Tzido/iStock via Getty Images

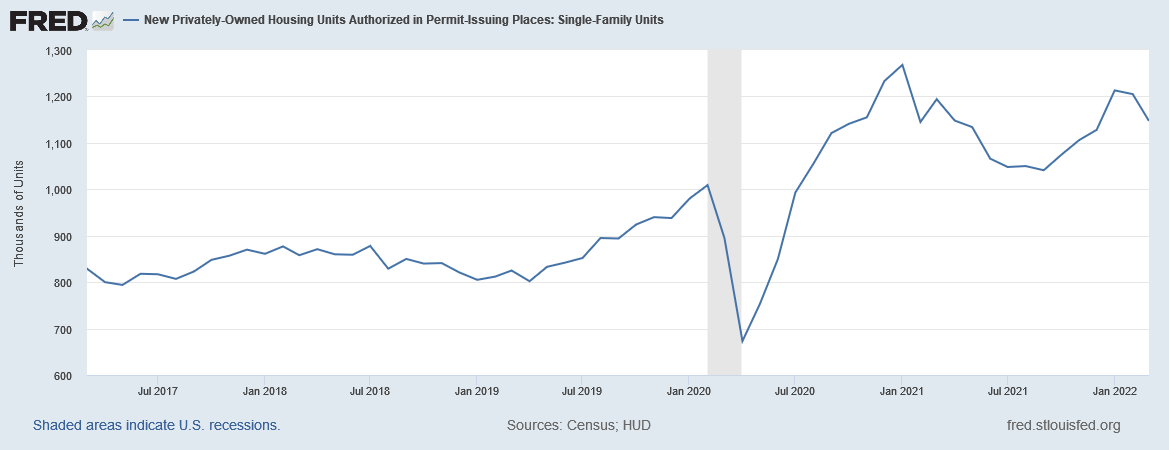

Unit building permits dropped:

Building permits release (Census)

Here’s a chart of the data.

1-unit building permits (FRED)

I noted a few days ago that housing market data is starting to show the effect of higher interest rates. This is the second consecutive month of declines and is likely the result of the more hawkish Fed.

Fed President Evans argues the Fed should raise rates above the neutral rate:

The U.S. central bank will probably raise interest rates above levels it considers neutral for the economy next year given the outlook for inflation, Federal Reserve Bank of Chicago President Charles Evans said.

“Probably we are going beyond neutral,” Evans said Tuesday during a moderated discussion at an Economic Club of New York event.

“That’s my expectation, when I see that, taking out special factors, I’m still left with 3 to 3.5% inflation” by the end of 2022, he said. “That’s not what we want. If we’re at a 2.5% inflation rate, I think we have more things to ponder there.”

The neutral rate is one that is neither stimulative nor restrictive for economic activity. Put more succinctly: the Fed intends to slow economic activity in its bid to tame inflation.

Every April, the world’s finance ministers and other economic policy leaders descend on Washington for the spring meetings of the International Monetary Fund and World Bank.

1.) Things feel different this year – and not just because D.C. has had a stubbornly late-arriving spring, Axios’ Neil Irwin writes.

Why it matters: The world is facing profound economic challenges – global supply shortages caused by the pandemic and war – that defy the ability of economic policymakers to solve through clever management of spending or interest rates.

State of play: Through the last 15 years of financial crises and slow recovery, the world faced serious economic problems, but ones that were largely “endogenous,” linked to the internal workings of their economies.

1.) Those sorts of crises are hard, but at least are responsive to the kinds of policy changes that finance ministers and central bankers can enact. Think of the global financial crisis and countless emerging market debt crises.

2.) The ongoing supply disruptions tied to the pandemic and war in Ukraine amount to “exogenous” events, both driven by non-economic forces but constraining global supplies.

The disruptions are now pretty extreme. Supply chain issues have been ongoing for several years with no sign of letting up. China has imposed wide-ranging lockdowns which have exacerbated the problem. Russian oil is now embargoed; trade routes through eastern Europe have been disrupted. There’s little that central banks and governments can do about this.

