da-kuk

Thesis

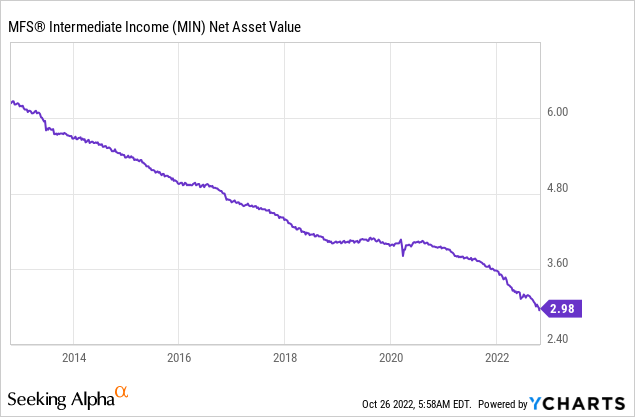

The MFS Intermediate Income Trust (NYSE:MIN) is a closed end fund that invests in treasuries and investment-grade bonds. The fund is not leveraged, which makes it an alternative to the popular investment grade bond ETF (LQD). While their 3- and 5-year total return performances are similar, MIN trails the ETF, and more importantly, has an unsupported dividend. The fund has stuck to a 9% dividend yield for the past years, despite a lack of cash-flows from its underlying assets, which has resulted in substantial NAV destruction:

The NAV graph for this fund looks fairly horrendous, as it has been losing value each and every year, by utilizing principal to pay interest on the CEF.

Rates have risen significantly in 2022, with the fund’s portfolio now generating cash-flows to support a portfolio dividend of around 5%. There is still a substantial gap to fill to the distribution policy, hence expect the NAV to continue falling.

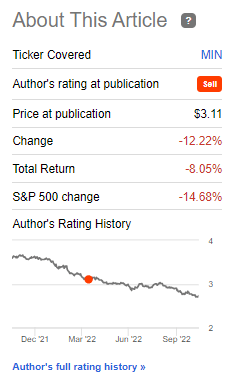

We started covering the fund in the beginning of the year, when we assigned it a Sell rating. The vehicle is down more than -12% on a price basis since our rating:

Author Rating Performance (Seeking Alpha)

The main vector behind the fund’s poor performance is represented by higher rates. Risk free rates have had a massive shift up in 2022 as the Fed is trying to contain inflation. Although the fund runs a fairly short duration, even the short and intermediate parts of the yield curve moved up significantly in 2022. With most of the rate increases now behind us, we feel the negative move in MIN is close to exhaustion. We are therefore moving from Sell to Hold on this fund.

Performance

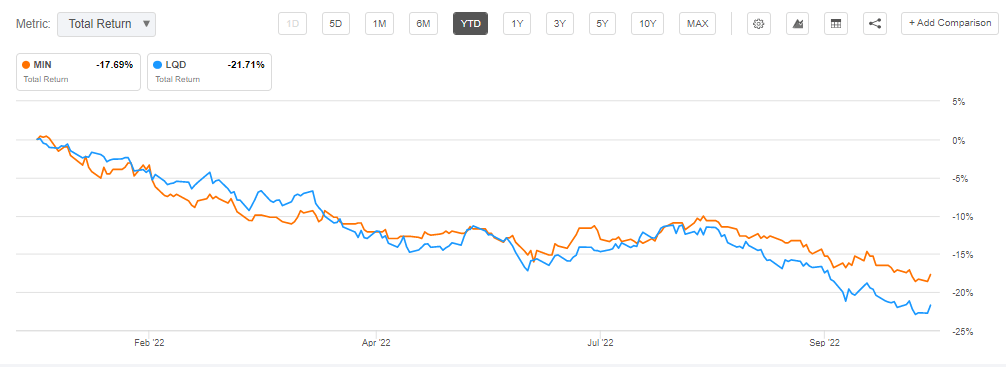

The fund is down -17% year to date, closely following the LQD performance:

YTD Total Return (Seeking Alpha)

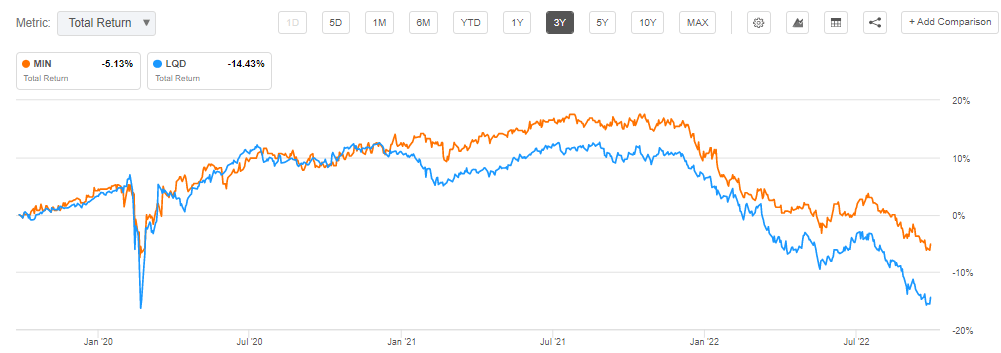

On a 3-year time frame the CEF exposes a negative performance, but manages to outperform LQD:

