metamorworks/iStock via Getty Images

Investment Thesis

Mobileye Global (NASDAQ:MBLY) is an autonomous driving solutions company. Mobileye’s advanced driver assistance systems (”ADAS”) is designed to advance the safety of road users.

Mobileye’s shares are soaring higher since its IPO. But as I look under the hood, there are more questions than answers.

As we go through, keep in mind that Mobileye Global’s results have to be compared with its pro-forma quarterly results in its S-1 filing.

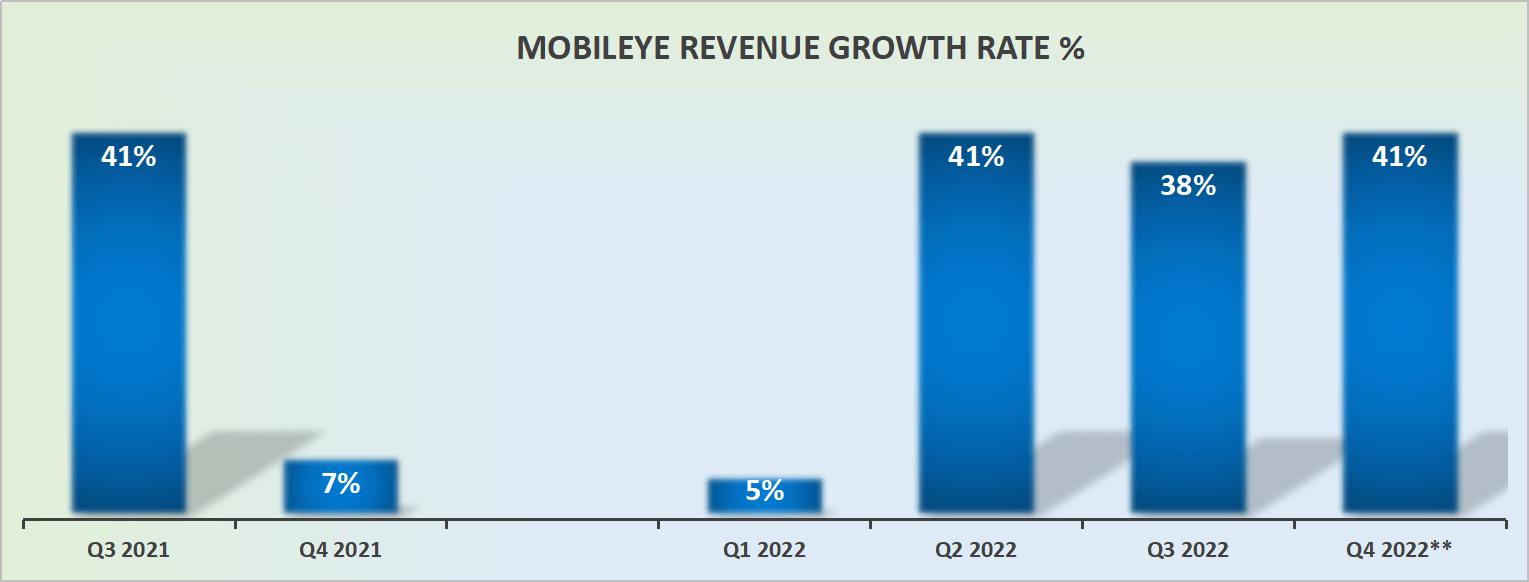

Revenue Growth Rates Remain Strong

MBLY s-1, Q3 2022 press statement

The above graphic looks odd. In the first instance, Q4 2021 and Q1 2022 post very much middle-of-the-road revenue growth rates. While Q3 2022 was up 41% y/y.

However, keep in mind that Q3 2021 compares against, the quarter ending in September 2020. And as you know, the middle part of 2020 was largely shut down, so Q3 2021 had very easy comparables.

Then, as we moved forward in 2020, there was an increase in pent-up demand, that made the comparables quarters of fiscal Q4 2021 and fiscal Q1 2022 look uninteresting.

And now, looking ahead to fiscal Q4 2022 as Mobileye once again compares with that easier quarter of Q4 2021, Mobileye is able to point to very strong guidance of 41% y/y revenue growth rates at the high end.

