da-kuk

In my view, the best way to play the market’s current rebound is to load up on “growth at a reasonable price” stocks – that is, tech stocks that have seen a beating over the past year but have strong fundamental tailwinds to pull them into recovery in 2023.

New Relic (NYSE:NEWR) is a company worth watching. Sidelined by competitor Datadog (DDOG) over the past few years and down nearly 50% over the past year, New Relic has turned a new leaf by successfully implementing its new sales strategy (which involved slimming down its product portfolio and emphasizing its free-trial setups that lead into paid accounts) and re-sparking its growth rates.

Though now a company that has shifted far away from the spotlight, I remain quite bullish on New Relic as it quietly achieves its internal targets and continues to build up its client base (which has now reached over 15k paid accounts, of which about four-fifths generate more than $100k in ARR). New Relic has also made strides in profitability, capitalizing on growing economies of scale and its multi-cloud infrastructure in order to boost gross margins to new records. Amid these tailwinds on both the top and bottom line, I think New Relic has plenty of catalysts to drive a continued rally in 2023.

Here is my full bullish thesis for New Relic:

- New Relic’s new, simplified sales approach has driven re-invigorated growth rates. Much of New Relic’s growth stagnation came from the fact that its product stack was very difficult to comprehend, especially at a time when companies like Datadog were stealing the limelight. “New Relic One” was rolled out in 2020 specifically to address this problem, in addition to dramatically reducing the company’s product count into just three main platforms, as well as rolling out a free tier with the hope of “landing and expanding” new customers. So far, the strategy has proven effective at maintaining robust ~20% y/y revenue growth.

- Consumption-based revenue model is a growth tailwind for New Relic. Other consumption-based software companies, like Twilio (TWLO) and Snowflake (SNOW), are able to drive superior growth and notch premium valuations. It also allows New Relic to derive value out of the smaller customers that may start on New Relic’s free tier and eventually move up to greater data volumes. Over recent quarters, New Relic’s net revenue retention rates have actually been increasing, indicating increased success at upselling to the existing customer base.

- Aligned to the “big data” trend. Data volumes are exploding, both more generally and for New Relic specifically as well. As more and more companies embrace unlocking the potential of data, New Relic’s overall market size and customer traction will continue to grow.

- Economies of scale. New Relic has pushed its pro forma gross margin profile to the mid-70s, allowing for tremendous operating leverage as it continues to grow. Add this on top of the fact that the company maintains a ~120% net revenue retention rate (indicating that the average customer expands their spend on New Relic by 20% in the following year), and we are looking at quite a profit machine in the future.

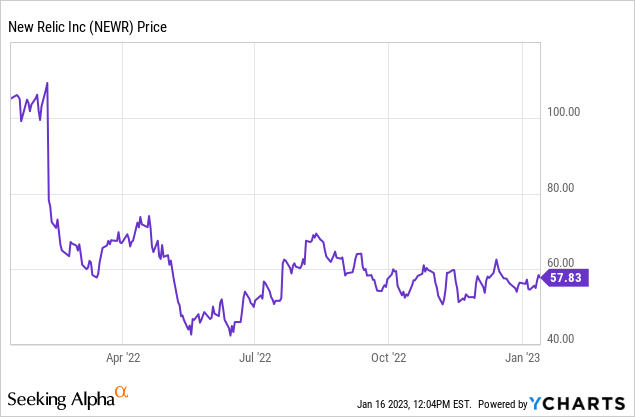

The biggest appeal to New Relic, of course, is its cheap valuation. At current share prices near $58, New Relic trades at a market cap of $3.95 billion. After we net off the $833.3 million of cash and $498.9 million of convertible debt on New Relic’s most recent balance sheet, the company’s resulting enterprise value is $3.62 billion.