3Y Total Return (Seeking Alpha)

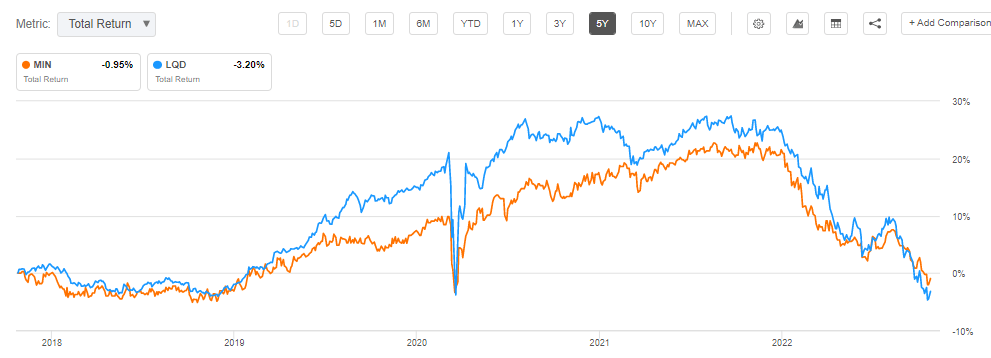

We can observe the close rates correlation on a 5-year return basis, as well as the total return profile that mirrors the LQD ETF:

5Y Total Return (Seeking Alpha)

We can see MIN generally underperforming LQD in the past 5 years, with the investment grade ETF (blue line) exhibiting a more robust historic total return (a larger upside captured in low rates environments).

Holdings

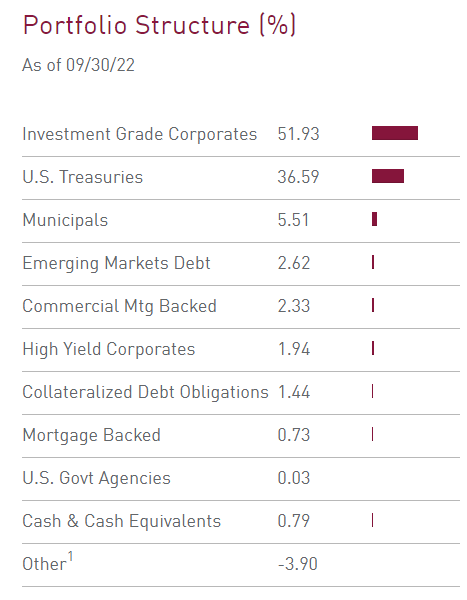

The fund is mainly focused on treasuries and investment grade bonds:

Portfolio Structure (Fund Fact Sheet)

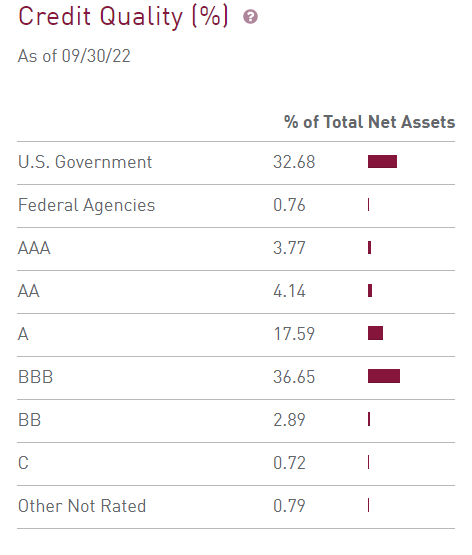

Its portfolio ratings are reflective of an investment grade vehicle:

Credit Quality (Fund Fact Sheet)

To note that the fund, for some reason, buckets U.S. Government securities in their own category, rather than the AAA bucket. A bit bizarre, because U.S. Government securities are rated AAA and should be presented as such. The only explanation we can think of here is the fact that the fund is trying to highlight that it holds 3.77% of AAA corporate bonds.

