SimonSkafar

The Investment Plan

Via Renewables Inc (NASDAQ:VIA) is a company in the energy sector. It operates in 19 different states in the United States. where they have totaled more than 400 000 residential customers. With the business divided into two different segments, retail electricity and retail natural gas. The first segment being involved in the transmission and sale of electricity to customers. But besides this they are also transporting, distributing and selling natural gas.

Right now I have seen a few things that would make me want to invest into Via Renewables. The debt the company took on hasn’t been used to properly expand and build revenue streams. Instead it has declined and shares have been diluted. There is a future for the company in the electricity market, but until there are some important steps taken by the management, I think investors are better off selling shares now.

Last Earnings Report Highlights

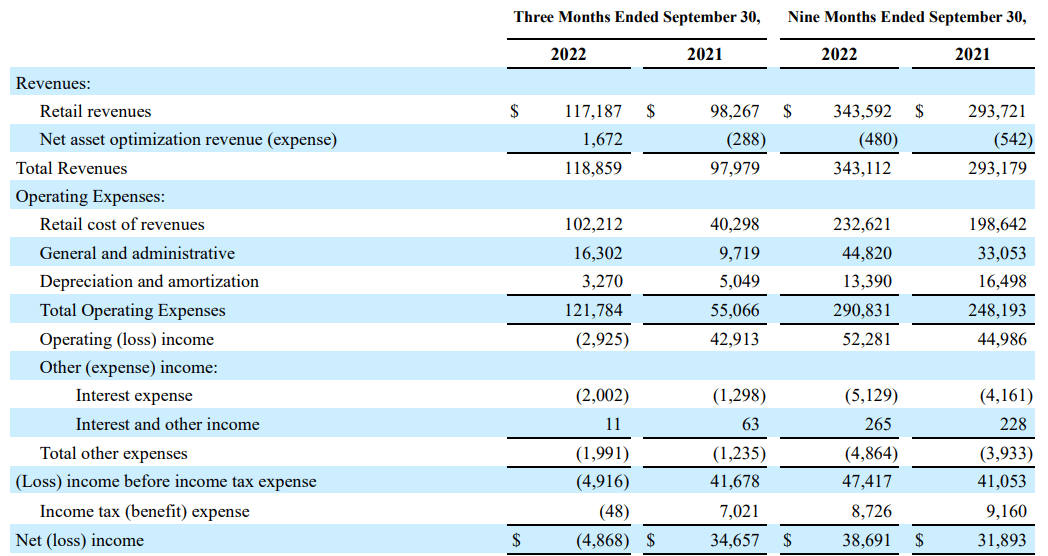

On November 2, 2022, Via Renewables presented to investors its Q3 earnings report. In terms of the bottom line for the company, I note a large decrease YoY. With a net loss $4.9 million compared to net income of $34.7 million the year before. The management mentioned that the reason for this large decrease was for a reduction on their mark-to-market hedges. Essentially the assets that they hold have fluctuated a lot in value causing this decrease in the bottom line. But I want to bring some positive news from the report at least. The top line saw an increase 19% from last year, ending the quarter with $117 million in revenues.

VIA Income Statement (Q3 Earnings Report)

Looking at what the management has to say about the future I see some optimistic and good outlooks. The CEO Keith Maxwell can be noted saying

We’re beginning to see utilities raise rates to keep up with rising energy prices, which presents an opportunity for Via to be a more competitive option.

I think that the company can leverage the current and possible upcoming market conditions and raise both the top and bottom line. The important part will be to once again see a positive net income.