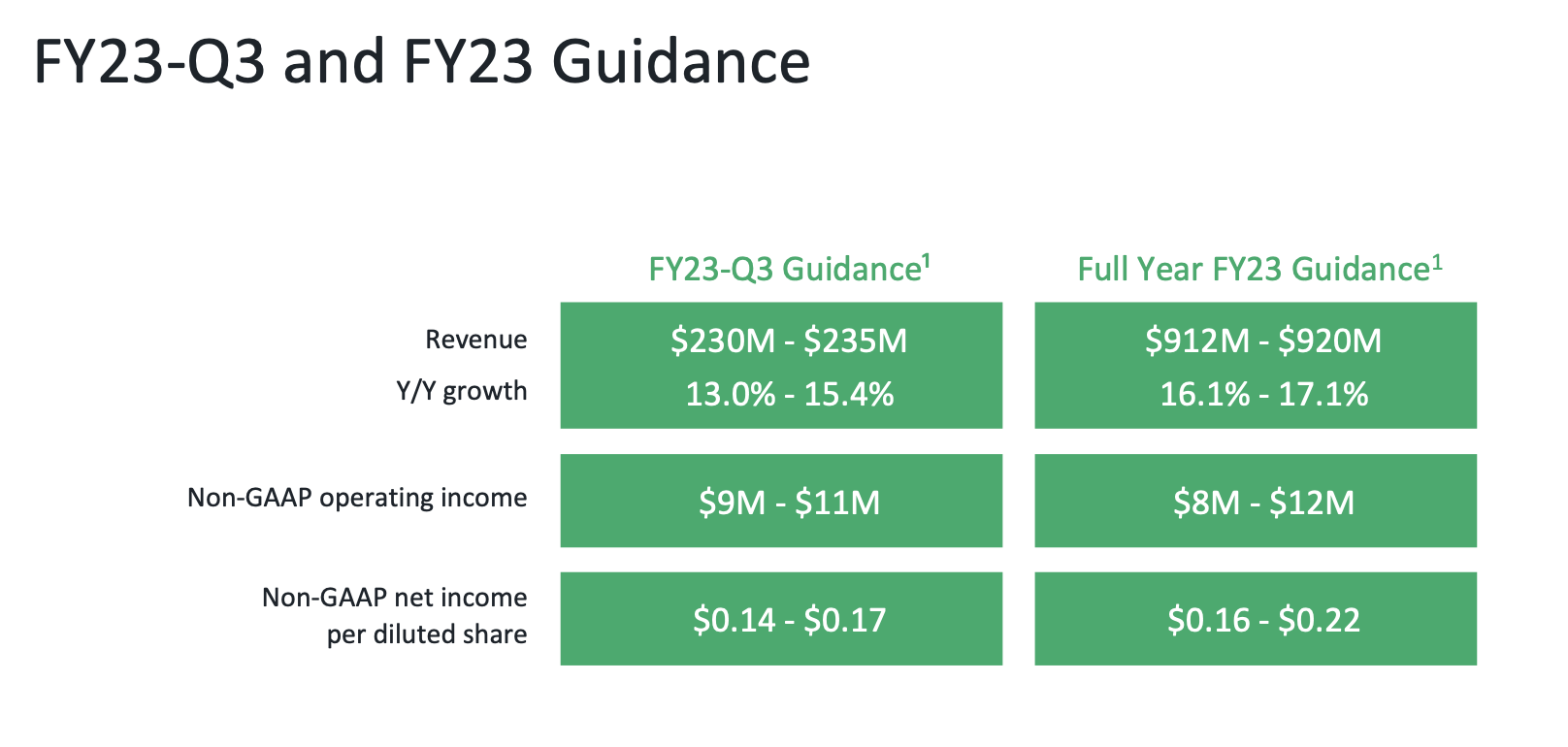

For the current fiscal year, New Relic has guided to $912-$920 million in revenue, representing 16-17% y/y growth.

New Relic outlook (New Relic Q2 earnings deck)

And looking ahead to FY24 (which for New Relic is the year ending in March 2024), Wall Street analysts have a consensus revenue target of $1.06 billion for the company, representing 15% y/y growth (data from Yahoo Finance).

This puts New Relic’s valuation multiples at:

- 4.0x EV/FY23 revenue

- 3.4x EV/FY24 revenue

The bottom line here: there’s no doubt that New Relic is no longer exactly an exciting growth software stock, but this is a perfect value-oriented, profit-generating play for the market rebound in 2022. Load up here.