Consequently, this is my point. There are some odd comparables afoot. On a more normalized basis, despite all the allure of advanced driver-assistance systems, if I were to speculate, fiscal 2023, next year, will probably see around 25% to 30% CAGR.

Incidentally, for their part, analysts following the company have as their consensus figure around 20% CAGR. Thus, this is the key takeaway, Mobileye’s revenue growth rates next year will be less interesting than they may appear on the surface.

With that context in mind, let’s discuss its profitability profile.

Profits Skid on Black Ice

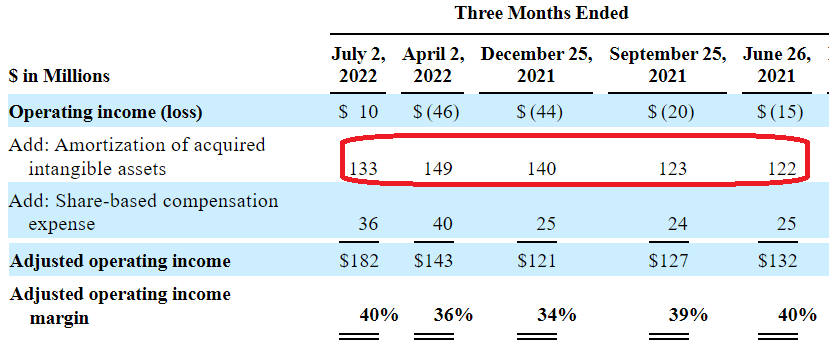

For Q4 2022, Mobileye points to 34% adjusted operating profit margins. This is flat with the 34% adjusted operating profit margins reported in the same quarter a year ago.

What I find interesting is that the biggest figure to be added back to its GAAP profitability isn’t stock-based compensation. In fact, stock-based compensation only amounts to 8% of revenue. The biggest add-back is the amortization of acquired intangible assets.

And in fact, this is the one thing that the auditors, PWC, pulled up Mobileye on, stating,

As described in Note 11 to the combined financial statements, the Company’s intangible asset balance was $3,071 million at December 25, 2021 and the amortization expense was $509 million for the year ended December 25, 2021. These intangible assets consist primarily of developed technology and customer relationships and brands that were attributed to the Company from Intel Corporation (the “Parent”) as part of the net parent investment in the Company primarily from the acquisition of Mobileye B.V. The recognition of those intangible assets included significant judgment in estimating the fair value of intangible assets […]

The paragraph above may look challenging to read, but what the auditors are saying is that it requires ”significant judgment in estimating the fair value of intangible assets”.

In other words, we know that you are adding back to your non-GAAP operating profits, but we can’t figure out what’s appropriate.

MBLY S-1

As you can see above, the amortization of assets is a recurring expense. It’s not a one-off, non-cash cost. It’s a persistent part of its operations.

MBLY Stock Valuation — 31x Next Year’s non-GAAP Operating Profits

For 2022 as a whole, Mobileye guides for approximately $655 million of adjusted operating income at the high end.

If we were to assume that next year, Mobileye’s adjusted operating income was to grow by a further 30%, as Mobileye increases its scale and finds efficiencies, then this would see Mobileye’s adjusted operating income reach approximately $851 million. This leaves the stock priced at 31x next year’s non-GAAP results.

On top of that, Mobileye has a $3.5 billion dividend to send back Intel (INTC) by April 2025. Put another way, in less than 3 years, Mobileye has to find $3.5 billion to send back to Intel.

The Bottom Line

In the best case, Mobileye’s free cash flows next year could reach around $600 to $700 million. However, that free cash flow will not be able to be used to reinvest aggressively to reinvest back into the business to grow Mobileye’s AV technology.

Instead, that cash will need to be shored up on its balance sheet, so that a $3.5 billion dividend can be sent to Intel.

Presently, the share price is soaring higher and there’s a lot of excitement. But having been through the 2022 bear market, I know how quickly excitement can turn into trepidation. So, whatever you decide, wear a seat belt.

Be the first to comment