Sector Outlook

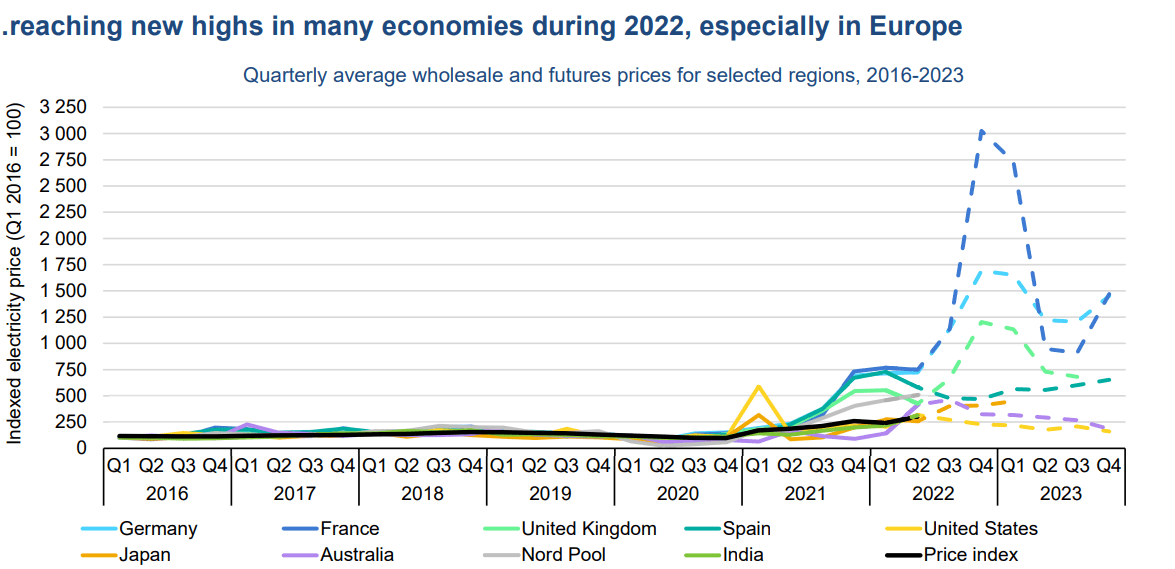

The electricity market is very dependent on what the output is for the suppliers. More than likely there will always be a surplus of electricity in the networks, but as supply might go down sometimes, it can cause sudden increases in price. I think that 2022 was an unusual year for the energy sector. We saw several spikes across the year. Given that the United States imports quite a bit of oil, a decrease in the world supply could cause the prices for consumers to spike, but for Via Renewables this would be good as it directly benefits the company’s revenues.

Electricity Market Outlook (iea.org)

I also mentioned that the company operates with natural gas. There is a large push for more renewable energy sources, clear headwinds for natural gas. But as with most things, it will take time until we have managed to adapt completely. Until then, natural gas will play a vital part of our energy supplies. Because of these reasons I think VIA should continue seeing revenue growth. What will be important for most companies is actively trying to keep operating expenses down to further hedge against possible tougher times.

Competition

Given that VIA operates as an electricity and utilities provider to a large customer base, the competition will be about securing more land when they can establish themselves. There are all types of sizes for companies in this space, some of the ones I think can offer competition would be MGE Energy Inc (MGEE), Genie Energy Ltd (GNE) and Otter Tail Corporation (OTTR). These are also companies focused on offering electricity utilities to customers in the United States.

I think that this space in general is a good place for investors to place money, as the contracts the company secures are long and will provide ample amounts of revenue.

Out of the companies I have mentioned, I believe GNE might be the best-placed company right now. They have growing revenues and a favorable entry point at these prices. The others have rich valuations that might need to come down a little bit. From investors, GNE might get more love than VIA too as they have a healthier dividend yield that won’t hurt the company’s financial position as much.

The Balance Sheet

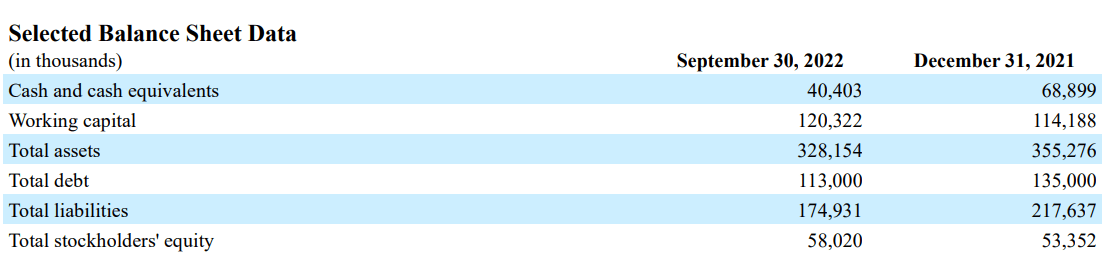

Via Renewables has been experiencing declining revenue growth the last years and this has caused the free cash flow to take a hit. But besides this the company also has $113 million in debt. With the cash position at just over $40 million this leaves little room for missteps by the management. Thankfully they don’t have any current debts that need to be paid in the next 12 months. But unless they have positive and growing cash flows again, this debt will force the company to dilute shares in order to raise capital.