Q2 download

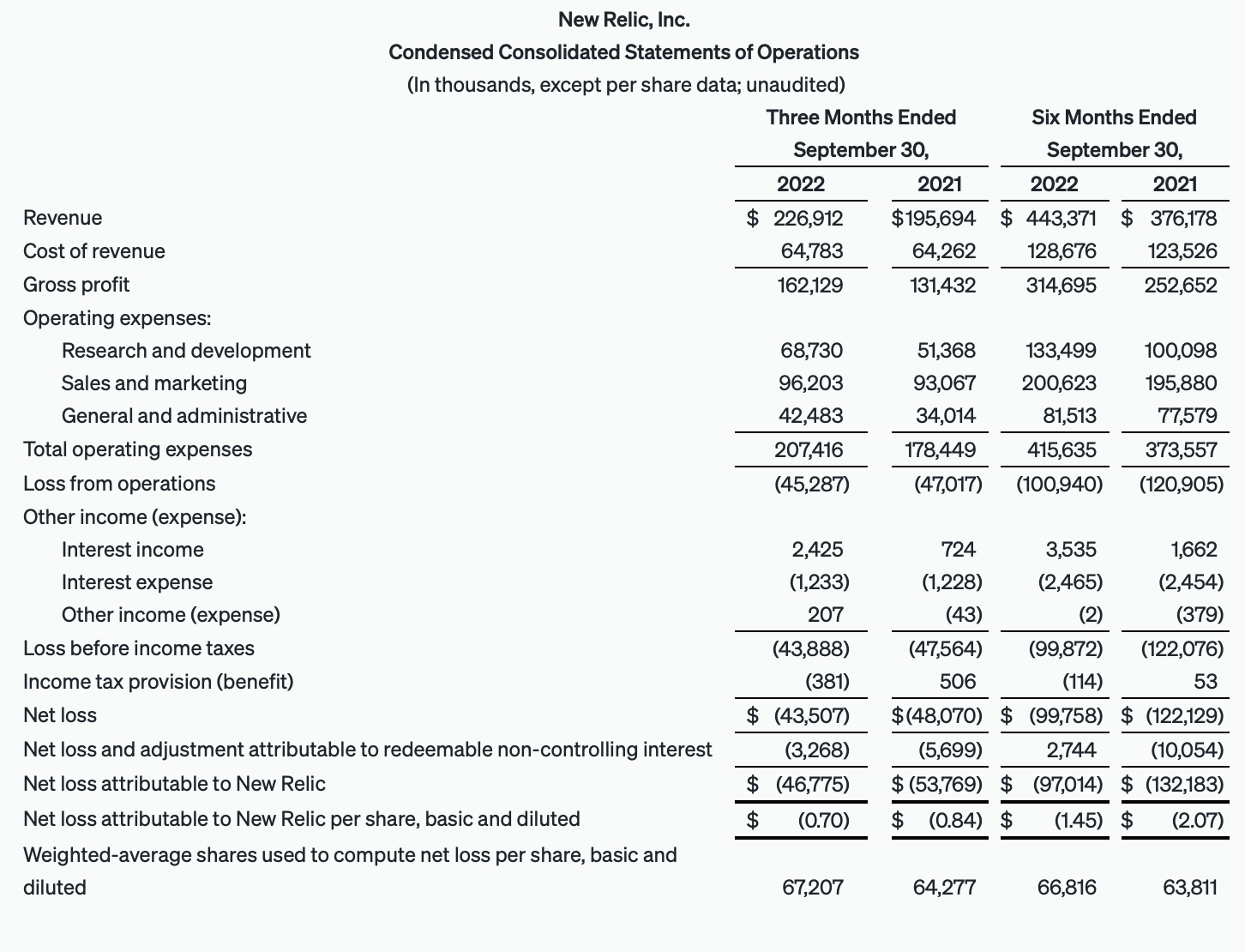

Let’s now highlight some of New Relic’s latest fundamental wins to shed some more detail on why the stock makes for such an attractive investment. The company’s fiscal Q2 (September quarter) results are shown below:

New Relic Q2 results (New Relic Q2 earnings deck)

New Relic’s revenue grew 16% y/y to $226.9 million, beating Wall Street’s expectations of $222.5 million (+14% y/y) by a two-point margin. Management notes that its efforts to bring in new cohorts of smaller customers via its trial programs have seen tremendous success. Per CEO Bill Staples’ remarks on the Q2 earnings call:

First, let’s focus on customer acquisition. Unlike competitors, who land new customers with a sales-led approach, only New Relic offers a unique perpetual free tier that offers every engineer an opportunity to learn and master observability, no credit card required or a fear of lock-in.

Since launching our free tier and pay-as-you-go model two years ago, we’ve been working to steadily increase the efficiency of this experience and nurture customer value to paid levels. In the second quarter, we added over 800 net new paid platform customers using the high-volume low-cost product-led growth model. At this rate, New Relic is now adding new paid platform customers at industry-leading levels.

Our progress here is masked by a long tail of small APM-only legacy customers, who signed up years ago and continue to pay us small amounts each month, but whose spend is not increasing and whose churn partially offsets our new customer growth.

This fast-growing cohort of customers, are new to the platform and embracing full stack observability practices at a rapid rate. It includes companies of all sizes from individual developers in the exploration phase to start-ups getting off the ground as well as large Fortune 2000 companies with engineering teams seeking to modernize their engineering practice.”