Premium / Discount to NAV

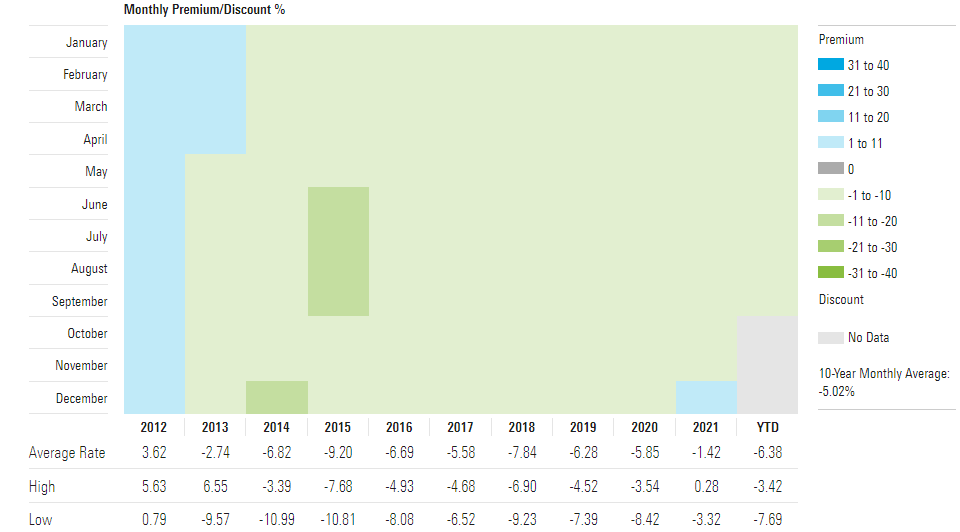

The fund has been trading at discounts to net asset value in the past decade:

Premium / Discount to NAV (Morningstar)

We think this behavior is warranted due to the over-distribution factor which is discussed in the below section. We expect the discount to NAV to persist, especially in today’s elevated rates environment, where viable alternatives exist.

NAV Performance

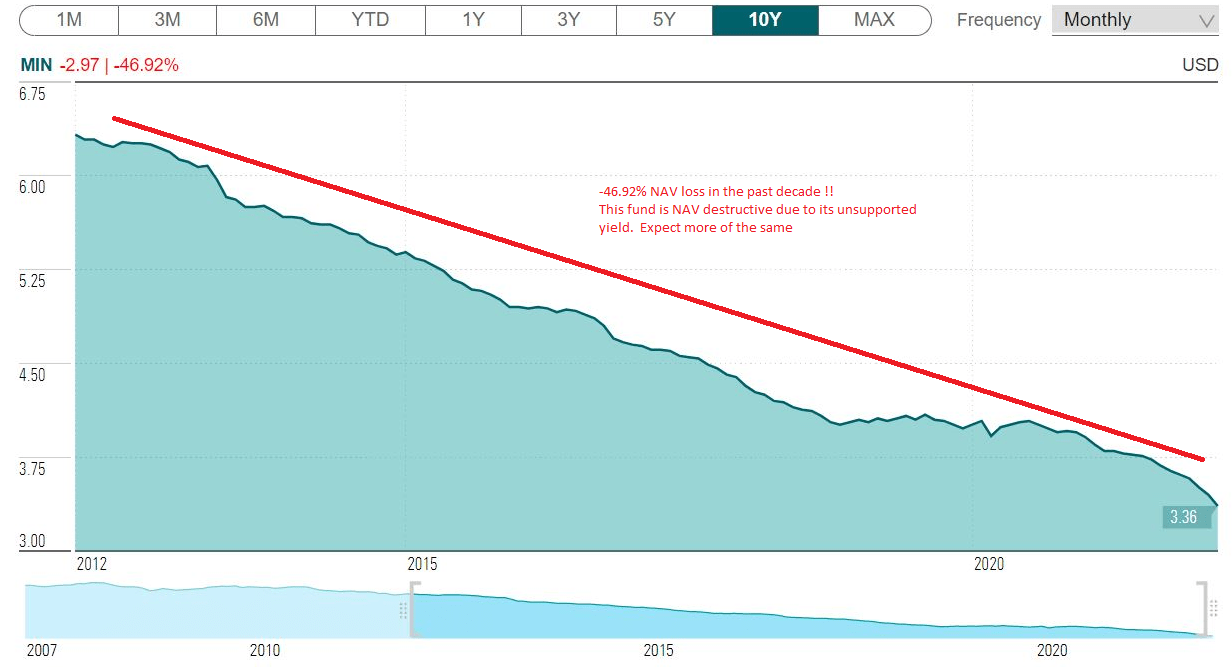

Due to the fact that the fund distributes a 9%+ yield that is unsupported by the received cash in the portfolio, what it ends up doing is paying that yield from NAV:

NAV Performance (CefConnect)

We do not like any NAV give-up above -1% since it represents a destructive management behavior and is not reflective of actual underlying assets performance or risk. In our mind, such a large discrepancy between yield and assets cash flows constitutes a marketing gimmick purely and is there to attract AUM rather than anything else. We are understanding in certain circumstances where on odd years a fund has to make a larger than normal ROC distribution due to timing issues, but on a 10-year basis, we do not want to see an annual NAV give-up above -1%. Investing in this fund means that every year 2/3rds of what you are getting is actually your own cashback.

Conclusion

MIN is a fixed income closed end fund. The vehicle focuses on investment grade bonds and treasuries. The main risk factor for this fund is represented by rates. With rates violently up in 2022, MIN has been pummeled. The CEF currently yields around 9%, but the dividend is unsupported. This is a well-known CEF for over-distribution, with its NAV having lost a tremendous amount of value in the past decade from this marketing gimmick. The current portfolio generates around 5% in coupons, and given the fact that the fund is not leveraged, do expect the NAV to keep decreasing as the fund maintains its large dividend policy. We rated the fund a Sell in the beginning of the year on the back of higher rates expectations. With most of the yield curve move behind us, we are now moving from Sell to Hold on this name.

Be the first to comment