imaginima

Debt reduction and balance sheet improvements have been a key theme in the energy infrastructure space for years. For many names, lowering leverage was a prerequisite before deploying excess cash flow to dividend increases and buybacks. Others are still working to reduce leverage before pursuing these shareholder-friendly initiatives. Today’s note examines leverage improvements from 2016 to 2022 for MLPs and broader midstream using the Alerian MLP Infrastructure Index (AMZI) and the Alerian Midstream Energy Index (AMNA), respectively, and explains why these improvements are important.

Average leverage at the index level reflects broad improvements for midstream/MLPs

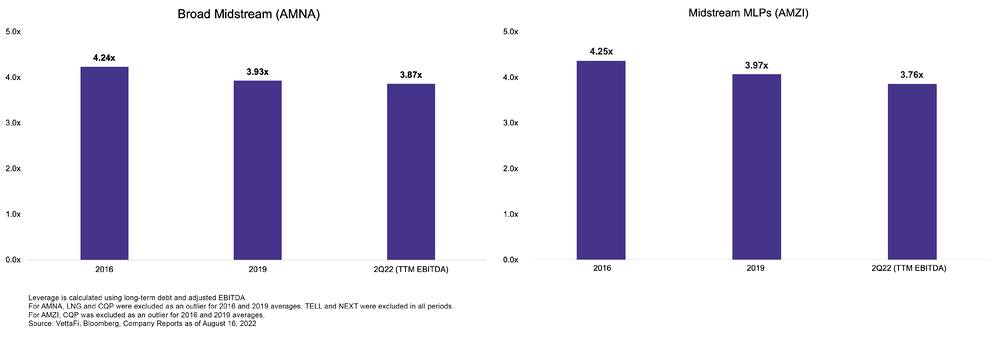

With free cash flow generation becoming more meaningful since 2020, a number of companies have used excess cash flow to reduce debt, while EBITDA growth has also contributed to lower leverage ratios. The chart below shows average leverage for current constituents of the AMZI and AMNA for 2016, 2019, and as of 2Q22. Average leverage for AMZI and AMNA constituents has declined from over 4.2x in 2016 to less than 3.9x today. Leverage was calculated using long-term debt and companies’ reported adjusted EBITDA. Note that leverage calculations can vary. Net debt is often used, and banks/creditors may make other adjustments.

Average Leverage Has Trended Lower For Current AMNA And AMZI Constituents (Author)

The charts show a noticeable improvement over time, with 2016 and 2019 providing useful mile markers. Recall, WTI oil prices fell to a multi-year low of $26 per barrel in February 2016, and this was also before the significant adoption of equity self-funding, which started to gain traction in late 2017. The 2019 data provides a pre-pandemic measure and coincides with a period when capital spending across the space was still elevated. Finally, data from 2Q22 and trailing 12-months’ EBITDA reflects the improvements afforded by the shift to significant free cash flow generation as spending has moderated, which has supported debt reduction. With improved balance sheets, midstream companies have been able to execute on dividend increases and buybacks, as strong free cash flow generation has provided enhanced financial flexibility.

