alexsl

When it comes to the crypto industry, we’ve seen quite the shakeup in 2022 with a series of bankruptcies, none more dramatic than the fall of FTX (FTT-USD). This has understandably made many investors cautious, prioritizing liquidity over potential gains. Silvergate Bank (NYSE:SI), in particular, felt the effects as crypto-related deposits on their SEN network dried up. But as any savvy investor knows, a downturn can also present opportunities. Now is the time to take a good hard look at what happened and figure out the best way to move forward.

What do we know about Silvergate’s financial situation?

The management team at the company held a conference call with shareholders and analysts to shed light on the recent developments and share their plans for the future. They were upfront and candid in addressing the challenges they faced and provided valuable insights. Here are a few key points to take note of:

The decrease in digital asset deposits from $11.9 billion to $3.8 billion at the end of December 2022 is certainly a cause for concern. However, it’s reassuring that the company’s management has implemented prudent policies to avoid a potential bank run. They have structured the balance sheet to withstand a 70% drawdown on deposits, and maintain cash reserves that exceed all remaining deposits. Additionally, they have taken measures to ensure that they can accommodate deposit inflows and outflows under a range of market conditions, and maintain cash liquidity to meet potential deposit outflows. This level of foresight and planning is a positive sign for the company’s long-term prospects.

During Q4 2022, Silvergate faced a challenge as customers withdrew deposits. To address this, the company used wholesale funding to satisfy outflows. However, to maintain a liquid balance sheet and accommodate sustained lower deposit levels, Silvergate sold debt securities for cash proceeds, resulting in a loss of $718 million. As of December 31, 2022, the company held $5.6 billion in debt securities, all of which are U.S. government or agency-backed and available for sale, and which include unrealized losses of approximately $0.3 billion. In early 2023, the company plans to sell a portion of these securities to reduce wholesale borrowings. This will result in the recognition of a fourth-quarter impairment charge related to the unrealized loss on those securities expected to be sold.

Despite the challenges faced by the company, Silvergate’s deposits seem safe and accessible. As of December 31, 2022, only $150 million of Silvergate’s deposits were from customers that have filed for bankruptcy. Silvergate held total cash and cash equivalents of approximately $4.6 billion, which is more than the deposits from digital asset customers.

You can check the business update here.

Silvergate Strategy Revamp

To ensure its business is strong in light of lower deposit levels, the company is taking steps to adjust its expenses and review its product offerings and customer relationships. One cost-saving measure Silvergate is implementing is a reduction of its workforce by approximately 40% or 200 people. This decision was made because the company had grown its employee headcount significantly in the recent past, but now needs to control expenses in light of the current situation. The company estimates total costs related to the workforce reduction at around $8 million and expects the majority of these charges to be incurred in Q1 2023. The company will also be streamlining its product portfolio to reduce complexity. In line with this approach, the company exited its mortgage warehouse lending product in the fourth quarter of 2022, incurring a restructuring charge of approximately $4 million.

Silvergate bank is exploring adjustments to its revenue model for SEN, its stablecoin exchange network, as it examines all of its products in the context of recent market trends. Silvergate doesn’t view the SEN business as a means of acquiring deposits to finance other asset strategies and is evaluating alternative pricing plans for the service as it continues to assess client needs.

The company no longer expects to derive value from its Diem assets in the short term, and as a result, recorded an impairment charge of $196 million in Q4 2022 related to developed technology assets acquired from Meta. This decision was made due to the current challenges in bringing a tokenized dollar to market. Accounting rules require that the intangible asset be written down when it cannot be justified by future revenues. Despite this, the company still believes that a tokenized dollar on a blockchain will have value in the market and the management believes it might be able to enter this space later.

Silvergate Risks and Opportunities

The situation is dynamic, and I will just mention some of the most critical risks in short term, this won’t be an exhausting list. Silvergate is currently facing class action lawsuits related to FTX and Alameda, which present a significant short-term risk for the company. The potential liabilities that the company might be facing are unknown.

Another uncertainty is how the balance sheet and earnings power will look like. We will have to wait for the earnings release and clarification during the earnings call to have a better understanding. However, the situation is so fluid that it might take months to have a clearer picture.

Another possibility arising from the current state of affairs is the possibility of a traditional big bank taking over Silvergate to acquire its crypto-related infrastructure. Alan Lane, Silvergate CEO, mentioned that the bank will always consider combining with a bigger company to help diversify and limit stress periods like the current one. He also states that being a crypto-only focused institution is still the most efficient structure for the bank, as it is unique and has created opportunities for them to differentiate themselves, and that it is quite likely that a larger institution that wants to get into the space will want to take a look at Silvergate because of its track record on the space. This presents both a risk and an opportunity. The risk is for investors who are deeply underwater to see the company being sold for a premium that won’t cover their losses. The opportunity lies in a quick repricing of the company based on a takeover offer at a significant premium from the current situation.

There are several other risks that are not covered here, we chose to focus on the most critical regarding the recent events. One obvious example is a potential fall, like DCG, that could reignite the deposits’ run and have another huge impact on the company’s earnings power.

Silvergate Valuation

In my opinion, Silvergate has been sitting on its crypto deposits since 2020 to avoid a bank run. That means they could afford to wait and that’s what they did when they first got loans to make up for lost deposits. But once they realized they might be in a permanent situation, they backed away from the loans and cut their asset base by $5 billion. I think that was smart, but it obviously hit the company’s earnings hard.

They were making 0.5% on their assets before this mess and now, with a new balance sheet that’s lost $8 billion in deposits, I figure the company can still make about $30 million a year in profits (1% times $3 billion earning assets – excluding the $5 billion in cash). At ten times profits, that values the bank at around its current market cap of $300 million.

Another way to look at it is by looking at the book value, which will be lower because of the impairment charges they took on the securities they sold. But even with that, the book value will still be around $300 million, which again is consistent with the current market price. Please bear in mind these are rough ballpark estimations, just to provide some color, and not to be used as figures for investment decisions.

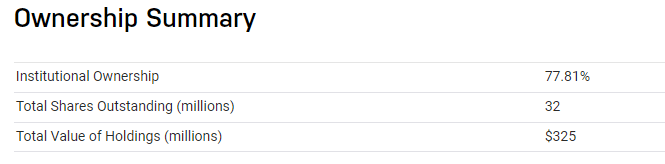

The opportunity here is a possible takeover attempt. With a high percentage of institutional ownership, it would likely require a big premium.

nasdaq.com

For that reason, I’ve increased my position in Silvergate, still keeping it as an underweight in my portfolio, but big enough that a possible takeover at a significant premium would make it break even. However, I don’t recommend other investors follow this strategy. This is more of a hedge for me because I didn’t want to see this company being sold for a low price, like $20, while I take a big loss. In reality, my positive outlook is on the future of this bank and the fact that the digital asset space will grow significantly, and Silvergate is one of the best available on-ramps for institutions.

Be the first to comment