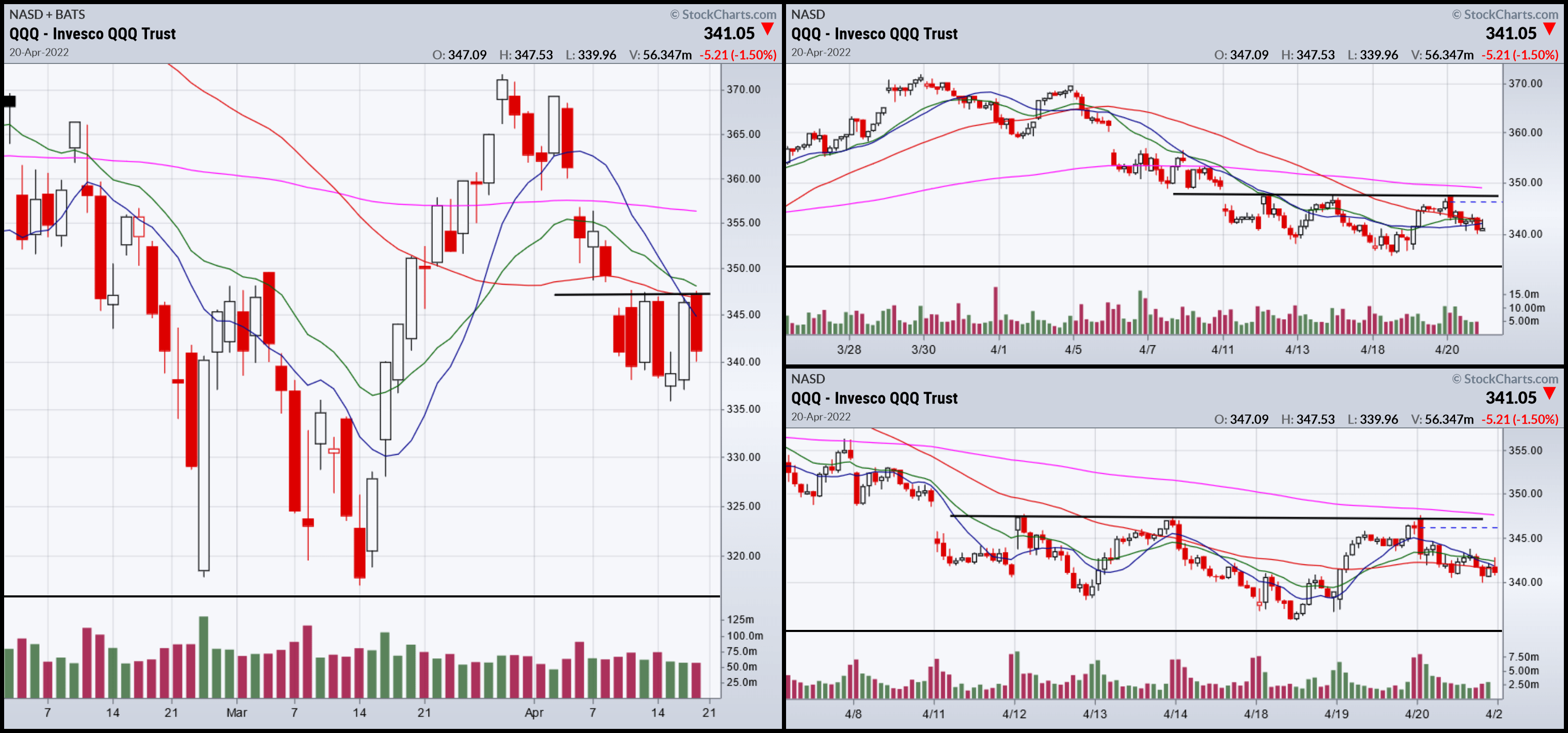

Let’s take a look at the charts.

SPY 3-month, 1-month, 2-week (StockCharts)

The SPY has the best charts. All three show that prices have broken through resistance. Today marked the second day of the upward rally.

3-month, 1-month, and 2-week QQQ (StockCharts)

The QQQ is still consolidating sideways. Today prices were lower due to Netflix (NFLX) selling off.

3-Month, 1-month, and 2-week IWM (StockCharts)

The IWM has broken through resistance, as seen on the 3-month and one-month charts.

Despite the progress, I’m still not that bullish due to the macro events, especially the Fed. However, I could be wrong.

Be the first to comment