VIA Balance Sheet (Q3 Earnings Report)

The assets they hold have been steadily decreasing since 2017, much thanks to the cash position being used to pay down debt. However they still have a healthy asset/liabilities ratio of 1.88 right now. As the company took on debt back in 2017, they have steadily been paying it off. The unfortunate thing is that as they took on this debt, they have continued seeing decreasing revenues. This makes it much harder for them to successfully get rid of any debt. In the future it will be important to see that the company is actually taking on debt and seeing it put to good use. Otherwise they’ll just use up their cash position and dilute shareholders more and more.

Outstanding Shares (Seeking Alpha)

This brings me to the next point, share dilution. Since 2017 they have diluted about 3% each year. I don’t think this will slow down but rather increase as they become more desperate to pay off liabilities. This will put a lot of risk on any investment in the company right now.

Free Cash Flow (Seeking Alpha)

Cash flow is one of the most important things for a company in order to have a good financial base to stand on. Right now Via Renewables have negative cash flows which makes it very hard to make a bull case for them. If you believe that tailwinds in the energy markets are ahead, then maybe the management could capitalize from this and once again have positive cash flows. But until then, the balance sheet remains unstable and filled with some red flags in my opinion.

Valuing The Company

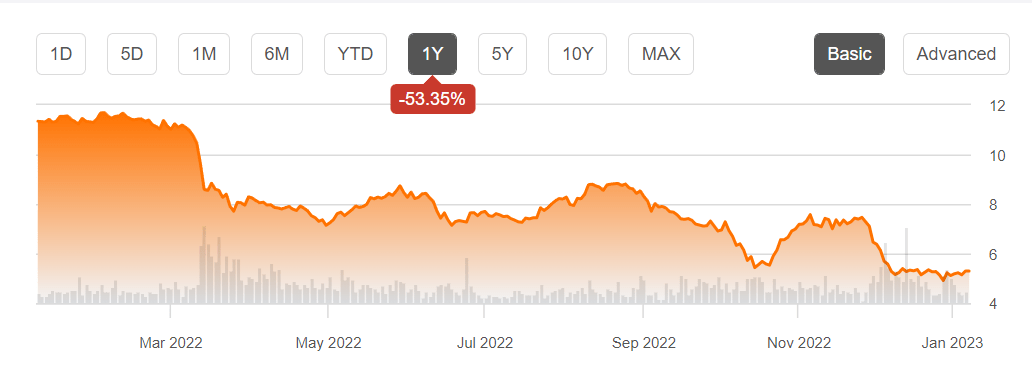

Right now I think there is little to argue why one should invest into Via Renewables. They have been seeing a decrease in the bottom line which has put the current valuation at a very rich price. Instead I think it’s better to name a few things I will look out for before even thinking about a bull case for the company.

Price Chart (Seeking Alpha)

If they can manage to increase the bottom line efficiently whilst not burning too much cash expanding that would be great. I think that they are in a sector where seasonal prices and revenues will occur, but getting a picture for how the long-term outlook would be is important.

With a focus on profitability free cash flow will come naturally. I think that building up a steady stream of this will be vital. It will help them have a good cash position to fall back on. But it also makes share dilution less likely, something that would hurt investors heavily in the long term.

I think that the best course of action right now is to sell shares in the company. If they can’t get the things I mentioned achieved, then there is no investment case to be made here.

Conclusion

Via Renewables saw great growth between 2015 and 2017. But when the company took on more and more debt, it failed to properly leverage it into more revenue as it expanded.

This has led the company to continue to dilute shares to pay off debt on time. Recently the decline in revenues has also led VIA to have negative cash flows. I think these setbacks are enough to discourage investors from putting any money into the company.

Looking at the sector, there will continue to be massive demand but which companies can make it out on top will be more difficult to make out.

I believe that there are too many risks involved with investing in Via. Therefore, I would sell any shares in the company and look for better opportunities elsewhere.

Be the first to comment