debt ends 2023 will largely depend upon their presently unknown working capital movements and whether they increase their shareholder returns. Although given the improvements within their industry, there are presently no reasons to expect it will spiral out of control. Given this outlook, it would be redundant to reassess their leverage, debt serviceability or liquidity in detail after only one quarter, especially since the earlier discussed topics were already the primary focus of this analysis.

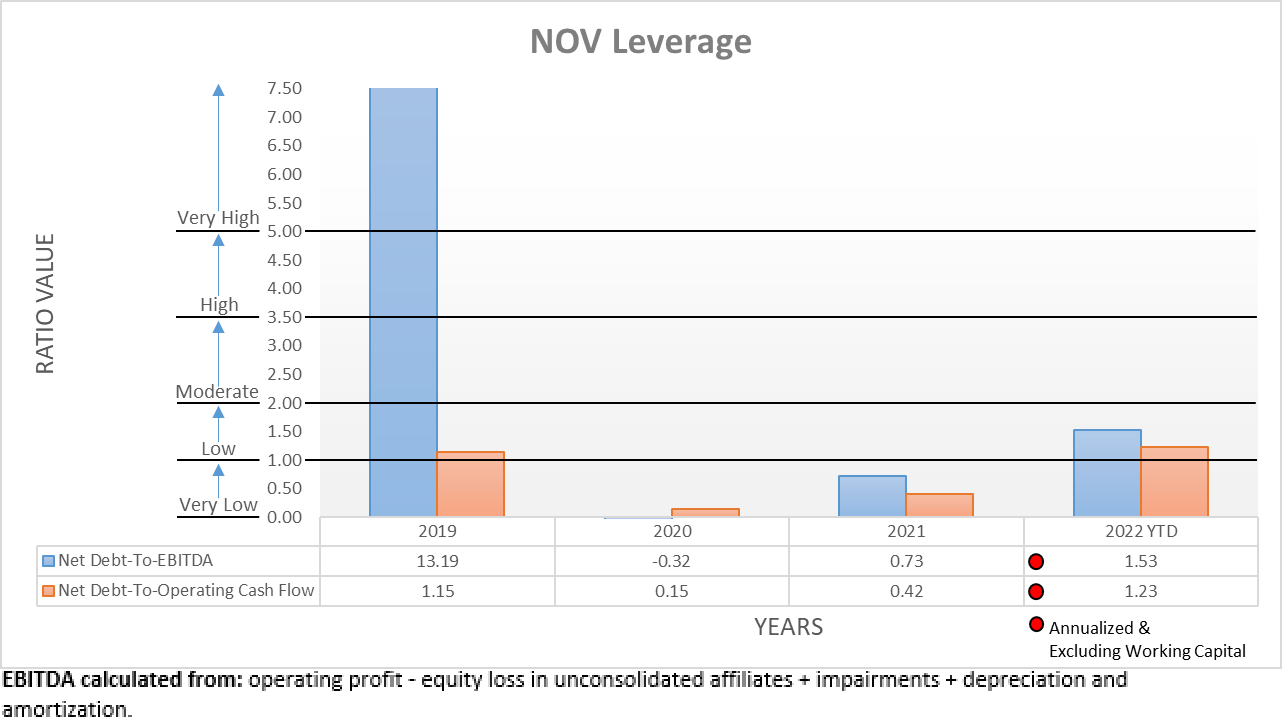

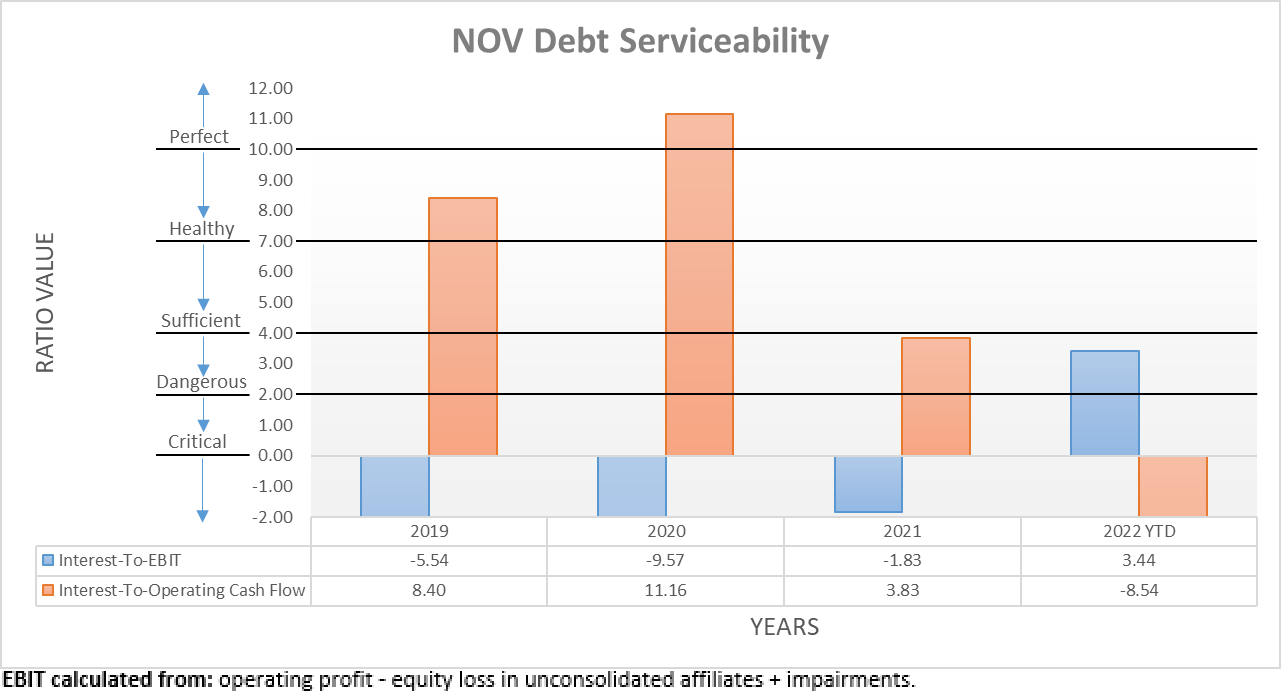

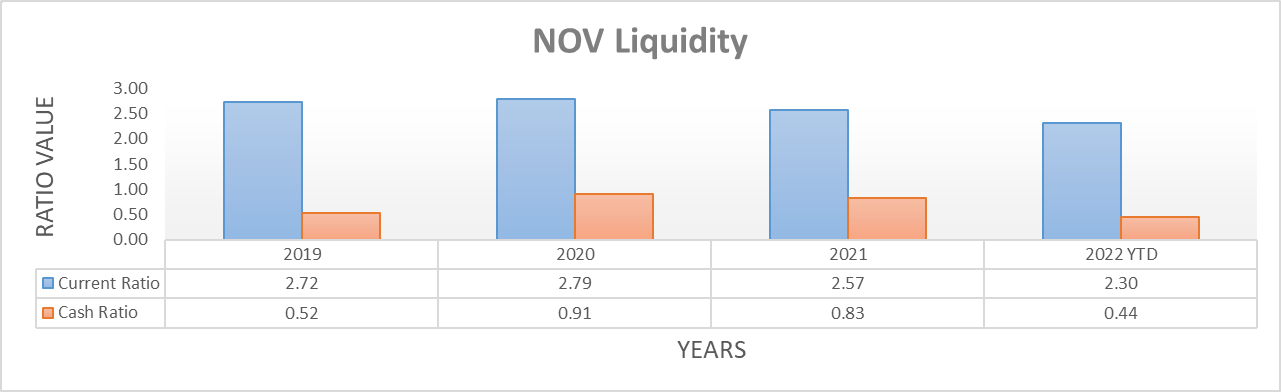

The three relevant graphs are still included below to provide context for any new readers, which shows despite their net debt increasing, their stronger underlying financial performance kept their leverage in check. As a result, they only see their net-to-EBITDA and net debt-to-operating cash flow at 1.53 and 1.23 respectively, which are within the low territory of between 1.01 and 2.00. Meanwhile, their debt serviceability is sufficient with interest coverage of 3.44 when compared against their EBIT, whilst their very large working capital build renders a comparison against their operating cash flow useless with a negative result. That said, even in the face of this cash-generating headwind, their liquidity remained strong with a current ratio of 2.30 and a cash ratio of 0.44. If interested in further details regarding these topics, please refer to my previously linked article.

Author Author Author

Conclusion

On one hand, it was positive to see their emerging green shoots grow stronger during the third quarter, with their underlying operating cash flow now back above its run rate during the full-year 2019. Whereas on the other hand, the oil and gas rig count In the United States appears to have stagnated in the last few months, thereby making it unlikely to see significantly stronger financial performance, especially with the prospects of a recession on the horizon.

Whilst I do not see a need to rush for the exits, I nevertheless feel that those investors sitting with sizeable gains may like to lock in some profits as their free cash flow yield is only around the mid-single-digit levels after their share price rally, which in light of this outlook makes it difficult to see another significant rally. Following this analysis, it should not be surprising to see that I now believe downgrading my previous buy rating to a hold rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from NOV’s SEC Filings, all calculated figures were performed by the author.

Be the first to comment