The company also noted strength in renewals, with New Relic’s sales team increasing its in-quarter committed renewal base by 3x compared to Q1, and that the company was able to pull forward $18 million in early renewals for customers who wanted to renew ahead of schedule. Net revenue retention rates clocked in at 119% for the quarter, approximately flat sequentially and still indicating healthy upsell activity.

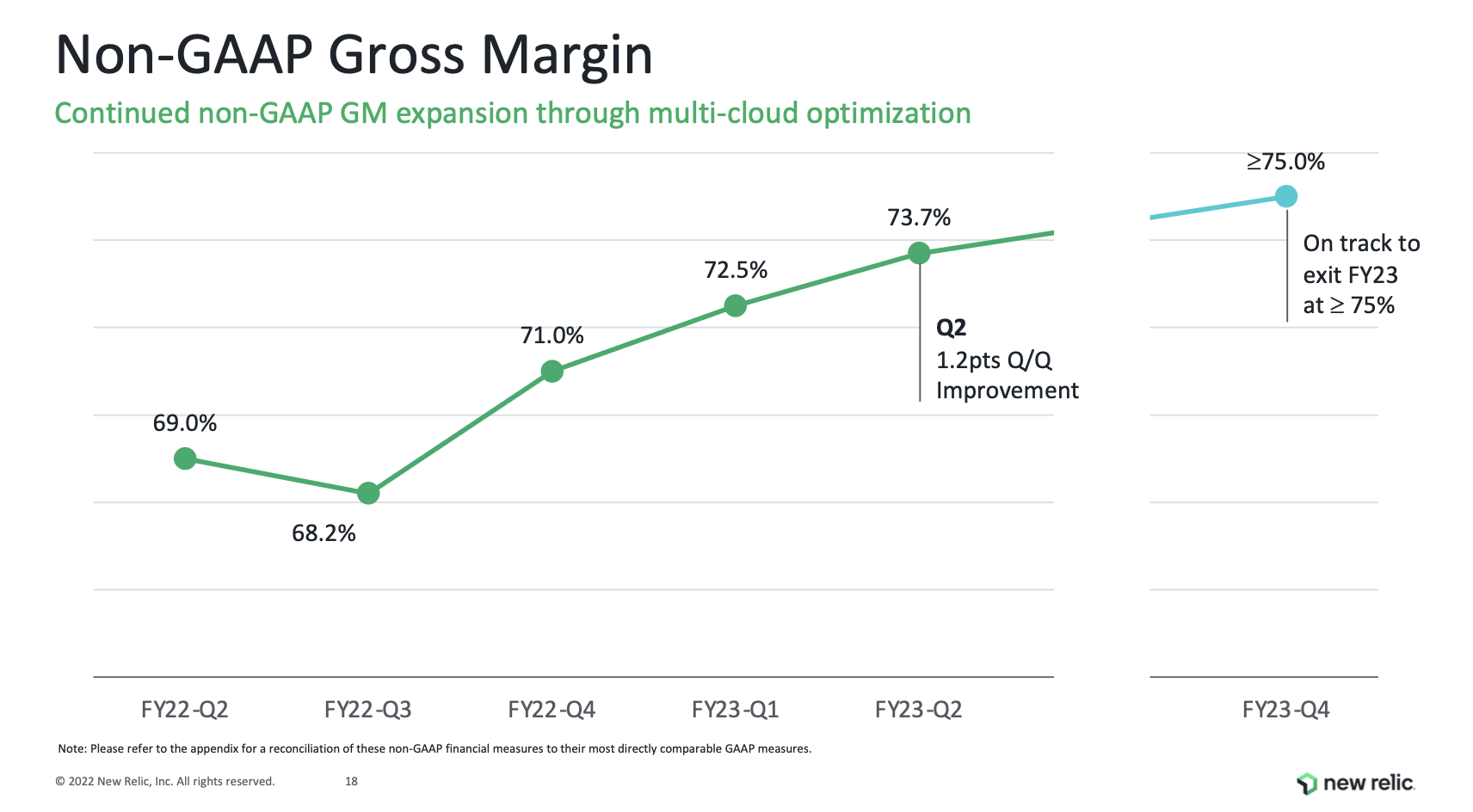

On the profitability front, pro forma gross margins expanded 470bps y/y and 120bps sequentially, and noted that it will exit FY23 at greater than a 75% pro forma gross margin.