Company-level data gives more color to improvements

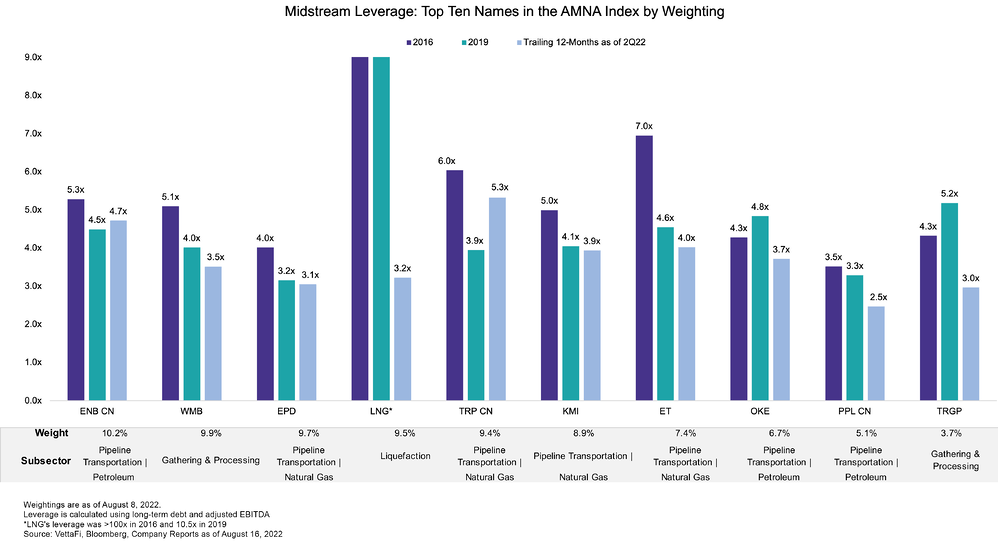

Examining leverage ratios at the constituent level provides helpful context around company-specific improvements and the varying factors which may affect leverage trends over time. The chart below shows leverage ratios, sector classifications, and weightings for the top ten constituents of AMNA (please see the appendix to reference the same chart for the AMZI). All ten names have lower leverage today than in 2016. Seven of the ten have leverage below 4.0x today, compared to only Pembina Pipeline (PBA, PPL.CN) having leverage below 4.0x in 2016.

Author

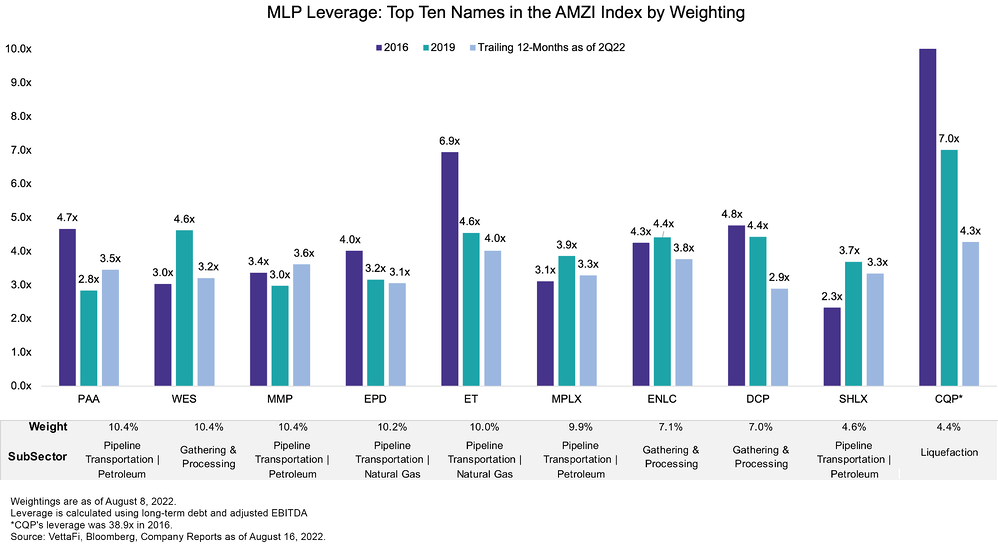

Digging into the constituent data provides a number of observations. Some companies had leverage ratios at or below 4.0x in each period, including Enterprise Products Partners (EPD), Magellan Midstream Partners (MMP), and MPLX (MPLX). These names were able to maintain or grow their distributions through challenging macro environments. Cheniere (LNG) and Cheniere Energy Partners (CQP) have seen notable improvements in leverage since 2016 as capital-intensive LNG projects entered service. Since announcing its long-term capital allocation plan in September 2021, Cheniere has paid down $3.1 billion in debt through 2Q22. For the large Canadian corporations Enbridge (ENB, ENB.CN) and TC Energy (TRP, TRP.CN), leverage has trended down from 2016 levels but remains elevated relative to other names as both companies work through an extensive project backlog in contrast to many peers.

Why is lower leverage important?

The massive buildout of energy infrastructure in the 2010s and financing challenges in 2014-16 when oil prices were retreating left a mark on the balance sheets of many midstream companies. Several names took steps to improve their balance sheets and were better positioned financially when the pandemic shocked energy markets. For some companies that were financially stretched, dividend cuts were key to shoring up the balance sheet during these difficult periods, and these cuts were painful for investors. The macro volatility of recent years adds important context to why companies have prioritized debt reduction and why companies that may have been comfortable with 4.5x-5x leverage in the past have adopted more conservative targets today. Lower leverage speaks to the overall improved financial health of the space and adds confidence that companies will be able to continue maintaining and growing dividends.

Bottom Line

With stronger balance sheets and enhanced financial flexibility supported by strong free cash flow generation, midstream companies are executing on shareholder-friendly returns in the form of dividends and buybacks and are better equipped to weather potential periods of market volatility.

Appendix

Top Ten Names In The AMZI Index By Weighting (Author)

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA).

Disclosure: © Alerian 2022. All rights reserved. This material is reproduced with the prior consent of Alerian. It is provided as general information only and should not be taken as investment advice. Employees of Alerian are prohibited from owning individual MLPs. For more information on Alerian and to see our full disclaimer, visit Disclaimers | Alerian

Be the first to comment