New Relic gross margins (New Relic Q2 earnings deck)

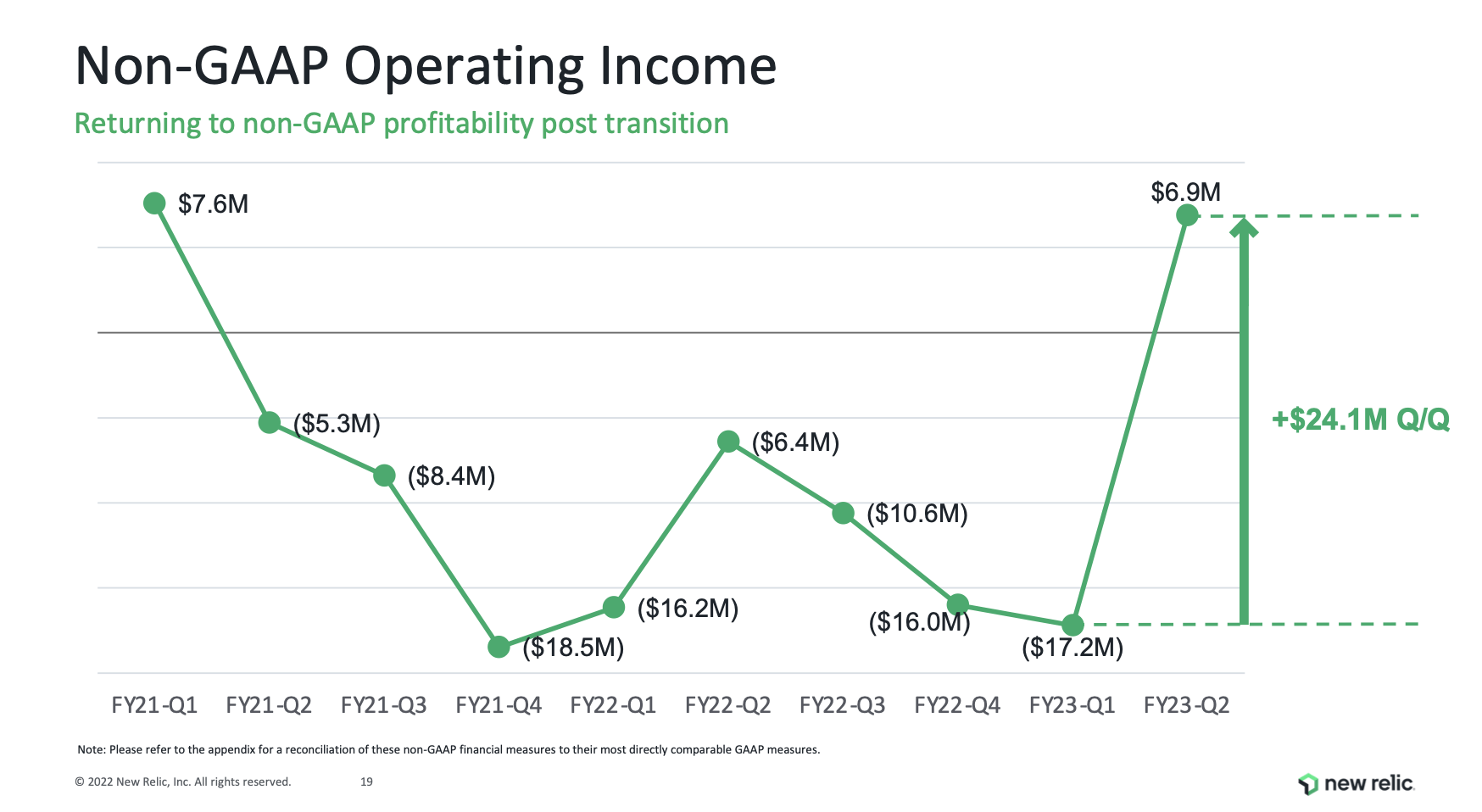

Pro forma operating income also shot up to $6.9 million, representing a 3% pro forma operating margin: six points better than -3% in the year-ago quarter. On top of the gross margin efficiency gains, the company has also been reducing its general and administrative spend and cutting down its real estate footprint as it moves to a hybrid work model.

New Relic operating margins (New Relic Q2 earnings deck)

Operating cash flows in the first half of FY23 also tallied up to $5.6 million, versus cash burn of -$27.2 million in the prior-year period.

Key takeaways

All in all, New Relic is succeeding in its sales initiatives, landing new customers and upselling existing ones, and significantly boosting its profitability. Though certainly an off-the-radar tech stock, New Relic’s combination of steady fundamentals plus cheap valuation shouldn’t be ignored.

Be the first to comment